Unlocking Your Dream Ride: The Definitive Guide to USAA Car Loan Credit Score Requirements

Unlocking Your Dream Ride: The Definitive Guide to USAA Car Loan Credit Score Requirements Carloan.Guidemechanic.com

Securing a car loan can feel like navigating a complex maze, especially when you factor in credit scores and lender-specific requirements. For military members, veterans, and their families, USAA stands out as a trusted financial partner. But what exactly does USAA look for in your credit score when you apply for an auto loan? And how can you position yourself for the best possible rates and terms?

This comprehensive guide will demystify the USAA car loan credit score landscape, offering in-depth insights, practical strategies, and expert advice. Our goal is to empower you with the knowledge to approach your USAA auto loan application with confidence, ensuring you drive away with a deal that truly benefits you.

Unlocking Your Dream Ride: The Definitive Guide to USAA Car Loan Credit Score Requirements

Understanding USAA: A Partner for the Military Community

Before diving into the specifics of credit scores, it’s essential to appreciate USAA’s unique position. The United Services Automobile Association (USAA) is more than just a bank; it’s a financial services group dedicated exclusively to serving active-duty military, veterans, and their eligible family members. This focus often translates into a deeper understanding of military life and its unique financial challenges and opportunities.

USAA offers a wide range of financial products, from insurance to banking and investments, all tailored to its specific membership. Their car loans are no exception, designed with competitive rates and member-centric features. Knowing this background helps to frame their lending approach, which, while still relying on creditworthiness, also considers the broader context of their members’ lives.

The Crucial Role of Your Credit Score in USAA Car Loans

Your credit score is arguably the most significant factor lenders consider when you apply for any type of credit, including an auto loan. It acts as a snapshot of your financial responsibility, telling lenders like USAA how likely you are to repay borrowed money on time. A higher score signals lower risk, typically leading to more favorable loan terms.

For USAA, assessing your creditworthiness through your score is a standard practice. It helps them determine not only whether to approve your loan but also the interest rate you’ll be offered. A strong credit score can translate into thousands of dollars saved over the life of your car loan, making it a critical number to understand and nurture.

What Credit Score Do You Really Need for a USAA Car Loan?

This is often the million-dollar question, and the answer, like with many lenders, isn’t a single, published number. USAA, similar to other major financial institutions, does not publicly disclose a minimum credit score requirement for its auto loans. This is primarily because lending decisions are multifaceted, taking into account a variety of factors beyond just a numerical score.

However, based on general industry standards and the experiences of countless borrowers, we can provide a realistic range. Typically, a FICO score of 660 or higher is often considered "good" enough to qualify for an auto loan from most reputable lenders, including USAA, albeit with varying interest rates.

Let’s break down what different credit score tiers generally mean for your USAA auto loan prospects:

- Excellent Credit (780-850): If your credit score falls into this range, you are considered a prime borrower. You’re highly likely to receive the most competitive interest rates and the most flexible terms from USAA. Lenders see you as a very low-risk borrower, eager to attract your business.

- Good Credit (660-779): This is where most successful USAA auto loan applicants likely fall. With a good credit score, you stand a strong chance of approval and will qualify for very good, though perhaps not the absolute lowest, interest rates. You demonstrate a solid history of managing credit responsibly.

- Fair Credit (600-659): While it might be more challenging, getting a USAA car loan with a fair credit score is often still possible. You might face slightly higher interest rates and potentially stricter terms. USAA may look more closely at other aspects of your financial profile to mitigate the perceived risk.

- Poor Credit (Below 600): Obtaining a traditional auto loan from a prime lender like USAA with a score in this range can be difficult. Approval is less likely, and if granted, the interest rates will be significantly higher, reflecting the increased risk. In such cases, alternative strategies might be necessary, which we’ll discuss later.

Based on my experience working with countless individuals navigating auto financing, while USAA is member-focused, they still operate under sound lending principles. Aiming for at least a "good" credit score (660+) significantly improves your chances of securing a favorable deal. Anything below that will require a stronger overall financial picture or a willingness to accept less ideal terms.

Factors USAA Considers Beyond Your Credit Score

While your credit score is a major player, it’s not the only factor USAA evaluates. A holistic assessment of your financial health helps them make a responsible lending decision. Understanding these additional criteria can help you strengthen your application.

Here are other key elements USAA will likely consider:

- Income and Debt-to-Income (DTI) Ratio: USAA wants to ensure you have a stable income sufficient to cover your loan payments comfortably. Your DTI ratio, which compares your total monthly debt payments to your gross monthly income, is crucial. A lower DTI (ideally below 40%) indicates you have enough disposable income to handle new debt.

- Loan-to-Value (LTV) Ratio: This ratio compares the amount you’re borrowing to the vehicle’s market value. A lower LTV, meaning you’re borrowing less relative to the car’s worth (often achieved with a larger down payment), reduces the lender’s risk and can lead to better terms.

- Down Payment: A substantial down payment demonstrates your financial commitment and reduces the amount you need to borrow. It can significantly improve your chances of approval, especially if your credit score is not in the "excellent" range.

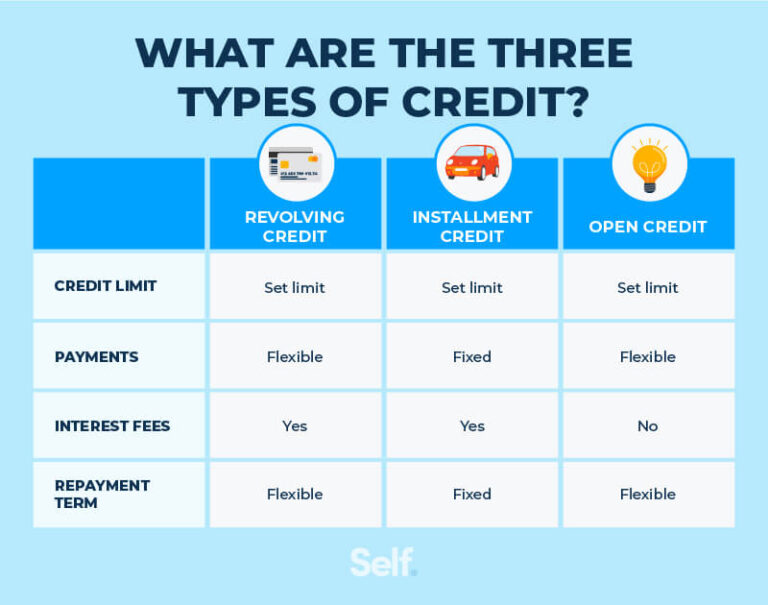

- Loan Term: The length of your loan also plays a role. Shorter loan terms (e.g., 36 or 48 months) typically come with lower interest rates but higher monthly payments, while longer terms (e.g., 60 or 72 months) offer lower monthly payments but accumulate more interest over time. USAA will assess if the chosen term is suitable for your financial situation.

- Vehicle Type and Age: The type and age of the vehicle you intend to purchase can impact the loan. Newer, more reliable vehicles often qualify for better rates than older, high-mileage cars, as they present less risk of mechanical issues that could affect your ability to repay.

- Membership History with USAA: While not explicitly a credit factor, your long-standing relationship with USAA as a member could indirectly influence their decision, especially in borderline cases. It signifies loyalty and a history of engaging with their services.

Each of these factors contributes to your overall risk profile. A strong showing in these areas can sometimes compensate for a slightly lower credit score, presenting a more appealing picture to USAA.

The USAA Car Loan Application Process: A Step-by-Step Guide

Applying for a USAA car loan is a streamlined process designed for its members. Knowing what to expect can help you prepare and move forward efficiently.

Here’s a typical overview of the steps involved:

- Determine Your Needs: Before applying, assess how much you can truly afford for a monthly car payment and the total loan amount. Consider insurance, maintenance, and fuel costs as well.

- Check Your Credit Score and Report: Obtain your free credit report from AnnualCreditReport.com and review your credit score. This gives you an accurate picture of where you stand and allows you to dispute any errors.

- Consider Pre-qualification vs. Pre-approval:

- Pre-qualification: This is a soft inquiry that doesn’t affect your credit score. It gives you an estimate of what you might qualify for, based on basic information.

- Pre-approval: This involves a hard inquiry, which may temporarily ding your credit score by a few points. However, it provides a firm offer of credit for a specific amount and interest rate, allowing you to shop for a car with confidence. Pro tip from us: Always aim for pre-approval. It puts you in a stronger negotiating position at the dealership.

- Gather Necessary Documents: Be prepared to provide documentation such as:

- Proof of identity (Driver’s License, Military ID)

- Proof of income (pay stubs, tax returns)

- Social Security Number

- Vehicle information (if you already have a specific car in mind)

- Apply Online or by Phone: USAA makes it easy to apply through their website or by calling their loan specialists. The application will ask for personal, financial, and employment information.

- Review the Offer: If approved, USAA will present you with the loan terms, including the interest rate, loan amount, and monthly payment. Carefully review all details before accepting.

- Finalize the Loan: Once you accept the offer, USAA will work with you to complete the necessary paperwork and disburse the funds, either directly to you or to the dealership.

The process is generally efficient, often with quick decisions, especially for members with strong credit profiles.

Strategies to Improve Your Credit Score for a Better USAA Car Loan

If your credit score isn’t where you want it to be, don’t despair. There are actionable steps you can take to improve it, which will not only benefit your USAA car loan application but your overall financial health.

Here are proven strategies to boost your credit score:

- Pay All Bills On Time, Every Time: Payment history is the most significant factor in your credit score (35% of FICO). Set up automatic payments or reminders to ensure you never miss a due date on credit cards, loans, or even utility bills reported to credit bureaus.

- Reduce Your Credit Card Balances: Your credit utilization ratio (how much credit you’re using versus how much you have available) accounts for 30% of your FICO score. Aim to keep this ratio below 30% across all your credit cards. Paying down balances frees up available credit and signals responsible management.

- Check Your Credit Report for Errors: Regularly review your credit reports from all three major bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. Errors can drag down your score. Dispute any inaccuracies immediately.

- Avoid Opening New Credit Accounts Unnecessarily: Each new credit application results in a hard inquiry, which can temporarily lower your score. Only apply for credit when absolutely necessary, especially in the months leading up to a major loan application.

- Don’t Close Old Credit Accounts: The length of your credit history (15% of FICO) matters. Keeping older, established accounts open, even if you don’t use them frequently, helps demonstrate a long track record of responsible credit use.

- Become an Authorized User (Cautiously): If a trusted family member with excellent credit adds you as an authorized user on their credit card, their positive payment history can reflect on your report. However, ensure they are responsible, as their missteps could also affect you.

Pro tips from us: Building credit takes time and consistency. Start early, even if you’re not planning to buy a car tomorrow. Small, consistent actions can lead to significant improvements over several months. Focus on establishing a positive payment history and managing your existing credit wisely.

Navigating USAA Car Loans with Less-Than-Perfect Credit

Even if your credit score isn’t stellar, securing a USAA car loan might still be within reach. It requires a more strategic approach and perhaps some flexibility on your part.

Common mistakes to avoid are applying to too many lenders simultaneously (which generates multiple hard inquiries), or assuming a low score means no options at all.

Here are some strategies for members with fair or poor credit:

- Consider a Co-signer: A co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. Their creditworthiness effectively backs your loan, reducing the risk for USAA. Ensure both parties understand the responsibilities, as the co-signer is equally liable for the debt.

- Make a Larger Down Payment: A substantial down payment reduces the amount you need to borrow, thereby decreasing USAA’s risk. It shows your commitment and can sometimes offset a lower credit score.

- Choose a Less Expensive Vehicle: Opting for a more affordable car means a smaller loan amount, which is easier to qualify for and more manageable to repay, especially with a higher interest rate.

- Improve Your Credit First: If time allows, dedicate a few months to actively improving your credit score using the strategies mentioned above. Even a 30-50 point increase can make a difference in your loan terms.

- Explore USAA’s Other Resources: USAA offers financial advisors and resources. They might be able to guide you on specific steps to take or alternative solutions tailored to your situation.

While USAA strives to support its members, they also have a fiduciary responsibility. Approving a loan to someone who is unlikely to repay it is not beneficial for either party. Therefore, presenting the strongest possible financial picture is always in your best interest.

Comparing USAA Car Loan Rates and Terms

Once you’ve strengthened your credit and understand the application process, comparing loan rates and terms becomes crucial. USAA is known for competitive rates, but it’s always wise to understand what makes a good deal.

- Understanding APR (Annual Percentage Rate): Don’t just look at the interest rate; focus on the APR. The APR includes the interest rate plus any fees associated with the loan, giving you the true annual cost of borrowing. A lower APR means less money paid over the life of the loan.

- Fixed vs. Variable Rates: Most auto loans come with fixed interest rates, meaning your monthly payment remains constant. Variable rates can fluctuate with market conditions, making your payments unpredictable. For stability, fixed rates are generally preferred for auto loans.

- Shorter vs. Longer Loan Terms: As discussed, shorter terms mean higher monthly payments but less interest paid overall. Longer terms mean lower monthly payments but more total interest. Calculate what you can comfortably afford each month without extending the loan unnecessarily.

- Shop Around (But Be Smart): While USAA is often a top choice for its members, it never hurts to get pre-approval offers from one or two other reputable lenders within a short timeframe (usually 14-45 days, depending on the credit scoring model). Credit bureaus typically treat multiple auto loan inquiries within this window as a single inquiry, minimizing the impact on your score. This allows you to compare offers and ensure USAA’s is truly the best for you.

For more insights into managing your finances and understanding loan terms, check out our guide on .

USAA Car Loan Pre-Approval: Your Secret Weapon

We briefly touched upon pre-approval, but its importance for securing a USAA car loan cannot be overstated. Getting pre-approved before you step foot in a dealership transforms your car buying experience.

Here’s why pre-approval is your secret weapon:

- Know Your Budget: With a pre-approval in hand, you know exactly how much you can borrow. This prevents you from falling in love with a car outside your financial reach and helps you focus your search.

- Shop with Confidence: You become a cash buyer in the eyes of the dealership. This means you can negotiate the car’s price based on its value, rather than being swayed by monthly payment schemes.

- Streamlined Dealership Experience: Dealerships often try to roll financing into the sales process, potentially adding markups or less favorable terms. With USAA pre-approval, you already have your financing secured, simplifying the transaction.

- Benchmark for Comparison: Your USAA pre-approval acts as a benchmark. If the dealership offers financing, you can compare their rates and terms directly with USAA’s. If the dealer can beat your USAA rate, great! If not, you simply stick with your pre-approved loan.

The process of getting pre-approved through USAA is straightforward and often provides a decision quickly. It’s a proactive step that puts you in control of your car buying journey.

The Power of USAA Membership for Auto Financing

Beyond competitive rates, USAA membership itself offers advantages when seeking an auto loan. Their deep understanding of military life often means a more empathetic and flexible approach to lending.

- Tailored Financial Guidance: USAA provides financial advice and resources specifically for military members and their families. This can be invaluable when planning a major purchase like a car.

- Exceptional Member Service: USAA is consistently ranked highly for its customer service. This means easier access to support and clearer communication throughout your loan application and repayment period.

- Potential for Special Offers: While not guaranteed, USAA occasionally offers special promotions or rates exclusive to its members, especially for auto loans.

Being a USAA member means you’re part of a community that understands your unique needs, making the car loan process potentially smoother and more beneficial. If you’re looking to improve your overall financial health and leverage such benefits, read our detailed post on .

FAQs about USAA Car Loans and Credit Scores

Here are answers to some common questions related to USAA car loans and credit scores:

- Does USAA use FICO or VantageScore?

USAA, like many major lenders, typically uses FICO scores, though they may review information from all three major credit bureaus (Experian, Equifax, TransUnion). - Can I get a USAA car loan if I’m a new member?

Yes, your eligibility for a USAA car loan is based on your creditworthiness and financial profile, not solely on the length of your membership. - Will applying for USAA pre-approval hurt my credit score?

Yes, a pre-approval typically involves a "hard inquiry" on your credit report, which can temporarily lower your score by a few points. However, the impact is usually minor and short-lived. - What if my credit score improves after I get a USAA loan?

If your credit score significantly improves, you might be able to refinance your USAA car loan at a lower interest rate, potentially saving you money. - Does USAA offer loans for used cars?

Yes, USAA offers loans for both new and used vehicles, often with competitive rates for both.

Conclusion: Drive Confidently with USAA

Navigating the world of car loans requires a solid understanding of your credit score and the lender’s expectations. For USAA members, the journey to securing an auto loan is often supported by a financial institution that understands and values their service. While USAA doesn’t publish a specific minimum credit score, aiming for a "good" credit score of 660 or higher will significantly enhance your chances of approval and unlock the most favorable rates.

Remember, your credit score is just one piece of the puzzle. Your income, debt-to-income ratio, down payment, and the vehicle itself all play vital roles. By taking proactive steps to improve your credit, getting pre-approved, and understanding the entire application process, you can confidently approach USAA for your next car loan. Drive away knowing you’ve secured a deal that’s not just competitive, but also respects your service and financial well-being.