Unlocking Your Dream Ride: The Essential Credit Score for a $40,000 Car Loan

Unlocking Your Dream Ride: The Essential Credit Score for a $40,000 Car Loan Carloan.Guidemechanic.com

Securing a car loan, especially for a significant amount like $40,000, is a major financial milestone for many. Whether you’re eyeing a luxury sedan, a robust SUV for your growing family, or a high-performance vehicle, the journey often begins long before you step onto the dealership lot. It starts with your credit score – your financial passport that determines not just whether you get approved, but also the terms of your loan.

As an expert blogger and professional SEO content writer, I’ve seen firsthand how crucial understanding your credit score is in the car buying process. This comprehensive guide will demystify the credit score requirements for a $40,000 car loan, providing you with the knowledge and strategies to navigate the application process confidently and secure the best possible deal. We’ll dive deep into what lenders look for, how to prepare your finances, and common pitfalls to avoid.

Unlocking Your Dream Ride: The Essential Credit Score for a $40,000 Car Loan

Understanding the $40,000 Car Loan Landscape

A $40,000 car loan represents a substantial financial commitment. It’s not just about the vehicle itself; it’s about the long-term impact on your budget, your credit profile, and your financial freedom. Lenders view a loan of this size as a higher risk compared to smaller amounts, which naturally amplifies the importance of your creditworthiness.

Many factors contribute to a lender’s decision, but your credit score stands out as the primary indicator of your financial responsibility. It’s a snapshot of your past borrowing behavior, and it gives lenders a quick, standardized way to assess the likelihood of you repaying your debt. For a $40,000 car, a strong credit score can literally save you thousands of dollars over the life of the loan in reduced interest payments.

The Credit Score: Your Financial Passport to Auto Financing

Before we delve into specific score ranges, let’s clarify what a credit score is and why it holds so much weight. Essentially, a credit score is a three-digit number, typically ranging from 300 to 850, that summarizes your credit risk. The most commonly used models are FICO and VantageScore, both of which evaluate similar aspects of your credit history.

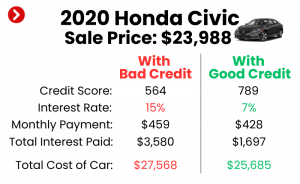

For a $40,000 car loan, lenders use this score to quickly gauge your reliability as a borrower. A higher score signals lower risk, which translates to better loan terms for you. This means lower interest rates, more flexible payment schedules, and potentially a larger choice of lenders willing to work with you. Conversely, a lower score suggests a higher risk, often leading to higher interest rates, stricter terms, or even denial.

Based on my experience, many people underestimate the direct correlation between their credit score and the total cost of their car loan. A few points difference in your score can translate into hundreds or even thousands of dollars saved on interest over a typical 5-7 year loan term. This is why proactive credit management is so vital.

What’s a "Good" Credit Score for a $40,000 Car Loan?

While there’s no single "magic number," lenders generally categorize credit scores into ranges, each associated with different levels of risk and corresponding loan offers. For a significant loan like $40,000, lenders prefer to see scores that demonstrate a strong history of responsible borrowing. Let’s break down what these ranges mean for your car loan application:

1. Excellent Credit (780+)

If your credit score falls into the "Excellent" category (typically 780 and above), you are in the prime position for securing a $40,000 car loan. Lenders view you as a highly reliable borrower with minimal risk.

With an excellent score, you can expect to qualify for the absolute best interest rates available, often advertised as the "lowest APRs." You’ll likely have a wide selection of lenders competing for your business, offering favorable terms, and potentially requiring a smaller down payment. This level of credit gives you significant leverage during negotiations, allowing you to secure the most affordable financing possible for your dream car.

2. Very Good Credit (740-779)

A "Very Good" credit score is also highly desirable for a $40,000 car loan. Borrowers in this range are still considered low-risk and will typically receive very competitive interest rates and favorable loan terms.

While you might not get the absolute rock-bottom rates reserved for the 780+ club, you will still access excellent financing options. Lenders will be eager to approve your application, and you’ll find the process smooth and straightforward. This score range demonstrates consistent financial responsibility, making you a very attractive candidate for substantial auto loans.

3. Good Credit (670-739)

This is where a significant portion of the population falls, and it’s a perfectly viable range for obtaining a $40,000 car loan. With a "Good" credit score, you are generally seen as a responsible borrower, though perhaps with a slightly higher risk profile than those in the "Very Good" or "Excellent" categories.

You can still expect approval for a $40,000 loan, but your interest rates might be a bit higher than those with superior scores. Lenders might also look more closely at other aspects of your financial profile, such as your income stability and debt-to-income ratio. The key here is to shop around for lenders, as rates can vary. Pro tips from us: credit unions often offer competitive rates for borrowers in this range.

4. Fair Credit (580-669)

Securing a $40,000 car loan with a "Fair" credit score presents more of a challenge, but it’s not impossible. Lenders view borrowers in this range as moderate risk, which means they’ll be more cautious.

You will likely face higher interest rates to compensate the lender for the increased risk. Approval might also require a larger down payment, a co-signer, or stricter loan terms. It’s crucial to be realistic about your options and thoroughly explore all avenues, including specialized lenders who work with fair credit. While you might get approved, carefully evaluate the total cost of the loan before committing.

5. Poor Credit (Below 580)

Obtaining a $40,000 car loan with a "Poor" credit score is exceptionally difficult and often comes with very unfavorable terms. Lenders consider borrowers in this category to be high-risk, making them hesitant to lend such a significant amount.

If approved, you would likely face extremely high interest rates, short repayment periods, and potentially require a substantial down payment or a strong co-signer. In many cases, it might be more prudent to focus on improving your credit score before seeking such a large loan. This approach can save you significant money and stress in the long run.

Beyond the Score: Other Factors Lenders Consider

While your credit score is undeniably important, it’s not the only factor lenders evaluate. For a $40,000 car loan, they’ll conduct a holistic review of your financial health to ensure you can comfortably manage the payments. Understanding these additional criteria can significantly boost your chances of approval.

1. Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is a critical metric. It’s calculated by dividing your total monthly debt payments by your gross monthly income. Lenders use DTI to assess your ability to take on additional debt.

For a $40,000 loan, a DTI of 36% or lower is generally preferred, though some lenders might go higher depending on other factors. A high DTI suggests you might already be overextended, making lenders hesitant to add another significant monthly payment to your obligations.

2. Payment History

This is the most impactful component of your credit score and a direct indicator of your reliability. Lenders want to see a consistent history of on-time payments across all your accounts – credit cards, previous loans, and mortgages.

Any missed or late payments, especially recent ones, can raise red flags and make lenders question your ability to manage a $40,000 car loan responsibly. A clean payment history shows you are disciplined and dependable.

3. Credit Utilization

Your credit utilization ratio is the amount of credit you’re currently using compared to your total available credit. For example, if you have a $10,000 credit limit and you’ve used $3,000, your utilization is 30%.

Lenders prefer to see this ratio below 30% on all your revolving accounts. High utilization suggests you might be over-reliant on credit, which can be a red flag for a new, large loan. Keeping your balances low demonstrates responsible credit management.

4. Length of Credit History

The longer your credit history, the better. A long history with various types of credit (credit cards, installment loans) allows lenders to see a more comprehensive picture of your borrowing habits over time.

A mature credit profile, showing consistent good behavior for several years, reassures lenders that you are a seasoned and reliable borrower. If you have a relatively short credit history, lenders might be more cautious.

5. Income Stability and Employment History

Lenders need assurance that you have a steady, sufficient income to make your monthly car payments. They will typically ask for proof of income, such as pay stubs, W-2s, or tax returns.

A stable employment history, showing you’ve been with the same employer for a significant period (e.g., two years or more), indicates financial stability. Frequent job changes or gaps in employment can make lenders wary.

6. Down Payment

Making a significant down payment on a $40,000 car loan is a powerful way to reduce lender risk. A larger down payment means you’re borrowing less money, and you have more equity in the vehicle from day one.

This reduces the lender’s exposure and can sometimes offset a less-than-perfect credit score, potentially leading to better interest rates. Pro tips from us: Aim for at least 10-20% down for a new car, and even more for a used one.

7. Vehicle Type and Age

The type and age of the car you’re buying also play a role. Lenders consider the vehicle as collateral for the loan. Newer, more reliable cars with a strong resale value are generally seen as lower risk.

Older, higher-mileage vehicles might be harder to finance for a $40,000 loan, as their value depreciates more rapidly, and they might pose a higher risk of mechanical issues. The loan-to-value (LTV) ratio is crucial here – lenders want to ensure the loan amount doesn’t significantly exceed the car’s value.

Preparing Your Credit for a $40,000 Car Loan: Actionable Steps

Proactive preparation is key to securing favorable terms for a $40,000 car loan. Don’t wait until you’re at the dealership to think about your credit. Here’s how to get your finances in prime shape:

1. Check Your Credit Report and Score Regularly

This is the absolute first step. You should know exactly where you stand. Obtain your free credit reports from AnnualCreditReport.com, which provides reports from all three major bureaus (Equifax, Experian, TransUnion).

Review each report meticulously for any errors or inaccuracies. Common mistakes to avoid are not checking all three reports, as information can vary between them. If you find discrepancies, dispute them immediately with the respective credit bureau; this can take time, so start early. For a deeper dive into managing your credit reports, you might find our article on Your Ultimate Guide to Checking and Fixing Your Credit Report helpful. (Simulated Internal Link)

2. Improve Your Credit Score

Once you know your score, if it’s not where you want it to be, take steps to improve it. Even small improvements can lead to significant savings on a $40,000 loan.

- Pay All Bills On Time, Every Time: Payment history is the most important factor. Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce Credit Card Balances: Pay down your credit card debt to lower your credit utilization ratio. Aim for below 30% on each card, and ideally below 10% for the best impact.

- Avoid New Credit Applications: Resist the urge to open new credit cards or take out other loans in the months leading up to your car loan application. Each new application can result in a hard inquiry, which temporarily dings your score.

- Become an Authorized User (Carefully): If a trusted family member with excellent credit adds you as an authorized user to one of their long-standing, well-managed credit accounts, it can sometimes boost your score. Ensure they maintain good habits, as their mistakes could impact you.

- Consider a Secured Credit Card: If your credit score is low, a secured credit card can be a great way to build positive credit history. You put down a deposit, which becomes your credit limit, and then use it like a regular credit card, paying it off each month. For more detailed strategies, check out our guide on 10 Proven Strategies to Boost Your Credit Score Fast. (Simulated Internal Link)

3. Save for a Substantial Down Payment

As discussed, a larger down payment reduces the amount you need to borrow and makes you a more attractive borrower. For a $40,000 car, aiming for a down payment of $4,000 to $8,000 (10-20%) is a strong strategy.

Not only does it reduce your monthly payments and overall interest, but it also helps prevent you from being "upside down" on your loan (owing more than the car is worth) early in the loan term.

4. Get Pre-Approved Before Shopping

Pre-approval is a game-changer. It means a lender has already reviewed your credit and financial information and is willing to lend you a specific amount at a particular interest rate.

This gives you a clear budget, allows you to negotiate with dealers as a cash buyer, and removes the stress of financing at the dealership. Common mistakes to avoid are only getting pre-approved through the dealer, as they may not offer the best rates. Shop around with banks, credit unions, and online lenders for your pre-approval.

5. Budget Realistically

Before you even think about the car, determine what you can truly afford. Factor in not just the monthly loan payment, but also insurance, fuel, maintenance, and potential repair costs.

A $40,000 car loan often comes with significant associated expenses. Use an online car loan calculator to estimate payments at various interest rates and loan terms to ensure it fits comfortably within your monthly budget.

Navigating the Application Process

Once your credit is in order and you’ve saved for a down payment, it’s time to apply for your $40,000 car loan. Here’s how to approach it strategically:

1. Gather All Necessary Documents

Lenders will require various documents to verify your identity, income, and residence. Be prepared with:

- Government-issued ID (driver’s license)

- Proof of income (pay stubs, W-2s, tax returns)

- Proof of residence (utility bill, lease agreement)

- Social Security Number

- Information about the vehicle you intend to purchase (if you have one in mind)

Having these ready streamlines the application process and shows you are organized.

2. Shop Around for Lenders

Don’t settle for the first offer you receive, especially from a dealership. Banks, credit unions, and online lenders all offer competitive rates. Apply to several lenders within a short window (typically 14-45 days, depending on the credit scoring model).

Multiple inquiries for the same type of loan within this timeframe will generally be treated as a single hard inquiry, minimizing the impact on your credit score. This allows you to compare offers without significant credit damage.

3. Understand Loan Terms (APR, Loan Length)

Always look at the Annual Percentage Rate (APR), which includes the interest rate plus any fees, giving you the true cost of borrowing. Also, consider the loan length.

While a longer loan term (e.g., 72 or 84 months) can lower your monthly payments, it significantly increases the total interest paid over the life of the loan. Aim for the shortest term you can comfortably afford to minimize overall cost.

What if Your Credit Score Isn’t Perfect?

Even if your credit score isn’t in the excellent range, there are still options for securing a $40,000 car loan. It might require more effort and some compromises, but it’s not a lost cause.

1. Consider a Co-signer

A co-signer with excellent credit can significantly improve your chances of approval and help you secure a better interest rate. The co-signer essentially guarantees the loan, meaning they are equally responsible for repayment if you default.

This reduces the lender’s risk. However, ensure both parties understand the implications; if you miss payments, it negatively impacts both your credit scores.

2. Secured Loan Options

Some lenders might offer a secured loan, where you use an asset (like savings or another vehicle) as collateral. This is less common for car loans, as the car itself is typically the collateral, but in some cases, it might be an option for borrowers with lower scores.

Alternatively, some lenders offer auto loans that are secured by the vehicle being purchased, but with stricter terms if your credit is poor.

3. Adjust Your Expectations: Smaller Loan or Less Expensive Car

If a $40,000 loan is proving too difficult or expensive with your current credit, consider adjusting your budget. A $30,000 or $25,000 car might be more attainable with a fair credit score, allowing you to build positive payment history.

You can always upgrade to your dream car later once your credit has improved. Realistic expectations are key to avoiding financial strain.

4. Wait and Improve Your Credit

Sometimes, the best strategy is to wait. Dedicate a few months to actively improving your credit score by paying down debt, making on-time payments, and addressing any errors on your report.

This long-term approach can lead to significantly better loan terms, saving you thousands of dollars over the loan’s duration. Pro tips from us: Even a 50-point increase can make a huge difference in APR.

Common Mistakes to Avoid When Applying for a $40,000 Car Loan

Based on my experience, many aspiring car owners make preventable errors that can jeopardize their loan approval or lead to overpaying. Here are common mistakes to steer clear of:

- Not Checking Your Credit First: Going into the application process blind is a major misstep. You won’t know what rates to expect or if you need to address any issues.

- Applying Everywhere at Once Indiscriminately: While shopping around is good, submitting dozens of applications without research can lead to numerous hard inquiries, temporarily harming your score. Focus on a few reputable lenders.

- Ignoring the Total Cost (APR, Fees): Focusing solely on the monthly payment can be deceiving. A low monthly payment achieved by stretching the loan term or accepting a high APR means you’ll pay significantly more in the long run. Always look at the APR and total interest paid.

- Stretching the Loan Term Too Long: While an 84-month loan might offer lower monthly payments for a $40,000 car, you’ll pay substantially more in interest and risk being "upside down" on your loan for a longer period.

- Buying More Car Than You Can Afford: It’s easy to get caught up in the excitement of a new vehicle. However, overextending yourself financially can lead to stress, missed payments, and damage to your credit. Stick to your budget.

- Falling for "Zero Down" Traps: While tempting, "zero down" offers often come with higher interest rates or other hidden costs. A down payment is almost always a good idea, especially for a large loan like $40,000.

Based on My Experience: The Realities of a $40,000 Car Loan

Navigating the world of auto financing for a significant purchase like a $40,000 vehicle truly underscores the value of financial preparedness. Based on my experience in analyzing countless credit profiles and loan applications, the single biggest differentiator for securing an excellent deal isn’t just a high credit score, but a holistic understanding of how lenders view your financial picture. It’s about showing consistency, responsibility, and foresight.

The peace of mind that comes with knowing you’ve secured the best possible interest rate, rather than settling for a higher one due to a rushed application or unaddressed credit issues, is invaluable. It directly translates into hundreds, if not thousands, of dollars saved over the lifetime of your loan. Conversely, the hidden costs of a poor credit score on a $40,000 loan can be staggering, turning an exciting purchase into a long-term financial burden. This is why investing time upfront to optimize your credit profile and understand the lending landscape is not just recommended, it’s essential.

For more information on understanding and managing your credit, a great external resource is the Consumer Financial Protection Bureau (CFPB) website, which offers unbiased advice on various financial topics including credit reports and scores. You can visit their site at consumerfinance.gov.

Conclusion: Drive Confidently Towards Your $40,000 Car Loan

Securing a $40,000 car loan requires more than just a desire for a new vehicle; it demands financial savvy and strategic planning. Your credit score is the cornerstone of this process, directly influencing your approval chances and the all-important interest rate. By understanding what constitutes a "good" credit score, addressing other crucial factors like DTI and income stability, and taking proactive steps to prepare your finances, you put yourself in the driver’s seat.

Remember, a little effort upfront can lead to significant savings and a smoother car-buying experience. Check your credit, dispute errors, work to improve your score, save for a healthy down payment, and shop around for the best rates. With this comprehensive guide, you’re well-equipped to confidently pursue your $40,000 car loan and drive away with a deal that makes financial sense for you.