Unlocking Your Dream Ride: The Ultimate Guide to 100% Car Loans (Zero Down Payment Auto Financing)

Unlocking Your Dream Ride: The Ultimate Guide to 100% Car Loans (Zero Down Payment Auto Financing) Carloan.Guidemechanic.com

Getting behind the wheel of a new car is an exciting prospect. For many, the biggest hurdle isn’t choosing the perfect model, but rather finding the upfront cash for a down payment. This is where the concept of a 100% car loan, often referred to as a zero down payment car loan or full financing car loan, comes into play. It promises to put you in your desired vehicle without needing a single dollar out of your pocket initially.

But is a 100% car loan too good to be true? While incredibly appealing, it’s a financial product that comes with its own set of advantages and disadvantages. As an expert blogger and professional in auto financing, I’m here to guide you through every aspect of securing a car loan without down payment, helping you make an informed decision. This comprehensive guide will delve deep into what it means, who it’s for, and how to navigate the process successfully.

Unlocking Your Dream Ride: The Ultimate Guide to 100% Car Loans (Zero Down Payment Auto Financing)

Understanding the 100% Car Loan Concept

Let’s start by demystifying what a 100% car loan truly entails. In simple terms, it’s an auto financing option where the lender covers the entire purchase price of the vehicle, including any applicable taxes and fees, without requiring an initial monetary contribution from you, the buyer. This means you don’t need to save up for a down payment, allowing you to drive off the lot sooner.

Traditionally, car loans involve a down payment, typically ranging from 10% to 20% of the vehicle’s price. This upfront payment reduces the total amount you need to borrow, thereby lowering your monthly payments and the overall interest paid. A car loan without down payment, however, bypasses this initial requirement entirely, rolling the full cost into your loan principal.

Why do lenders offer these types of loans? In a highly competitive auto market, offering full financing car loan options helps lenders attract a broader range of customers. For borrowers with excellent credit and stable income, it can be a convenient and flexible way to acquire a vehicle. However, it’s also a product where lenders carefully assess risk, as they are fronting the entire cost of the depreciating asset.

The Advantages of a 100% Car Loan

Opting for a zero down payment car loan can be highly beneficial in several scenarios. Understanding these advantages is crucial for determining if this financing route aligns with your personal financial situation.

1. Immediate Accessibility to a Vehicle

One of the most significant benefits of a 100% car loan is the ability to acquire a vehicle without immediate savings. If you need a car urgently – perhaps your old one broke down, or you’ve moved to a new area without reliable public transport – waiting to save for a down payment simply isn’t an option. This loan allows you to meet your transportation needs quickly.

2. Enhanced Financial Flexibility

With a no money down car loan, your savings remain intact. This means you can keep your cash reserves available for other important financial needs. Whether it’s building your emergency fund, making other investments, or addressing unexpected expenses, retaining your liquidity offers a valuable layer of financial security. You avoid tying up a significant sum in a depreciating asset.

3. Quicker Purchase Process

The time-consuming process of saving for a substantial down payment is completely bypassed. If you qualify, you can move from browsing to owning much faster. This streamlined approach can be particularly appealing for those who value efficiency and want to avoid prolonged financial planning for an initial lump sum.

4. Convenience and Simplicity

Often, dealerships or financial institutions that offer 100 percent car loan options strive to make the process as seamless as possible. They might bundle financing, insurance, and the vehicle purchase into a single, convenient package. This can reduce the administrative burden on the buyer, making the overall experience smoother.

The Disadvantages and Potential Pitfalls

While the allure of a zero down payment car loan is strong, it’s essential to be aware of the potential drawbacks. These loans aren’t without their risks and can lead to higher long-term costs if not approached carefully.

1. Higher Monthly Payments

Since you’re financing the entire cost of the car, the principal amount of your loan will be significantly larger compared to a loan with a down payment. This directly translates to higher monthly payments. It’s crucial to ensure these increased payments fit comfortably within your budget without straining your finances.

2. More Interest Paid Overall

A larger loan principal, especially when combined with a longer loan term, means you will pay more in total interest over the life of the loan. Even a seemingly small difference in the interest rate can add up to thousands of dollars over five or six years. Always calculate the total cost of the loan, not just the monthly payment.

3. Risk of Negative Equity (Being Upside Down)

This is perhaps the most significant risk associated with 100% car loans. Negative equity, often called being "upside down" on your loan, occurs when the outstanding balance of your loan is greater than the current market value of your vehicle. Cars depreciate rapidly, especially new ones, losing a significant portion of their value the moment they’re driven off the lot.

With a no money down car loan, you start with zero equity. If your car depreciates faster than you pay down the loan, you can quickly find yourself in a negative equity position. This becomes problematic if your car is totaled in an accident (your insurance payout might not cover the loan balance) or if you want to trade it in early. Pro Tip: Always understand the depreciation rates for your chosen vehicle and consider Gap Insurance, which we’ll discuss later.

4. Stricter Eligibility Requirements

Lenders view full financing car loans as higher risk because they have more capital invested without an initial buyer contribution. Consequently, they often impose stricter eligibility criteria. This typically means you’ll need an excellent credit score, a stable income, and a low debt-to-income ratio to qualify for favorable terms.

5. Limited Vehicle Options

Not all vehicles or dealerships will offer 100 percent car loan options. Lenders might prefer to offer full financing on newer, more reliable vehicles that hold their value better, as this reduces their risk. This could limit your choices, especially if you’re looking at older or less common models.

Who is a 100% Car Loan For?

While attractive, a 100% car loan isn’t suitable for everyone. It’s a specific financial tool that best serves certain individuals or circumstances.

- Individuals with Excellent Credit Scores: If you have a stellar credit history (typically 700+), you are the prime candidate. Lenders will be more willing to offer you a car loan without down payment at competitive interest rates because your creditworthiness signals a low risk of default.

- Those with Stable and High Income: A consistent, substantial income demonstrates your ability to manage the higher monthly payments associated with full financing. Lenders look for a low debt-to-income ratio to ensure you’re not overextending yourself.

- People Who Prioritize Cash Liquidity: If you prefer to keep your savings liquid for emergencies, investments, or other financial goals, a zero down payment car loan allows you to do so. This can be a strategic choice for savvy financial planners.

- First-Time Car Buyers with Limited Savings: While caution is advised due to the risks, a 100% car loan can be a gateway for young professionals or recent graduates who need a car but haven’t had time to build significant savings. They must, however, have strong credit and income.

- Individuals Needing a Vehicle Urgently: As mentioned, if an unforeseen event necessitates an immediate car purchase and you lack a down payment, this option can provide a quick solution.

Key Factors Affecting Your 100% Car Loan Approval

Securing a 100% car loan is not just about wanting one; it’s about meeting stringent lender requirements. Several critical factors will influence your approval chances and the terms you receive.

1. Your Credit Score and History

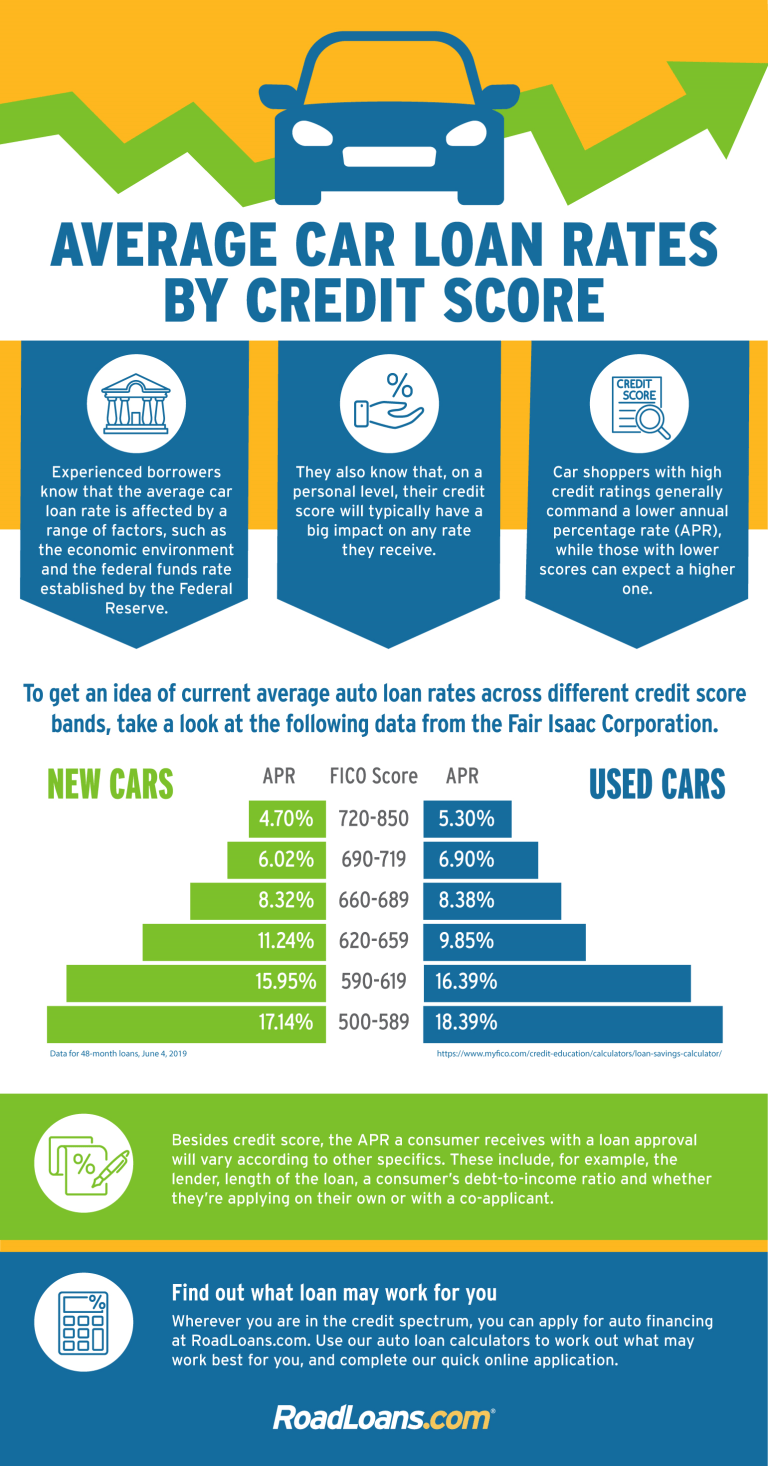

This is arguably the most crucial factor. Lenders use your credit score to assess your reliability as a borrower. For a zero down payment car loan, they need strong assurance that you will repay the full amount. Based on my experience, a credit score above 700 is often considered ideal for securing the best terms on 100% financing, with scores above 750 opening the doors to even more favorable rates. A solid credit history demonstrating timely payments on previous debts is equally important.

2. Income and Employment Stability

Lenders want to see a consistent and sufficient income stream to cover your monthly car payments, along with all your other financial obligations. They will typically ask for proof of employment, such as pay stubs, W-2s, or tax returns. A stable employment history, ideally with the same employer for several years, reassures lenders of your financial reliability.

3. Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer a low DTI, as it indicates you have enough disposable income to comfortably manage new loan payments. For a full financing car loan, where payments are higher, a low DTI becomes even more critical for approval.

4. Loan-to-Value (LTV) Ratio

The LTV ratio compares the amount you want to borrow to the appraised value of the vehicle. For a 100% car loan, your LTV ratio is at its maximum (100% or slightly higher if fees are rolled in). Lenders are cautious with high LTVs, as it increases their risk if you default. They’ll scrutinize the car’s value and your ability to repay even more closely.

5. Vehicle Choice

The type of vehicle you intend to purchase can also impact approval. Lenders generally prefer to finance newer, more reliable cars that hold their value well. This is because these vehicles represent less risk to them in case of repossession, as they can recoup more of their losses. High-end luxury cars or very old vehicles might be harder to get 100% financing for.

6. Co-signer (Optional but Helpful)

If your credit score or income isn’t strong enough on its own, a co-signer with excellent credit and stable finances can significantly improve your chances of approval. A co-signer essentially guarantees the loan, taking on equal responsibility for repayment if you default. This reduces the lender’s risk.

Steps to Secure a 100% Car Loan

Navigating the auto financing landscape can seem daunting, but with a clear plan, securing a car loan without down payment becomes manageable. Here’s a step-by-step guide:

1. Check Your Credit Score and Report

Before you even start looking at cars, know where you stand financially. Obtain your free credit reports from the major credit bureaus (Experian, Equifax, TransUnion) and check your score. Look for any errors and address them. This initial check will give you a realistic idea of your chances and help you target appropriate lenders.

2. Determine Your Budget (Beyond the Loan Payment)

While a 100% car loan covers the purchase price, remember there are other costs of car ownership. Factor in insurance premiums (which can be higher for newer, fully financed cars), registration fees, maintenance, fuel, and potential repair costs. A comprehensive budget ensures you can afford the car long-term, not just the monthly payment.

3. Get Pre-Approved from Multiple Lenders

Don’t limit yourself to dealership financing initially. Apply for pre-approval from various financial institutions, including banks, credit unions, and online lenders. This allows you to compare interest rates and loan terms without commitment. Pro Tip: Pre-approval gives you significant bargaining power at the dealership, as you walk in knowing your financing options and an approved budget.

4. Gather Necessary Documents

Lenders will require documentation to verify your identity, income, and residency. Prepare these in advance to expedite the process:

- Government-issued ID (driver’s license)

- Proof of income (pay stubs, W-2s, tax returns)

- Proof of residency (utility bill)

- Proof of insurance (you’ll need this before driving off)

5. Research and Choose Your Vehicle

With your pre-approval in hand and a clear budget, research cars that fit your needs and financial parameters. Remember that lenders might prefer to offer full financing car loan options on newer, more reliable models. Focus on the total price of the vehicle, not just the monthly payment.

6. Negotiate with the Dealership

When you’re at the dealership, focus on negotiating the total purchase price of the vehicle first. Only after you’ve agreed on a price should you discuss financing options. You can use your pre-approved offer as leverage to ensure the dealership’s financing is competitive. Be wary of add-ons that inflate the price.

7. Read the Fine Print Carefully

Before signing anything, meticulously read all loan documents. Understand the interest rate, loan term, total amount repayable, any penalties for early repayment, and all fees. If anything is unclear, ask for clarification. Don’t rush this critical step.

Common Mistakes to Avoid When Getting a 100% Car Loan

Even with the best intentions, borrowers can fall into traps when seeking a zero down payment car loan. Being aware of these common mistakes can save you significant financial heartache.

- Not Checking Your Credit Score: Skipping this vital first step means you’re going into negotiations blind. You won’t know what kind of rates to expect, leaving you vulnerable to unfavorable offers.

- Focusing Only on Monthly Payments: Dealerships often emphasize low monthly payments. However, this can be achieved by extending the loan term, which means you pay significantly more interest over time. Always consider the total cost of the loan.

- Skipping Pre-Approval: Relying solely on dealership financing limits your options and negotiating power. Pre-approval from an independent lender puts you in a stronger position.

- Not Budgeting for All Ownership Costs: A 100% car loan covers the car’s price, but insurance, registration, maintenance, and fuel are substantial ongoing expenses. Failing to budget for these can lead to financial strain.

- Ignoring the Risk of Negative Equity: Many borrowers overlook the potential of being "upside down" on their loan. This can have serious consequences if your car is totaled or if you need to sell it before the loan is significantly paid down.

- Impulsive Buying: The excitement of a new car, especially with no money down, can lead to hasty decisions. Take your time, compare options, and avoid buying a car you can’t truly afford long-term.

- Not Comparing Multiple Offers: Accepting the first loan offer you receive is a common mistake. Always compare terms from at least three different lenders to ensure you’re getting the most competitive rate.

Alternatives to a 100% Car Loan

While a 100% car loan can be a good option for some, it’s not the only path to car ownership. Exploring alternatives can sometimes lead to a more financially sound decision, especially if you’re concerned about the potential downsides.

1. Saving for a Down Payment

The traditional approach remains one of the most financially responsible. Saving even a small down payment (10-20%) significantly reduces your loan principal, lowers monthly payments, and decreases the total interest paid. It also creates immediate equity in your vehicle, mitigating the risk of negative equity. For more tips on managing your finances for such a goal, you might find our article on "Understanding Your Credit Score for Better Loan Approvals" (Internal Link Placeholder) helpful.

2. Purchasing a Used Car

Used cars often come with a lower purchase price and have already undergone their most significant depreciation. This means lower loan amounts, smaller payments, and less risk of negative equity. With proper research, you can find reliable used vehicles that offer excellent value. Consider exploring "The Smart Buyer’s Guide to Used Cars" (Internal Link Placeholder) for more insights.

3. Leasing a Car

Leasing is a different form of auto financing where you essentially rent a car for a set period (typically 2-4 years) and then return it. You don’t own the car, but monthly payments are generally lower than loan payments for a new vehicle. It’s a good option if you like driving new cars frequently and don’t mind not building equity.

4. Improving Your Credit Score First

If your credit score isn’t in the "excellent" range, taking time to improve it before applying for any car loan, especially a 100% car loan, can yield significant savings. A higher credit score qualifies you for lower interest rates, which can save you thousands over the life of the loan. This might involve paying down existing debts or correcting errors on your credit report.

Pro Tips for Smart Auto Financing (Even with a 100% Loan)

Even if you choose a zero down payment car loan, there are strategies you can employ to make it a smarter financial move.

- Consider a Shorter Loan Term: While it means higher monthly payments, a shorter loan term (e.g., 48 months instead of 72) drastically reduces the total interest you pay and helps you build equity faster, lessening the negative equity risk.

- Refinance Later: If your credit score improves significantly after you’ve taken out the loan, or if interest rates drop, consider refinancing your car loan. This could secure you a lower interest rate, reducing your monthly payments or the overall cost of the loan.

- Invest in Gap Insurance: This is almost a non-negotiable for a 100% car loan. Gap insurance covers the "gap" between what your standard auto insurance pays out if your car is totaled or stolen and the remaining balance on your loan. Without it, you could be left owing money on a car you no longer possess.

- Avoid Unnecessary Add-ons: Dealerships often try to upsell you on extended warranties, paint protection, fabric guards, and other accessories. While some might be useful, many are overpriced and can inflate your loan amount, further increasing your interest payments. Be discerning.

- Regularly Review Your Loan: Stay informed about your loan balance and how much equity you’ve built. Understanding your financial position with the car can help you make better decisions down the road, whether it’s trading in, selling, or refinancing. For more general advice on auto loans and responsible borrowing, you can refer to trusted external resources like Investopedia’s guide on auto loans .

Conclusion

A 100% car loan can be a powerful tool, providing immediate access to a vehicle without the need for an upfront down payment. For individuals with excellent credit, stable income, and a clear understanding of the financial implications, it can be a convenient and flexible financing solution. However, it’s crucial to approach these loans with caution, fully understanding the potential for higher overall costs and the significant risk of negative equity.

By thoroughly checking your credit, budgeting wisely, getting pre-approved, and avoiding common pitfalls, you can navigate the process effectively. Remember, the goal is not just to get a car, but to do so in a way that aligns with your long-term financial health. Weigh the pros and cons carefully, consider all alternatives, and make an informed decision that puts you in the driver’s seat of your financial future, as well as your dream car.