Unlocking Your Dream Ride: The Ultimate Guide to a $26,000 Car Loan

Unlocking Your Dream Ride: The Ultimate Guide to a $26,000 Car Loan Carloan.Guidemechanic.com

Securing a car loan is a significant financial decision, and if you’re considering financing a vehicle around the $26,000 mark, you’re in a common position. This isn’t just about finding the cheapest car; it’s about understanding the entire process, from preparing your finances to managing your loan effectively. A $26,000 car loan can open doors to a wide range of reliable new or pre-owned vehicles, but navigating the options requires knowledge and strategic planning.

As an expert blogger and SEO content writer, my mission here is to provide you with a comprehensive, in-depth guide that demystifies the $26,000 car loan process. We’ll cover everything you need to know to secure the best possible terms, avoid common pitfalls, and drive away with confidence. This article is designed to be your ultimate resource, ensuring you make informed decisions every step of the way.

Unlocking Your Dream Ride: The Ultimate Guide to a $26,000 Car Loan

Understanding What a $26,000 Car Loan Entails

A $26,000 car loan typically means you’re looking at a mid-range new car, a well-equipped used car, or even a luxury model that’s a few years old. This amount is substantial enough to require careful consideration of your financial health and the terms of the loan. It’s not just the principal amount; interest, fees, and the loan term will significantly impact your total repayment.

Based on my experience, many first-time buyers or those upgrading from a smaller car often find themselves in this price bracket. It offers a sweet spot between affordability and access to desirable features and reliability. However, securing the best loan for this amount depends heavily on your preparedness.

Before You Apply: Essential Preparations for Your $26,000 Car Loan

The most crucial step in securing a favorable $26,000 car loan happens before you even set foot in a dealership or apply online. Thorough preparation empowers you, giving you leverage and clarity. Rushing this stage is one of the common mistakes to avoid.

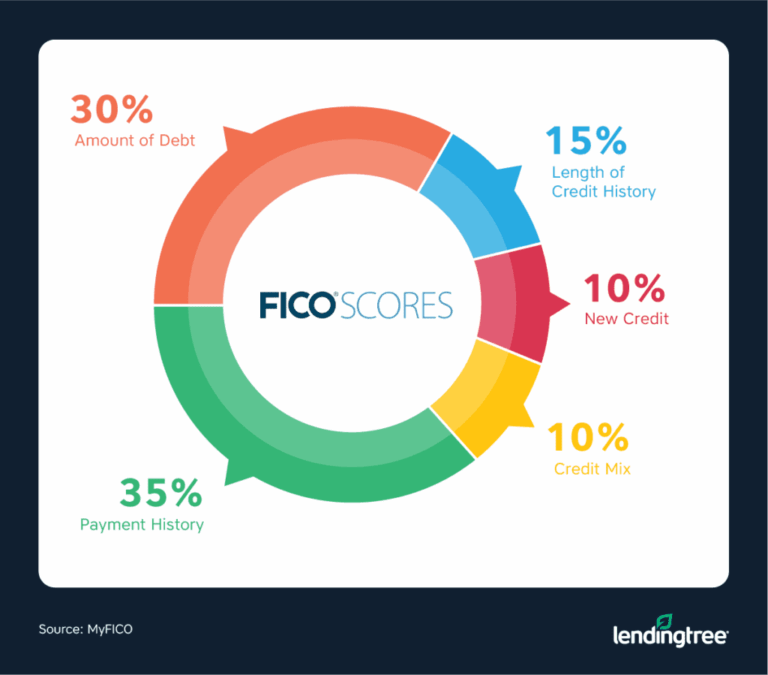

1. Know Your Credit Score Inside Out

Your credit score is arguably the most influential factor in determining your loan’s interest rate. Lenders use it to assess your creditworthiness – essentially, how likely you are to repay the loan on time. A higher score typically translates to a lower Annual Percentage Rate (APR), saving you potentially thousands over the life of the loan.

Pro tips from us: Obtain your credit report from all three major bureaus (Experian, Equifax, TransUnion) well in advance. Review them for any inaccuracies or discrepancies. Dispute any errors you find, as correcting them can boost your score. Websites like AnnualCreditReport.com allow you to get a free report annually.

2. Master Your Budget: What Can You Truly Afford?

While a lender might approve you for a $26,000 loan, it doesn’t automatically mean you should take it. Your budget needs to account for more than just the monthly car payment. Factor in insurance, fuel, maintenance, and potential parking costs.

Based on my experience, many people overlook these additional expenses, leading to financial strain later. A good rule of thumb is that your total car-related expenses, including your loan payment, should ideally not exceed 10-15% of your net monthly income. Create a detailed budget to understand your real disposable income.

3. The Power of a Down Payment

A significant down payment can dramatically improve your loan terms. When you put money down, you reduce the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid. Lenders also view a substantial down payment as a sign of financial stability and commitment.

Even a 10-20% down payment on a $26,000 loan ($2,600-$5,200) can make a huge difference. It can also help you avoid being "upside down" on your loan, where you owe more than the car is worth, especially in the early years of ownership.

4. Understand Your Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is another critical metric lenders scrutinize. It’s the percentage of your gross monthly income that goes towards paying your monthly debt payments (like credit cards, student loans, mortgage, and existing car loans). Lenders prefer a DTI ratio below 36%, though some may go higher depending on other factors.

A lower DTI indicates that you have more disposable income available to comfortably manage your new car loan payments. If your DTI is high, consider paying down other debts before applying for a new loan. This strategic move can significantly improve your chances of approval and secure a better rate.

The Application Process for Your $26,000 Car Loan

Once you’ve prepared your finances, the application process becomes much smoother. Knowing what to expect and what documents to gather will save you time and stress.

1. Gather Your Documents

Lenders require specific documentation to verify your identity, income, and financial stability. Having these ready will streamline your application.

- Proof of Identity: Driver’s license, state ID, or passport.

- Proof of Income: Recent pay stubs (typically 1-2 months), W-2s, tax returns (if self-employed), or bank statements.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement with your current address.

- Social Security Number: Required for credit checks.

- Vehicle Information (if applicable): If you’ve already chosen a car, have its VIN, make, model, and mileage.

2. Get Pre-Approved First

One of the most valuable pro tips from us is to get pre-approved for a loan before you visit a dealership. Pre-approval gives you a clear understanding of how much you can borrow, at what interest rate, and under what terms. This allows you to shop for a car with confidence, knowing your financing is already in place.

More importantly, it gives you negotiating power at the dealership. You’re no longer just a customer; you’re a cash buyer in their eyes, as you already have external financing secured. If the dealership offers better terms, great! If not, you have your pre-approval as a fallback.

Where to Secure Your $26,000 Car Loan

You have several options when it comes to where to get your car loan. Each has its pros and cons, and it’s wise to explore a few before making a decision.

1. Dealership Financing

Dealerships often offer convenient, one-stop shopping. They work with multiple lenders and can sometimes secure competitive rates, especially for new car purchases or through special manufacturer incentives.

However, the common mistake to avoid here is relying solely on dealership financing without having an alternative offer. Always compare their rates to pre-approvals you’ve received elsewhere. Dealerships may also try to "up-sell" you on additional products like extended warranties or GAP insurance, which can inflate your total loan amount.

2. Banks and Credit Unions

Traditional banks are a popular choice for car loans. They offer a range of loan products and often have competitive rates for customers with good credit. Building a relationship with your bank can sometimes lead to preferential treatment.

Credit unions, on the other hand, are member-owned financial institutions. Based on my experience, they often offer some of the most competitive interest rates and personalized service, as their primary goal is to serve their members rather than maximize profits. If you’re eligible to join a credit union, it’s definitely worth exploring their loan options.

3. Online Lenders

The rise of online lenders has provided consumers with more choices and often a streamlined application process. Companies like LightStream, Capital One Auto Finance, and many others specialize in auto loans and can offer quick approvals and competitive rates, particularly for those with strong credit.

The convenience of applying from home and comparing offers from multiple lenders simultaneously is a significant advantage. Just be sure to verify the lender’s reputation and read reviews before committing.

Decoding Loan Terms: APR, Loan Term, and Monthly Payments

Understanding the key components of your $26,000 car loan is vital. These factors directly impact your monthly budget and the total cost of borrowing.

1. Annual Percentage Rate (APR)

The APR is the true cost of borrowing, encompassing not just the interest rate but also any additional fees associated with the loan. A lower APR means you pay less in interest over the life of the loan. Even a seemingly small difference in APR can translate to hundreds or thousands of dollars saved.

For example, on a $26,000 loan over 60 months, a 5% APR would result in total interest of about $3,450, while a 7% APR would be closer to $4,700. Always focus on the APR when comparing loan offers.

2. Loan Term

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A longer loan term means lower monthly payments, which can seem attractive. However, it also means you’ll pay more in total interest over time.

Based on my experience, opting for the shortest loan term you can comfortably afford is usually the most financially savvy decision. It reduces your overall interest burden and helps you build equity in your vehicle faster.

3. Monthly Payments

Your monthly payment is the fixed amount you’ll pay each month until the loan is fully repaid. This figure is determined by the loan amount, the APR, and the loan term. While a lower monthly payment might seem appealing, remember it often comes at the cost of a longer term and more interest.

Always ensure your monthly payment fits comfortably within your budget, allowing for other essential expenses and some savings. Don’t stretch your budget too thin just to afford a slightly more expensive car.

Tips for Getting Approved for Your $26,000 Car Loan (Even with Less-Than-Perfect Credit)

While a good credit score is ideal, it’s still possible to get approved for a $26,000 car loan even if your credit isn’t stellar. It might require a bit more effort and strategic thinking.

1. Improve Your Credit Score First

If time allows, take steps to improve your credit score before applying. Pay down existing debts, especially high-interest credit card balances. Make all your payments on time, as payment history is the most significant factor in your score.

You can also consider becoming an authorized user on someone else’s well-managed credit card. This can help boost your credit history, provided the primary account holder maintains good credit practices.

2. Consider a Larger Down Payment

A larger down payment reduces the risk for the lender. If you have a lower credit score, offering to put down a significant chunk of money can make your application much more appealing. It demonstrates your commitment and reduces the amount of money the lender is risking.

3. Find a Co-Signer

If you have a trusted friend or family member with excellent credit, asking them to co-sign your loan can significantly increase your chances of approval and secure a better interest rate. A co-signer legally agrees to be responsible for the loan if you default.

However, be aware of the implications for your co-signer. Their credit will be affected if you miss payments, and it’s a serious commitment. Ensure you are absolutely confident in your ability to repay the loan if you go this route.

4. Explore Lenders Specializing in Subprime Loans

Some lenders specialize in working with borrowers who have less-than-perfect credit. While their interest rates might be higher, they offer a viable path to vehicle ownership. Do thorough research to ensure they are reputable and offer fair terms.

Common mistakes to avoid here include predatory lenders with excessively high interest rates or hidden fees. Always read the fine print and compare offers.

Common Pitfalls and How to Avoid Them

Navigating the car loan landscape can be tricky. Based on my experience, here are some common mistakes people make and how to steer clear of them.

- Only Focusing on Monthly Payments: While important, fixating solely on the monthly payment can lead to longer loan terms and higher overall costs. Always consider the total amount you’ll pay, including interest.

- Not Getting Pre-Approved: As mentioned, pre-approval is your financial superpower. Without it, you’re negotiating blindly at the dealership.

- Skipping the Test Drive and Inspection: A $26,000 car is a big investment. Always thoroughly test drive and, for used cars, get an independent mechanic to inspect it. Don’t let financing overshadow the vehicle’s condition.

- Ignoring Additional Costs: Remember insurance, maintenance, fuel, and registration. These can add hundreds to your monthly expenses.

- Falling for "Payment Packing": This is when a dealership adds extra products (like extended warranties, GAP insurance, or etching) into your loan without fully explaining them or getting your explicit consent. Always scrutinize the final paperwork before signing.

Managing Your $26,000 Car Loan Like a Pro

Once you’ve secured your $26,000 car loan, smart management ensures a smooth repayment journey and can even save you money.

1. Make Payments On Time, Every Time

This is non-negotiable. Timely payments are crucial for maintaining a good credit score and avoiding late fees. Set up automatic payments to ensure you never miss a due date.

Pro tips from us: If you anticipate difficulty making a payment, contact your lender immediately. They may offer options like deferment or a modified payment plan, which is always better than simply missing a payment.

2. Consider Refinancing

If your credit score has improved significantly since you first took out the loan, or if interest rates have dropped, refinancing your $26,000 car loan could save you money. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms.

You can typically refinance with your current lender or explore options with other banks, credit unions, or online lenders. This can significantly reduce your monthly payment or the total interest paid over the loan term.

3. Paying Off Your Loan Early

If you have extra funds, consider making additional principal payments. Even small extra payments can shave months off your loan term and significantly reduce the total interest you pay. Always confirm with your lender that there are no prepayment penalties.

Based on my experience, paying off a car loan early is a fantastic way to free up cash flow and eliminate debt. It’s a smart financial move if your budget allows.

What if You Can’t Get Approved for a $26,000 Car Loan?

It can be disheartening if your initial applications are denied. However, it’s not the end of the road. There are still options to explore.

1. Reassess Your Budget and Loan Amount

Perhaps a $26,000 car loan is just slightly out of reach for now. Consider looking at vehicles in a lower price range, say $18,000-$22,000. Reducing the principal amount makes the loan less risky for lenders and easier for you to manage.

2. Work on Your Credit Score

If denial was due to poor credit, dedicate time to improving it. Focus on paying bills on time, reducing credit card balances, and reviewing your credit report for errors. This is a long-term strategy but highly effective.

3. Save for a Larger Down Payment

The more you put down, the less you need to borrow. If you can save up a larger down payment, it increases your chances of approval and secures better terms when you reapply.

4. Consider a More Affordable Used Car

A reliable used car that’s a few years older can offer excellent value and come with a much lower price tag. This reduces the amount you need to borrow, making approval easier. For example, exploring our guide on "Tips for Buying a Used Car" could provide valuable insights if you decide to go this route.

The Road Ahead: Driving Smart with Your $26,000 Car Loan

Securing a $26,000 car loan is a significant step towards owning a reliable vehicle. By understanding the process, preparing your finances, comparing offers, and managing your loan diligently, you can ensure a positive and financially sound experience. Remember that knowledge is power, especially when it comes to financial decisions.

Always prioritize what you can truly afford, rather than what a lender says you can borrow. With the insights provided in this comprehensive guide, you are now well-equipped to navigate the world of car loans and drive away with confidence. For more information on managing your finances, consider exploring resources like the Consumer Financial Protection Bureau, which offers excellent advice on auto loans and other financial topics.

Happy driving, and may your journey be smooth and financially responsible! If you’re looking for more ways to save money on your vehicle, check out our article on "Optimizing Your Car Insurance: A Comprehensive Guide."