Unlocking Your Dream Ride: The Ultimate Guide to Car Loan Calculators with Interest Breakdown

Unlocking Your Dream Ride: The Ultimate Guide to Car Loan Calculators with Interest Breakdown Carloan.Guidemechanic.com

Buying a car is an exciting milestone, but for many, the joy can quickly turn into anxiety when confronted with the complexities of financing. Beyond just the sticker price, understanding your car loan – especially how interest accrues – is paramount. This isn’t just about knowing your monthly payment; it’s about seeing the full financial picture, empowering you to make smarter, more economical choices.

As an expert blogger and someone who has navigated countless car financing scenarios, I’ve seen firsthand how a lack of understanding can lead to significant overspending. That’s why today, we’re diving deep into an invaluable tool: the Car Loan Calculator with Interest Breakdown. This isn’t just another online widget; it’s your personal financial compass, guiding you through the labyrinth of auto loans and revealing exactly where your money goes.

Unlocking Your Dream Ride: The Ultimate Guide to Car Loan Calculators with Interest Breakdown

Why Understanding Your Car Loan is Absolutely Crucial

Think of a car loan as a long-term commitment, often spanning several years. During this period, you’re not just paying for the car itself; you’re also paying for the privilege of borrowing money. This "privilege" is called interest, and it can add thousands to the total cost of your vehicle.

Based on my experience, many buyers focus solely on the monthly payment. While crucial for budgeting, this narrow focus can be deceptive. A low monthly payment might seem attractive, but it often hides a longer loan term and a much higher total interest paid over the life of the loan. Understanding the full breakdown allows you to compare offers effectively and negotiate from a position of strength.

What Exactly is a Car Loan Calculator (and Why You Need One)?

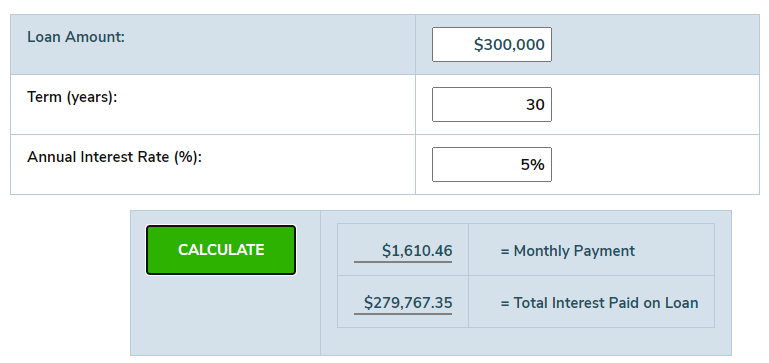

At its core, a car loan calculator is a digital tool designed to help you estimate your monthly car payments. You input key financial figures like the loan amount, interest rate, and loan term, and it instantly crunches the numbers for you. But a basic calculator only tells you so much.

The real power lies in a Car Loan Calculator with Interest Breakdown. This advanced version goes beyond just the monthly payment. It provides a detailed amortization schedule, showing you exactly how much of each payment goes towards the principal (the actual amount you borrowed) and how much goes towards interest. This granular view is a game-changer for financial planning.

It unveils the hidden costs and allows you to visualize the journey of your loan. You’ll see how your principal balance decreases over time and how your interest payments gradually shrink as you get closer to paying off the loan. This transparency is invaluable.

Key Components of a Car Loan You Need to Understand

Before you can effectively use any calculator, you need to grasp the fundamental elements that make up your car loan. Each component plays a vital role in determining your monthly payment and the total cost of your loan.

1. Loan Principal

This is the actual amount of money you are borrowing to purchase the car. It’s the sticker price of the vehicle, minus any down payment, trade-in value, or rebates. Essentially, it’s the base amount upon which interest will be calculated.

A higher principal amount will naturally lead to higher monthly payments and more interest paid over the loan’s lifetime, assuming all other factors remain constant. Reducing your principal through a larger down payment is one of the most effective ways to save money.

2. Interest Rate (APR vs. Interest Rate)

The interest rate is the percentage charged by the lender for borrowing the money. It’s expressed as an annual percentage. A lower interest rate means you’ll pay less for the privilege of borrowing.

It’s important to distinguish between the stated "interest rate" and the "Annual Percentage Rate" (APR). The APR is a broader measure of the cost of borrowing money, as it includes the interest rate plus any additional fees or charges imposed by the lender, such as origination fees. Always compare APRs when shopping for loans, as this gives you a more accurate picture of the total cost.

3. Loan Term

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This is a critical factor influencing both your monthly payment and the total interest paid.

A longer loan term will result in lower monthly payments, which can be tempting for budget-conscious buyers. However, a longer term also means you’ll pay more in total interest over the life of the loan, as the lender has more time to accrue interest on the principal. Conversely, a shorter term means higher monthly payments but significantly less interest paid overall.

4. Down Payment

A down payment is the initial sum of money you pay upfront towards the purchase of the car. This amount reduces the principal loan amount, which in turn lowers your monthly payments and the total interest you’ll pay.

Pro tips from us: Aim for as large a down payment as you can comfortably afford. Even a small increase in your down payment can lead to substantial savings over the loan term, and it also helps you build equity in your vehicle faster.

5. Trade-in Value

If you’re trading in your old vehicle, its value can also reduce the amount you need to finance. Similar to a down payment, a higher trade-in value directly lowers your loan principal.

Ensure you get a fair valuation for your trade-in, as this can significantly impact your new car loan. Research your car’s value beforehand using reputable online tools.

How Interest Works on Car Loans: Amortization Explained

The concept of amortization is central to understanding your car loan’s interest breakdown. Amortization is the process of paying off a debt over time through a series of regular payments. Each payment consists of two parts: principal repayment and interest payment.

Early in your loan term, a larger portion of your monthly payment goes towards interest. This is because the outstanding principal balance is at its highest. As you make more payments, the principal balance gradually decreases, and consequently, a larger portion of your subsequent payments goes towards reducing the principal, with less going to interest.

This "interest-heavy" start is why making extra payments early on can be so impactful. It directly reduces the principal, which in turn reduces the amount of interest calculated on future payments.

The Power of the Interest Breakdown: What It Reveals

The true magic of a Car Loan Calculator with Interest Breakdown lies in its ability to visualize this amortization process. It transforms abstract numbers into a clear, actionable roadmap.

Here’s what this breakdown empowers you to do:

- Identify Total Interest Paid: This is perhaps the most eye-opening revelation. You’ll see the cumulative cost of borrowing, allowing you to truly understand the overall financial commitment.

- Compare Loan Offers Effectively: With the full interest breakdown, you can move beyond just comparing APRs. You can see how different loan terms and rates impact not only your monthly payment but also the total interest paid.

- Make Informed Decisions: Should you take a 60-month loan or a 72-month loan? The interest breakdown will clearly illustrate the additional cost of extending the term, helping you balance affordability with long-term savings.

- Strategize to Save on Interest: By seeing how interest accrues, you can identify opportunities to pay down your principal faster. This could involve making extra payments or even considering refinancing if rates drop.

Without this detailed breakdown, you’re essentially flying blind, making decisions based on incomplete information. This tool gives you the full picture.

Using a Car Loan Calculator With Interest Breakdown: A Step-by-Step Guide

Using this powerful tool is straightforward once you understand the inputs. Here’s how to maximize its potential:

-

Gather Your Data:

- Loan Amount: The price of the car minus any down payment or trade-in.

- Interest Rate (APR): The annual percentage rate offered by your lender.

- Loan Term: The number of months you plan to take to repay the loan.

- Down Payment: (Optional, but highly recommended) The amount you plan to pay upfront.

-

Input the Information: Enter these figures into the respective fields of the calculator. Most reputable calculators are user-friendly and clearly label these inputs.

-

Generate the Amortization Schedule: Click "calculate" or "view breakdown." The calculator will then display your estimated monthly payment and, crucially, an amortization schedule. This schedule will typically show:

- Payment Number

- Date of Payment

- Beginning Balance

- Interest Paid for that Payment

- Principal Paid for that Payment

- Ending Balance

-

Interpret the Results:

- Monthly Payment: Confirm this fits comfortably within your budget.

- Total Interest Paid: This is the sum of all interest payments over the loan term.

- Amortization Table: Observe how the interest portion of your payment decreases over time, while the principal portion increases. This illustrates the loan’s progression.

Pro tip from us: Don’t just run one scenario! Experiment with different interest rates, loan terms, and down payment amounts. See how a small change can significantly impact your monthly payment and the total interest you’ll pay. This iterative process is key to finding the best loan structure for you.

Advanced Strategies & Pro Tips from an Expert

Based on my experience in personal finance, there are several advanced strategies you can employ to further optimize your car loan and save a substantial amount of money.

- Making Extra Payments: Even small, consistent extra payments can make a huge difference. Since early payments are interest-heavy, anything extra you pay directly reduces your principal. This means less interest is calculated on your remaining balance for all subsequent payments, effectively shortening your loan term and saving you money.

- Refinancing Your Loan: If your credit score has improved since you first took out the loan, or if interest rates have dropped, consider refinancing. This involves taking out a new loan with a lower interest rate to pay off your existing one. Use a car loan calculator to see how much you could save with a new, lower APR.

- Improving Your Credit Score: Before even applying for a loan, focus on boosting your credit score. Lenders offer the best interest rates to borrowers with excellent credit. A higher score translates directly to lower interest payments over the life of your loan. For more detailed advice, you might want to check out our blog post on .

- The Impact of a Larger Down Payment: We touched on this, but it bears repeating. A larger down payment immediately reduces the amount you need to borrow, thus reducing both your monthly payment and the total interest paid. It also creates a buffer against depreciation, helping you avoid being "upside down" on your loan.

Common Mistakes to Avoid When Taking Out a Car Loan

Even with the best tools, common pitfalls can lead to financial regret. Here are some common mistakes to avoid:

- Focusing Only on Monthly Payments: This is perhaps the biggest trap. A low monthly payment might feel good, but if it comes with an excessively long loan term, you could end up paying significantly more in total interest. Always look at the overall cost.

- Ignoring the Total Cost of the Loan: Beyond the monthly payment, understand the total amount you will pay back, including all interest. This holistic view is what the interest breakdown calculator provides, so use it!

- Not Shopping Around for Loans: Never accept the first loan offer you receive, especially from the dealership. Always compare offers from multiple lenders – banks, credit unions, and online lenders. Even a half-percent difference in APR can save you hundreds, if not thousands, over the loan term.

- Extending Loan Terms Too Much: While a longer loan term lowers your monthly payment, it also increases the total interest paid and means you’ll be making payments for longer. This can lead to "negative equity" where you owe more than the car is worth, especially as cars depreciate rapidly.

Choosing the Right Car Loan Calculator

Not all car loan calculators are created equal. When choosing one, look for these features:

- Clear and Intuitive Interface: Easy to input your data.

- Amortization Schedule/Interest Breakdown: This is non-negotiable for true insight.

- Ability to Adjust Variables: You should be able to easily change the loan amount, interest rate, and term to see different scenarios.

- Reputable Source: Choose calculators from trusted financial institutions, consumer protection websites, or well-known financial publications. For instance, you can often find excellent resources and calculators on sites like .

Beyond the Calculator: What Else to Consider?

While understanding your loan is paramount, it’s only one piece of the car ownership puzzle. A truly savvy buyer considers the entire cost of ownership.

- Insurance Costs: Your car’s make, model, age, and your driving record significantly impact insurance premiums. Get quotes before you buy.

- Maintenance and Repairs: Newer cars often come with warranties, but older vehicles can incur substantial maintenance costs. Budget for routine servicing and potential repairs.

- Fuel Costs: Consider the car’s fuel efficiency. A car with great MPG can save you a lot of money over its lifetime, especially with fluctuating gas prices.

- Depreciation: Cars lose value over time, often significantly in the first few years. Factor this into your long-term financial planning, especially if you plan to trade in or sell the car relatively soon.

For a deeper dive into overall financing strategies, consider reading our comprehensive .

Drive Smarter, Not Just Harder

The journey to owning your dream car doesn’t have to be fraught with financial uncertainty. By leveraging a Car Loan Calculator with Interest Breakdown, you gain unparalleled clarity into one of your most significant purchases. You move from being a passive borrower to an empowered decision-maker.

This tool is more than just a calculator; it’s a financial education in your hands. It allows you to visualize the impact of every financial choice, from your down payment to your loan term, helping you drive away not just with a new car, but with complete peace of mind. Use it wisely, and you’ll save money, reduce stress, and truly take control of your car ownership experience.