Unlocking Your Dream Ride: The Ultimate Guide to Getting a Car Loan for an Individual Seller

Unlocking Your Dream Ride: The Ultimate Guide to Getting a Car Loan for an Individual Seller Carloan.Guidemechanic.com

Buying a car can be an exhilarating experience, but the journey often begins long before you turn the ignition. For many savvy shoppers, the allure of purchasing from an individual seller is undeniable. It promises better deals, unique finds, and often a more transparent interaction than a traditional dealership. However, the path to financing a car from a private party can seem shrouded in mystery, leading many to believe it’s either impossible or overly complicated.

As an expert in auto financing, I can confidently tell you that securing a car loan for an individual seller is not only possible but also a smart move that can save you a significant amount of money. This comprehensive guide will demystify the process, equip you with expert insights, and provide a step-by-step roadmap to navigate private party auto financing successfully. We’ll dive deep into everything you need to know, from getting pre-approved to signing on the dotted line, ensuring you’re well-prepared to make a confident and informed purchase.

Unlocking Your Dream Ride: The Ultimate Guide to Getting a Car Loan for an Individual Seller

Why Opt for an Individual Seller Over a Dealership?

Before we delve into the intricacies of financing, let’s understand why buying from a private party often makes financial sense. The reasons are compelling and can significantly impact your overall cost and satisfaction.

Firstly, individual sellers typically don’t have the overhead costs associated with a dealership, such as sales commissions, facility maintenance, and extensive advertising. This translates directly into lower asking prices for the same make and model. You’re essentially cutting out the middleman, pocketing the savings yourself.

Secondly, there’s often more room for negotiation when dealing with a private seller. While dealerships have strict pricing structures and profit margins, an individual might be more flexible, especially if they need to sell quickly. This flexibility can lead to a better deal, allowing you to stretch your budget further or get a higher-spec vehicle.

Finally, buying privately often provides a clearer picture of the vehicle’s history and maintenance. Owners who are passionate about their cars often keep meticulous records and can share personal insights into the vehicle’s quirks and care. This personal touch can offer a level of transparency that’s sometimes harder to find in a high-volume dealership environment.

Understanding the "Car Loan For Individual Seller" Landscape

The process of getting a car loan for an individual seller differs significantly from traditional dealership financing. Lenders perceive private sales with a slightly different lens, primarily due to the lack of a formal business entity guaranteeing the sale. This doesn’t mean it’s harder, just different.

When you finance through a dealership, the dealer often has established relationships with multiple lenders, streamlining the application process. For a private sale, you’re essentially acting as your own "dealership" in terms of finding the financing. Lenders evaluate private sales more closely because they don’t have the same reconditioning and warranty backing that a certified pre-owned vehicle from a dealership might offer. This perceived higher risk means lenders will focus heavily on both your creditworthiness and the vehicle’s condition.

The most common types of loans for private party purchases are secured auto loans and, in some cases, unsecured personal loans. A secured auto loan uses the car itself as collateral, making it the preferred and often more affordable option. Personal loans, while simpler to obtain in some ways, typically come with higher interest rates because they are not backed by any collateral. Understanding these differences is crucial for securing the best possible terms.

Step-by-Step Guide to Securing Your Private Party Auto Loan

Navigating the world of private party auto financing requires a structured approach. Based on my experience, following these steps meticulously will significantly increase your chances of a smooth and successful purchase.

Step 1: Get Pre-Approved – Your Financial Foundation

This is arguably the most crucial step when seeking a car loan for an individual seller. Obtaining pre-approval before you even start seriously looking at cars gives you immense power and clarity. It transforms you from a speculative buyer into a serious contender.

Pre-approval means a lender has reviewed your financial profile and determined how much they are willing to lend you, at what interest rate, and under what terms. This allows you to set a realistic budget and avoid the disappointment of falling in love with a car you can’t afford. More importantly, it gives you the confidence to negotiate with a private seller, knowing your financing is already in place.

To get pre-approved, you’ll typically need to provide documentation such as proof of income (pay stubs, tax returns), your Social Security number for a credit check, and details about your existing debts. Lenders will assess your credit score, debt-to-income ratio, and employment stability. Pro tip from us: Don’t settle for the first pre-approval offer. Shop around with several banks, credit unions, and online lenders. Each might offer slightly different rates and terms, and a small difference in interest can save you thousands over the life of the loan.

Step 2: Find Your Ideal Car (and Seller) – The Vehicle Hunt

With your pre-approval in hand, you’re ready to find the perfect vehicle. This stage involves thorough research and due diligence to ensure you’re making a sound investment. Remember, when buying privately, "buyer beware" holds significant weight.

Start by researching specific makes and models that fit your needs and budget. Utilize online marketplaces, local classifieds, and even social media groups. Once you find a potential candidate, the next step is critical: obtain a vehicle history report. Services like Carfax or AutoCheck can reveal past accidents, flood damage, salvage titles, and service records. This report is non-negotiable and provides vital transparency.

Equally important is an independent pre-purchase inspection by a trusted mechanic. Even if the car looks pristine, a professional inspection can uncover hidden mechanical issues or structural damage that could become costly repairs down the line. Common mistakes to avoid are skipping this inspection or relying solely on the seller’s assurances. Based on my experience, this small investment can save you from a major financial headache. Meet the seller, ask detailed questions about the car’s history, maintenance, and reasons for selling, and always verify their identity.

Step 3: Navigating the Loan Application – From Pre-Approval to Final Approval

Once you’ve found the perfect car and it has passed inspection, you’ll need to finalize your car loan for an individual seller. This involves providing your lender with specific details about the vehicle you intend to purchase.

The lender will require the car’s Vehicle Identification Number (VIN), current mileage, and potentially photos or a copy of the seller’s title. They’ll use this information to conduct their own due diligence, verifying the car’s value and ensuring it meets their lending criteria. Some lenders might have restrictions on the age or mileage of vehicles they will finance, especially for private sales. For example, vehicles older than 10-12 years or with extremely high mileage might be harder to finance with a secured auto loan.

It’s paramount to be transparent with your lender that this is a private party sale. Do not try to obscure this fact, as it can complicate or even nullify your loan approval. The lender will need to understand how the transaction will be structured, specifically how they will pay the individual seller and how their lien will be recorded on the vehicle’s title. This step transitions your pre-approval into a full approval, contingent on the vehicle meeting all requirements.

Step 4: The Transaction: Completing the Sale – Title, Funds, and Keys

This is the moment of truth where the money changes hands and the vehicle officially becomes yours. The process is a bit different than at a dealership, where paperwork is often handled seamlessly.

The lender, upon final approval, will typically issue a check directly to the seller or arrange a wire transfer. They will not usually give the funds directly to you for a secured auto loan, as they need to ensure the lien is properly placed. The seller will then sign over the vehicle’s title to you. It’s crucial that the title is clear, meaning there are no existing liens on it. If there is a lien, the seller’s lender must be paid off first, and a lien release obtained. Your lender will then record their lien on the title.

Pro tip: Do not take possession of the vehicle until all funds have cleared and the title transfer is initiated, with the lender’s lien properly recorded. This protects both you and the lender. After the transaction, you’ll need to register the vehicle in your name with your state’s Department of Motor Vehicles (DMV) and obtain auto insurance before driving it off. This typically involves paying sales tax and registration fees. For a detailed guide on title transfer procedures, you might find resources like the DMV Official Guide to Title Transfer helpful.

Key Factors Affecting Your Loan Approval and Rates

Several critical factors influence whether you get approved for a car loan for an individual seller and the interest rate you’ll pay. Understanding these can help you prepare and present the strongest application possible.

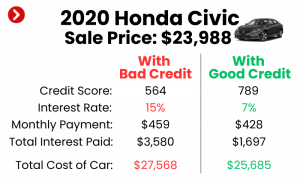

Credit Score: Your Financial Report Card

Your credit score is arguably the most significant factor lenders consider. It’s a numerical representation of your creditworthiness, reflecting your payment history, outstanding debts, length of credit history, and new credit applications. A higher credit score signals lower risk to lenders, leading to better interest rates and more favorable loan terms.

- Excellent (780+): You’ll qualify for the best rates available.

- Good (670-779): Still eligible for competitive rates, though perhaps not the absolute lowest.

- Fair (580-669): You might get approved, but expect higher interest rates.

- Poor (Below 580): Securing a loan can be challenging, often requiring a larger down payment or a co-signer, and rates will be significantly higher.

If your score isn’t where you want it, consider taking steps to improve it before applying, such as paying down existing debt or disputing inaccuracies on your credit report.

Debt-to-Income Ratio (DTI): Are You Overextended?

Your Debt-to-Income (DTI) ratio is another crucial metric. It’s the percentage of your gross monthly income that goes towards paying your monthly debt payments. Lenders use DTI to assess your ability to manage monthly payments and take on new debt.

A lower DTI indicates that you have more disposable income available to comfortably make your car loan payments. Most lenders prefer a DTI of 36% or less, though some might go up to 43%. If your DTI is too high, it signals that you might be overextended financially, making lenders hesitant to approve your loan or offering less favorable terms.

Vehicle Age and Mileage: The Collateral’s Value

Unlike personal loans, a secured auto loan uses the car as collateral. Lenders, therefore, are very interested in the vehicle’s market value and its ability to hold that value over time. Older cars with very high mileage are generally considered higher risk because their depreciation rate is often faster, and they are more prone to mechanical issues.

Most lenders have specific criteria for the age and mileage of vehicles they will finance, especially for private sales. For instance, some may not finance vehicles older than 8-10 years or with more than 100,000-120,000 miles. These restrictions aim to protect the lender’s investment. If the car you want falls outside these parameters, you might need to consider an unsecured personal loan or find a specialized lender.

Down Payment: Reducing Risk, Lowering Payments

Making a down payment significantly strengthens your loan application. It demonstrates your financial commitment to the purchase and immediately reduces the amount you need to borrow. From a lender’s perspective, a down payment reduces their risk, as they have less money invested in the vehicle from the outset.

A substantial down payment can also lead to lower monthly payments, less interest paid over the life of the loan, and potentially a better interest rate. While a down payment isn’t always mandatory, especially for highly qualified borrowers, it’s always a strategic move that can improve your loan terms and overall financial health.

Types of Lenders for Private Party Auto Loans

Knowing where to look for a car loan for an individual seller is just as important as knowing the process. Different types of lenders offer varying benefits and might cater to different borrower profiles.

- Traditional Banks: Large national and regional banks are a common source for auto loans. They offer a wide range of financial products and can be convenient if you already have an account with them. Their rates are generally competitive, but their approval process might be more stringent, especially for older or higher-mileage vehicles.

- Credit Unions: Often considered the best option for auto loans, credit unions are non-profit organizations that typically offer lower interest rates and more flexible terms than traditional banks. They are member-owned, meaning profits are returned to members in the form of better rates and fewer fees. You usually need to become a member to apply, but eligibility is often broad.

- Online Lenders: The digital age has brought forth numerous online lenders specializing in auto loans, including private party financing. These platforms offer convenience, often providing quick pre-approvals and streamlined application processes. They can be a great option for comparing rates from multiple lenders with a single application.

- Personal Loans: While not specifically an auto loan, an unsecured personal loan can be used to purchase a car from a private seller. The main advantage is that it doesn’t use the car as collateral, which can be useful if the car is too old or high-mileage for a secured loan. However, personal loans typically come with higher interest rates due to the increased risk for the lender. For a deeper dive into the distinctions, you might want to read our article on Understanding Different Auto Loan Types.

Common Pitfalls and How to Avoid Them

Even with the best intentions, missteps can occur when securing a car loan for an individual seller. Being aware of these common pitfalls can help you steer clear of potential problems.

One significant mistake is not getting a pre-purchase inspection. As discussed, this seemingly minor oversight can lead to buying a lemon and facing exorbitant repair costs shortly after purchase. Another pitfall is rushing the process. Pressure from a seller or excitement about a car can lead to hasty decisions, skipping vital due diligence steps. Take your time, verify everything, and don’t be afraid to walk away if something feels off.

Not verifying the seller’s identity and the title’s authenticity is another critical error. Ensure the seller is the legal owner of the vehicle and that the title is clear, legitimate, and correctly signed. Common mistakes also include assuming all lenders offer private party loans. Always confirm with a lender upfront that they finance private sales, as some only work with dealerships. Finally, forgetting to budget for additional costs like sales tax, registration fees, insurance, and potential maintenance can strain your finances. Always factor these into your overall budget.

Pro Tips for a Smooth Private Car Purchase

To ensure your journey to owning a car from an individual seller is as smooth as possible, here are some expert tips:

- Always Verify the VIN: Cross-reference the VIN on the vehicle with the VIN on the title and the vehicle history report. Discrepancies are a major red flag.

- Meet in a Safe, Public Place: When meeting a seller, especially for a test drive or final transaction, choose a well-lit, public location. Consider bringing a friend or family member for added safety.

- Get Everything in Writing: Even for private sales, a simple bill of sale documenting the transaction details (price, VIN, date, names of buyer/seller) is crucial. This protects both parties.

- Be Patient and Thorough: Good deals take time to find and execute properly. Don’t let excitement override your critical thinking.

- Don’t Be Afraid to Negotiate: Most private sellers expect some negotiation. Do your research on the car’s market value (using resources like Kelley Blue Book or NADA) and present a fair offer. For more general advice on safe used car buying, check out our guide on Tips for Buying a Used Car Safely.

Conclusion: Your Road to Private Party Car Ownership Awaits

Securing a car loan for an individual seller might initially seem daunting, but as we’ve explored, it’s a completely achievable and often highly rewarding process. By understanding the unique landscape of private party financing, diligently following each step from pre-approval to title transfer, and avoiding common pitfalls, you can confidently navigate the purchase of your next vehicle.

The benefits of buying from a private party—potential cost savings, better negotiation opportunities, and direct insights into a vehicle’s history—are significant. With the right preparation, a bit of patience, and the expert knowledge shared in this guide, you are well-equipped to unlock your dream ride without the dealership markup. Remember, the key is thoroughness, transparency, and a proactive approach. Start your journey today, armed with the knowledge to make a smart, informed decision, and drive away in the car you’ve always wanted.