Unlocking Your Dream Ride: The Ultimate Guide to Securing a $45,000 Car Loan

Unlocking Your Dream Ride: The Ultimate Guide to Securing a $45,000 Car Loan Carloan.Guidemechanic.com

The thought of driving away in a brand-new or high-quality used vehicle is exciting, and for many, a $45,000 car loan represents the sweet spot for achieving that dream. This budget opens up a vast array of options, from well-equipped sedans and versatile SUVs to entry-level luxury models and powerful trucks. However, securing a loan of this magnitude requires careful planning, a clear understanding of the financial landscape, and strategic execution.

Based on my extensive experience in automotive financing and consumer credit, navigating the world of car loans can feel overwhelming. This comprehensive guide is designed to cut through the complexity, providing you with the in-depth knowledge and actionable strategies you need to confidently secure a $45,000 car loan. We’ll explore everything from improving your credit score to finding the best interest rates, ensuring you drive away with not just a great car, but also a smart financial decision.

Unlocking Your Dream Ride: The Ultimate Guide to Securing a $45,000 Car Loan

Understanding the $45,000 Car Loan Landscape

A $45,000 car loan is a significant financial commitment, placing you in a bracket where lenders scrutinize your financial health thoroughly. This loan amount typically finances a premium new vehicle or a relatively recent, well-appointed used car. It’s crucial to approach this decision with a solid financial foundation and a clear understanding of what lenders look for.

This isn’t just about the purchase price; it’s about the total cost of ownership over the loan term. Your monthly payments, interest accrued, insurance costs, and maintenance expenses all factor into whether a $45,000 car is truly affordable for your budget. We’ll delve into how to assess all these components to ensure long-term financial comfort.

Key Factors Influencing Your $45,000 Car Loan Approval

Lenders assess several critical factors when evaluating your application for a $45,000 auto loan. Understanding these elements is your first step towards securing favorable terms and a smooth approval process. Each factor plays a pivotal role in determining your eligibility and the interest rate you’ll be offered.

Proactively addressing these areas before you apply can significantly improve your chances of approval and save you thousands over the life of your car loan. Let’s break down the most important considerations in detail.

1. Your Credit Score: The Cornerstone of Loan Approval

Your credit score is arguably the single most important factor lenders consider. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher score signals less risk to lenders, often translating into lower interest rates and better loan terms.

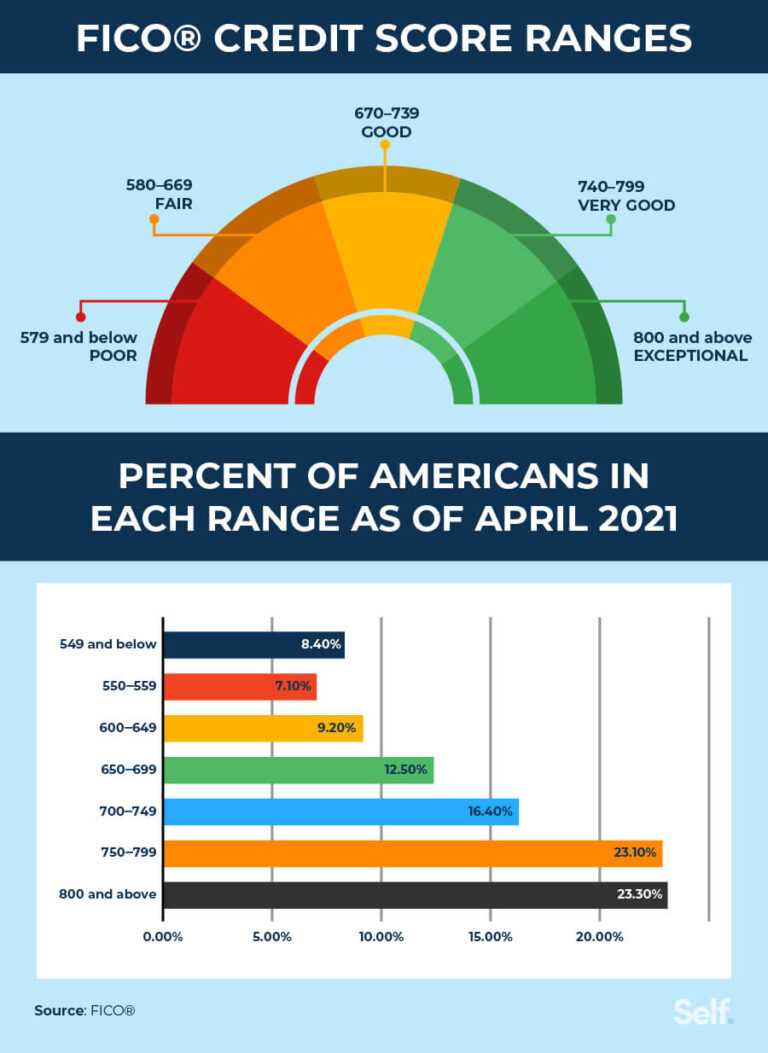

For a $45,000 car loan, a strong credit score (generally 700 and above) is highly advantageous. Lenders use scores like FICO or VantageScore to quickly gauge your reliability. A lower score doesn’t necessarily mean outright rejection, but it will likely result in a higher interest rate, increasing your overall cost.

Pro tips from us: Before applying, obtain your credit reports from all three major bureaus (Equifax, Experian, TransUnion) and check for any errors. Dispute inaccuracies promptly, as even small mistakes can negatively impact your score. Regularly paying bills on time, keeping credit utilization low, and avoiding new credit inquiries right before applying can all boost your score. If your score is below 670, consider taking a few months to improve it before seeking a significant loan like a $45,000 auto loan.

2. Debt-to-Income Ratio (DTI): Are You Overextended?

Your Debt-to-Income (DTI) ratio is another critical metric lenders use to assess your ability to manage additional debt. It compares your total monthly debt payments (including rent/mortgage, credit card payments, student loans, etc.) to your gross monthly income. Lenders prefer a DTI ratio below 43%, though some may approve loans with a DTI up to 50% for applicants with excellent credit.

To calculate your DTI, sum up all your monthly debt payments and divide that by your gross monthly income, then multiply by 100 to get a percentage. For example, if your total monthly debts are $1,500 and your gross income is $4,000, your DTI is 37.5%. A low DTI indicates you have enough disposable income to comfortably make your $45,000 car loan payments.

3. The Power of a Down Payment: Reducing Risk and Cost

Making a substantial down payment is one of the smartest moves you can make when financing a car, especially for a $45,000 vehicle. A down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the loan term. It also demonstrates your financial commitment to the purchase, making you a more attractive borrower to lenders.

Based on my experience, aiming for at least 10-20% of the vehicle’s price as a down payment is ideal. For a $45,000 car, this means putting down $4,500 to $9,000. A larger down payment can also help you avoid being "upside down" on your loan (owing more than the car is worth) early on, which is a common mistake many car buyers make.

4. Loan Term: Balancing Monthly Payments and Total Cost

The loan term, or the length of time you have to repay the loan, significantly impacts both your monthly payment and the total interest paid. Common terms range from 36 to 72 months, with some stretching to 84 months or even longer. While a longer term means lower monthly payments, it also means you’ll pay more in total interest over the life of the loan.

For a $45,000 car loan, carefully consider the trade-offs. A 72-month loan might make the monthly payment more manageable, but you’ll be paying interest for an extended period. Conversely, a 36-month loan will have higher monthly payments but save you considerable interest. Pro tips from us suggest finding the shortest term you can comfortably afford, aligning it with the expected lifespan of the vehicle to avoid negative equity.

5. Interest Rates: The Cost of Borrowing

The interest rate is the percentage charged by the lender for borrowing money. It’s expressed as an Annual Percentage Rate (APR) and includes both the interest rate and any additional fees. A lower APR directly translates to lower monthly payments and less money paid over the loan term. Your credit score, DTI, down payment, and the current market rates all influence the APR you’ll receive.

Shopping around for the best interest rate is non-negotiable. Even a half-percentage point difference on a $45,000 car loan can save you hundreds, if not thousands, of dollars. We’ll discuss how to compare offers effectively to ensure you get the most competitive rate available.

6. Income Stability: Proving Your Ability to Pay

Lenders want assurance that you have a consistent and reliable source of income to make your monthly payments. They typically look for stable employment history, often preferring at least two years in the same job or industry. If you’re self-employed, you’ll need to provide more extensive documentation, such as tax returns, to prove your income stability.

Recent job changes or periods of unemployment can raise red flags for lenders. Having a steady income stream demonstrates your capacity to meet your financial obligations for a $45,000 car loan, making you a less risky borrower.

Navigating the $45,000 Car Loan Application Process

Once you understand the key factors, it’s time to prepare for the application process itself. Being organized and informed will not only streamline the experience but also empower you to negotiate better terms. This is where strategic planning truly pays off.

Don’t rush into signing the first offer you receive; patience and thoroughness are your allies. Let’s outline the steps to a successful application.

1. Preparation is Key: Gather Your Documents

Before you even speak to a lender, gather all necessary documentation. This proactive step can significantly speed up the approval process. Common documents include:

- Proof of Income: Recent pay stubs (1-3 months), W-2s, or tax returns (for self-employed individuals).

- Proof of Identity: Driver’s license or state ID.

- Proof of Residency: Utility bill or lease agreement.

- Social Security Number: For credit checks.

- Vehicle Information: If you’ve already chosen a specific car, have its VIN and mileage handy.

Having these documents ready demonstrates your seriousness and efficiency, which can positively influence lenders.

2. Shopping for Lenders: Explore All Your Options

One of the biggest mistakes to avoid is only getting financing through the dealership. While convenient, dealership financing isn’t always the most competitive option. Explore various lenders to find the best terms for your $45,000 car loan.

- Banks: Traditional banks often offer competitive rates, especially if you’re an existing customer.

- Credit Unions: These member-owned institutions frequently have some of the lowest interest rates available.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and others specialize in online auto loans, offering quick approvals and competitive rates.

- Dealership Financing: While you should explore other options first, dealerships can sometimes match or beat outside offers, especially if they have incentives from their lending partners.

Pro tips from us: Apply to 2-3 different lenders within a short timeframe (usually 14-45 days, depending on the credit scoring model). This allows multiple inquiries to be treated as a single "hard pull" on your credit report, minimizing impact while maximizing your chances of finding the best rate.

3. The Power of Pre-approval: Shop Like a Cash Buyer

Getting pre-approved for a $45,000 car loan before you step foot in a dealership is a game-changer. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a particular interest rate, contingent on the final vehicle choice.

This empowers you to negotiate the car price as if you were a cash buyer, separating the loan negotiation from the vehicle negotiation. You’ll know exactly what you can afford, and you won’t be swayed by high-pressure sales tactics related to financing. It puts you in the driver’s seat.

4. Understanding the Loan Offer: Read the Fine Print

Once you receive loan offers, don’t just look at the monthly payment. Scrutinize the entire loan agreement, paying close attention to:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and fees.

- Total Loan Amount: Ensure it matches your expectations.

- Loan Term: Confirm it aligns with your financial plan.

- Fees: Look for origination fees, document fees, or prepayment penalties.

- Additional Products: Be wary of add-ons like extended warranties, GAP insurance, or service contracts being rolled into your loan without your explicit consent or understanding. While some of these can be beneficial, ensure you truly need them and that they don’t inflate your $45,000 car loan unnecessarily.

Common Mistakes to Avoid When Securing a $45,000 Car Loan

Based on my experience, several pitfalls can derail even the most prepared car buyer. Avoiding these common mistakes can save you significant money and stress:

- Focusing Only on the Monthly Payment: While important, it’s easy to extend the loan term to lower the payment, ultimately paying more in interest. Always consider the total cost of the loan.

- Not Shopping Around for Loans: As mentioned, relying solely on dealership financing can mean missing out on better rates from banks or credit unions.

- Ignoring Your Credit Report: Errors on your credit report can unjustly harm your approval chances and interest rates.

- Buying More Car Than You Can Afford: Even with a $45,000 loan, consider all associated costs like insurance, maintenance, and fuel.

- Forgetting About the Trade-in Value: If you have a trade-in, negotiate its value separately from the new car’s price to ensure you get a fair deal.

Budgeting for Your $45,000 Car Loan: Beyond the Monthly Payment

Securing a $45,000 car loan is only one part of the equation; integrating it into your overall budget is crucial for long-term financial health. A car’s cost extends far beyond the sticker price and monthly payment.

Failing to account for these additional expenses is a common oversight that can lead to financial strain. Let’s look at the full picture.

1. Calculating Monthly Payments: A Realistic Approach

While online calculators can give you an estimate, it’s vital to understand the factors at play. Your monthly payment for a $45,000 car loan will depend on the interest rate, the loan term, and any down payment you make. For example, a $45,000 loan at 6% APR over 60 months (5 years) would result in a monthly payment of approximately $869.67. Over 72 months (6 years) at the same rate, it drops to about $750.32.

Pro tips from us: Always factor in a buffer. Don’t budget to the absolute penny, as unexpected expenses can arise. Use a spreadsheet to test different scenarios for down payments and loan terms to see what truly fits your comfort zone.

2. Beyond the Monthly Payment: The True Cost of Car Ownership

Remember that your car loan payment is just one piece of the puzzle. Other significant costs include:

- Car Insurance: For a $45,000 vehicle, comprehensive insurance can be substantial. Factors like your age, driving record, location, and the car’s make/model (especially if it’s considered high-risk) will influence your premiums. Get insurance quotes before finalizing your purchase.

- Fuel Costs: A more expensive car might also have higher fuel consumption or require premium fuel.

- Maintenance and Repairs: While new cars come with warranties, regular maintenance is still required. Luxury or performance vehicles often have higher parts and labor costs.

- Registration and Taxes: Annual registration fees and potentially sales tax (which might be rolled into your loan or paid upfront) are ongoing expenses.

- Parking Fees/Tolls: Depending on where you live and drive, these can add up.

3. Pro Tips for Financial Planning with Your Auto Loan

- Create a Detailed Budget: Track all your income and expenses to see how a $45,000 car loan payment truly fits.

- Build an Emergency Fund: Having 3-6 months of living expenses saved can protect you if unexpected financial challenges arise.

- Consider GAP Insurance: If you’re putting down a small down payment, GAP (Guaranteed Asset Protection) insurance can cover the difference between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen. This is particularly relevant for a $45,000 vehicle that depreciates quickly.

Choosing the Right Vehicle for Your $45,000 Budget

With a $45,000 car loan, your options are plentiful. This budget allows for a wide range of choices, but making the right decision involves more than just aesthetics. Consider your lifestyle, needs, and long-term financial goals.

Whether you opt for a new or used vehicle, each comes with its own set of advantages and considerations.

New vs. Used Car Considerations

- New Car: Offers the latest technology, full factory warranty, and the peace of mind of being the first owner. However, new cars depreciate rapidly in the first few years.

- Used Car: You can often get a more feature-rich or higher-end model for the same $45,000 budget compared to a new car. Depreciation has already occurred, offering better value. However, warranties might be shorter or non-existent, and maintenance history is crucial.

Pro tips from us: If buying used, always get a pre-purchase inspection from an independent mechanic and review the vehicle history report (CarFax or AutoCheck). For a $45,000 investment, this due diligence is non-negotiable.

Resale Value, Reliability, and Features

When choosing a specific model, research its:

- Resale Value: Some brands and models hold their value better than others, which can be beneficial if you plan to sell or trade it in within a few years.

- Reliability Ratings: Consult consumer reports and automotive reviews to understand potential long-term maintenance costs.

- Features: Prioritize features that genuinely enhance your driving experience and meet your needs, rather than getting caught up in expensive add-ons you won’t use.

Post-Approval: Managing Your $45,000 Car Loan

Once you’ve secured your $45,000 car loan and driven off the lot, your financial journey doesn’t end. Effective loan management is key to minimizing costs and achieving financial freedom. This includes making timely payments and understanding your options for refinancing or early repayment.

This final stage is where discipline truly pays off, ensuring your car loan serves you, rather than the other way around.

1. Making Payments On Time: Protect Your Credit

Consistently making your monthly payments on time is paramount. Late payments can severely damage your credit score, making future borrowing more expensive and difficult. Set up automatic payments to ensure you never miss a due date.

Even a single late payment can stay on your credit report for up to seven years, negatively impacting your financial standing. Prioritize your $45,000 car loan payments to maintain a healthy credit profile.

2. Considering Refinancing: When and Why

Refinancing involves taking out a new loan to pay off your existing car loan. This can be beneficial if:

- Interest Rates Have Dropped: If market rates have fallen since you took out your original loan.

- Your Credit Score Has Improved: A significantly better credit score can qualify you for a lower rate.

- You Want to Change Your Loan Term: You might want to shorten it to pay less interest or lengthen it to lower monthly payments (though this will increase total interest).

Refinancing a $45,000 car loan can potentially save you a substantial amount of money over the remaining loan term. It’s always worth exploring your options after a year or two, especially if your financial situation has improved.

3. Paying Off Early: Pros and Cons

Some lenders allow you to pay off your car loan early without penalty. This can save you a significant amount in interest charges.

- Pros: Reduces total interest paid, frees up monthly cash flow, reduces your DTI, and you own the car outright sooner.

- Cons: Ensure there are no prepayment penalties. The money used to pay off the car could potentially be invested elsewhere for a higher return, or used for higher-interest debt (like credit cards).

Evaluate your overall financial picture before deciding to pay off your $45,000 car loan early.

Frequently Asked Questions (FAQs) about $45,000 Car Loans

Q1: What credit score do I need for a $45,000 car loan?

While there’s no hard minimum, a score of 700+ will generally qualify you for the most competitive interest rates. Scores between 660-699 are considered fair, but you might face slightly higher rates. Below 660, approval for a $45,000 loan might be more challenging or come with significantly higher rates.

Q2: How much should my monthly payment be for a $45,000 car loan?

This depends heavily on your interest rate and loan term. As a general rule, many financial experts suggest your total car expenses (payment, insurance, fuel, maintenance) should not exceed 10-15% of your gross monthly income. Use online calculators to estimate payments based on different rates and terms.

Q3: Can I get a $45,000 car loan with no down payment?

It’s possible, especially with excellent credit, but generally not recommended. A down payment reduces your loan amount, lowers your monthly payments, and helps prevent you from being "upside down" on the loan. It also makes you a more attractive borrower.

Q4: Is it better to get a car loan from a bank or a dealership?

It’s always best to shop around. Banks and credit unions often offer competitive rates, and getting pre-approved through them gives you leverage at the dealership. Dealerships can sometimes match or beat these offers, but it’s crucial to have an external offer to compare against.

Q5: What happens if I can’t make my car loan payments?

If you anticipate difficulty, contact your lender immediately. They may offer options like deferment, renegotiating terms, or temporary payment reductions. Ignoring the problem can lead to late fees, damage to your credit score, repossession of the vehicle, and further financial complications.

Conclusion: Drive Confidently with Your $45,000 Car Loan

Securing a $45,000 car loan is a significant financial step that requires diligence, research, and a clear understanding of the process. By focusing on your credit health, understanding your debt-to-income ratio, making a smart down payment, and meticulously shopping for the best loan terms, you can confidently navigate the financing landscape.

Remember, the goal isn’t just to get approved, but to secure a loan that aligns with your financial goals and allows you to enjoy your new vehicle without undue stress. Armed with the knowledge from this ultimate guide, you are now well-equipped to make informed decisions, avoid common pitfalls, and drive away in your dream car with a smart and sustainable $45,000 auto loan. Plan wisely, negotiate assertively, and enjoy the journey!

External Link: For an excellent resource on understanding various car loan terms and using payment calculators, visit the Consumer Financial Protection Bureau’s auto loan guide: https://www.consumerfinance.gov/consumer-tools/auto-loans/