Unlocking Your Dream Ride: The Ultimate Guide to Securing a Dodge Car Loan

Unlocking Your Dream Ride: The Ultimate Guide to Securing a Dodge Car Loan Carloan.Guidemechanic.com

The roar of a HEMI engine, the aggressive stance of a Challenger, or the robust utility of a Durango – owning a Dodge isn’t just about driving; it’s about an experience. For many, a Dodge represents power, iconic American muscle, and a statement on the road. But before you can feel that thrill behind the wheel, there’s a crucial step: securing the right financing.

Navigating the world of auto loans can seem daunting, but it doesn’t have to be. This comprehensive guide will demystify the Dodge car loan process, offering expert insights and actionable advice to help you drive away in your dream Dodge with confidence and the best possible terms. We’ll cover everything from understanding your credit to finding the best lenders, ensuring you make an informed decision every step of the way.

Unlocking Your Dream Ride: The Ultimate Guide to Securing a Dodge Car Loan

Why a Dodge? More Than Just a Car

Before we dive into the financing specifics, let’s briefly acknowledge the allure. Dodge vehicles stand out. They embody a unique blend of heritage, performance, and distinctive design, from the raw power of the Charger and Challenger to the family-friendly, yet still potent, Durango. This isn’t just a purchase; it’s an investment in a lifestyle, and finding the right Dodge car loan is key to making that lifestyle accessible.

Understanding what makes a Dodge special helps frame why a well-researched financing plan is so important. You’re not just buying transportation; you’re buying a piece of automotive legacy.

The Dodge Car Loan Landscape: What You Need to Know

Securing a car loan involves more than simply asking for money. It’s about understanding the financial ecosystem that supports vehicle purchases. When you’re looking for a Dodge car loan, you’ll encounter various terms and options, each designed to fit different financial situations.

Your goal isn’t just to get approved, but to get approved on terms that align with your budget and financial goals. This means looking beyond the monthly payment to the total cost of the loan, including interest, fees, and any additional charges. Being informed is your greatest asset.

Key Factors Influencing Your Dodge Car Loan Approval and Terms

Several critical elements come into play when lenders evaluate your application for a Dodge car loan. Understanding these factors empowers you to improve your standing and negotiate more effectively. Based on my experience, focusing on these areas upfront can significantly impact your loan outcome.

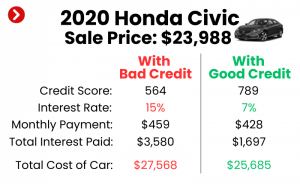

Your Credit Score: The Cornerstone of Car Loans

Your credit score is arguably the most influential factor in securing any loan, including a Dodge car loan. It’s a three-digit number that summarizes your creditworthiness, reflecting your history of borrowing and repayment. Lenders use this score to assess the risk of lending to you.

A higher credit score typically translates to lower interest rates and more favorable loan terms. Conversely, a lower score might mean higher interest rates or even require a larger down payment or a co-signer. Pro tips from us: always check your credit score and report well before you apply. This allows you time to correct any errors or address issues that might be dragging your score down.

The Power of a Down Payment

A down payment is the initial sum of money you pay towards the purchase of your Dodge. It directly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. A substantial down payment also signals financial stability to lenders.

Common mistakes to avoid are skipping a down payment entirely, if possible. While it might seem appealing to finance 100% of the vehicle, a larger down payment significantly reduces your financial burden and can often secure better interest rates. Aim for at least 10-20% of the vehicle’s price if your budget allows.

Debt-to-Income Ratio (DTI): A Lender’s Perspective

Your debt-to-income ratio (DTI) is another crucial metric lenders consider. It’s a simple calculation: your total monthly debt payments divided by your gross monthly income. This ratio helps lenders understand how much of your income is already committed to existing debts.

A lower DTI indicates that you have more disposable income available to comfortably manage your new Dodge car loan payments. Lenders generally prefer a DTI below 43%, though this can vary. Keeping an eye on your DTI ensures you’re not overextending yourself financially, making you a more attractive borrower.

Loan Term: Balancing Monthly Payments and Total Cost

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This choice significantly impacts both your monthly payment and the total amount of interest you’ll pay over the loan’s life.

Shorter loan terms mean higher monthly payments but less interest paid overall, getting you out of debt faster. Longer loan terms offer lower monthly payments, making the Dodge more "affordable" in the short term, but you’ll pay substantially more in interest over time. Carefully consider what payment schedule fits your budget without incurring excessive long-term costs.

Vehicle Age & Type: New vs. Used Dodge Financing

The age and type of the Dodge you’re financing also play a role. New Dodge vehicles often qualify for lower interest rates and special manufacturer incentives through programs like Stellantis Financial Services (Dodge’s captive finance arm). Lenders perceive new cars as less risky due to warranties and predictable depreciation.

Used Dodge vehicles, while often more affordable upfront, might come with slightly higher interest rates due to perceived higher risk or lack of manufacturer incentives. However, the lower purchase price can still result in a more manageable total loan amount. Be sure to factor in potential maintenance costs for older models when budgeting.

Where to Get Your Dodge Car Loan: Exploring Your Options

When it comes to securing a Dodge car loan, you have several avenues to explore. Each has its own advantages and disadvantages, and shopping around is a pro tip that can save you thousands of dollars.

1. Dodge Dealership Financing (Stellantis Financial Services)

Many buyers opt for financing directly through the Dodge dealership. This is often facilitated by Stellantis Financial Services, the captive finance company for Dodge and other Stellantis brands.

- Pros: Convenience (one-stop shop), potential for special promotional rates, lease options, and incentives (e.g., low APR deals, cash back) offered by the manufacturer. Dealers can also work with multiple lenders to find you an option.

- Cons: You might not always get the absolute lowest rate compared to shopping independently, and the focus might be more on closing the deal than finding your ideal financial product.

Based on my experience, dealership financing can be highly competitive, especially if there are manufacturer-backed incentives. However, it’s always wise to compare their offer with pre-approvals you’ve secured elsewhere.

2. Banks & Credit Unions

Traditional financial institutions are a popular choice for auto loans. Both national banks and local credit unions offer competitive rates for Dodge car loans.

- Pros: Often lower interest rates, particularly for customers with good credit or existing relationships. Credit unions, in particular, are known for their customer-centric approach and competitive rates. Pre-approval from these institutions can give you significant negotiating power at the dealership.

- Cons: The application process might take slightly longer than dealership financing, and you’ll need to handle the financing paperwork separately from the vehicle purchase.

Pro tips from us: Always get pre-approved by your bank or credit union before stepping foot in a dealership. This establishes a baseline interest rate, making it easier to identify a good deal and avoid paying too much.

3. Online Lenders

The digital age has brought a new wave of online-only lenders specializing in auto loans. These platforms offer a streamlined application process and quick decisions.

- Pros: Speed and convenience (apply from anywhere, anytime), competitive rates, and often cater to a wider range of credit scores, including those with less-than-perfect credit. They can also provide multiple offers from different lenders through a single application.

- Cons: Less personalized service compared to a local bank, and you need to be vigilant about checking their legitimacy and terms. Ensure they are reputable and transparent with their fees.

Online lenders are an excellent option for comparing multiple offers quickly and efficiently. Just make sure to read reviews and verify their credentials.

The Dodge Car Loan Application Process: A Step-by-Step Guide

Understanding the application process will help you feel more in control and prepared. It’s not just about filling out forms; it’s about presenting yourself as a reliable borrower.

Step 1: Preparation is Key

Before you even think about applying, gather your necessary documents. This includes a valid driver’s license, proof of income (pay stubs, tax returns), proof of residence (utility bills), and insurance information. Having these ready streamlines the entire process.

Knowing your financial standing, including your credit score and DTI, is also part of preparation. This allows you to anticipate potential challenges or leverage your strong financial position.

Step 2: Get Pre-Approved

This is perhaps the most powerful step you can take. Pre-approval means a lender has provisionally agreed to lend you a certain amount at a specific interest rate, based on a preliminary review of your credit and finances.

- Benefits: It gives you a firm budget, transforming you into a cash buyer in the eyes of the dealership. This negotiating power can lead to a better deal on the vehicle itself. It also clarifies your interest rate, so you can focus on the car price, not the loan terms.

- Soft vs. Hard Inquiries: Most pre-approvals involve a "soft" credit inquiry, which doesn’t affect your score. Once you proceed with a specific lender, a "hard" inquiry will be made.

Step 3: Application Submission

Once you’ve chosen a lender and are ready to finalize your purchase, you’ll submit a formal application. This involves providing detailed financial information and authorizing a hard credit pull.

The lender will then review all your information, including your credit report, income stability, and DTI. This is where they make their final decision on your Dodge car loan approval and the exact terms.

Step 4: Understanding the Offer

When you receive a loan offer, don’t just look at the monthly payment. Scrutinize the Annual Percentage Rate (APR), which is the true cost of borrowing, including interest and some fees. Understand the total cost of the loan over its entire term.

Look for any hidden fees, prepayment penalties, or other clauses that might impact your financial future. This thorough review ensures there are no surprises down the road.

Step 5: Finalizing the Deal

Once you’re satisfied with the loan terms, it’s time to sign the paperwork. Read every single document carefully before putting your signature on it. Ensure all the agreed-upon terms—APR, loan amount, term length, and any fees—are accurately reflected in the final contract.

Never feel rushed during this stage. If you have questions, ask them. This is a legally binding agreement, and your understanding is paramount.

Navigating Special Situations for Your Dodge Car Loan

Not everyone has perfect credit or a straightforward financial history. Here’s how to approach a Dodge car loan in less-than-ideal circumstances.

Bad Credit Dodge Car Loan: It’s Possible!

Having a low credit score doesn’t automatically disqualify you from getting a Dodge car loan. It just means you might need to take a different approach. Many lenders specialize in subprime auto loans for individuals with poor credit.

- Strategies:

- Co-signer: A co-signer with good credit can significantly improve your chances of approval and secure better rates.

- Larger Down Payment: As discussed, a larger down payment reduces the risk for the lender.

- Subprime Lenders: These lenders are more willing to work with bad credit but often charge higher interest rates.

- Focus on Affordability: Consider a less expensive used Dodge model to keep the loan amount lower.

- Common mistakes to avoid: Not checking your credit report for errors, and jumping at the first offer without comparing options. Pro tips: Use this loan as an opportunity to rebuild your credit by making consistent, on-time payments.

First-Time Car Buyer

If this is your first time financing a vehicle, you might lack a robust credit history. Some lenders and dealerships offer specific programs designed for first-time buyers.

These programs might have specific income requirements or require a co-signer. Focus on building a credit history with a smaller, more manageable loan if necessary, or opt for a slightly older, less expensive Dodge model.

Refinancing Your Dodge Car Loan

Perhaps you initially secured a loan with less-than-favorable terms, or your credit score has significantly improved since your purchase. Refinancing your Dodge car loan might be a smart move.

- When it makes sense:

- You can get a lower interest rate, reducing your total cost.

- Your credit score has improved.

- You want to lower your monthly payments by extending the loan term (though this increases total interest).

- You want to shorten your loan term to pay it off faster (which increases monthly payments).

- How to do it: Shop around for new lenders just like you did for your initial loan. Compare their offers, and if you find a better deal, apply to refinance your existing loan.

Budgeting for Your Dodge: Beyond the Monthly Payment

A Dodge car loan payment is just one piece of the puzzle. As an expert blogger, I can tell you that neglecting the other costs associated with car ownership is a common pitfall.

- Insurance Costs: Dodge vehicles, especially performance models, often have higher insurance premiums. Get quotes before you buy.

- Maintenance and Repairs: All cars need maintenance. Factor in routine service, tires, and potential unexpected repairs.

- Fuel Costs: The powerful engines in many Dodge models can be thirsty. Estimate your fuel budget based on your driving habits.

- Registration and Taxes: Don’t forget annual registration fees and sales tax, which can be substantial depending on your state.

Pro tips from us: Create a comprehensive budget that includes all these expenses, not just your monthly loan payment. This holistic view will prevent financial surprises down the road.

Common Mistakes to Avoid When Getting a Dodge Car Loan

To ensure a smooth and financially sound purchase, be mindful of these frequent errors:

- Not Shopping Around: Settling for the first loan offer without comparing rates from multiple lenders is a costly mistake.

- Focusing Only on Monthly Payment: While important, an artificially low monthly payment might come from an extended loan term, leading to significantly more interest paid over time.

- Ignoring the Total Cost: Always calculate the total amount you’ll pay over the life of the loan, including all interest and fees.

- Skipping Pre-Approval: Without pre-approval, you lose significant negotiating leverage at the dealership.

- Not Reading the Fine Print: Every clause in your loan agreement is important. Understand what you’re signing.

- Letting the Dealer Run Multiple Credit Checks Without Permission: Too many hard inquiries in a short period can negatively impact your credit score.

Pro Tips for Securing the Best Dodge Car Loan

Based on my extensive experience in the auto finance world, here are some actionable tips to help you get the most favorable Dodge car loan:

- Boost Your Credit Score: Pay bills on time, reduce credit card balances, and check for errors on your report. Even a few points can make a difference. (For more detailed advice, you might want to check out our article on Tips for Improving Your Credit Score Before a Car Loan – Internal Link Placeholder).

- Save for a Larger Down Payment: The more you put down, the less you borrow, and the better your terms are likely to be.

- Get Pre-Approved from Multiple Sources: This empowers you with negotiating leverage and allows you to choose the best offer.

- Be Ready to Negotiate: Don’t be afraid to ask for a better rate or terms, especially if you have competing offers.

- Understand All Terms Before Signing: Ask questions until you’re completely clear on the APR, total cost, and any fees.

- Consider a Co-signer (If Needed): If your credit isn’t ideal, a trusted co-signer can be a game-changer for approval and rates.

- Factor in All Ownership Costs: Remember the bigger picture beyond just the loan payment. (Another great resource is our guide on Understanding Car Insurance for Your New Vehicle – Internal Link Placeholder).

- Utilize Resources: The Consumer Financial Protection Bureau (CFPB) offers excellent, unbiased information on auto loans that can help you make informed decisions. (External Link: https://www.consumerfinance.gov/consumer-tools/auto-loans/ – This is an example, make sure to link to the specific auto loan section.)

Conclusion: Drive Away with Confidence

Securing a Dodge car loan doesn’t have to be a stressful ordeal. By understanding the key factors that influence your approval, exploring all your lending options, and meticulously preparing for the application process, you can navigate the journey with confidence. Remember, the goal isn’t just to get a loan, but to get the right loan – one that fits your budget, secures favorable terms, and ultimately allows you to enjoy the thrill of your new Dodge without financial worry.

Take your time, do your research, and don’t be afraid to ask questions. With this comprehensive guide, you’re well-equipped to make an informed decision and embark on your Dodge adventure with peace of mind. Happy driving!