Unlocking Your Dream Ride: The Ultimate Guide to the Car Loan Prequalification Calculator

Unlocking Your Dream Ride: The Ultimate Guide to the Car Loan Prequalification Calculator Carloan.Guidemechanic.com

Buying a new car is an exciting milestone, often accompanied by the thrill of choosing a model, imagining road trips, and envisioning daily commutes in style. However, before you even step foot onto a dealership lot, there’s a crucial, often overlooked, step that can save you time, money, and a significant amount of stress: using a Car Loan Prequalification Calculator.

Based on my experience in automotive finance, understanding your borrowing power upfront is not just a convenience; it’s a strategic advantage. This comprehensive guide will demystify the car loan prequalification calculator, explaining why it’s an indispensable tool for every prospective car buyer, how it works, and how you can leverage it to secure the best possible deal. Get ready to transform your car buying journey from daunting to delightful!

Unlocking Your Dream Ride: The Ultimate Guide to the Car Loan Prequalification Calculator

What Exactly is a Car Loan Prequalification Calculator?

At its core, a Car Loan Prequalification Calculator is an online tool designed to give you an early, unofficial estimate of how much money a lender might be willing to loan you for a car purchase. Think of it as a preliminary health check for your potential auto loan. It allows you to input some basic financial information and, in return, provides an estimated loan amount, interest rate, and potential monthly payment.

It’s important to understand that prequalification is distinct from pre-approval. While both offer a glimpse into your borrowing capacity, prequalification is generally a softer, less formal inquiry. It doesn’t typically involve a hard credit check, meaning it won’t impact your credit score. This makes it a fantastic, risk-free way to gauge your financial standing before making any commitments.

Why is Prequalification an Essential First Step?

Many car buyers make the mistake of falling in love with a vehicle before understanding their financial limits. This often leads to disappointment or, worse, taking on a loan with unfavorable terms. Using a Car Loan Prequalification Calculator proactively empowers you in several significant ways.

Firstly, it provides immense clarity on your affordability. Knowing roughly how much you can borrow helps you set realistic expectations for the types of vehicles you can genuinely afford, rather than chasing cars that are financially out of reach. This saves you from the frustration of finding your "perfect car" only to discover it’s beyond your budget.

Secondly, it significantly streamlines the car buying process. Instead of spending hours at a dealership discussing financing options for cars you might not even qualify for, you arrive with a clear understanding of your financial parameters. This focused approach makes your time more efficient and productive.

Finally, and perhaps most importantly, prequalification gives you powerful negotiation leverage. When you know your estimated borrowing capacity and interest rate, you can negotiate with dealers on the car price with confidence. You’re no longer solely reliant on their financing offers, putting you in a stronger position.

How Does a Car Loan Prequalification Calculator Work?

The magic behind a Car Loan Prequalification Calculator lies in its ability to quickly process your inputs against a set of general lending criteria. While each calculator might vary slightly, they typically ask for similar pieces of information. Understanding these inputs is key to getting an accurate estimate.

You’ll usually be prompted to enter details such as your estimated credit score range (e.g., excellent, good, fair), your annual income, the desired loan amount, the preferred loan term (e.g., 36, 48, 60 months), and any potential down payment or trade-in value you plan to offer. Some calculators might also ask for your zip code to factor in regional interest rates.

Once you input these details, the calculator’s algorithm quickly assesses your financial profile based on typical lending standards. It then provides an estimate of the interest rate you might qualify for, the total loan amount, and a projected monthly payment. Remember, this is an estimate, a snapshot based on the data you provide.

Key Factors Influencing Your Prequalification Estimate

Several critical financial components directly impact the estimates generated by a Car Loan Prequalification Calculator. Understanding these factors will not only help you use the tool more effectively but also identify areas where you might improve your financial standing before applying for a formal loan.

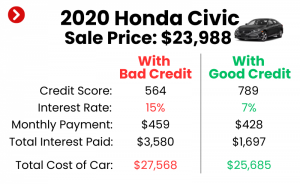

The most significant factor is almost always your credit score. Lenders use this three-digit number to assess your creditworthiness and the likelihood of you repaying a loan. A higher credit score (generally 700+) typically translates to lower interest rates because you’re perceived as a lower risk. Conversely, a lower score will likely result in higher rates or even difficulty securing a loan. Based on my experience, consistently checking your credit score and report for inaccuracies is a pro tip every car buyer should follow.

Your income and debt-to-income (DTI) ratio are also crucial. Lenders want to ensure you have sufficient income to comfortably make your loan payments in addition to your existing financial obligations. Your DTI ratio compares your total monthly debt payments to your gross monthly income. A lower DTI (ideally below 40%) signals to lenders that you have enough disposable income to handle new debt responsibly.

The loan amount and term you request play a direct role in your monthly payment and the total interest paid. A larger loan amount will naturally lead to higher payments, assuming the same interest rate and term. Similarly, a longer loan term (e.g., 72 months instead of 48 months) can lower your monthly payments, but you’ll generally pay more in interest over the life of the loan. It’s a balance between affordability and total cost.

Furthermore, any down payment you make can significantly reduce the amount you need to borrow, thereby lowering your monthly payments and potentially the overall interest paid. A substantial down payment also shows lenders your commitment and reduces their risk. The same principle applies to your trade-in value; if you’re trading in an existing vehicle, its value acts like a down payment, reducing your new loan amount.

Finally, broader interest rates in the market at the time of your prequalification can influence the estimate. These rates are dynamic and can fluctuate based on economic conditions and central bank policies. While you can’t control market rates, being aware of the prevailing environment helps you set realistic expectations.

Benefits of Using a Prequalification Calculator

The advantages of leveraging a Car Loan Prequalification Calculator extend far beyond just getting an estimated number. They fundamentally change your approach to car buying, making it a more informed and less stressful experience.

Firstly, it provides unparalleled clarity on affordability. You’ll know precisely what price range of vehicles you should be considering, eliminating the guesswork. This prevents the common pitfall of falling for a car that ultimately stretches your budget too thin.

Secondly, it helps you understand potential interest rates based on your credit profile. This knowledge is power. If the estimated rate is higher than you hoped, it gives you time to work on improving your credit score before applying for a formal loan. Pro tips from us: knowing your estimated rate also helps you identify if a dealership’s offer is competitive or if you should seek financing elsewhere.

Another significant benefit is identifying areas for financial improvement. By inputting your details, you might realize your credit score needs work, or your debt-to-income ratio is a bit high. This calculator acts as an early warning system, giving you the opportunity to strengthen your financial position before applying for a hard inquiry loan.

It also significantly streamlines the car buying process. Imagine walking into a dealership already knowing your budget and what kind of loan terms you might qualify for. This focus allows you to spend less time on financing discussions and more time on test drives and negotiating the actual car price.

Ultimately, using this tool leads to reduced stress and fewer surprises. There’s nothing worse than getting your hopes up for a specific car only to be denied financing or offered exorbitant interest rates. Prequalification helps you avoid these disheartening moments by preparing you for what to expect.

Limitations of Prequalification Calculators

While incredibly useful, it’s crucial to acknowledge that a Car Loan Prequalification Calculator has its limitations. It’s a powerful estimation tool, but it’s not a crystal ball or a binding offer.

The primary limitation is that the results are always estimates, not guarantees. The actual interest rate and loan amount you qualify for may differ once a lender conducts a full credit check and reviews your complete financial application. The calculator uses general parameters, whereas actual lenders consider a much wider array of specific criteria.

Furthermore, these calculators don’t consider all lender-specific criteria. Each bank, credit union, or online lender has its own unique underwriting standards, risk assessments, and promotional offers. A calculator provides a generic benchmark, not an exact match for every single lender’s specific policies.

Finally, market fluctuations can impact the accuracy of older prequalification estimates. Interest rates can change, and lending standards might adjust over time. It’s always a good idea to use the calculator close to when you plan to apply for a loan for the most up-to-date information.

Pro Tips for Maximizing Your Prequalification Calculator Experience

To get the most accurate and useful results from a Car Loan Prequalification Calculator, follow these expert recommendations. Based on my experience, a little extra effort here pays dividends.

Firstly, be accurate with your inputs. Don’t guess your income or credit score. Use your actual figures as closely as possible. If you’re unsure of your credit score, many credit card companies offer free access to it, or you can get a free report from annualcreditreport.com.

Secondly, check your credit report beforehand. This isn’t just about knowing your score; it’s about identifying any errors or discrepancies that could negatively impact your loan application. Correcting these errors before applying can significantly improve your chances of securing better terms.

Thirdly, experiment with different scenarios. Try adjusting the down payment amount, the loan term, or even your estimated credit score range (if you plan to improve it). This helps you understand how different variables affect your monthly payment and overall cost, allowing you to find a sweet spot that fits your budget.

Crucially, understand the difference between prequalification and pre-approval. Prequalification is a soft inquiry, an estimate. Pre-approval involves a more detailed review of your finances, including a hard credit inquiry, and results in a conditional offer from a specific lender. While prequalification is a great starting point, pre-approval gives you a firm offer to take to the dealership.

Finally, don’t stop at just one calculator. Try using calculators from different reputable financial institutions or automotive finance websites. This can give you a broader perspective and help you compare potential offers, as different calculators might use slightly different algorithms or data sets.

What to Do After Prequalifying

So, you’ve used the Car Loan Prequalification Calculator and have an estimate of your borrowing power. What’s next? This is where you transition from estimation to action, strategically preparing for your car purchase.

Your first step is to review the estimates carefully. Understand the estimated interest rate, monthly payment, and total loan amount. Does this align with your budget and financial goals? If not, consider adjusting your expectations or working on improving your financial profile.

Next, it’s time to shop for actual loans. Armed with your prequalification estimate, you can now approach various lenders (banks, credit unions, online lenders) to get pre-approved offers. Remember, pre-approval involves a hard credit inquiry, so aim to get all your pre-approvals within a short window (typically 14-45 days, depending on the credit bureau) to minimize the impact on your credit score. This is called rate shopping.

With pre-approved loan offers in hand, you’re now in an excellent position to prepare for a formal application. Gather all necessary documents, such as proof of income, identification, and residence. Being organized will make the final application process smooth and efficient.

Most importantly, you can now negotiate with confidence at the dealership. You have a benchmark interest rate and a clear understanding of your budget. You can compare the dealership’s financing offers against your pre-approved loans, ensuring you get the most favorable terms possible for your new vehicle. This financial readiness can save you thousands over the life of the loan.

Common Mistakes to Avoid

Even with the best intentions, car buyers can make mistakes that undermine the benefits of prequalification. Being aware of these common pitfalls can help you navigate the process more effectively.

A common mistake is ignoring your debt-to-income ratio (DTI). While the calculator might not explicitly ask for all your monthly debts, failing to consider how new car payments will impact your overall DTI can lead to future financial strain. Lenders scrutinize this, and a high DTI can lead to loan denial or less favorable terms.

Another pitfall is not factoring in additional costs beyond the car’s sticker price. Remember to budget for sales tax, registration fees, insurance, and any extended warranties or add-ons. These can significantly increase your total financial commitment and might push you beyond your prequalified loan amount.

Many mistakenly assume the estimate from the calculator is final. It’s crucial to reiterate that it’s an estimate, a guide, not a guaranteed offer. Treat it as a starting point for further investigation, not the end-all-be-all.

Only focusing on the monthly payment is another significant error. While a low monthly payment seems appealing, it often comes at the cost of a longer loan term and more interest paid over time. Always consider the total cost of the loan, not just the monthly figure. Pro tips from us: a slightly higher monthly payment for a shorter term can save you substantial money in the long run.

Finally, and perhaps the biggest mistake, is skipping prequalification altogether. Walking into a dealership without any prior understanding of your financing options puts you at a distinct disadvantage. You’re more susceptible to higher interest rates and less favorable terms.

Conclusion: Empower Your Car Buying Journey

The Car Loan Prequalification Calculator is more than just a convenient online tool; it’s a strategic asset for anyone looking to purchase a vehicle. By providing an early, no-impact estimate of your borrowing power, it equips you with the knowledge and confidence to approach the car buying process with clarity and control. From understanding your affordability and potential interest rates to identifying areas for financial improvement and gaining crucial negotiation leverage, its benefits are undeniable.

Don’t let the excitement of a new car overshadow the importance of financial preparedness. Take the time to utilize this powerful tool, understand its insights, and follow our expert tips. By doing so, you’ll not only secure a better deal but also embark on your new car journey feeling empowered, informed, and financially secure. Your dream ride awaits, and with smart planning, it’s well within your reach.