Unlocking Your Drive: A Comprehensive Guide to Your Chances Of Getting A Car Loan

Unlocking Your Drive: A Comprehensive Guide to Your Chances Of Getting A Car Loan Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect, but the path to financing it can often feel like navigating a complex maze. One of the most common questions on potential car buyers’ minds is: "What are my chances of getting a car loan?" Understanding the factors that influence car loan approval is not just about securing a vehicle; it’s about making an informed financial decision that serves you well in the long run.

This in-depth guide is designed to demystify the car loan process, providing you with expert insights and actionable strategies. We’ll explore exactly what lenders scrutinize, how you can enhance your appeal, and even how to navigate challenging scenarios like bad credit. By the end of this article, you’ll have a clear roadmap to boost your car loan approval chances and drive away with confidence.

Unlocking Your Drive: A Comprehensive Guide to Your Chances Of Getting A Car Loan

Understanding the Foundation: What Lenders Truly Look For

When you apply for a car loan, lenders aren’t just looking at your enthusiasm for a new ride. They’re assessing your creditworthiness – your ability and likelihood to repay the loan as agreed. This evaluation is based on several key financial indicators, each playing a crucial role in determining your eligibility and the terms of your loan.

Based on my experience, a common mistake many applicants make is focusing solely on one aspect, like their income, while neglecting others. Lenders take a holistic view, and understanding each component is your first step towards a successful application.

Your Credit Score: The Cornerstone of Loan Approval

Your credit score is arguably the most significant factor lenders consider. It’s a three-digit number that summarizes your credit history, reflecting how responsibly you’ve managed debt in the past. A higher score signals lower risk to lenders, often translating into better loan terms and a higher chance of approval.

Different credit score ranges typically indicate varying levels of risk. Scores above 700 are generally considered good to excellent, giving you access to the most competitive interest rates. Scores between 600 and 699 are often categorized as fair, while anything below 600 may be deemed subprime or poor credit, making approval more challenging and interest rates significantly higher.

Pro tips from us: Always review your credit report from all three major bureaus (Equifax, Experian, TransUnion) at least once a year. This allows you to identify and dispute any inaccuracies that could be unfairly dragging down your score, potentially improving your car loan chances. For a deeper dive into improving your credit score, check out our guide on .

Debt-to-Income (DTI) Ratio: Your Financial Balancing Act

Beyond your credit score, lenders closely examine your debt-to-income (DTI) ratio. This percentage compares your total monthly debt payments to your gross monthly income. It’s a critical indicator of your ability to manage additional debt without becoming overextended.

To calculate your DTI, simply add up all your monthly debt payments – this includes student loans, credit card minimums, mortgage or rent, and any existing car loans. Then, divide that sum by your gross monthly income (before taxes and deductions). For instance, if your debts total $1,500 and your gross income is $4,500, your DTI is 33%.

Most lenders prefer a DTI ratio of 36% or lower, though some may go up to 43% for car loans, especially for applicants with strong credit scores. A lower DTI indicates that you have plenty of income left after covering your existing obligations, making you a more attractive borrower for a new car loan.

Income Stability and Employment History: Proof of Payment Capacity

Lenders want assurance that you have a steady, reliable source of income to make your monthly car loan payments. Your employment history provides this crucial insight. They’ll typically look for consistent employment over a period, often requiring at least six months to a year at your current job.

Longer employment at the same company demonstrates stability and a lower risk of sudden income loss. For self-employed individuals, lenders usually require at least two years of tax returns to prove consistent income. This ensures they have a clear picture of your earnings potential.

Common mistakes to avoid are changing jobs right before applying for a loan or having significant gaps in employment. These can raise red flags for lenders, suggesting potential instability in your income stream.

The Power of a Down Payment: Reducing Risk and Cost

Making a down payment on a car loan is one of the most effective ways to improve your chances of approval and secure more favorable terms. A down payment reduces the total amount you need to borrow, which in turn lowers your monthly payments and the overall interest paid over the life of the loan.

From a lender’s perspective, a down payment signals your financial commitment to the purchase and reduces their risk. If you default, they have a smaller principal amount to recover. Many experts recommend aiming for at least a 10% down payment for a used car and 20% for a new car, though even a smaller amount can make a difference.

Based on my experience, even a modest down payment can significantly impact your loan approval and interest rate, especially if your credit score is not in the excellent range. It shows good faith and financial responsibility.

Loan-to-Value (LTV) Ratio: Don’t Over-Finance

The loan-to-value (LTV) ratio compares the amount you borrow to the actual market value of the car you intend to purchase. Lenders calculate this to ensure they are not financing more than the vehicle is worth, which would put them at greater risk if you were to default.

For example, if a car is valued at $20,000 and you borrow $18,000, your LTV is 90%. A lower LTV, ideally below 100%, is generally preferred. This means your loan amount is less than or equal to the car’s value. If you borrow more than the car is worth (e.g., rolling over negative equity from a trade-in), your LTV will be over 100%, which can make approval harder and lead to higher interest rates.

Pro tips from us: Aim to keep your LTV as low as possible. A substantial down payment is an excellent way to achieve this. Avoiding add-ons that inflate the loan amount beyond the car’s actual value is also crucial.

Boosting Your Chances: Strategies for Success

Understanding what lenders look for is only half the battle. The other half involves proactively implementing strategies to make yourself a more attractive borrower. These steps can significantly improve your car loan chances, leading to better terms and a smoother buying experience.

Proactively Improve Your Credit Score

Since your credit score is so vital, taking steps to improve it before applying for a car loan is a highly effective strategy. This isn’t an overnight fix, but consistent effort can yield significant results. Start by ensuring all your bill payments are made on time, every time. Payment history is the largest factor in your credit score.

Next, focus on reducing your existing credit card debt. A lower credit utilization ratio (the amount of credit you’re using compared to your available credit) can quickly boost your score. Also, avoid opening new credit accounts right before applying for a car loan, as this can temporarily lower your score.

Get Pre-Approved: Your Secret Weapon

One of the most powerful steps you can take is getting pre-approved for a car loan before you even set foot in a dealership. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a certain interest rate. This offers numerous advantages.

Firstly, it provides you with a realistic budget, so you know exactly how much car you can afford. Secondly, it transforms you into a cash buyer at the dealership, giving you significant negotiating power on the car’s price. Thirdly, it allows you to identify any potential issues with your application early, giving you time to address them.

Shop Around for Lenders: Don’t Settle for the First Offer

Based on my experience, one of the most common mistakes people make is simply accepting the financing offered by the car dealership without exploring other options. While dealership financing can sometimes be competitive, it’s crucial to shop around. Banks, credit unions, and online lenders often offer varying rates and terms.

Apply to several different lenders within a short timeframe (usually 14-45 days, depending on the credit scoring model). Multiple inquiries for the same type of loan within this window are typically treated as a single inquiry, minimizing the impact on your credit score. Comparing offers empowers you to choose the best deal.

Consider a Co-Signer (If Necessary and Strategic)

If your credit history is thin or less than perfect, a co-signer might be the key to improving your car loan chances. A co-signer is someone with excellent credit who agrees to be equally responsible for the loan if you fail to make payments. This reduces the lender’s risk and can help you secure approval or a better interest rate.

However, choosing a co-signer is a serious decision with significant implications. Both your credit scores will be affected by the loan, and if you default, the co-signer is legally obligated to repay the debt. Pro tips from us: Only consider this option with someone you trust implicitly, and ensure both parties fully understand the responsibilities involved.

Choose the Right Vehicle: Aligning Affordability with Approval

The type of car you choose also impacts your loan chances. New cars typically have lower interest rates due to their higher resale value, which provides better collateral for the lender. Used cars can sometimes have higher rates, but their lower price point might make them more accessible.

It’s also essential to choose a vehicle that aligns with your budget and credit profile. Trying to finance a luxury car with a modest income and a fair credit score will significantly reduce your approval chances. For further insights on vehicle choices, our article offers more detailed comparisons.

Special Scenarios: Navigating Challenges

Not everyone has a pristine credit history or a hefty down payment. The good news is that even in challenging circumstances, getting a car loan is often possible. It simply requires a more strategic approach and an understanding of the specific options available.

Bad Credit Car Loans: A Path to Rebuilding

Having bad credit doesn’t automatically close the door on car ownership. Many lenders specialize in subprime auto loans, designed for individuals with lower credit scores. While approval is possible, it comes with important considerations.

Expect higher interest rates, as lenders perceive a greater risk. You might also be required to make a larger down payment or accept a shorter loan term to mitigate this risk. Pro tips from us: Focus on getting a reliable, affordable vehicle with a bad credit loan, and make every payment on time. This is an excellent opportunity to rebuild your credit history for future financial endeavors.

Common mistakes to avoid are falling for predatory lenders who offer excessively high-interest rates or hidden fees. Always read the fine print and compare offers, even with bad credit.

First-Time Car Buyer Loans: Establishing Your Credit

If you’re a first-time car buyer, you might lack a substantial credit history, which can be a hurdle. Lenders have no past behavior to assess, making them cautious. However, specific programs and strategies cater to this situation.

Some lenders offer first-time buyer programs with more lenient credit requirements, often requiring a co-signer or a larger down payment. Another option is a secured loan, where the car itself serves as collateral. Building a positive credit history with a smaller, manageable loan can pave the way for better terms on future purchases.

No Down Payment Car Loans: Weighing the Risks

While it’s possible to find "no down payment" car loans, they often come with downsides. Without a down payment, you’re borrowing the entire cost of the car, which means higher monthly payments and more interest paid over the loan’s life.

Additionally, you’re at a higher risk of becoming "upside down" or having negative equity – owing more on the car than it’s worth. This can happen quickly due to depreciation. While convenient, a zero down payment loan might not be the most financially prudent choice in the long run.

The Application Process: What to Expect

Once you’ve done your homework and identified potential lenders, the application process itself is fairly straightforward. Knowing what to expect can help you prepare and ensure a smooth experience.

Gathering Your Documents: Be Prepared

Lenders will require various documents to verify your identity, income, and residency. Typically, you’ll need:

- Government-issued photo identification (driver’s license, passport).

- Proof of income (recent pay stubs, tax returns for self-employed).

- Proof of residence (utility bill, lease agreement).

- Proof of insurance (you’ll need to secure this before driving off the lot).

Having these documents readily available will expedite the application process and demonstrate your preparedness to the lender.

Filling Out the Application: Accuracy is Key

When completing the loan application, ensure all information is accurate and consistent with your supporting documents. Any discrepancies can cause delays or even lead to denial. Be honest about your financial situation; lenders will verify the information you provide.

Don’t rush through the application. Take your time to double-check all fields. This attention to detail reflects positively on you as a borrower.

Understanding the Offer: Read the Fine Print

Once approved, you’ll receive a loan offer outlining the terms. This is a critical moment to review everything carefully before signing. Pay close attention to:

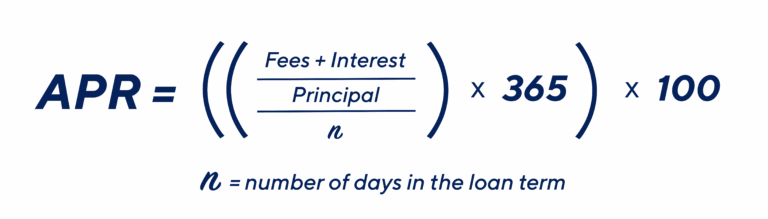

- Annual Percentage Rate (APR): This is the total cost of borrowing, including interest and fees, expressed as a yearly percentage.

- Loan Term: The length of time you have to repay the loan (e.g., 60 months, 72 months). Longer terms mean lower monthly payments but more interest paid over time.

- Monthly Payment: Ensure this fits comfortably within your budget.

- Any Fees: Look for origination fees, document fees, or prepayment penalties.

Pro tips from us: Don’t hesitate to ask questions if anything is unclear. It’s your right to understand every aspect of your loan agreement before committing.

Beyond Approval: Maintaining Financial Health

Securing a car loan is a significant achievement, but the journey doesn’t end there. Responsible management of your car loan can have a lasting positive impact on your financial health and future borrowing opportunities.

Budgeting for Car Ownership: More Than Just Payments

Remember that the monthly car payment is just one component of car ownership. You’ll also need to budget for:

- Car Insurance: This is a legal requirement and can vary significantly based on your vehicle, location, and driving history.

- Fuel Costs: A major ongoing expense, especially with fluctuating gas prices.

- Maintenance and Repairs: Regular servicing and unexpected repairs are inevitable. Setting aside an emergency fund for this is wise.

- Registration and Licensing Fees: Annual costs to keep your vehicle legal.

Failing to account for these additional costs is a common mistake that can strain your budget, even if you comfortably afford the car payment.

Making Payments on Time: Building Your Credit Legacy

Consistently making your car loan payments on time is paramount. Each on-time payment reinforces your positive credit history, slowly building your credit score. This discipline will benefit you when you apply for other loans, such as a mortgage, in the future.

Set up automatic payments if possible to avoid missed due dates. If you anticipate difficulty making a payment, contact your lender immediately. They may offer options like deferment, though this isn’t guaranteed.

Refinancing Options: Seizing Better Opportunities

As your credit score improves over time or if interest rates drop, you might have the opportunity to refinance your car loan. Refinancing involves taking out a new loan to pay off your existing one, often with a lower interest rate or a more favorable term.

This can significantly reduce your monthly payments or the total amount of interest you pay over the life of the loan. It’s worth exploring refinancing options after you’ve made a consistent string of on-time payments and seen an improvement in your credit profile. For official information on credit reports and scores, resources like the Consumer Financial Protection Bureau (CFPB) provide excellent guidance.

Conclusion: Drive Away with Confidence

Understanding your chances of getting a car loan boils down to preparation, knowledge, and strategic action. By focusing on the key factors lenders evaluate – your credit score, DTI ratio, income stability, and down payment – you can significantly improve your eligibility. Implementing strategies like pre-approval and shopping around for lenders will empower you to secure the best possible terms.

Whether you have excellent credit or are navigating challenges like a limited history or past financial setbacks, there’s often a path to car ownership. The most important takeaway is to be informed, honest with yourself about your financial capacity, and diligent in your approach. With this comprehensive guide, you’re now equipped with the insights needed to confidently pursue your next vehicle and drive away knowing you’ve made a smart financial decision.