Unlocking Your Drive: A Deep Dive into American Heritage Car Loan Rates

Unlocking Your Drive: A Deep Dive into American Heritage Car Loan Rates Carloan.Guidemechanic.com

The open road beckons, and a new car, or perhaps a reliable used one, often feels like the key to unlocking new possibilities. Yet, the journey to vehicle ownership often involves navigating the complex world of financing. For many in the Greater Philadelphia area and beyond, American Heritage Credit Union stands out as a strong contender for auto loans. But what truly defines American Heritage car loan rates, and how can you ensure you secure the best possible deal?

Based on my extensive experience in consumer finance, understanding not just the numbers, but the underlying factors and the application process, is crucial. This comprehensive guide will peel back the layers, offering an in-depth look at American Heritage Credit Union’s auto loan offerings, from deciphering their rates to mastering the application process and beyond. Our ultimate goal is to equip you with the knowledge to make an informed decision, potentially saving you thousands over the life of your loan.

Unlocking Your Drive: A Deep Dive into American Heritage Car Loan Rates

Understanding the American Heritage Advantage: Why a Credit Union?

Before diving into rates, it’s essential to grasp what makes American Heritage Credit Union, and credit unions in general, distinct from traditional banks. This fundamental difference often translates directly into more favorable terms for members.

Credit unions are not-for-profit financial cooperatives owned by their members. Unlike banks, which are driven by shareholder profits, credit unions return their earnings to members in the form of lower loan rates, higher savings rates, and fewer fees. This member-centric philosophy is a cornerstone of the credit union model.

American Heritage Credit Union, specifically, serves a broad community, offering a full suite of financial products and services. Their mission focuses on improving the financial well-being of their members. This commitment often manifests in highly competitive car loan rates and a more personalized service experience.

Deciphering American Heritage Car Loan Rates: What Influences the Numbers?

When you look at advertised car loan rates, whether from American Heritage or any other lender, it’s important to understand that these are often "starting from" rates. Your individual rate will be determined by a confluence of factors unique to your financial profile and the specific loan you seek.

Pro tips from us: Never assume you’ll get the lowest advertised rate without first understanding these influencing elements. Being prepared is half the battle.

Here’s a detailed breakdown of what typically shapes American Heritage car loan rates:

1. Your Credit Score: The Ultimate Predictor

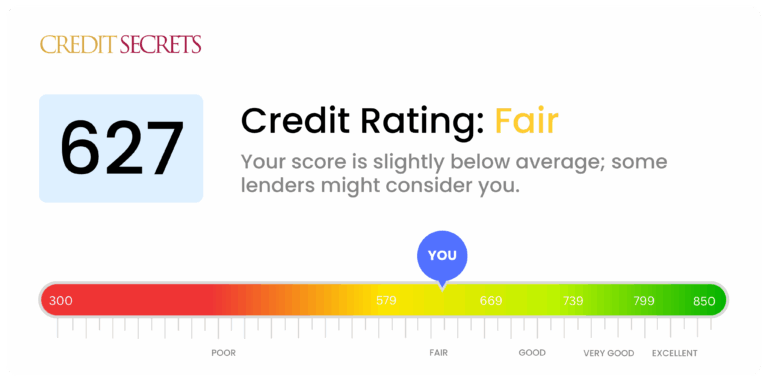

Your credit score is arguably the single most impactful factor in determining the interest rate you’ll receive on an auto loan. Lenders, including American Heritage, use this three-digit number to assess your creditworthiness and the likelihood of you repaying the loan. A higher score signals lower risk, which usually translates to a lower interest rate.

FICO scores, which range from 300 to 850, are the most commonly used. Generally, scores above 720 are considered excellent, while those between 660-719 are good. If your score falls into the "good" or "excellent" categories, you’re more likely to qualify for American Heritage’s most competitive rates.

Common mistakes to avoid are applying for a loan without checking your credit score first. This leaves you guessing and unable to address any inaccuracies or areas for improvement.

2. The Loan Term: Length Matters

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). While a longer loan term means lower monthly payments, it almost always results in a higher total amount of interest paid over the life of the loan.

Lenders often charge higher interest rates for longer terms because they are taking on more risk over an extended period. Conversely, shorter terms usually come with lower interest rates but higher monthly payments. It’s a critical balance to strike based on your budget and financial goals.

Based on my experience, many people get fixated solely on the monthly payment. While important, always consider the total cost of the loan across different terms.

3. Your Down Payment: Reducing Risk, Reducing Rates

Making a substantial down payment on your vehicle can significantly impact the interest rate you’re offered. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. When the lender’s risk decreases, they are often willing to offer more attractive interest rates.

Additionally, a healthy down payment helps prevent you from being "upside down" on your loan, meaning you owe more than the car is worth. This provides an added layer of security for both you and American Heritage Credit Union.

Pro tips from us: Aim for at least 10-20% down on a new car, and potentially more for a used vehicle, to see a noticeable positive impact on your loan terms.

4. Vehicle Type and Age: New vs. Used, and More

The type of vehicle you intend to purchase also plays a role. New cars often qualify for slightly lower interest rates than used cars. This is because new cars typically depreciate slower initially, have warranties, and are generally seen as less risky by lenders.

For used cars, the age and mileage can also influence the rate. An older, high-mileage vehicle might be deemed a higher risk due to potential mechanical issues, leading to a slightly higher interest rate. American Heritage, like other lenders, will factor in the collateral’s value and expected lifespan.

5. Debt-to-Income Ratio (DTI): Your Financial Bandwidth

Your debt-to-income ratio (DTI) is a percentage that compares your total monthly debt payments to your gross monthly income. Lenders use DTI to assess your ability to take on additional debt and manage your payments. A lower DTI indicates you have more disposable income available to cover your car loan payments.

American Heritage will look for a DTI that suggests you are not overextended financially. A DTI below 36% is often considered ideal, though this can vary depending on other factors in your application.

The American Heritage Car Loan Application Process: A Step-by-Step Guide

Securing a car loan with American Heritage Credit Union is designed to be a straightforward and member-friendly process. Knowing what to expect can ease any anxieties and help you prepare thoroughly.

1. Pre-Approval: Your Strategic Advantage

Based on my experience, seeking pre-approval is one of the smartest moves you can make before stepping onto a dealership lot. Pre-approval means American Heritage Credit Union has reviewed your financial information and tentatively agreed to lend you a specific amount at a particular interest rate.

Benefits of pre-approval include:

- Clear Budget: You know exactly how much car you can afford.

- Negotiating Power: You become a cash buyer, giving you leverage at the dealership.

- Rate Certainty: You lock in a rate, protecting you from surprises.

- Time Savings: Streamlines the purchasing process.

To get pre-approved, you’ll typically provide information similar to a full application, including your income, employment history, and authorization for a credit check.

2. Required Documentation: Be Prepared

When you’re ready to apply, whether for pre-approval or a final loan, having your documents in order will expedite the process. Common documents requested by American Heritage include:

- Proof of Identity: Valid government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs, W-2s, or tax returns (for self-employed individuals).

- Proof of Residency: Utility bill or lease agreement.

- Vehicle Information: If you’ve already chosen a car, details like VIN, make, model, and mileage.

Gathering these items beforehand will make your application smooth and efficient.

3. Submitting Your Application: Online or In-Branch

American Heritage Credit Union offers convenient ways to apply for a car loan:

- Online Application: This is often the quickest method, allowing you to apply from the comfort of your home.

- In-Branch Visit: If you prefer face-to-face interaction or have specific questions, visiting a local American Heritage branch allows you to speak directly with a loan officer.

The choice depends on your personal preference and how quickly you need a decision.

4. The Decision and Closing: Finalizing Your Loan

Once your application is submitted, American Heritage will review your information, including your credit report and financial history. They will then notify you of their decision. If approved, you’ll receive the specific loan terms, including your interest rate, loan amount, and monthly payment schedule.

The final step involves signing the loan documents. This is where you’ll agree to all the terms and conditions. Be sure to read everything carefully and ask any questions you have before signing.

Pro Strategies to Secure the Best American Heritage Car Loan Rates

While many factors influence your rate, there are proactive steps you can take to put yourself in the strongest possible position to secure the most favorable terms from American Heritage Credit Union.

1. Elevate Your Credit Score

This is paramount. A higher credit score directly translates to lower interest rates.

- Pay Bills On Time: Payment history is the most significant factor in your credit score.

- Reduce Debt: Lowering your credit utilization (the amount of credit you’re using compared to your total available credit) can quickly boost your score.

- Check Your Credit Report: Dispute any errors immediately. For a deeper dive, check out our guide on How to Improve Your Credit Score for Better Loan Rates. (Internal Link Example)

2. Build a Substantial Down Payment

As discussed, a larger down payment reduces the loan amount and the lender’s risk. Aim for 20% if possible, especially for new vehicles. This not only lowers your monthly payments but also reduces the total interest you’ll pay over time.

Consider setting up a dedicated savings account specifically for your car down payment. Even small, consistent contributions add up.

3. Shop Around (Even Within AHCU’s Offerings)

While focusing on American Heritage, it’s wise to compare their rates and terms with a few other reputable lenders, especially other credit unions. This ensures you’re getting a competitive offer. However, limit your applications to avoid multiple hard inquiries on your credit report within a short period, which can temporarily lower your score.

Also, inquire about different loan products or promotions American Heritage might be offering. Sometimes there are special rates for specific vehicle types or during certain times of the year.

4. Consider a Co-signer (When Appropriate)

If your credit score is less than ideal, or you’re a first-time borrower with limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate.

A co-signer essentially guarantees the loan, taking on equal responsibility for repayment. This is a big ask, so ensure both parties understand the commitment involved.

5. Understand Refinancing Options

If you already have a car loan with a higher interest rate, American Heritage Credit Union might offer refinancing options. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms.

This can be a great strategy if your credit score has improved since you first took out the loan, or if interest rates have dropped. It’s always worth exploring if you can save money on your current vehicle.

Common Mistakes to Avoid When Applying for a Car Loan

Navigating the car loan process can be tricky, and certain pitfalls can cost you money and peace of mind. Here are common mistakes to steer clear of:

- Focusing Solely on Monthly Payments: While your monthly budget is important, fixating only on the lowest monthly payment can lead to longer loan terms and significantly more interest paid over time. Always ask for the total cost of the loan.

- Skipping Pre-Approval: As emphasized, going to the dealership without pre-approval puts you at a disadvantage. You lose negotiating power and might feel pressured into dealership financing that isn’t the best deal.

- Ignoring the Fine Print: Always read your loan agreement thoroughly before signing. Understand all fees, prepayment penalties (though rare with credit unions), and specific terms.

- Applying to Too Many Lenders at Once: While shopping around is good, submitting applications to a dozen different lenders in a short period can negatively impact your credit score due to multiple hard inquiries. Group your inquiries within a 14-45 day window to have them count as a single inquiry for scoring purposes.

- Underestimating Additional Costs: Remember to factor in insurance, registration, maintenance, and fuel costs beyond just your car payment. A car loan is just one piece of the ownership puzzle.

Beyond the Rate: The American Heritage Advantage

While competitive rates are a major draw, choosing American Heritage Credit Union for your car loan extends beyond just the numbers. Their credit union model offers several distinct advantages that enhance the overall member experience.

- Personalized Service: As a member, you’re not just a customer; you’re an owner. This often translates into more personalized attention and support from loan officers who genuinely want to help you achieve your financial goals.

- Financial Education Resources: American Heritage often provides resources and workshops to help members improve their financial literacy, which can be invaluable when making significant financial decisions like a car purchase.

- Community Involvement: Credit unions are deeply rooted in their communities. By choosing American Heritage, you’re supporting an institution that invests back into the local area.

- Member Benefits: Beyond car loans, membership opens the door to other competitive products and services, including savings accounts, checking accounts, mortgages, and more.

- Safety and Security: American Heritage Credit Union is federally insured by the National Credit Union Administration (NCUA), an independent agency of the U.S. government. This means your deposits are insured up to at least $250,000, just like FDIC insurance for banks. You can learn more about NCUA insurance at NCUA.gov. (External Link Example)

Conclusion: Driving Towards Smart Car Ownership with American Heritage

Securing a car loan is a significant financial decision that impacts your budget for years to come. By thoroughly understanding American Heritage car loan rates, the factors that influence them, and the strategic steps you can take, you empower yourself to make the best choice.

American Heritage Credit Union, with its member-focused philosophy, often provides competitive rates, flexible terms, and a supportive application process. Remember that your credit score, loan term, and down payment are powerful levers you can pull to influence your final rate. By being prepared, leveraging pre-approval, and avoiding common mistakes, you can drive away with not just a new vehicle, but also a smart financial decision.

We encourage you to visit American Heritage Credit Union’s website or one of their branches to discuss your specific car loan needs. With the right approach, your journey to car ownership can be both exciting and financially sound.