Unlocking Your Drive: The Definitive Guide to a Car Loan Calculator With Total Interest Paid

Unlocking Your Drive: The Definitive Guide to a Car Loan Calculator With Total Interest Paid Carloan.Guidemechanic.com

Dreaming of a new set of wheels? For most of us, buying a car involves taking out a loan. While the excitement of a new vehicle is undeniable, the reality of car financing can often feel like navigating a complex maze. Many prospective buyers focus solely on the monthly payment, overlooking a critical figure that significantly impacts their financial health: the total interest paid over the life of the loan.

Understanding the true cost of your car loan, beyond just the sticker price and monthly commitment, is paramount. This is where a robust car loan calculator with total interest paid becomes your indispensable co-pilot. It’s not just a tool; it’s your financial compass, guiding you toward informed decisions and potentially saving you thousands of dollars. In this comprehensive guide, we’ll peel back the layers of auto financing, empowering you to calculate, understand, and strategically reduce your total interest burden.

Unlocking Your Drive: The Definitive Guide to a Car Loan Calculator With Total Interest Paid

Why Your Focus Should Shift: Beyond Monthly Payments to Total Interest Paid

It’s easy to get fixated on the "affordability" of a monthly car payment. A lower monthly payment often feels like a win, especially when budgeting. However, this narrow focus can be a significant financial pitfall.

Based on my experience as a financial blogger specializing in consumer credit, prioritizing only the monthly payment is one of the most common and costly mistakes borrowers make. Lenders know this and often structure loans, particularly longer-term ones, to offer seemingly attractive low monthly payments. What they don’t always highlight is how these extended terms dramatically inflate the total interest you’ll pay.

A car loan calculator that specifically highlights the total interest paid brings transparency to the entire financing process. It shifts your perspective from a short-term budgetary convenience to a long-term financial commitment. By seeing the full picture, you can make smarter choices that align with your financial goals, not just your immediate desire for a new car.

Deconstructing the Car Loan Calculator: Key Components You Need to Know

To effectively use a car loan calculator and grasp its output, you must first understand the fundamental variables that feed into it. Each component plays a crucial role in determining both your monthly payment and the total interest you’ll ultimately pay.

1. The Vehicle’s Purchase Price (Loan Amount)

This is the starting point. The purchase price is the agreed-upon cost of the vehicle before any down payment, trade-in, taxes, or fees. It directly impacts the principal amount you’ll need to borrow. The higher the purchase price, the larger your loan amount will be, assuming other factors remain constant.

It’s vital to negotiate the best possible purchase price before discussing financing. Every dollar you shave off the purchase price directly reduces the amount you need to finance, which in turn reduces the total interest you’ll pay over time. Don’t let the financing discussion distract you from getting a fair deal on the car itself.

2. Your Down Payment

A down payment is the initial amount of cash you pay upfront toward the vehicle’s purchase price. This reduces the principal loan amount you need to borrow. For example, if a car costs $30,000 and you put down $5,000, you’re only financing $25,000.

The benefits of a larger down payment are multifaceted. Firstly, it immediately lowers your monthly payment. More importantly, it significantly decreases the total interest paid because you’re borrowing less money. Additionally, a substantial down payment can sometimes help you secure a better interest rate from lenders, as it signals less risk.

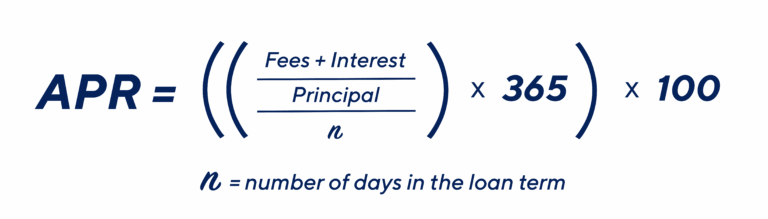

3. The Interest Rate (APR – Annual Percentage Rate)

The interest rate, often expressed as an Annual Percentage Rate (APR), is arguably the most critical factor affecting your total interest paid. It’s essentially the cost of borrowing money, expressed as a percentage of the principal loan amount. A higher APR means you’ll pay more for the privilege of borrowing.

Your APR is influenced by several factors, including your credit score, the loan term, the economy’s prime rate, and the lender’s specific policies. A good credit score is your best friend here, as it typically qualifies you for the lowest available rates. Always compare APRs from multiple lenders, not just the monthly payment, to find the most cost-effective loan.

4. The Loan Term (Duration)

The loan term refers to the length of time you have to repay the loan, usually expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This factor has a dual impact on your finances. A longer loan term generally results in lower monthly payments, which can seem appealing.

However, a longer term also means you’re paying interest for a longer period, significantly increasing the total interest paid over the life of the loan. Conversely, a shorter loan term will lead to higher monthly payments but drastically reduce the total interest you accrue. Finding the right balance between affordability and minimizing interest is key.

5. Trade-in Value (if applicable)

If you have an existing vehicle you plan to sell or trade in, its value can act much like a down payment. The agreed-upon trade-in value is subtracted from the purchase price of your new car, reducing the amount you need to finance.

Just like a cash down payment, a strong trade-in value lowers your principal loan amount, thereby decreasing both your monthly payments and the total interest you’ll pay. It’s wise to research your car’s trade-in value independently before visiting the dealership to ensure you’re getting a fair offer.

Your Step-by-Step Guide: How to Use a Car Loan Calculator Effectively

Using a car loan calculator, especially one that emphasizes total interest paid, is straightforward once you understand its inputs. Here’s how to maximize its utility:

-

Gather Your Data: Before you even open the calculator, have these figures ready:

- Vehicle Price: The negotiated selling price of the car.

- Down Payment: How much cash you plan to put down.

- Trade-in Value (if any): The estimated or agreed-upon value of your old car.

- Interest Rate (APR): The rate you’ve been offered or anticipate based on your credit score.

- Loan Term: The number of months you’re considering for repayment.

-

Input the Information:

- Enter the

Vehicle Price. - Input your

Down Paymentamount. - Add your

Trade-in Value(if applicable). Many calculators will automatically subtract these from the vehicle price to determine theLoan Amount. - Enter the

Interest Rate(APR). Make sure to input it as a percentage (e.g., 5.5 for 5.5%). - Select or input your desired

Loan Termin months.

- Enter the

-

Calculate and Analyze the Results:

- Click the "Calculate" or "Submit" button.

- The calculator will instantly display:

- Monthly Payment: The amount you’ll owe each month.

- Total Interest Paid: The entire sum of interest you will pay over the life of the loan.

- Total Cost of Loan: The sum of the principal loan amount plus the total interest paid.

- Sometimes, it will also show the

Total Cost of Car, which is the total loan cost plus your down payment and trade-in difference.

-

Experiment with Scenarios: This is where the calculator truly shines. Don’t just run one calculation.

- Try different down payment amounts to see how it impacts total interest.

- Adjust the loan term (e.g., 60 months vs. 72 months) to observe the trade-off between monthly payment and total interest.

- If you have varying interest rate offers, input each one to compare their impact on the overall cost. This experimentation empowers you to find the sweet spot that balances affordability with minimizing long-term costs.

Understanding Amortization: The Heart of Your Car Loan

When you take out a car loan, you’re not just paying back the principal (the amount you borrowed); you’re also paying interest on that principal. The process of gradually paying off a loan over time through a series of regular payments is called amortization.

What’s crucial to understand about amortization, especially with car loans, is how interest is calculated and applied. In the initial stages of your loan, a larger portion of your monthly payment goes towards paying off the interest. As the loan matures, and your principal balance decreases, a greater percentage of each payment then goes towards reducing the principal.

This front-loading of interest means that early on, you’re primarily covering the cost of borrowing the money. Because of this, even small extra payments directed specifically towards the principal in the early years can have a disproportionately large impact on reducing your total interest paid and shortening your loan term. This insight is a powerful tool for strategic repayment.

Smart Strategies to Drastically Reduce Your Total Interest Paid

Minimizing the total interest you pay on a car loan is a direct path to significant savings. Here are several proven strategies:

1. Maximize Your Down Payment

As discussed, a larger down payment reduces the principal loan amount. Less principal means less interest accrues over time. Aim for at least 10-20% of the vehicle’s purchase price if possible.

Pro tips from us: If you can’t save a large down payment immediately, consider delaying your purchase for a few months to accumulate more funds. The long-term savings will often outweigh the short-term wait. Also, remember your trade-in counts towards your down payment.

2. Opt for the Shortest Loan Term You Can Afford

While longer terms offer lower monthly payments, they come at the steep cost of increased total interest. A 60-month loan will almost always result in significantly less total interest than a 72-month or 84-month loan for the same amount and interest rate.

Use your car loan calculator with total interest paid to compare the total interest paid on different loan terms. You might find that stretching your budget slightly for a shorter term yields substantial savings in the long run. It’s a trade-off worth exploring.

3. Boost Your Credit Score for a Lower APR

Your credit score is a direct reflection of your creditworthiness to lenders. A higher credit score (generally above 700) indicates less risk, allowing you to qualify for lower interest rates. Even a difference of one or two percentage points on your APR can save you hundreds, if not thousands, in total interest.

Before applying for a car loan, check your credit report for errors and work to improve your score. Pay bills on time, reduce existing debt, and avoid opening new credit accounts. can provide more detailed steps.

4. Shop Around and Compare Offers from Multiple Lenders

Never take the first financing offer you receive, especially not just from the dealership. Dealerships often have partnerships with specific lenders, but they might not always offer you the best rate.

Seek pre-approval from banks, credit unions, and online lenders before you even step foot on a dealership lot. Having multiple loan offers in hand gives you leverage to negotiate for the best possible APR and terms. This competitive shopping is one of the most effective ways to reduce your interest rate.

5. Consider Refinancing Your Car Loan

If you already have a car loan but your credit score has improved, interest rates have dropped, or you found a better offer, refinancing could be a smart move. Refinancing involves taking out a new loan to pay off your existing car loan, ideally with a lower interest rate or better terms.

Refinancing can significantly reduce your total interest paid, especially if you can secure a much lower APR or shorten your loan term. offers an in-depth look at this option.

6. Make Extra Payments (Especially Principal-Only Payments)

Even small extra payments can make a big difference, particularly if directed towards the principal. Since interest is calculated on the remaining principal balance, reducing that balance faster means less interest accrues.

Check with your lender to ensure extra payments are applied directly to the principal and that there are no prepayment penalties. Even rounding up your monthly payment by $20-$50 can shave off months from your loan term and hundreds from your total interest.

Common Mistakes to Avoid When Financing a Car

Navigating car financing can be tricky, and certain missteps can cost you dearly. Being aware of these common pitfalls can help you avoid them.

1. Focusing Solely on the Monthly Payment

As highlighted earlier, this is perhaps the biggest mistake. A low monthly payment might seem attractive, but if it comes with an extended loan term and a high interest rate, you’ll end up paying far more in total. Always evaluate the total cost of the loan, including total interest paid, not just the monthly installment.

2. Ignoring the Annual Percentage Rate (APR)

The APR is the true cost of borrowing. Some borrowers get distracted by promotional offers or disregard the APR in favor of a low monthly payment. A high APR will always lead to more interest paid, regardless of the principal amount or term. Always demand to know the APR and compare it across lenders.

3. Not Getting Pre-Approved Before Shopping

Walking into a dealership without pre-approved financing is like walking into a negotiation blindfolded. Without a solid loan offer in hand, you have no benchmark. Dealers might try to inflate the interest rate or bundle in unnecessary add-ons. Pre-approval gives you a strong negotiating position and clarity on your budget.

4. Extending the Loan Term Excessively

While longer terms mean lower monthly payments, they expose you to more interest over time and increase the risk of being "upside down" on your loan (owing more than the car is worth). This can be problematic if you need to sell or trade in the car before the loan is paid off. Aim for the shortest term that fits comfortably within your budget.

5. Forgetting About Hidden Fees and Add-ons

Dealerships often offer extended warranties, GAP insurance, service contracts, and other add-ons. While some might be valuable, others are unnecessary and significantly increase your loan amount, thereby increasing the total interest you’ll pay. Scrutinize every line item and only accept what you truly need or want.

6. Not Understanding the Full Cost of Ownership

Your car loan payment is just one piece of the puzzle. Overlooking insurance, maintenance, fuel, and depreciation means you’re not seeing the full financial picture. A holistic view ensures you can truly afford the car.

Beyond the Calculator: Other Crucial Factors to Consider for Car Ownership

While a car loan calculator with total interest paid is an essential tool, responsible car ownership extends beyond just the loan. To truly budget for a vehicle, you must consider the full spectrum of costs.

1. Car Insurance Costs

This is often a significant ongoing expense. Insurance premiums vary wildly based on the car’s make and model, your driving history, age, location, and the type of coverage you choose. Always get insurance quotes for specific vehicles before committing to a purchase.

2. Maintenance and Repairs

Every car, new or used, will require maintenance. Oil changes, tire rotations, brake pads, and unforeseen repairs are part of ownership. Newer cars typically have lower initial maintenance costs but can become expensive as they age. Factor these potential costs into your monthly budget.

3. Fuel Expenses

The type of car you choose directly impacts your fuel budget. A fuel-efficient compact car will cost significantly less to run than a large SUV or a sports car. Consider your daily commute and typical driving habits when evaluating a car’s fuel economy.

4. Depreciation

Cars are depreciating assets, meaning they lose value over time. While not a direct loan cost, depreciation is a crucial factor in the overall financial impact of car ownership. Some cars hold their value better than others. Researching a vehicle’s depreciation rate can give you a clearer picture of its long-term cost.

For a deeper dive into car ownership costs, reputable sources like Edmunds.com or Kelley Blue Book (KBB.com) offer excellent tools and data on True Cost to Own.

The Power of Knowledge: Making Informed Decisions

The journey to owning a car should be exciting, not financially draining. By harnessing the power of a car loan calculator with total interest paid, you transform from a passive borrower into an informed and empowered consumer. You gain the ability to visualize the long-term financial implications of your choices, compare different financing scenarios, and negotiate from a position of strength.

Understanding how interest works, what influences your loan terms, and the strategies to minimize your costs means you’re not just buying a car; you’re making a smart investment in your financial future.

Conclusion: Drive Smarter, Not Harder

Navigating the world of car financing doesn’t have to be intimidating. With the right tools and knowledge, you can ensure your next vehicle purchase is a financially sound one. A car loan calculator with total interest paid is more than just a numbers cruncher; it’s a strategic partner that reveals the true cost of your loan, empowering you to make choices that align with your budget and financial goals.

Remember to prioritize a larger down payment, aim for a shorter loan term, strive for a strong credit score, and always compare offers from multiple lenders. By avoiding common pitfalls and focusing on the total interest paid, you can save thousands of dollars over the life of your car loan. Drive smarter, understand your financing, and enjoy the open road with financial peace of mind.