Unlocking Your Drive: The Definitive Guide to Car Loan APR and How to Get the Best Deal

Unlocking Your Drive: The Definitive Guide to Car Loan APR and How to Get the Best Deal Carloan.Guidemechanic.com

The thrill of a new car, the freedom of the open road – it’s a dream many of us share. But before you get behind the wheel, there’s a crucial financial component that can significantly impact your ownership experience: the Annual Percentage Rate (APR) of your car loan. Understanding car loan APR isn’t just about knowing a number; it’s about mastering the true cost of your vehicle and empowering yourself to make smart financial decisions.

As an expert blogger and professional in personal finance, I’ve seen firsthand how a lack of understanding about APR can lead to thousands of dollars in unnecessary expenses over the life of a loan. This comprehensive guide is designed to demystify car loan APR, provide you with actionable strategies, and ensure you drive away with the best possible deal. Let’s dive deep into everything you need to know about your car loan’s APR.

Unlocking Your Drive: The Definitive Guide to Car Loan APR and How to Get the Best Deal

What Exactly is Car Loan APR? Beyond Just the Interest Rate

When you borrow money to buy a car, you’re not just paying back the principal amount; you’re also paying for the privilege of borrowing that money. This cost comes in two primary forms: the interest rate and various fees. The Annual Percentage Rate (APR) is a standardized measure that bundles both the interest rate and most associated fees into a single, comprehensive percentage.

Think of the interest rate as the base price for borrowing. It’s what the lender charges you for using their money, expressed as a percentage of the principal balance. However, the APR goes a step further. It includes the interest rate plus other mandatory charges and fees involved in securing the loan, such as origination fees, documentation fees, and sometimes even credit report fees, if they are financed into the loan. This makes the APR a much more accurate reflection of the total annual cost of your car loan.

Pro Tip from us: Always focus on the APR, not just the advertised interest rate. A lower interest rate might look appealing, but if it comes with high hidden fees, your actual APR could be significantly higher, meaning you pay more in the long run.

Why Does Your Car Loan APR Matter So Much? The Real Cost of Borrowing

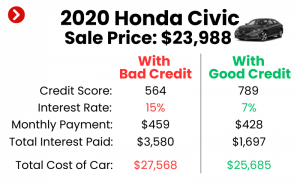

Understanding your car loan APR is absolutely critical because it directly dictates the total cost of your vehicle purchase. A seemingly small difference in APR can translate into hundreds, or even thousands, of dollars over the life of your loan. This impacts your monthly payments and, more importantly, the overall financial burden of your car.

Consider this: a $30,000 car loan over five years at a 5% APR will cost you significantly less than the same loan at a 9% APR. While the monthly payment difference might seem manageable, the cumulative effect over 60 months is substantial. A higher APR means more of your monthly payment goes towards interest, extending the time it takes to build equity in your vehicle and increasing the total amount you repay.

Based on my experience, many car buyers get fixated on the monthly payment figure alone. While important for budgeting, it can be misleading if you don’t consider the underlying APR. Lenders can easily reduce your monthly payment by simply extending the loan term, but this often means you pay much more in interest over time due to a higher total repayment and potentially a higher APR. Always weigh the monthly payment against the total cost of the loan, which is heavily influenced by the APR.

The Key Players: Factors That Influence Your Car Loan APR

The APR you qualify for isn’t arbitrary; it’s a carefully calculated figure based on a range of factors that lenders use to assess their risk. Understanding these elements puts you in a stronger negotiating position.

1. Your Credit Score: The Cornerstone of Your Loan Application

Your credit score is arguably the most significant factor influencing your car loan APR. It’s a three-digit number that summarizes your creditworthiness, indicating how reliably you’ve managed debt in the past. Lenders use this score to predict the likelihood of you repaying your loan on time.

Individuals with excellent credit scores (typically 720 and above) are considered low-risk borrowers. They generally qualify for the most favorable APRs because lenders are confident in their ability to repay. Conversely, those with lower credit scores (below 620) are seen as higher risk, leading to higher APRs to compensate the lender for that increased risk. Building and maintaining a strong credit score is paramount for securing a competitive car loan APR.

2. The Loan Term: Shorter Paths Often Mean Lower Rates

The length of your loan, known as the loan term, also plays a crucial role in determining your APR. Generally, shorter loan terms (e.g., 36 or 48 months) tend to come with lower APRs compared to longer terms (e.g., 72 or 84 months). This is because a shorter term reduces the lender’s exposure to risk over time.

While a longer loan term might offer lower monthly payments, making the car seem more affordable, it often results in a higher APR and significantly more interest paid over the life of the loan. This is a common trap for buyers focusing solely on the monthly budget. Always evaluate the trade-off between monthly payment affordability and the total cost of interest.

3. Your Down Payment: Showing Your Commitment

Making a substantial down payment signals to lenders that you are financially committed to the vehicle and less likely to default on the loan. A larger down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk.

When you put more money down upfront, you’re financing less, which often translates to a lower APR. Furthermore, a larger down payment helps you avoid being "upside down" on your loan, where you owe more than the car is worth, especially in the early years of ownership.

4. Vehicle Type and Age: New vs. Used, Luxury vs. Economy

The car itself can influence your APR. Newer vehicles often qualify for slightly lower APRs than used cars. This is because new cars typically hold their value better initially, making them more secure collateral for the lender. Used cars, especially older models, carry higher depreciation risk and may require higher APRs.

Similarly, the type of vehicle – a luxury SUV versus a basic sedan – can also impact the loan terms. Lenders consider the resale value and overall market demand when assessing the risk associated with the collateral.

5. Lender Type: Banks, Credit Unions, Dealerships, and Online Lenders

Different types of lenders offer varying APRs and terms.

- Banks are traditional institutions offering competitive rates, especially to customers with good credit.

- Credit unions are member-owned and often provide some of the best APRs due to their non-profit status.

- Dealership financing can be convenient, but their rates might not always be the most competitive, as they often mark up rates for profit. However, some dealerships offer special promotional rates from manufacturer financing arms.

- Online lenders have become increasingly popular, offering quick pre-approvals and competitive rates, often leveraging technology for efficiency.

Shopping around with multiple lender types is a key strategy for finding the lowest APR.

6. Market Conditions: The Broader Economic Picture

The overall economic environment and prevailing interest rates set by central banks (like the Federal Reserve in the U.S.) can also affect car loan APRs. When interest rates are generally low across the economy, car loan APRs tend to be lower, and vice-versa. While you can’t control market conditions, being aware of them helps you understand why rates might be higher or lower at certain times.

7. Debt-to-Income Ratio (DTI): Your Financial Bandwidth

Lenders also look at your debt-to-income ratio (DTI), which compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income available to comfortably make your car loan payments, signifying lower risk to the lender and potentially qualifying you for a better APR. A high DTI suggests you might be stretched thin financially, leading to a higher perceived risk and consequently, a higher APR.

Decoding the Application Process: How Lenders Determine Your APR

The process of getting a car loan and the subsequent APR offer involves several steps where lenders assess your financial profile.

- Application Submission: You provide personal and financial details, including your income, employment history, existing debts, and desired loan amount.

- Credit Check: With your permission, the lender pulls your credit report from one or more credit bureaus. This is a "hard inquiry" that temporarily impacts your credit score but is necessary for loan approval.

- Underwriting: An underwriter reviews all the provided information, including your credit score, DTI, employment stability, and the value of the vehicle you intend to purchase. They use this holistic view to assess your risk profile.

- Risk Assessment & APR Assignment: Based on their internal models and your risk profile, the lender assigns an APR that they believe is appropriate. Borrowers with lower risk profiles receive lower APRs, while higher-risk borrowers face higher rates.

Strategies to Secure the Best Possible Car Loan APR

Now that you understand what influences your APR, let’s explore actionable strategies to help you secure the most favorable terms.

1. Boost Your Credit Score: The Long-Term Investment

Improving your credit score is the single most effective way to lower your car loan APR.

- Pay bills on time, every time: Payment history is the biggest factor in your score.

- Reduce outstanding debt: Especially credit card balances, as high utilization hurts your score.

- Check your credit report regularly: Dispute any errors that could be dragging your score down. You can get free copies from AnnualCreditReport.com.

- Avoid opening new credit accounts: Especially in the months leading up to a car loan application, as this can temporarily lower your score.

For more detailed guidance, consider reading our comprehensive guide on .

2. Save for a Larger Down Payment: Reduce Risk, Reduce Rates

Aim to put down at least 10-20% of the car’s purchase price. A larger down payment reduces the principal amount you need to borrow, which lowers the lender’s risk and often leads to a better APR. It also helps you build equity faster and can reduce your overall interest paid.

3. Shop Around Aggressively: The Power of Comparison

This is a non-negotiable step. Never take the first loan offer you receive, especially not from the dealership without comparing.

- Get pre-approved: Apply for pre-approval from several different lenders – banks, credit unions, and online lenders – before you even step foot in a dealership. This provides you with concrete offers and a benchmark.

- Compare APRs, not just monthly payments: Focus on the total cost of the loan and the APR.

- Use pre-approvals as leverage: If a dealership offers financing, you can use your pre-approval offers to negotiate for an even better rate.

4. Consider a Shorter Loan Term: Balance Affordability with Savings

While it means higher monthly payments, opting for the shortest loan term you can comfortably afford will almost always result in a lower APR and significantly less interest paid over the life of the loan. Run different scenarios through a car loan calculator to see the impact on total cost.

5. Negotiate, Negotiate, Negotiate: Every Point Matters

Don’t be afraid to negotiate the APR offered to you. If you have strong credit and multiple pre-approval offers, you have significant leverage. Lenders are often willing to budge a bit to win your business. Always ask, "Is this the absolute best APR you can offer?"

6. Get Pre-Approved: Your Secret Weapon

Getting pre-approved for a car loan before you visit the dealership gives you immense power. It separates the financing negotiation from the car price negotiation. You walk into the dealership knowing exactly what interest rate you qualify for, allowing you to focus solely on getting the best price for the car itself. This also helps you avoid feeling pressured into accepting a less favorable dealer financing option.

7. Be Mindful of Add-ons: They Inflate Your Loan

Dealerships often try to sell you various add-ons like extended warranties, paint protection, or VIN etching. While some might have value, many are overpriced and can be financed into your loan, increasing the principal amount and, consequently, the total interest you pay based on your APR. Carefully consider each add-on and negotiate its price or decline it if it’s not truly necessary.

Common Mistakes to Avoid When Dealing with Car Loan APR

Even savvy buyers can fall into traps. Here are some common pitfalls to steer clear of:

- Focusing Only on Monthly Payments: As mentioned, this is a dangerous approach. A low monthly payment might hide a high APR and a very long loan term, leading to significantly higher total costs. Always look at the total amount you’ll pay back.

- Not Getting Pre-Approved: Walking into a dealership without a pre-approval is like playing poker without looking at your cards. You lose your negotiating power on financing and are at the mercy of the dealer’s rates.

- Ignoring the Fine Print: Always read your loan documents carefully before signing. Understand all terms, conditions, fees, and penalties. If something is unclear, ask for clarification.

- Accepting Dealer Financing Without Comparison: Dealerships are businesses; they often make a profit on financing. While they can sometimes offer competitive rates, especially promotional ones, always compare their offer to independent pre-approvals.

- Extending Loan Term Too Much: While a longer term lowers monthly payments, it almost always means you’ll pay substantially more in interest over time. Avoid pushing the loan term beyond what’s financially sensible for your budget and the car’s value.

- Falling for "Zero Interest" Traps: Be extremely cautious with 0% APR offers. They are usually reserved for buyers with impeccable credit and often come with strict conditions, shorter terms, or a higher purchase price if you forgo other incentives. Understand the full terms before committing.

Refinancing Your Car Loan: A Second Chance at a Better APR

What if you’ve already purchased a car and realize your APR isn’t as good as it could be? You might have an opportunity to refinance. Refinancing involves taking out a new loan to pay off your existing car loan, ideally with a lower APR or more favorable terms.

When to consider refinancing:

- Your credit score has significantly improved: If you’ve worked hard to boost your credit since your original purchase, you likely qualify for better rates now.

- Interest rates have dropped: If overall market rates have decreased, you might find a lower APR.

- Your financial situation has changed: You might be able to afford a shorter term with a lower APR.

- You want to reduce your monthly payment: While lowering APR is the primary goal, refinancing can also extend your term to reduce payments, though this comes with the caveat of potentially paying more interest overall.

The process is similar to applying for your initial loan: you apply to new lenders, they assess your credit, and if approved, they pay off your old loan. Based on my experience, refinancing can save borrowers hundreds or even thousands of dollars over the remaining term of their loan, making it a powerful tool for financial optimization.

Pro Tips from an Expert: Navigating the Car Loan Landscape

As someone who has guided countless individuals through the car buying process, here are some invaluable insights:

- Always look beyond the sticker price: The true cost of a car involves not just the purchase price, but also the total interest paid, insurance, maintenance, and fuel. Your APR is a huge part of that true cost.

- Don’t be afraid to walk away: If a deal doesn’t feel right, or you’re being pressured, politely decline and leave. There will always be another car and another deal. Your financial well-being is more important than a salesperson’s commission.

- Leverage online calculators: Before you even start shopping, use online car loan calculators to estimate monthly payments and total interest paid at different APRs and loan terms. This will give you a realistic budget and help you understand the impact of various scenarios. A reliable tool can be found on sites like the Consumer Financial Protection Bureau (CFPB) at .

- Understand "upside down": If you owe more on your car than it’s worth, you’re "upside down" or have "negative equity." A large down payment and a favorable APR help prevent this, especially in the early years of a loan.

- Consider gap insurance: If you have a small down payment and a long loan term, gap insurance can be a smart investment. It covers the difference between what you owe on your loan and what your car’s actual cash value is if it’s totaled or stolen.

Understanding Your Loan Documents: What to Look For

Before you sign any paperwork, carefully review the loan agreement. This document is legally binding and contains all the critical details of your loan.

- Annual Percentage Rate (APR): This should be clearly stated. Verify it matches what you were quoted.

- Interest Rate: This is the nominal rate, separate from the APR. Understand the difference.

- Total Finance Charge: This is the total amount of interest and fees you will pay over the life of the loan. It’s the ultimate measure of the loan’s cost.

- Total Amount of Payments: This is the sum of all your monthly payments over the entire loan term.

- Loan Term: The number of months you have to repay the loan.

- Prepayment Penalties: Check if there are any penalties for paying off your loan early. Most car loans do not have them, but it’s important to confirm.

- Late Payment Fees: Understand the charges and grace period for late payments.

Conclusion: Empowering Your Car Purchase with APR Knowledge

The journey to owning a car should be exciting, not intimidating. By truly understanding the APR of your car loan, you transform yourself from a passive consumer into an empowered negotiator. This isn’t just a number; it’s a powerful tool that dictates how much you truly pay for your vehicle and impacts your financial future for years to come.

Remember to prioritize improving your credit, shop around diligently for the best rates, and always scrutinize the total cost of the loan, not just the monthly payment. With the strategies and insights shared in this guide, you are well-equipped to navigate the complexities of car financing, secure the most favorable APR, and drive away confident in your smart financial decision. Start your journey to a smarter car purchase today!