Unlocking Your Drive: The Expert’s Guide to Determining APR on a Car Loan (And Why It Matters More Than You Think)

Unlocking Your Drive: The Expert’s Guide to Determining APR on a Car Loan (And Why It Matters More Than You Think) Carloan.Guidemechanic.com

Buying a car is an exciting milestone, whether it’s your first set of wheels or an upgrade to a newer model. However, the thrill of a new vehicle can quickly be overshadowed by the complexities of financing. Many buyers focus solely on the monthly payment, overlooking a critical figure that dictates the true cost of their loan: the Annual Percentage Rate, or APR. Understanding how to determine APR on a car loan isn’t just about financial literacy; it’s about saving thousands of dollars and making an informed decision that empowers your financial future.

As an expert blogger and professional SEO content writer with years of experience navigating the automotive financing landscape, I can tell you that mastering the APR is your ultimate superpower in car buying. This comprehensive guide will demystify the process, explain what truly influences your rate, and arm you with the strategies to secure the best possible deal. Get ready to transform from a passive borrower into an empowered negotiator.

Unlocking Your Drive: The Expert’s Guide to Determining APR on a Car Loan (And Why It Matters More Than You Think)

What Exactly is APR, and Why Is It Your North Star?

Before we dive into how to determine your car loan APR, let’s firmly establish what it is. The Annual Percentage Rate (APR) represents the true annual cost of borrowing money. It’s not just the interest rate; it’s a broader measure that includes the interest rate plus any additional fees or costs associated with obtaining the loan.

Think of it this way: the interest rate is the cost of borrowing the principal amount, expressed as a percentage. The APR, however, encompasses that interest rate and other charges like origination fees, documentation fees, and sometimes even credit report fees, rolled into a single, comprehensive annual percentage. This is why the APR is always the more accurate reflection of your loan’s total cost. Based on my experience, focusing solely on the interest rate is one of the most common pitfalls new car buyers make.

APR vs. Interest Rate: The Critical Distinction

Many people use "APR" and "interest rate" interchangeably, but this is a significant mistake. While closely related, they are not the same. The interest rate is simply the percentage charged by the lender for the use of their money, calculated on the principal balance of the loan.

The APR, on the other hand, is a more holistic figure. It’s mandated by the Truth in Lending Act to provide consumers with a standardized way to compare loan offers. It ensures that when you’re comparing two different car loan offers, you’re looking at the total cost of borrowing, not just a partial figure. This makes the APR your most reliable tool for an apples-to-apples comparison between lenders.

Key Factors That Drive Your Car Loan APR

Your car loan APR isn’t a random number; it’s a carefully calculated figure based on several interconnected factors. Understanding these elements is the first step in knowing how to influence your own rate. Pro tips from us: The more favorably these factors align, the lower your potential APR.

1. Your Credit Score: The Undisputed King

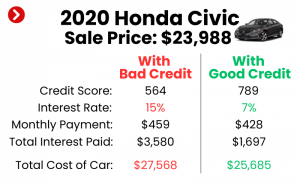

Without a doubt, your credit score is the single most influential factor in determining your car loan APR. Lenders use your credit score as a primary indicator of your creditworthiness and your likelihood of repaying the loan. A higher credit score signals lower risk to lenders, which translates into lower interest rates and, consequently, a lower APR.

Borrowers with excellent credit (typically 750+) can expect to receive the most competitive rates, often significantly lower than those with average or poor credit scores. Conversely, a low credit score will result in a higher APR, as lenders compensate for the increased risk of default. This is why it’s crucial to check your credit report well before you start car shopping.

2. The Loan Term: How Long Will You Pay?

The length of your loan, also known as the loan term, plays a substantial role in your APR. Generally, shorter loan terms (e.g., 36 or 48 months) tend to come with lower APRs compared to longer terms (e.g., 60, 72, or even 84 months). Lenders perceive shorter terms as less risky because they get their money back faster, reducing the potential for unforeseen circumstances or vehicle depreciation to impact repayment.

While a longer loan term might offer a lower monthly payment, it almost always means you’ll pay more in total interest over the life of the loan and typically incur a higher APR. It’s a trade-off that requires careful consideration of your budget and long-term financial goals.

3. Your Down Payment: Putting Skin in the Game

The amount of money you put down upfront on your car purchase directly impacts the amount you need to borrow. A larger down payment reduces the loan principal, which in turn reduces the lender’s risk. Lenders view a significant down payment as a sign of your commitment and financial stability, often rewarding it with a lower APR.

Aiming for a down payment of at least 10-20% of the vehicle’s value is a smart strategy. Not only does it help secure a better APR, but it also reduces your monthly payments and lessens the chances of being "upside down" on your loan, where you owe more than the car is worth.

4. Your Debt-to-Income (DTI) Ratio

Your debt-to-income ratio is a measure that compares your total monthly debt payments to your gross monthly income. Lenders use this ratio to assess your ability to take on additional debt. A lower DTI ratio indicates that you have more disposable income available to cover your car loan payments, making you a more attractive borrower.

While there isn’t a universal cut-off, a DTI ratio below 36% is often considered favorable. A high DTI can signal financial strain, leading lenders to offer a higher APR or even deny your loan application.

5. Vehicle Type: New vs. Used, Make and Model

The type of vehicle you’re financing can also influence your APR. New cars often qualify for lower APRs than used cars, primarily because they hold their value better initially and are perceived as less risky collateral. Lenders know that a new car is less likely to break down in the short term, which could impede your ability to make payments.

Used cars, especially older models or those with high mileage, typically carry higher APRs due to increased depreciation and potential maintenance issues. The specific make and model can also play a role, with some vehicles retaining value better than others, thus influencing lender risk assessment.

6. Market Interest Rates and Economic Conditions

Broader economic factors, such as the prevailing market interest rates set by central banks (like the Federal Reserve in the U.S.), have an overarching impact on all lending rates, including car loan APRs. When the Federal Reserve raises its benchmark interest rate, it generally leads to higher borrowing costs across the board.

Conversely, during periods of economic stimulus, rates may drop. While you can’t control these macro-economic forces, being aware of them helps you understand why rates might be higher or lower at a particular time.

7. Lender Type: Where You Get Your Loan Matters

Different types of lenders offer varying APRs based on their business models, risk assessments, and target customers. Banks, credit unions, and dealership financing arms each have their own lending criteria and rate structures. Credit unions, for example, are often known for offering some of the most competitive APRs because they are non-profit organizations focused on their members.

Dealership financing can sometimes be convenient, but it’s essential to compare their offers with those from independent lenders. Some dealerships might mark up interest rates to increase their profit, so always shop around before committing.

The Step-by-Step Guide: How to Determine Your Car Loan APR

Now that we understand the influencing factors, let’s walk through the practical steps to determine your car loan APR effectively. This process is about empowerment and informed decision-making.

Step 1: Gather Your Financial Information

Before you even step foot in a dealership, prepare your financial portfolio. This includes:

- Your Credit Report and Score: Obtain your free annual credit report from all three major bureaus (Equifax, Experian, TransUnion) and check your scores. Look for any errors that could be negatively impacting your score and dispute them. This is a critical first step.

- Proof of Income: Recent pay stubs, W-2s, or tax returns will verify your income stability.

- Proof of Residence: Utility bills or a lease agreement.

- Identification: Driver’s license or state ID.

- Current Debt Information: A list of your monthly debt payments (credit cards, student loans, mortgage, etc.) to help calculate your DTI.

Having these documents ready will streamline the application process and show lenders you are a serious and organized borrower.

Step 2: Get Pre-Approved from Multiple Lenders

This is, hands down, the most crucial step in securing a favorable APR. Don’t wait until you’re at the dealership to think about financing. Apply for pre-approval with at least 3-5 different lenders – including banks, credit unions, and online lenders.

Pre-approval involves a soft credit inquiry (which doesn’t impact your score) to give you an estimate of the loan amount and APR you qualify for. This step allows you to walk into the dealership with a concrete offer in hand, giving you leverage to negotiate. Common mistakes to avoid are relying solely on dealership financing, which often presents less competitive rates.

Step 3: Understand the Loan Offer Sheet

Once you receive pre-approval offers, carefully examine the loan offer sheet (sometimes called a Truth in Lending Disclosure). This document legally requires lenders to disclose the APR, loan term, total finance charges, and total amount of payments.

Pay close attention to the APR listed. This is the number you want to compare across different offers. Don’t be swayed by just the monthly payment; a lower monthly payment over a longer term might hide a higher APR and ultimately cost you more.

Step 4: Utilize Online APR Calculators

While pre-approvals give you a solid offer, online car loan APR calculators can provide a quick estimate and help you understand how different variables (loan amount, interest rate, term) affect your potential monthly payment and total interest paid. These tools are excellent for budgeting and comparing scenarios before you even apply for pre-approval.

Many reputable financial websites offer free car loan calculators. Input the principal amount you plan to borrow, the interest rate you anticipate (based on your credit score and current market rates), and the desired loan term. The calculator will then show you the estimated monthly payment and total interest.

Step 5: Don’t Forget the Fees!

Remember, APR includes fees. When comparing offers, ensure you’re looking at the total cost, not just the advertised interest rate. Some lenders might offer a seemingly low interest rate but then tack on significant origination fees, processing fees, or documentation fees that inflate the overall APR.

Always ask for a detailed breakdown of all fees included in the loan. A transparent lender will readily provide this information. If a lender is hesitant to disclose fees, consider that a red flag.

Decoding the Numbers: A Simplified Example

Let’s illustrate how interest and fees combine to form your APR.

Imagine you borrow $20,000 for a car.

- Scenario A (Simple Interest): The lender offers a 5% interest rate. Over 60 months, with no fees, your total interest paid would be X, and your APR would effectively be 5%.

- Scenario B (With Fees): The lender offers a 4.5% interest rate but charges a $500 origination fee. While the interest rate is lower, that $500 fee needs to be amortized over the loan term. This fee effectively increases the overall cost of borrowing. When that $500 is factored in alongside the interest, your actual APR for Scenario B might be 5.2% or even higher, making it more expensive than Scenario A, despite the lower nominal interest rate.

This simplified example highlights why the APR is a more accurate indicator of the true cost.

Strategies for Securing a Lower APR

Now that you know how to determine APR on a car loan, let’s explore actionable strategies to ensure you get the best possible rate.

- Improve Your Credit Score: This is your most powerful lever. Pay bills on time, reduce credit card balances, and avoid opening new credit accounts in the months leading up to your car purchase. A higher score directly translates to a lower APR.

- Increase Your Down Payment: The more cash you put down, the less you need to borrow, and the less risky you appear to lenders. This often results in a lower APR.

- Choose a Shorter Loan Term: While it means higher monthly payments, a shorter loan term usually comes with a lower APR and significantly reduces the total interest you pay over the life of the loan.

- Shop Around Extensively: As emphasized earlier, getting pre-approved by multiple lenders is non-negotiable. Compare offers not just on monthly payments but, crucially, on the APR. This competition among lenders works in your favor.

- Negotiate with Lenders: Don’t be afraid to use competing pre-approval offers as leverage. Tell your preferred lender about a better APR you received elsewhere and ask if they can match or beat it. Many are willing to negotiate to earn your business.

- Consider a Co-signer (with Caution): If your credit score is less than ideal, a co-signer with excellent credit can help you qualify for a lower APR. However, understand that the co-signer is equally responsible for the loan, and their credit will be affected if you miss payments.

- Refinancing as a Future Option: If you secure a car loan with a higher APR due to circumstances at the time of purchase, you might be able to refinance your car loan later when your credit has improved or market rates have dropped. This can lead to significant savings over the remaining loan term. For more on this, you might find our article, "Refinancing Your Car Loan: A Comprehensive Guide" (hypothetical internal link), particularly helpful.

When is a "Good" Car Loan APR?

Defining a "good" car loan APR is subjective and depends heavily on your individual financial profile, especially your credit score. However, we can offer some general benchmarks:

- Excellent Credit (750+): You could potentially qualify for APRs in the low single digits, sometimes even 0-3% for new car promotions.

- Good Credit (670-749): Expect APRs typically in the 4-7% range.

- Average Credit (580-669): APRs in this range often fall between 8-12% or higher.

- Poor Credit (Below 580): You might face APRs of 15% or more, if approved at all.

Remember, these are general guidelines. Always compare actual offers you receive against the current market rates and your credit profile.

The Pitfalls: Common Mistakes to Avoid When Determining APR

Based on my experience, many buyers inadvertently make mistakes that cost them money. Avoid these common missteps:

- Focusing Only on the Monthly Payment: This is perhaps the biggest trap. A low monthly payment might seem appealing, but if it’s achieved by extending the loan term and increasing the APR, you’ll pay significantly more over time.

- Not Shopping Around: Settling for the first loan offer, especially from the dealership, almost guarantees you’re leaving money on the table. Always compare multiple offers.

- Ignoring Fees: As discussed, fees can dramatically inflate your APR. Always ask for a detailed breakdown of all charges.

- Not Checking Your Credit Report: Errors on your credit report can unjustly raise your APR. Reviewing it beforehand allows you to correct inaccuracies.

- Getting Pre-Approved Too Late: Waiting until you’re already at the dealership puts you at a disadvantage. Get your financing ducks in a row before you start negotiating for the car itself.

- Forgetting About Total Cost: Always consider the total amount you will pay over the life of the loan, not just the monthly payment. This calculation includes the principal, all interest, and all fees.

Pro Tips from an Expert

Beyond the steps and strategies, here are a few more insights from years in the finance and automotive world:

- The Power of Pre-Approval: This is your strongest negotiation tool. When you walk into a dealership with a pre-approved loan offer, you’re buying the car, not the financing. This forces the dealership to either beat your existing offer or let you walk away with outside financing.

- Read the Fine Print: I cannot stress this enough. Every loan document contains critical details. Understand the prepayment penalties (if any), late fees, and what happens if you miss a payment.

- Don’t Be Afraid to Walk Away: If an offer doesn’t feel right, or if the APR is higher than you anticipated, be prepared to walk away. There will always be another car and another lender. Your financial well-being is paramount.

- Educate Yourself Continuously: The more you understand about personal finance and lending, the better decisions you’ll make. Resources like the Consumer Financial Protection Bureau (CFPB) offer excellent, unbiased information on car loans and other financial products. You can find more valuable information on understanding car loans at CFPB’s Auto Loan page (external link).

Conclusion: Empowering Your Car Buying Journey

Determining the APR on a car loan is not just a technicality; it’s a fundamental step in smart financial planning. By understanding what APR truly represents, knowing the factors that influence it, and diligently following our step-by-step guide, you empower yourself to make informed decisions that save you money and stress. Remember, the goal isn’t just to get a car; it’s to get a car on terms that support your financial health.

Armed with this knowledge, you are no longer a passive recipient of loan offers. You are an informed consumer, ready to compare, negotiate, and secure the best possible financing for your next vehicle. Drive confidently, knowing you’ve mastered the art of determining your car loan APR. For further insights into managing your automotive finances, consider exploring our article on "Budgeting for Your Next Car: Beyond the Monthly Payment" (hypothetical internal link).