Unlocking Your Drive: The Ultimate Guide to Car Loan Duration and Its True Impact

Unlocking Your Drive: The Ultimate Guide to Car Loan Duration and Its True Impact Carloan.Guidemechanic.com

Buying a car is an exciting milestone, often representing freedom, convenience, and a significant personal investment. For many, this dream becomes a reality through a car loan, a financial tool that bridges the gap between aspiration and ownership. Yet, amidst the excitement of choosing the perfect model and color, one crucial element often gets overlooked: the car loan duration.

This isn’t just a minor detail; it’s a fundamental decision that profoundly impacts your monthly budget, the total cost of your vehicle, and your overall financial well-being for years to come. As an expert blogger and SEO content writer with years of experience navigating the complexities of auto financing, I’ve seen firsthand how the right (or wrong) loan term can make all the difference. In this comprehensive guide, we’ll dive deep into everything you need to know about car loan duration, helping you make an informed choice that truly serves your financial goals.

Unlocking Your Drive: The Ultimate Guide to Car Loan Duration and Its True Impact

Understanding Car Loan Duration: The Foundation of Your Auto Finance

At its core, car loan duration, also known as the loan term or auto loan length, refers to the period over which you agree to repay the money borrowed to purchase your vehicle. This period is typically expressed in months, with common terms ranging from 36 months (3 years) to 84 months (7 years), and sometimes even longer.

The chosen loan term directly influences two critical aspects of your auto loan: your monthly payments and the total amount of interest you’ll pay over the life of the loan. Understanding this fundamental relationship is the first step toward making a smart financing decision. It’s not just about what you can afford each month; it’s about the bigger picture of what you’re truly paying for your car.

The Interplay: Car Loan Duration, Monthly Payments, and Total Cost

The length of your car loan term is a powerful lever that directly impacts both your immediate financial outflow and your long-term financial commitment. It’s a balancing act between lower monthly payments and the overall cost of your vehicle.

Shorter Loan Terms (e.g., 36-48 Months)

Opting for a shorter car loan duration, such as 36 or 48 months, means you’ll be paying off your vehicle more quickly. This approach has several distinct advantages, though it does come with a higher immediate financial commitment.

With a shorter loan term, your monthly payments will be notably higher compared to a longer loan for the same amount. This is because you’re condensing the repayment of the principal loan amount into a fewer number of months. You need to ensure your budget can comfortably accommodate these larger payments without straining your other financial obligations.

However, the significant upside of a shorter loan term is the substantial reduction in the total interest you’ll pay over the life of the loan. Since you’re borrowing money for a shorter period, the lender has less time to accrue interest on the outstanding balance. This translates into considerable savings, making the overall cost of your car significantly lower.

Furthermore, a shorter auto loan length allows you to build equity in your vehicle much faster. Equity is the difference between your car’s market value and what you still owe on it. Building equity quickly means you’re less likely to be "upside down" on your loan (owing more than the car is worth), which offers greater financial flexibility if you decide to sell or trade in your vehicle in the future.

Who it’s best for: Shorter loan terms are ideal for individuals with a stable, higher income who prioritize saving on interest and achieving debt-free ownership sooner. They also suit those who plan to keep their vehicle for a long time, well beyond the loan term.

Longer Loan Terms (e.g., 72-84 Months)

Conversely, choosing a longer car loan duration, such as 72 or 84 months, stretches your repayment period over a greater number of months. This strategy is often appealing due to its immediate impact on your monthly budget.

The primary benefit of a longer loan term is significantly lower monthly payments. By extending the repayment period, the principal loan amount is spread out, making each individual payment more manageable. This can be particularly attractive if you’re trying to keep your monthly expenses down or if you’re financing a more expensive vehicle.

However, this affordability comes at a cost. The most significant drawback of a longer auto loan length is the substantial increase in the total amount of interest paid over the life of the loan. While each payment is smaller, you’re paying interest for a much longer time, leading to thousands of dollars in additional costs that you might not initially anticipate.

Another critical consideration with extended loan terms is the risk of negative equity, often referred to as being "upside down" on your loan. Cars depreciate rapidly, especially in the first few years. With a longer loan, your car’s value might decrease faster than you pay off the loan, leaving you owing more than the car is worth. This situation can be problematic if you need to sell or trade in your car before the loan is fully repaid.

Who it’s best for: Longer loan terms can be suitable for individuals who need the lowest possible monthly payment to fit a desired vehicle into their budget, perhaps due to lower income or other pressing financial commitments. It might also be considered if the interest rate is exceptionally low, though this is rare for extended terms.

Pro tips from us: Based on my experience, the "sweet spot" for many borrowers balances affordability with minimizing total interest. For a new car, a 60-month (5-year) loan often strikes a good balance. For used cars, aiming for 36-48 months is generally advisable to mitigate depreciation risks. Always run the numbers for various scenarios.

Key Factors Influencing Your Ideal Car Loan Duration

Choosing the right car loan duration isn’t a one-size-fits-all decision. Several personal and financial factors should guide your choice, ensuring it aligns with your overall financial health.

Your Budget & Monthly Cash Flow

Your current budget and monthly cash flow are arguably the most critical determinants of your ideal car loan length. It’s essential to assess how much you can truly afford to pay each month without compromising other necessary expenses or your savings goals.

A common financial guideline suggests that your total car-related expenses (payment, insurance, fuel, maintenance) should not exceed 10-15% of your net monthly income. Exceeding this can lead to financial strain. When evaluating your budget, consider your debt-to-income ratio – the percentage of your gross monthly income that goes towards debt payments. A high ratio signals to lenders (and should signal to you) that you’re potentially stretching too thin.

Common mistakes to avoid are focusing solely on the monthly payment without considering the bigger picture of your overall financial obligations. A lower monthly payment might seem attractive, but if it comes with a significantly higher total cost or pushes you into negative equity, it might not be the best long-term decision. Always prioritize financial stability over the lowest possible payment if it means sacrificing other financial goals.

Interest Rates

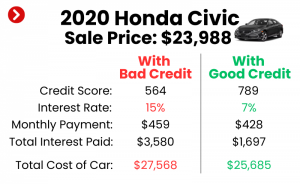

The interest rate on your car loan plays a pivotal role in the total cost of borrowing and is intrinsically linked to the loan duration. A higher interest rate, especially when combined with a longer loan term, can exponentially increase your total payout.

Your credit score is the primary factor determining the interest rate you’ll qualify for. Borrowers with excellent credit typically receive the lowest rates, making longer terms less punishing in terms of total interest. However, if you have a lower credit score, lenders will offer higher interest rates, and extending the loan term further amplifies the total interest burden.

It’s crucial to understand how interest accumulates. Even a seemingly small difference in the interest rate can amount to thousands of dollars over a 72 or 84-month loan. Always factor the interest rate into your duration decision. For more insights on how interest rates are calculated and their impact, you can refer to resources like the Consumer Financial Protection Bureau’s guide on understanding auto loans.

Down Payment

The size of your down payment can significantly influence the car loan duration you might consider. A larger down payment reduces the principal amount you need to borrow, thereby lowering your monthly payments or allowing you to choose a shorter loan term without a dramatic increase in those payments.

Making a substantial down payment helps you build equity in your vehicle from day one. This immediate equity acts as a buffer against rapid depreciation, reducing the risk of being upside down on your loan. Based on my experience, a down payment of at least 10-20% for a new car and 20% or more for a used car is often recommended to create a healthier loan-to-value ratio.

If you have a significant down payment, you might be able to comfortably afford a shorter loan term, saving you a considerable amount in interest. Conversely, a smaller down payment might necessitate a longer loan duration to keep monthly payments manageable, but this increases your exposure to higher interest costs and negative equity.

Vehicle Depreciation

Vehicle depreciation is the rate at which your car loses value over time, and it’s a silent killer of financial plans when combined with an unsuitable car loan duration. Most cars lose a significant portion of their value in the first few years, sometimes as much as 20% in the first year alone.

The relationship between loan term and depreciation is critical. With a longer loan term, particularly 72 or 84 months, your car’s value can depreciate faster than you pay down the principal balance. This creates a situation of negative equity, where you owe more on the car than it is currently worth. This is a common mistake I’ve seen many borrowers make.

Being in a negative equity position can be financially crippling if you need to sell or trade in your car before the loan is paid off. You’d have to pay the difference out of pocket, or roll the negative equity into a new loan, which creates an even larger debt burden. Always consider the car’s expected depreciation curve when deciding on your loan length.

Your Future Financial Plans

Your personal financial outlook and future plans should also weigh heavily on your car loan duration decision. Consider your job stability, potential salary changes, or upcoming major expenses like a home purchase, college tuition, or starting a family.

If you anticipate significant life changes that might impact your income or expenses, a shorter loan term might offer greater peace of mind by getting the car debt paid off sooner. Conversely, if you foresee a period of reduced income, a longer term with lower payments might seem appealing, but it could lock you into a long-term debt obligation that becomes difficult to manage.

Pro tips from us: Always consider the "what if" scenarios. Life is unpredictable, and locking yourself into a very long-term car loan can limit your financial flexibility when unforeseen circumstances arise.

The Hidden Costs of Longer Car Loan Durations

While a longer car loan duration might offer the immediate gratification of lower monthly payments, it often conceals several significant financial drawbacks that accumulate over time. These hidden costs can turn an initially attractive deal into a far more expensive proposition.

Increased Total Interest Paid

This is perhaps the most significant hidden cost, yet it’s often underestimated. When you extend your loan term, you’re not just spreading out the principal; you’re also extending the period over which interest accrues on that principal. Even if the interest rate remains the same, the sheer duration means you’re paying interest for longer.

For example, a $30,000 loan at 5% APR for 60 months might cost you around $3,900 in total interest. Extend that to 84 months, and the total interest could jump to over $5,600, a difference of $1,700 for the exact same car and principal amount. This extra money could have gone into savings, investments, or other important financial goals.

Negative Equity (Being Upside Down)

As discussed earlier, negative equity is a substantial risk with longer car loan durations. This occurs when the outstanding balance on your loan is greater than the current market value of your vehicle. Since cars depreciate rapidly, especially in their early years, a long loan term means you’re paying off the car’s value at a slower rate than it’s losing value.

If you find yourself in a negative equity situation and need to sell or trade in your car, you’ll have to pay the difference out of pocket. This can be a substantial sum. To mitigate this risk, many lenders will require you to purchase Guaranteed Asset Protection (GAP) insurance, especially with longer terms or small down payments. While GAP insurance provides a safety net, it’s an additional cost, further eroding the perceived savings of a lower monthly payment.

Extended Warranty Overlap

Many new cars come with a manufacturer’s warranty, typically lasting for 3 years/36,000 miles or 5 years/60,000 miles. If you opt for an 84-month car loan duration, you might be paying off your vehicle long after the original warranty has expired. This means you’ll be responsible for the full cost of any repairs that arise in the later years of your loan, adding unexpected expenses to your budget.

Some dealerships might also try to sell you an extended warranty as part of your financing package. While these can offer peace of mind, buying an extended warranty for a car you’ll be paying off for seven years means you’re potentially paying for coverage on a car that’s significantly older and more prone to issues, or even beyond the point you plan to own it.

Potentially Higher Insurance Premiums

While not a direct cost of the loan itself, lenders often require comprehensive and collision coverage on financed vehicles to protect their investment. For longer loan terms, especially if the car is expensive or has a high loan-to-value ratio, lenders might require specific, often more expensive, levels of coverage for a longer period.

This isn’t always the case, but it’s a factor to consider. If you had planned to reduce your insurance coverage as the car aged and its value depreciated, a long loan term might prevent you from doing so, keeping your premiums higher for longer.

Strategies for Choosing the Optimal Car Loan Duration

Making an informed decision about your car loan duration requires careful consideration and a proactive approach. Here are some strategies to help you choose the term that best fits your financial situation.

-

Assess Your True Affordability: Go beyond just the monthly payment. Create a detailed budget that includes all your income and expenses. Use the "10-15% rule" as a guideline for your total car-related costs. Can you comfortably afford the payment for a shorter term without sacrificing savings or other financial goals?

-

Run the Numbers (Scenario Planning): Don’t just look at one loan offer. Use online car loan calculators to compare different loan terms (e.g., 36, 48, 60, 72 months) with varying interest rates. See how much total interest you’d pay for each scenario. This visual comparison often highlights the significant savings of shorter terms.

-

Consider a Larger Down Payment: If possible, save up for a substantial down payment. This reduces the amount you need to borrow, which can either lower your monthly payments for a given term or allow you to choose a shorter loan duration with manageable payments, ultimately saving you money on interest.

-

Improve Your Credit Score Before Applying: Your credit score is key to securing lower interest rates. Before you even start shopping for a car, take steps to improve your credit score. Pay bills on time, reduce outstanding debt, and check your credit report for errors. A better credit score can drastically reduce your total interest paid, making shorter terms even more attractive. For more guidance on this, check out our article on How to Improve Your Credit Score for a Car Loan (Internal Link Placeholder).

-

Shop Around for Lenders: Don’t automatically accept the financing offered by the dealership. Get pre-approved for a loan from several different banks, credit unions, and online lenders. Comparing multiple offers will give you leverage and ensure you get the best possible interest rate and terms for your car loan duration.

-

Understand Refinancing Options: Life circumstances change. If you initially chose a longer term for affordability but your financial situation improves, consider refinancing your car loan. Refinancing can allow you to secure a lower interest rate or a shorter loan term, reducing your total interest paid. We delve deeper into this in our guide: The Ultimate Guide to Car Loan Refinancing (Internal Link Placeholder).

Pro tips from us: Always aim for the shortest car loan duration you can comfortably afford without straining your budget. This strategy minimizes interest, builds equity faster, and gets you out of debt sooner.

When Longer Durations Might Make Sense (and When They Don’t)

While the general advice leans towards shorter loan terms, there are specific, albeit rare, circumstances where a longer car loan duration might be a justifiable choice. However, it’s crucial to understand these nuanced situations to avoid common pitfalls.

Situations Where Longer Terms Are Justifiable:

- Temporary Cash Flow Issues with a Clear Plan: If you’re facing a temporary, short-term cash flow challenge but have a concrete plan to increase income or reduce expenses in the near future, a longer term might offer necessary breathing room. The key here is the "clear plan" and the intent to refinance or aggressively pay down the loan once your situation improves. This isn’t a long-term strategy but a short-term tactical move.

- Exceptionally Low-Interest Rates (Rare): In very rare economic conditions, you might find an auto loan with an interest rate that is exceptionally low, perhaps even lower than what you could earn by investing that money elsewhere. In such a scenario, the additional interest paid over a longer term might be negligible, or the opportunity cost of paying it off quickly might be higher. This is a sophisticated financial decision and not applicable to most borrowers.

- As a Last Resort for Essential Transportation: If having a reliable vehicle is absolutely essential for your work or family, and a longer term is the only way to make the monthly payments for a safe and dependable car, it might be a necessary evil. However, this should prompt a deeper look into your overall financial health and strategies for increasing income or reducing other expenses to avoid similar situations in the future.

Common mistakes to avoid are using long terms out of habit or simply because the dealership offers them, without a thorough understanding of the true cost. Many people assume a 72 or 84-month term is "normal" without realizing the significant financial implications.

When to Avoid Longer Loan Durations:

- High Interest Rates: If your credit score results in a high interest rate, extending the loan term will lead to an exorbitant amount of total interest paid. The cumulative cost can quickly make the car far more expensive than its sticker price.

- Buying a Rapidly Depreciating Car: Some car models lose value much faster than others. Pairing a long loan term with a vehicle known for rapid depreciation almost guarantees you’ll be in a negative equity position for a significant portion of the loan.

- If You Plan to Trade In Frequently: If you typically upgrade your vehicle every 2-3 years, a long loan term is a terrible idea. You’ll almost certainly owe more than the car is worth when you’re ready for a new one, creating a cycle of rolling negative equity into new loans.

- Without a Substantial Down Payment: A small or no down payment combined with a long loan term is a recipe for disaster, almost guaranteeing negative equity and a higher total cost.

Beyond the Term: Other Considerations for Your Auto Loan

While car loan duration is paramount, it’s just one piece of the auto financing puzzle. To ensure a truly sound financial decision, you must also look at other aspects of your loan agreement.

First, check for prepayment penalties. Some lenders charge a fee if you pay off your loan early or make extra payments. This can negate some of the benefits of trying to shorten your effective loan duration. Always read the fine print to ensure your loan is open to early repayment without penalty.

Second, be aware of balloon payments. While less common in standard auto loans, some specialized financing structures might include a large lump-sum payment due at the end of the loan term. This can be a huge surprise if you’re not prepared for it. Ensure you fully understand the repayment structure before signing.

Finally, always understand the full loan agreement. Don’t be afraid to ask questions about anything you don’t understand. This includes the Annual Percentage Rate (APR), any fees, the exact total cost of the loan, and your rights as a borrower. Your financial future depends on your informed consent.

Conclusion: Empowering Your Car Loan Duration Decision

Choosing the right car loan duration is a critical financial decision that extends far beyond just the monthly payment. It’s about understanding the true cost of your vehicle, managing your long-term financial health, and protecting yourself from common pitfalls like negative equity and excessive interest.

By carefully considering your budget, credit score, down payment, the impact of depreciation, and your future financial plans, you can select a loan term that aligns with your financial goals. Remember, the goal isn’t just to get the lowest monthly payment, but to secure the most financially sound auto loan that serves your best interests. Make an informed choice, and drive away with confidence, knowing you’ve made a smart investment in your future.