Unlocking Your Drive: The Ultimate Guide to Navigating Snap Car Loan Success

Unlocking Your Drive: The Ultimate Guide to Navigating Snap Car Loan Success Carloan.Guidemechanic.com

Securing reliable transportation is more than just a convenience; it’s often a necessity for work, family, and daily life. However, for many individuals, the path to vehicle ownership can seem fraught with obstacles, especially when a less-than-perfect credit history stands in the way. Traditional lenders often turn their backs on those with credit challenges, leaving a significant portion of the population feeling stranded.

This is where specialized financing solutions like Snap Car Loan enter the picture. Designed to bridge the gap for those who don’t fit the mold of conventional auto lending, Snap Car Loan offers a ray of hope. But what exactly is it, who can truly benefit, and how can you navigate the process to maximize your chances of approval and future financial success?

Unlocking Your Drive: The Ultimate Guide to Navigating Snap Car Loan Success

As expert bloggers and SEO content writers, our mission is to provide you with the most comprehensive, in-depth, and actionable guide to Snap Car Loan. We’ll peel back the layers, share professional insights, and equip you with the knowledge to make informed decisions. This article will serve as your ultimate pillar content, ensuring you understand every facet of securing and managing a Snap Car Loan responsibly.

What Exactly is a Snap Car Loan?

At its core, a Snap Car Loan is a specialized form of auto financing tailored for individuals who might struggle to qualify for traditional bank or credit union loans. These are often referred to as "subprime" auto loans, meaning they are extended to borrowers with credit scores below what prime lenders typically accept. The primary goal of Snap Car Loan is to provide an accessible pathway to vehicle ownership for those with credit blemishes, limited credit history, or unique financial circumstances.

Unlike conventional lenders who prioritize pristine credit scores, Snap Car Loan looks at a broader range of factors. They understand that a credit score doesn’t always tell the full story of an individual’s financial capability or their commitment to making payments. Their focus is often on your current ability to pay and your stability.

This type of financing is not a direct loan from Snap Car Loan itself. Instead, Snap acts as a facilitator, connecting you with a network of dealerships and lenders who specialize in non-prime auto financing. They streamline the application process, making it quicker and less intimidating than navigating multiple lenders independently.

Who Can Truly Benefit from a Snap Car Loan?

The target demographic for a Snap Car Loan is broad, encompassing anyone who finds themselves outside the traditional lending criteria. Based on my experience guiding countless individuals through the car buying process, I’ve seen firsthand how vital these options are for specific groups. If you identify with any of the following scenarios, a Snap Car Loan could be a viable solution for you:

- Individuals with a Bad Credit History: Perhaps you’ve had past financial difficulties, such as late payments, collections, or even charge-offs. These events significantly impact your credit score, making traditional auto loans difficult to obtain. Snap Car Loan understands that past mistakes don’t define your present potential.

- Those with No Credit History: If you’re new to credit, a young adult, or someone who has always paid with cash, you might not have a credit score established. This "thin file" can be just as challenging as bad credit for prime lenders. Snap Car Loan can provide that crucial first step to building a credit profile.

- Previous Bankruptcies or Repossessions: While these are significant credit events, they don’t have to be a permanent roadblock. Many lenders in the Snap Car Loan network are willing to work with individuals who have gone through bankruptcy or repossession, especially if time has passed and you can demonstrate renewed financial stability.

- People Needing a Fresh Start: Life throws curveballs, and sometimes financial situations change unexpectedly. A Snap Car Loan can offer a fresh start, allowing you to secure transportation and, importantly, begin rebuilding your credit score with responsible payments. It’s an opportunity to show consistent financial behavior.

It’s important to understand that while a Snap Car Loan can be a lifeline, it’s not a magic bullet. It’s a tool designed to help you get where you need to go, both literally and financially, when other doors are closed.

The Snap Car Loan Application Process: A Step-by-Step Guide

Navigating the application process for any loan can feel daunting, but Snap Car Loan aims to simplify it. From an expert perspective, preparing thoroughly is key to a smooth and successful experience. Here’s a detailed breakdown of what to expect:

1. Pre-Application Considerations and Budgeting

Before you even fill out an application, take a moment to assess your financial situation realistically. How much can you truly afford for a monthly car payment, including insurance, fuel, and maintenance? Over-extending yourself can lead to financial strain down the road. Use a budget planner to understand your income and expenses thoroughly.

Consider your transportation needs versus wants. While a brand-new luxury SUV might be appealing, a reliable used sedan might be a more sensible and approvable option for your first Snap Car Loan. Realistic expectations are crucial.

2. The Online Application: What to Expect

The initial step typically involves a quick and straightforward online application. You’ll be asked for basic personal and financial information. This often includes your name, address, contact details, employment history, and income.

Snap Car Loan’s online portal is designed to be user-friendly, allowing you to complete this step from the comfort of your home. The goal here is to get a preliminary assessment of your eligibility without requiring extensive documentation upfront.

3. Required Documentation: Proof of Stability

Once your initial application shows promise, you’ll need to provide supporting documents. Pro tips from us: Gather all your documents beforehand to expedite the process. Lenders want to see proof of your current stability and ability to repay the loan.

Commonly requested documents include:

- Proof of Income: Recent pay stubs (usually 2-3 months), bank statements showing direct deposits, or tax returns if self-employed.

- Proof of Residence: Utility bills, a lease agreement, or mortgage statement with your current address.

- Valid Identification: A driver’s license or state-issued ID.

- Social Security Number: For credit verification purposes.

- References: Sometimes, personal references are requested, though this is less common with online applications.

Ensuring these documents are readily available and up-to-date will significantly speed up your approval process. Any discrepancies or delays in providing information can prolong the waiting period.

4. Dealership Involvement: Your Partner in Purchase

Snap Car Loan works with a network of approved dealerships that specialize in working with non-prime borrowers. Once you’re pre-approved, you’ll typically be connected with a local dealership that can help you select a vehicle within your approved budget and loan terms.

These dealerships are experienced in navigating the complexities of subprime auto financing. They understand the nuances of Snap Car Loan and can guide you through the vehicle selection and final paperwork. This partnership is a key differentiator, as it provides a personalized touch to the online application process.

5. Approval Timeline: Patience is a Virtue

While Snap Car Loan aims for quick preliminary approvals, the finalization of your loan can vary. Initial online pre-approvals can happen in minutes. However, the full approval, including verification of documents and vehicle selection, might take anywhere from a few hours to a couple of business days.

Factors influencing the timeline include how quickly you provide requested documents and the specific lender’s internal processing times. Stay in communication with the dealership and the Snap Car Loan representatives to ensure everything moves smoothly.

Understanding Loan Terms and Conditions

When dealing with any financial product, especially a subprime auto loan like Snap Car Loan, understanding the terms and conditions is paramount. Common mistakes to avoid are signing without fully comprehending the agreement or focusing solely on the monthly payment. Here’s what you need to pay close attention to:

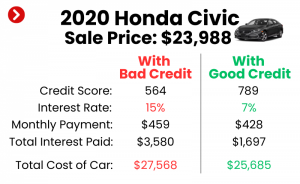

1. Interest Rates (APR)

Interest rates for Snap Car Loans are generally higher than those for prime borrowers. This is because lenders assume a greater risk when extending credit to individuals with lower credit scores. The Annual Percentage Rate (APR) includes both the interest rate and any additional fees, giving you the true cost of borrowing over a year.

It’s crucial to compare the APR across different offers if you receive multiple. Even a slight difference in APR can amount to hundreds or thousands of dollars over the life of the loan. Don’t be shy about asking for clarification on how your APR was determined.

2. Loan Term

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A longer loan term generally results in lower monthly payments, which can be appealing for budgeting. However, it also means you’ll pay more in total interest over the life of the loan.

Conversely, a shorter loan term will have higher monthly payments but will save you money on interest and get you out of debt faster. Weigh your budget constraints against the total cost of the loan when deciding on a term.

3. Down Payment

A down payment is the initial amount of money you pay upfront towards the purchase of the vehicle. While some Snap Car Loans might be available with no down payment, making one is almost always a good idea. A substantial down payment offers several benefits:

- Increases Approval Chances: It reduces the lender’s risk, making you a more attractive borrower.

- Lowers Monthly Payments: You’re financing less, so your payments will be smaller.

- Reduces Total Interest Paid: Less principal means less interest accrues over time.

- Helps Avoid Negative Equity: A down payment helps ensure you don’t owe more than the car is worth, especially in the early years of the loan.

Pro tips from us: Even a small down payment can make a significant difference. If you can save up a few hundred or a couple of thousand dollars, it will strengthen your application considerably.

4. Fees and Charges

Be diligent in reviewing the loan agreement for any additional fees. These might include:

- Origination Fees: A fee charged by the lender for processing the loan.

- Documentation Fees (Doc Fees): Charged by the dealership for preparing paperwork.

- Late Payment Fees: Penalties for missed or late payments.

- Prepayment Penalties: Though less common now, some loans might charge a fee if you pay off your loan early. Always confirm if your loan has this clause.

Understanding all these components ensures you have a clear picture of your financial commitment before signing on the dotted line.

Maximizing Your Chances of Approval

While Snap Car Loan is designed for those with credit challenges, it doesn’t mean approval is guaranteed for everyone. From my perspective as an expert, lenders still look for signs of responsible borrowing and repayment capacity. Here’s how you can significantly boost your chances of getting approved:

- Demonstrate Stable Income and Employment: Lenders want to see that you have a consistent and verifiable source of income. This reassures them that you have the financial means to make your monthly payments. Long-term employment with the same employer is a huge plus.

- Provide a Strong Down Payment: As discussed, a down payment reduces the risk for the lender and shows your commitment. The more you can put down, the better your chances of approval and potentially securing a better interest rate.

- Choose a Realistic Vehicle: Don’t aim for the most expensive car you can imagine. Opt for a reliable, moderately priced used vehicle that aligns with your income and budget. Lenders are more likely to approve a loan for a car they deem appropriate for your financial situation.

- Clean Up Minor Credit Report Errors: Even if your credit isn’t perfect, it’s worth checking your credit report for inaccuracies. Dispute any errors you find; removing them could slightly improve your score and present a more accurate financial picture.

- Consider a Co-Signer (If Applicable): If you have a trusted friend or family member with good credit who is willing to co-sign for you, this can dramatically increase your chances of approval and potentially secure a lower interest rate. Remember, a co-signer is equally responsible for the loan, so it’s a serious commitment.

- Maintain a Low Debt-to-Income Ratio: While Snap Car Loan caters to those with challenges, having too much existing debt compared to your income can still be a red flag. Try to pay down other small debts before applying.

- Be Honest and Transparent: Provide accurate information on your application. Any misrepresentation can lead to delays or outright rejection. Honesty builds trust with the lender.

Beyond Approval: Managing Your Snap Car Loan Responsibly

Getting approved for a Snap Car Loan is a significant first step, but the journey doesn’t end there. Responsible management of your loan is crucial for achieving financial stability and improving your credit score. Pro tips from us: Treat this loan as an opportunity to build a stronger financial future.

1. Make Timely Payments, Every Time

This is arguably the most critical aspect of responsible loan management. Missing payments or making them late will negatively impact your credit score and can incur late fees. Set up automatic payments from your bank account to ensure you never miss a due date. If automatic payments aren’t an option, mark your calendar and set reminders.

Consistent, on-time payments are reported to credit bureaus and are a powerful way to demonstrate financial responsibility. This will be instrumental in improving your credit score over time.

2. Budget for the Total Cost of Car Ownership

Your monthly car payment is just one piece of the puzzle. Don’t forget to budget for other essential expenses associated with vehicle ownership:

- Car Insurance: Mandatory in most places, and rates can be higher for newer drivers or those with a history of claims.

- Fuel: A significant ongoing cost, especially with fluctuating gas prices.

- Maintenance: Regular oil changes, tire rotations, and unexpected repairs are inevitable. Set aside a small amount each month for a "car maintenance fund."

- Registration and Licensing Fees: Annual costs that vary by state.

Ignoring these costs can quickly lead to financial stress, making it difficult to keep up with your car payments.

3. Understand the Impact on Your Credit Score

A Snap Car Loan, when managed well, can be a powerful tool for credit building. Each on-time payment contributes positively to your payment history, which is the most influential factor in your credit score. As your credit score improves, you’ll gain access to better financial products and lower interest rates in the future.

Conversely, late payments, defaults, or repossessions will severely damage your credit, making it even harder to secure financing in the future. This loan is a chance to reset and demonstrate reliability. For more in-depth advice on improving your credit, you might find our article on helpful.

4. Explore Refinancing Possibilities

After a year or two of making consistent, on-time payments, your credit score will likely have improved significantly. At this point, you may be eligible to refinance your Snap Car Loan with a traditional lender at a much lower interest rate.

Refinancing can save you a substantial amount of money over the remaining life of the loan. Keep an eye on your credit score and shop around for refinancing offers once you feel your credit has stabilized and improved.

Potential Downsides and How to Mitigate Them

While Snap Car Loan offers a valuable service, it’s crucial to be aware of potential drawbacks. Understanding these allows you to make an informed decision and take steps to mitigate risks. Common mistakes to avoid include ignoring these potential issues until they become problems.

1. Higher Interest Rates

As mentioned, subprime loans inherently come with higher interest rates due to the increased risk lenders undertake. This means you will pay more in total interest compared to someone with excellent credit.

- Mitigation: Focus on making a substantial down payment to reduce the principal. Also, actively work on improving your credit score so you can refinance to a lower rate as soon as possible. Regularly check your credit report for errors and make timely payments on all debts.

2. Risk of Negative Equity

Negative equity, or being "upside down" on your loan, occurs when you owe more on your car than it’s currently worth. This is a common issue with new and some used vehicles, especially with long loan terms and minimal down payments, because cars depreciate quickly.

- Mitigation: Make a significant down payment. Choose a vehicle that holds its value reasonably well. Consider a shorter loan term if your budget allows. Avoid adding extra products (like extended warranties) into the financing if you can pay for them separately, as this increases the loan amount without adding to the car’s inherent value.

3. Limited Vehicle Selection (Potentially)

Depending on the dealership and your specific approval terms, your choice of vehicles might be somewhat limited. You might not qualify for the newest or most luxurious models.

- Mitigation: Be flexible and realistic about your vehicle needs versus wants. Focus on reliability and affordability. Remember that this vehicle is a stepping stone. Once your credit improves, you’ll have more options in the future.

4. The Temptation to Over-Borrow

Because lenders are focusing on your ability to pay rather than just your credit score, there might be a temptation to take out a larger loan than you truly need or can comfortably afford.

- Mitigation: Stick to your budget. Determine your absolute maximum affordable monthly payment (including all car ownership costs) before you start shopping. Don’t let a dealership pressure you into a more expensive vehicle than you planned for. This external link to the Consumer Financial Protection Bureau (CFPB) offers excellent general advice on smart car buying: https://www.consumerfinance.gov/consumer-tools/auto-loans/

Alternatives to Snap Car Loan

While Snap Car Loan offers a valuable service, it’s always wise to explore all your options, especially if you’re concerned about higher interest rates or other terms. There are other avenues to consider for auto financing, particularly for those with credit challenges.

1. Credit Unions

Credit unions are non-profit organizations that often offer more flexible lending terms and lower interest rates than traditional banks, especially for members. If you have a relationship with a credit union, or can join one, it’s worth checking their auto loan offerings. They are often more willing to work with individuals who have a less-than-perfect credit history, viewing them as members rather than just numbers.

2. Other Subprime Lenders

Snap Car Loan is one player in the subprime auto lending market, but it’s not the only one. There are other specialized lenders and online platforms that cater to borrowers with bad credit. Shopping around and comparing offers from multiple lenders can help you find the best possible terms.

Be cautious, however, and always research the reputation of any lender before proceeding. Look for transparent terms and positive customer reviews.

3. Buy Here Pay Here Dealerships (with caution)

These dealerships offer in-house financing, meaning they are both the seller and the lender. They often approve individuals with very poor credit, as they prioritize your ability to make payments directly to them.

However, "Buy Here Pay Here" dealerships often come with significantly higher interest rates, shorter repayment terms, and limited vehicle warranties. They can be a last resort but should be approached with extreme caution, and you should thoroughly understand every aspect of the loan agreement.

4. Saving Up for a Cheaper Car

If immediate transportation isn’t an absolute emergency, consider saving up enough cash to buy a cheaper, reliable used car outright. This eliminates interest payments entirely and avoids the complexities of loans. It’s the most financially sound option if patience is a luxury you can afford.

For a deeper dive into other car financing options, including more about credit unions and general auto loan advice, read our comprehensive article on .

Conclusion: Your Road to Financial Freedom with Snap Car Loan

Securing a vehicle with a less-than-perfect credit history can feel like an uphill battle, but solutions like Snap Car Loan exist precisely to help individuals overcome these hurdles. By acting as a crucial bridge between borrowers and specialized lenders, Snap Car Loan offers a genuine opportunity for transportation and, more importantly, for financial rehabilitation.

Throughout this comprehensive guide, we’ve explored what Snap Car Loan entails, who it benefits most, and how to navigate its application process with confidence. We’ve highlighted the critical importance of understanding loan terms, maximizing your approval chances, and managing your loan responsibly to build a stronger financial future. While potential downsides exist, they are manageable with careful planning and informed decision-making.

Remember, a Snap Car Loan is more than just a means to get a car; it’s a powerful tool for credit building. By making consistent, on-time payments, you’re not just paying for your vehicle; you’re investing in your financial future, paving the way for better opportunities and lower interest rates down the road. Take the first step today, explore your options, and embark on your journey towards reliable transportation and enhanced financial freedom with Snap Car Loan.