Unlocking Your Ideal Auto Loan: A Deep Dive into Good Car Loan Companies and Smart Financing Strategies

Unlocking Your Ideal Auto Loan: A Deep Dive into Good Car Loan Companies and Smart Financing Strategies Carloan.Guidemechanic.com

The dream of a new car – the fresh scent, the smooth ride, the freedom of the open road – is exhilarating. But before you can cruise off into the sunset, there’s a crucial step: securing the right financing. For many, this means navigating the complex world of car loans. The choice of your car loan company isn’t just a minor detail; it’s a decision that will profoundly impact your financial well-being for years to come.

Finding good car loan companies is paramount to a successful vehicle purchase. It’s about more than just getting approved; it’s about securing terms that fit your budget, understanding the fine print, and feeling confident in your financial partner. This comprehensive guide will empower you with the knowledge and strategies needed to identify the best auto loan options, ensuring you drive away with not just a great car, but also a smart financial deal.

Unlocking Your Ideal Auto Loan: A Deep Dive into Good Car Loan Companies and Smart Financing Strategies

Why Choosing the Right Car Loan Company Matters Immensely

Many prospective car buyers make the mistake of focusing solely on the vehicle’s price and monthly payment, overlooking the significance of the lender. Based on my experience in the automotive and finance industries, this oversight can lead to thousands of dollars in unnecessary interest and a less-than-ideal borrowing experience.

Your choice of a car loan company directly influences your interest rate, the total amount you’ll pay over the life of the loan, and even the flexibility you have if financial circumstances change. A reputable lender offers transparent terms, competitive rates, and excellent customer service, fostering a stress-free borrowing journey. Conversely, a poor choice can lead to hidden fees, inflexible terms, and frustrating interactions.

Key Factors That Define a "Good" Car Loan Company

Not all lenders are created equal. Distinguishing between a mediocre option and one of the truly good car loan companies requires understanding the core attributes that set them apart. These factors are your checklist when evaluating potential financing partners.

1. Competitive Interest Rates and APR

The interest rate is arguably the most critical factor in a car loan, directly determining how much extra you pay for the privilege of borrowing. A good company offers rates that are competitive based on your credit profile and current market conditions. They understand that a lower Annual Percentage Rate (APR) translates to significant savings for you.

Always look beyond just the advertised interest rate; focus on the APR. The APR includes not only the interest rate but also any additional fees associated with the loan, providing a more accurate picture of the total annual cost of borrowing. A transparent lender will always highlight the APR clearly.

2. Transparent Terms and Conditions

Hidden fees and confusing clauses are red flags. A truly good car loan company prides itself on transparency, clearly outlining all terms and conditions upfront. This means no surprises regarding origination fees, prepayment penalties, or late payment charges.

They will provide you with a straightforward loan agreement that is easy to understand, allowing you to make an informed decision. Pro tips from us: always read the entire loan agreement, no matter how long, before signing. If anything is unclear, ask for clarification.

3. Excellent Customer Service and Support

Borrowing money can be complex, and questions or issues may arise during the life of your loan. A reputable lender offers accessible and responsive customer service. This includes easy-to-reach support via phone, email, or online chat, and knowledgeable representatives who can assist with inquiries about payments, refinancing, or account management.

Look for companies with positive customer reviews regarding their support staff and problem resolution. A smooth application process is good, but ongoing support is what truly defines a long-term positive relationship.

4. Flexible Repayment Options

Life is unpredictable, and a good car loan company recognizes this by offering some degree of flexibility. This could include a range of loan terms (e.g., 36, 48, 60, 72 months) to help you manage your monthly payments, or options for payment deferrals in times of hardship.

While flexibility is good, remember that longer terms often mean paying more interest over time. A good lender will help you understand the trade-offs between a lower monthly payment and the total cost of the loan.

5. Streamlined and Efficient Application Process

In today’s digital age, convenience is key. Good car loan companies typically offer an efficient, user-friendly online application process that can often provide pre-approval or instant decisions. This saves you time and reduces stress.

They will clearly list the required documents and guide you through each step, making the journey from application to approval as smooth as possible. This efficiency reflects a company that values your time and embraces modern technology.

6. Strong Reputation and Positive Reviews

Before committing to any lender, investigate their reputation. Look at independent review sites, consumer protection agency ratings, and financial forums. Good car loan companies will generally have a high rating with organizations like the Better Business Bureau (BBB) and consistently positive feedback from past and current customers.

Pay attention to recurring complaints or praises. A pattern of unresolved issues or poor customer interactions is a clear warning sign to avoid. Conversely, consistent praise for fairness and helpfulness indicates a trustworthy lender.

7. Diverse Range of Loan Products

A lender that offers a variety of loan products demonstrates a commitment to serving diverse customer needs. This might include loans for new cars, used cars, refinancing existing loans, or even options for those with less-than-perfect credit.

This versatility indicates a comprehensive understanding of the market and a desire to match customers with the most suitable financial solutions. It means they’re not just a one-size-fits-all provider.

Types of Car Loan Companies You’ll Encounter

The landscape of auto financing is broad, with several types of institutions vying for your business. Understanding their unique characteristics can help you narrow down your search for good car loan companies.

1. Banks (Traditional Lenders)

Pros: Established institutions, often offer competitive rates for borrowers with excellent credit, familiar banking relationships.

Cons: Can have stricter credit requirements, slower approval processes, less flexibility for those with challenged credit.

Major national and regional banks are often the first stop for many seeking auto loans. They typically offer a stable and secure lending environment. If you have a strong credit history and an existing relationship with a bank, you might find attractive rates.

However, their stringent underwriting criteria can make it challenging for individuals with lower credit scores to qualify for their best offers. It’s always worth checking with your current bank first, as they might offer loyalty discounts.

2. Credit Unions

Pros: Member-focused, often offer lower interest rates than banks, more flexible with borrowers, strong community ties.

Cons: Requires membership (often easy to join), may have fewer branches or online tools than large banks.

Credit unions are non-profit financial cooperatives, meaning their profits are returned to members in the form of lower rates and fees. They are often among the good car loan companies for competitive rates and a more personalized approach.

While you need to be a member to borrow, joining is usually straightforward, often requiring just a small deposit or meeting a simple geographic or associational criterion. Don’t overlook credit unions in your search; they can be a hidden gem for auto financing.

3. Online Lenders

Pros: Convenience, speed, easy comparison shopping, often cater to a broader range of credit scores.

Cons: Less personal interaction, can be harder to vet legitimacy without physical presence, rates vary widely.

The digital age has brought a surge of online-only lenders specializing in auto financing. These platforms offer unparalleled convenience, allowing you to apply and get pre-approved from the comfort of your home. They are often quick, providing decisions within minutes.

Many online lenders use advanced algorithms to assess risk, which can sometimes translate to options for borrowers who might not qualify with traditional banks. However, it’s crucial to thoroughly research any online lender to ensure they are reputable and secure.

4. Dealership Financing

Pros: Convenience (one-stop shop), potential for special manufacturer incentives, can facilitate loans for various credit types.

Cons: Potentially higher interest rates, less transparency, limited comparison shopping.

Dealerships often act as intermediaries, connecting you with a network of lenders. While convenient, this "one-stop shop" approach can sometimes come at a cost. The dealership might mark up the interest rate to earn a profit, or push you towards lenders that offer them the best commission.

While some manufacturer-backed deals can be excellent, it’s always wise to arrive at the dealership with your own pre-approval in hand. This gives you leverage and a benchmark against which to compare their offers.

5. Specialty Lenders (Bad Credit Auto Loans)

Pros: Provide options for those with challenged credit, focus on specific financial situations.

Cons: Generally higher interest rates, stricter terms, potential for predatory practices if not chosen carefully.

For individuals with poor credit scores, specialty lenders fill a critical gap. These companies are willing to take on higher risks but typically charge higher interest rates to compensate. When exploring these options, it’s especially important to identify good car loan companies that are transparent and fair.

Avoid lenders that pressure you, demand large upfront fees, or offer terms that seem too good to be true. Always verify their licensing and check reviews carefully.

The Pre-Approval Advantage: Your Secret Weapon

One of the most powerful strategies when seeking a car loan is getting pre-approved. This step is often overlooked, but it can transform your car-buying experience from stressful to empowering.

Pre-approval means a lender has reviewed your credit and financial information and determined that you qualify for a loan up to a certain amount, at a specific interest rate. This is usually a "soft inquiry" on your credit report, meaning it won’t negatively impact your score.

How Pre-Approval Empowers You

Walking into a dealership with a pre-approval letter in hand is like having cash. It immediately establishes you as a serious buyer with financing already secured. This shifts the negotiation power from the dealership to you. You can focus on negotiating the car’s price, knowing exactly what financing terms you qualify for independently.

It also acts as a benchmark. Any financing offer from the dealership can be directly compared to your pre-approved loan, ensuring you get the best possible deal. If their offer is higher, you can confidently decline and stick with your pre-approval.

How to Compare Car Loan Offers Like a Pro

Once you have multiple offers from good car loan companies, comparing them effectively is crucial. Don’t just look at the monthly payment; delve into the details.

1. APR vs. Interest Rate: Know the Difference

As mentioned, the APR (Annual Percentage Rate) is your best friend. The interest rate is just one component. The APR includes the interest rate plus any fees (like origination fees) charged by the lender, expressed as an annual percentage.

Always compare offers based on their APR, not just the advertised interest rate. A lower interest rate with high fees can result in a higher overall APR than an offer with a slightly higher interest rate but no fees.

2. Loan Term: Shorter vs. Longer

The loan term is the length of time you have to repay the loan (e.g., 36, 48, 60, 72 months). A shorter loan term means higher monthly payments but significantly less interest paid over the life of the loan.

A longer loan term results in lower monthly payments, making the car seem more affordable initially. However, you’ll end up paying substantially more in total interest. Common mistakes to avoid are extending the loan term too much just to lower the monthly payment, as this can lead to being "upside down" on your loan (owing more than the car is worth).

3. Down Payment: Your Financial Lever

A larger down payment reduces the amount you need to borrow, which directly lowers your monthly payments and the total interest paid. It also signals to lenders that you’re a lower risk, potentially securing you a better interest rate.

Pro tips from us: aim for at least a 10-20% down payment if possible. This not only saves you money but also provides a buffer against depreciation, reducing the risk of negative equity.

4. Fees: Read the Fine Print

Be vigilant about any fees associated with the loan. These can include origination fees, application fees, or prepayment penalties. While good car loan companies are transparent, some may try to sneak in charges.

Prepayment penalties are particularly important to watch out for. These are fees charged if you pay off your loan early. Ideally, look for loans without such penalties, giving you the flexibility to pay down your debt faster if you wish.

5. Total Cost of the Loan: The Ultimate Metric

To truly compare offers, calculate the total cost of each loan. This is the sum of the principal amount borrowed plus all interest and fees over the entire loan term.

For example, a $20,000 loan at 5% APR for 60 months might cost roughly $22,645 in total. The same loan at 6% APR for 72 months might have a lower monthly payment but cost over $24,000 in total. Use an online car loan calculator to quickly compare these figures.

Preparing for Your Car Loan Application

Being prepared can streamline the application process and increase your chances of securing the best terms from good car loan companies.

First, gather all necessary documents. This typically includes government-issued identification (driver’s license), proof of income (pay stubs, tax returns), proof of residence (utility bills), and possibly bank statements. Having these ready will prevent delays.

Second, check your credit score and report. You are entitled to a free credit report from each of the three major bureaus annually. Review it for any errors and address them before applying. Understanding your credit score gives you insight into the types of rates you can expect. For a deeper dive into improving your credit score, check out our article on .

Finally, understand your budget. Don’t just think about the monthly car payment; factor in insurance, fuel, maintenance, and potential parking costs. A good car loan should fit comfortably within your overall financial picture.

Common Mistakes to Avoid When Seeking a Car Loan

Based on years of observing car buyers, certain pitfalls repeatedly trip people up. Avoiding these can save you considerable time, money, and stress.

1. Not Getting Pre-Approved

As discussed, skipping pre-approval is a significant missed opportunity. It leaves you vulnerable to dealership markups and limits your negotiating power. Always secure independent financing offers first.

2. Focusing Only on Monthly Payment

This is perhaps the most common mistake. Salespeople are adept at manipulating the loan term to achieve a "low monthly payment" without disclosing the total cost. Always look at the APR and the total amount paid over the loan’s life.

3. Not Reading the Fine Print

The devil is often in the details. Skipping the thorough review of your loan contract can lead to unexpected fees, unfavorable terms, or even predatory clauses. Take your time, ask questions, and understand every line.

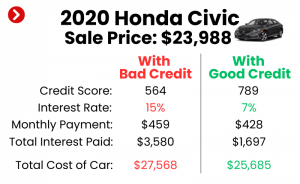

4. Ignoring Your Credit Score

Your credit score is a major determinant of your interest rate. If you don’t know your score, you can’t accurately gauge the competitiveness of an offer. Work on improving it if necessary before applying.

5. Accepting the First Offer

Whether it’s from your bank or the dealership, never take the first offer. Shop around, compare multiple lenders, and leverage competition to get the best deal. This is where identifying multiple good car loan companies becomes invaluable.

Pro Tips for Securing the Best Car Loan

To truly master the car loan process and align yourself with the best possible terms, consider these expert recommendations.

- Boost Your Credit Score: Even a small improvement in your credit score can translate into a significantly lower interest rate. Pay down credit card debt, ensure on-time payments, and dispute any errors on your credit report.

- Save for a Larger Down Payment: The more you can put down upfront, the less you need to borrow. This reduces your overall interest costs and can lead to more favorable loan terms.

- Shop Around Aggressively: Don’t settle for the first quote. Apply to at least 3-5 different good car loan companies (banks, credit unions, online lenders) within a short period (typically 14-45 days) to minimize the impact on your credit score. Multiple inquiries within this window are usually counted as a single inquiry for rate shopping.

- Negotiate Effectively: Use your pre-approval as leverage when negotiating at the dealership. Be prepared to walk away if the terms aren’t favorable.

- Consider Refinancing Later: If you secure a car loan with less-than-ideal terms (e.g., due to poor credit at the time of purchase), you can always refinance your loan later once your credit score improves or interest rates drop. Many good car loan companies also specialize in refinancing. If you’re curious about the mechanics of monthly payments, our guide to provides further insights.

Conclusion: Drive Away with Confidence

Navigating the world of car loans can seem daunting, but by arming yourself with knowledge, you can transform a potentially stressful experience into a confident decision. The key lies in understanding what makes good car loan companies stand out: transparency, competitive rates, excellent service, and flexibility.

By getting pre-approved, comparing offers diligently based on APR and total cost, and avoiding common mistakes, you position yourself for success. Remember, the goal is not just to get a car, but to get a car on terms that genuinely work for your financial future. Do your homework, ask the right questions, and you’ll be well on your way to driving off with your ideal vehicle and an auto loan that makes sense. For more general advice on consumer finance and loans, you can always consult trusted resources like the Consumer Financial Protection Bureau (CFPB) website.