Unlocking Your Maximum Car Loan: A Comprehensive Guide to Driving Your Dream Car Home

Unlocking Your Maximum Car Loan: A Comprehensive Guide to Driving Your Dream Car Home Carloan.Guidemechanic.com

Buying a car is a significant financial decision, often representing one of the largest purchases many individuals make after a home. For most, securing a car loan is an essential step in this journey. But have you ever wondered, "What’s the absolute maximum car loan I can get?" This question, while seemingly straightforward, opens up a world of factors that influence not just the loan amount, but also your financial well-being.

As an expert blogger and professional in the financial content space, I’ve seen countless individuals navigate the complexities of auto financing. My mission today is to equip you with the knowledge to not only understand your maximum car loan potential but also to strategically position yourself for the best possible terms. We’ll delve deep into the mechanics of car loans, explore the critical factors lenders consider, and provide actionable strategies to maximize your approval while ensuring you make a financially sound decision. This isn’t just about getting the biggest loan; it’s about getting the right loan for your circumstances.

Unlocking Your Maximum Car Loan: A Comprehensive Guide to Driving Your Dream Car Home

What Does "Maximum Car Loan" Truly Mean? Beyond Just the Highest Number

When we talk about a "maximum car loan," it’s easy to think solely of the highest dollar figure a lender might offer. However, this perspective is incomplete and potentially misleading. A truly maximum car loan isn’t just the most money you can borrow; it’s the largest amount you can responsibly afford without jeopardizing your other financial commitments or sinking into overwhelming debt.

Lenders, of course, have their own maximums based on their risk assessment models. They evaluate your creditworthiness, income, and existing debts to determine how much they’re willing to lend. But your personal "maximum" should always be guided by your budget and long-term financial goals. Taking on too much car debt, even if approved, can lead to financial strain, making it difficult to save, invest, or handle unexpected expenses. It’s a delicate balance between lender willingness and personal affordability.

The Pillars of Your Car Loan Eligibility: Key Factors Lenders Assess

Lenders are essentially evaluating risk when you apply for a car loan. They want to ensure you have the capacity and willingness to repay the borrowed amount. Several key factors form the bedrock of their decision-making process, directly influencing how much car loan you can secure and at what interest rate. Understanding these elements is your first step towards maximizing your car loan potential.

1. Your Credit Score: The Cornerstone of Loan Approval

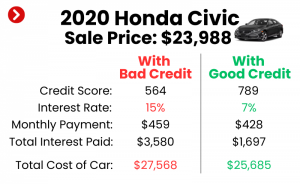

Your credit score is arguably the single most influential factor in determining your car loan eligibility and the terms you’ll receive. This three-digit number, often a FICO or VantageScore, acts as a summary of your credit history, reflecting your reliability as a borrower. A higher credit score signals lower risk to lenders, making them more willing to offer larger loan amounts at more favorable interest rates.

Based on my experience, a credit score above 720 is generally considered "excellent," opening doors to the best rates and highest loan limits. Scores between 660 and 719 are typically good, while those below 600 might face higher interest rates or require a larger down payment. Lenders use this score to quickly gauge your past payment behavior, the types of credit you’ve managed, and your overall debt burden. It’s a snapshot of your financial responsibility, directly impacting the maximum car loan amount you qualify for.

2. Income and Employment Stability: Proving Your Repayment Capacity

Lenders need assurance that you have a consistent and sufficient income stream to comfortably cover your monthly car loan payments. They’re not just looking at the number on your pay stub; they’re also scrutinizing the stability of your employment. A long history with the same employer or within the same industry signals reliability.

They will typically ask for proof of income, such as pay stubs, W-2 forms, or tax returns (especially for self-employed individuals). While there isn’t a universal minimum income for a car loan, lenders want to see that your income is substantial enough to cover not only the car payment but also your existing debts and living expenses. This income-to-expense ratio is crucial for them to determine your maximum car loan capacity.

3. Debt-to-Income (DTI) Ratio: A Critical Affordability Metric

Your Debt-to-Income (DTI) ratio is a powerful indicator of your financial health and a major determinant of your maximum car loan. It’s calculated by dividing your total monthly debt payments (including rent/mortgage, credit card minimums, student loans, etc.) by your gross monthly income. This percentage tells lenders how much of your income is already committed to debt.

A lower DTI ratio suggests you have more disposable income available to take on a new car loan payment. Most lenders prefer a DTI ratio below 43%, though some may approve loans for applicants with slightly higher ratios if other factors are exceptionally strong. Pro tips from us: aiming for a DTI under 36% before applying for a car loan significantly strengthens your position and can increase your maximum approval amount.

4. Your Down Payment: Reducing Lender Risk and Loan Amount

The amount of money you put down upfront on a car plays a significant role in your car loan approval and the total amount you need to borrow. A substantial down payment immediately reduces the principal loan amount, which in turn lowers your monthly payments and the total interest paid over the life of the loan. From a lender’s perspective, a larger down payment also signifies a greater commitment from you, reducing their risk.

Common mistakes to avoid are underestimating the power of a down payment. Even a 10-20% down payment can make a noticeable difference in your loan terms and approval odds. For used cars, where depreciation can be faster, a larger down payment is often even more crucial to avoid being "upside down" on your loan (owing more than the car is worth).

5. Loan Term and Interest Rate: The Interplay of Cost and Time

The loan term (how long you have to repay the loan) and the interest rate are inextricably linked and directly impact your monthly payment, and thus, the maximum car loan you can afford. A longer loan term generally results in lower monthly payments, which might seem appealing as it allows you to "afford" a more expensive car. However, it also means you’ll pay more in total interest over the life of the loan.

Conversely, a shorter loan term means higher monthly payments but less total interest paid. Lenders often have limits on the maximum loan term they’ll offer, especially for older vehicles. Understanding this balance is key; while a longer term might increase your approved loan amount, it might not be the most financially savvy choice in the long run.

6. Vehicle Age and Type: Asset Value and Depreciation

The specific car you’re looking to finance also influences the maximum loan amount. Lenders consider the vehicle’s age, make, model, and condition because these factors affect its resale value and how quickly it depreciates. Newer cars, especially those with good reliability ratings, are generally easier to finance for higher amounts because they hold their value better.

Used cars, particularly older models, may have stricter lending criteria, including lower maximum loan-to-value (LTV) ratios. This means lenders might only finance a certain percentage of the car’s market value, requiring a larger down payment from you. Luxury vehicles might also face different lending standards due to their higher price points and specialized market.

7. Co-signer (If Applicable): A Boost for Eligibility

If you have a lower credit score or insufficient income, a co-signer with excellent credit and stable income can significantly improve your chances of getting approved for a car loan, and potentially for a higher amount. A co-signer essentially guarantees the loan, promising to make payments if you default. This reduces the risk for the lender.

However, it’s crucial to understand the implications for the co-signer. Their credit is on the line, and any missed payments will negatively impact their credit score as well as yours. While a co-signer can help you reach your maximum car loan potential, it should be a carefully considered decision for both parties.

Strategies to Maximize Your Car Loan Approval and Amount

Now that we understand the factors, let’s explore proactive strategies you can employ to not only increase your chances of approval but also potentially secure a larger loan amount with better terms. These aren’t quick fixes but rather smart financial moves that demonstrate your reliability to lenders.

1. Improve Your Credit Score: A Long-Term Investment

Improving your credit score is one of the most effective ways to boost your car loan potential. Start by checking your credit report for errors and disputing any inaccuracies. Focus on paying all your bills on time, as payment history is the largest component of your score. Reduce your credit card balances to lower your credit utilization ratio (the amount of credit you’re using compared to your total available credit).

Pro tips from us: Even a small increase in your credit score can translate into thousands of dollars saved over the life of a car loan. This is a journey, not a sprint, so start well before you plan to buy a car. For more detailed guidance, consider reading our article on (Internal Link 1 Placeholder).

2. Increase Your Down Payment: Show Your Commitment

As discussed, a larger down payment significantly strengthens your loan application. It reduces the amount you need to borrow, lowers your monthly payments, and signals financial stability to lenders. Make it a priority to save aggressively for a down payment before you even start car shopping.

Consider selling an existing vehicle, saving tax refunds, or temporarily cutting discretionary spending to build up your down payment fund. Even an extra few hundred or thousand dollars can make a difference in your approved loan amount and interest rate.

3. Reduce Existing Debt: Optimize Your DTI

Lowering your existing debt, especially high-interest credit card debt, directly improves your DTI ratio. This shows lenders that you have more financial bandwidth to take on a new car payment. Focus on paying down your smallest debts first to gain momentum, or tackle high-interest debts to save money.

Reducing your DTI is a powerful strategy. It directly impacts your perceived affordability and can be a significant factor in a lender’s decision to offer you a higher maximum car loan amount. It demonstrates responsible financial management.

4. Shop Around for Lenders: Don’t Settle for the First Offer

This is a critical step many car buyers overlook. Don’t just accept the financing offered by the dealership. Banks, credit unions, and online lenders often have competitive rates and terms. Apply for pre-approval with several different lenders to compare offers.

Based on my experience, credit unions, in particular, often offer some of the most competitive auto loan rates because they are member-owned and non-profit. Shopping around within a short timeframe (usually 14-45 days, depending on the credit scoring model) will only count as a single hard inquiry on your credit report, so it won’t negatively impact your score significantly.

5. Get Pre-Approved: Walk in with Power

Pre-approval is a game-changer. It means a lender has already reviewed your finances and determined how much they’re willing to lend you, at what interest rate, and for what term. You’ll receive a pre-approval letter stating these terms. This transforms you into a cash buyer at the dealership, giving you significant leverage in negotiations.

With pre-approval in hand, you can focus solely on negotiating the car’s price, rather than juggling both the car price and financing terms simultaneously. It also gives you a clear maximum budget, preventing you from falling in love with a car you can’t truly afford.

6. Consider a Co-signer (Wisely): A Strategic Boost

If your credit isn’t strong enough on its own, a co-signer can be a valuable asset. However, this decision should not be taken lightly. Ensure both you and your co-signer fully understand the responsibilities and risks involved.

A co-signer should be someone with excellent credit and a stable financial history, and most importantly, someone you trust implicitly and who trusts you. While it can help you secure a higher maximum car loan, it’s a shared financial obligation.

Common Mistakes to Avoid When Seeking a Maximum Car Loan

Even with the best intentions, car buyers can make missteps that hinder their ability to secure a good car loan or lead to financial regret. Based on my experience, here are some common mistakes to actively avoid:

- Applying to Too Many Lenders Haphazardly: While shopping around is good, submitting countless applications over an extended period can negatively impact your credit score due to multiple hard inquiries. Bundle your applications within a short window to minimize impact.

- Ignoring Your Debt-to-Income (DTI) Ratio: Focusing solely on your credit score without considering your DTI is a common pitfall. Lenders look at both. A high DTI, even with good credit, can limit your maximum loan amount.

- Focusing Only on the Monthly Payment: This is perhaps the biggest mistake. A low monthly payment achieved through a very long loan term often means paying significantly more in total interest. Always consider the total cost of the loan, not just the monthly figure.

- Not Reading the Fine Print: Always thoroughly review your loan agreement. Understand the interest rate, any fees, prepayment penalties (though rare for auto loans), and the total amount you’ll repay. Don’t be rushed into signing.

- Misrepresenting Income or Information: This is not only unethical but can lead to severe legal consequences. Always be honest and accurate in your loan application. Lenders will verify your information.

- Buying More Car Than You Can Truly Afford: Just because a lender approves you for a certain maximum amount doesn’t mean you should borrow that much. Always factor in insurance, maintenance, fuel, and other hidden costs.

Calculating Your True Affordability: Beyond the Loan Amount

Securing a maximum car loan is only one piece of the puzzle. The true measure of a financially savvy car purchase is whether you can truly afford the total cost of ownership. This goes beyond the monthly loan payment and includes several other significant expenses.

Consider these often-overlooked costs:

- Car Insurance: The cost of insurance can vary wildly based on the car’s value, your driving record, age, and location. Get insurance quotes before you finalize your car purchase.

- Fuel Costs: Estimate your monthly fuel expenses based on your commute and the car’s fuel efficiency.

- Maintenance and Repairs: All cars require maintenance, and older or luxury vehicles can have significantly higher repair costs. Research typical maintenance schedules and common issues for the specific model you’re considering.

- Registration and Taxes: Factor in annual registration fees and any sales tax associated with the purchase.

- Parking Fees/Tolls: If applicable, these can add up over time.

Pro tips from us: Create a comprehensive car budget that includes all these elements. For detailed guidance on creating a budget for your new vehicle, refer to our article: (Internal Link 2 Placeholder). This holistic approach ensures your "maximum car loan" aligns with your overall financial health, not just a lender’s approval.

The Pre-Approval Advantage: Your Secret Weapon

We briefly touched on pre-approval, but its importance warrants a deeper dive. Getting pre-approved is arguably the most powerful tool in your car buying arsenal. It shifts the power dynamic from the dealership to you.

When you walk into a dealership with a pre-approval letter, you’re essentially telling them, "I already have financing secured." This forces them to compete with your existing offer. They might try to beat your rate, or at the very least, they know they can’t inflate the financing terms to compensate for a lower car price. It separates the car negotiation from the financing negotiation, making both processes clearer and more transparent.

Pre-approval also gives you invaluable clarity on your budget. You know precisely how much you can spend, preventing emotional overspending. It streamlines the purchase process, allowing you to drive away in your new car faster once you’ve made your selection.

Dealership vs. Bank/Credit Union: Where to Get the Best Deal

The question of where to secure your car loan is fundamental. Both dealerships and independent financial institutions (banks, credit unions, online lenders) offer financing, but their approaches and potential benefits can differ significantly.

- Dealership Financing: Dealerships often act as intermediaries, working with multiple lenders (banks, captive finance companies like Toyota Financial Services, etc.). They can offer convenience, sometimes matching or even beating outside offers to close a sale. However, they may also mark up interest rates to profit from the financing. Common mistakes to avoid are assuming the dealership’s "best offer" is truly the best without comparing it to external options.

- Banks and Credit Unions: These institutions directly lend money. As mentioned, credit unions are particularly known for competitive rates due to their non-profit structure. Banks offer a wide range of products and often have established relationships with their customers. Applying directly to these institutions gives you a transparent view of their rates and terms before you step foot on a lot.

Pro tips from us: The ideal strategy is to get pre-approved from a bank or credit union before visiting the dealership. Use that pre-approval as leverage. See if the dealership can beat it. If not, you have a solid financing option ready. This ensures you’re getting the most competitive terms available. For more insights on smart car buying, explore resources like the Consumer Financial Protection Bureau (CFPB) auto loan guide:

Conclusion: Driving Away with Confidence and a Smart Loan

Securing your maximum car loan isn’t just about the highest dollar figure; it’s about intelligent borrowing that aligns with your financial capacity and long-term goals. We’ve explored the critical factors lenders scrutinize – from your credit score and DTI to your down payment and employment stability. We’ve also armed you with actionable strategies, such as improving your credit, increasing your down payment, shopping for lenders, and leveraging pre-approval, all designed to put you in the driver’s seat of your financial future.

Remember, the goal is not merely to get approved for a car loan, but to secure the best car loan for your situation – one that offers favorable terms and doesn’t strain your budget. By understanding these principles and implementing these strategies, you’re well on your way to making an informed decision, driving home your dream car with confidence, and maintaining robust financial health. Happy car hunting, and may your loan terms be ever in your favor!