Unlocking Your Ride: A Comprehensive Guide to Navigating Car Loans with Confidence (Inspired by the Lincoln Financial Standard)

Unlocking Your Ride: A Comprehensive Guide to Navigating Car Loans with Confidence (Inspired by the Lincoln Financial Standard) Carloan.Guidemechanic.com

The open road beckons, and for many, a new vehicle represents freedom, convenience, and a significant life milestone. However, the journey to car ownership often begins long before you even set foot on a dealership lot – it starts with understanding car loans. Securing the right auto financing can be as crucial as choosing the car itself, impacting your monthly budget, long-term financial health, and overall peace of mind.

In this comprehensive guide, we’ll delve deep into the world of car loans, exploring every facet from understanding the basics to mastering the application process and managing your debt responsibly. While Lincoln Financial Group is primarily known for its robust insurance and retirement planning solutions, the name itself evokes a standard of financial stability, comprehensive service, and client-centric approaches. When we discuss "Lincoln Financial Car Loans" in this context, we’re drawing a parallel to the caliber of reliable, well-structured auto financing you should seek from any reputable financial institution. Our aim is to equip you with the knowledge to approach car financing with the same confidence and strategic planning associated with top-tier financial guidance.

Unlocking Your Ride: A Comprehensive Guide to Navigating Car Loans with Confidence (Inspired by the Lincoln Financial Standard)

Based on my extensive experience in financial writing and consumer credit, navigating car loans can feel daunting, but with the right insights, it becomes a clear path. This article will serve as your ultimate resource, ensuring you gain real value, make informed decisions, and ultimately drive away with a financing deal that truly serves your best interests. Get ready to transform uncertainty into empowerment.

The Foundation: Deconstructing the Car Loan Landscape

Before we explore the nuances of applying for and managing vehicle financing, it’s essential to grasp the fundamental components of a car loan. Think of this as laying the groundwork for your financial house – without a strong foundation, everything else is precarious.

What Exactly is a Car Loan?

At its core, a car loan is a sum of money borrowed from a financial institution (like a bank, credit union, or even the car manufacturer’s financing arm) specifically for the purpose of purchasing a vehicle. In exchange for this sum, you agree to repay the borrowed amount, known as the principal, along with an additional charge called interest, over a predetermined period, or term. This repayment is typically made in fixed monthly installments.

Most car loans are what we call "secured loans." This means the vehicle you’re purchasing acts as collateral for the loan. If you fail to make your payments as agreed, the lender has the legal right to repossess the car to recover their losses. This distinction is crucial because it often allows lenders to offer more favorable interest rates compared to unsecured loans, as their risk is mitigated by the asset.

Key Components You Must Understand

Every car loan, regardless of the lender, will involve three primary elements that dictate your overall cost and monthly payments:

- Principal: This is the actual amount of money you borrow to buy the car. It’s the sticker price of the vehicle, minus any down payment or trade-in value. Understanding your principal helps you gauge the true cost of the car itself.

- Interest Rate: This is the cost of borrowing money, expressed as a percentage of the principal. It’s the lender’s profit for extending you credit. A lower interest rate means you’ll pay less over the life of the loan, saving you potentially thousands of dollars.

- Loan Term: This refers to the length of time, typically in months (e.g., 36, 48, 60, 72, or even 84 months), over which you agree to repay the loan. A shorter term usually means higher monthly payments but less interest paid overall, while a longer term offers lower monthly payments but accrues more interest over time.

Pro Tip from Us: Don’t just focus on the monthly payment. While it’s important for budgeting, truly understanding the principal, interest rate, and loan term will give you a complete picture of the total cost of ownership. Many people make the mistake of extending loan terms to lower monthly payments without realizing the significant increase in total interest paid. Always calculate the total cost over the loan’s lifetime.

Navigating the Car Loan Landscape: What to Expect from Reputable Lenders

When seeking a car loan, you’re essentially looking for a financial partner. Just as you’d expect reliability and clear terms from a robust financial institution, understanding what to look for in a lender is paramount. This section will guide you through the process of identifying a trustworthy source for your vehicle financing, embodying the principles of clarity and excellent service you’d associate with a name like Lincoln Financial.

What to Look For in a Lender: The Pillars of Trust

Not all lenders are created equal. When aspiring for the caliber of service and reliability implied by "Lincoln Financial Car Loans," you should meticulously evaluate potential financial institutions based on several key criteria:

- Reputation and Trustworthiness: Research reviews and ratings. Does the lender have a history of transparent dealings and positive customer experiences? A solid reputation is often a strong indicator of fair practices.

- Competitive Interest Rates: Compare offers from multiple lenders. Even a fraction of a percentage point difference can save you a substantial amount over the loan term. Don’t assume the first offer is the best.

- Flexible Loan Terms: Look for a range of loan term options that can be tailored to your financial situation. A good lender won’t push you into a term that doesn’t fit your budget.

- Exceptional Customer Service: How easy is it to get in touch with them? Are their representatives knowledgeable and helpful? Good customer service can make a significant difference, especially if you encounter any issues during the loan’s life.

- Transparency: All fees, charges, and conditions should be clearly disclosed upfront. There should be no hidden clauses or surprises.

Types of Car Loans: Tailoring to Your Needs

Reputable lenders typically offer various types of car loans to suit different purchasing scenarios:

- New Car Loans: These are for brand-new vehicles straight from the dealership. They often come with the lowest interest rates due to the car’s high value and lower depreciation risk for the lender.

- Used Car Loans: For pre-owned vehicles, these loans can have slightly higher interest rates than new car loans, reflecting the higher risk associated with an older vehicle’s potential mechanical issues and depreciation.

- Refinancing Car Loans: If you already have a car loan but your credit score has improved, or interest rates have dropped, you might consider refinancing. This involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms. This can significantly reduce your monthly payments or the total interest paid.

Based on My Experience: The biggest mistake consumers make is accepting the financing offered by the dealership without exploring external options. Dealerships often have partnerships that might not be the most competitive for your specific credit profile. Always secure pre-approvals from at least two independent financial institutions before you even start negotiating at the dealership. This empowers you with leverage.

The Power of Pre-Approval: Your Secret Weapon

Securing a car loan pre-approval before you visit a dealership is one of the smartest moves you can make. It transforms you from a casual shopper into a cash buyer in the eyes of the dealer.

- What is Pre-Approval? It’s a conditional commitment from a lender stating that they are willing to lend you a certain amount of money at a specific interest rate, subject to final verification and the vehicle meeting their criteria.

- Benefits:

- Know Your Budget: You’ll know exactly how much you can afford, preventing you from falling in love with a car outside your price range.

- Negotiating Power: With pre-approval in hand, you can negotiate the car’s price more effectively, as financing is already secured. You’re not relying on the dealer to find you a loan.

- Focus on the Car: You can concentrate solely on finding the right vehicle, rather than simultaneously worrying about financing.

- Benchmark for Dealer Offers: Your pre-approved rate gives you a baseline. If the dealership offers a higher rate, you know to push back or stick with your pre-approval.

The robust financial planning associated with Lincoln Financial Group extends to prudent car loan decisions, and pre-approval is a prime example of such foresight. It’s about taking control of your financial journey from the outset.

The Application Process: A Step-by-Step Guide to Approval

Once you’ve identified potential lenders and understand the different types of loans, the next phase is the application itself. This is where your financial profile comes into play, and preparation is key to a smooth and successful approval process. Just as Lincoln Financial aims for clarity in its services, your application should be a clear representation of your financial standing.

Required Documents: Get Organized Early

Lenders need to verify your identity, income, and financial stability. Having these documents ready can significantly expedite the application process. Common documents you’ll need include:

- Proof of Identity: Valid driver’s license, state ID, or passport.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, tax returns (if self-employed or for additional verification).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Credit History Information: While lenders will pull your credit report, it’s wise to have checked your own report beforehand.

- Social Security Number: For credit checks and identification.

- Trade-in Information (if applicable): Vehicle title, registration, and any outstanding loan details.

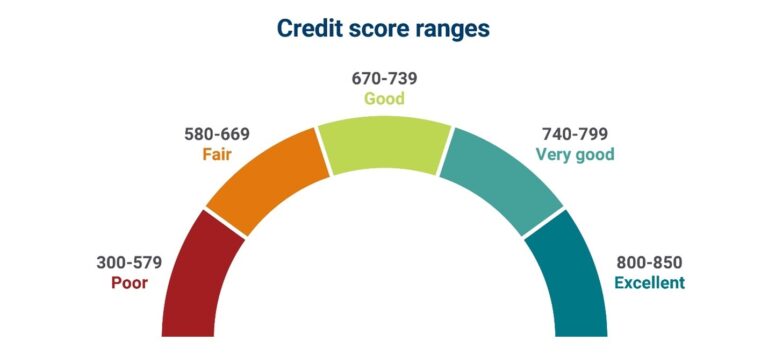

The Pivotal Role of Your Credit Score

Your credit score is arguably the most influential factor in securing a favorable car loan. It’s a three-digit number that summarizes your creditworthiness, telling lenders how likely you are to repay your debts.

- Good Credit Car Loans: If you have an excellent credit score (generally 700+), you’re considered a low-risk borrower. This will grant you access to the lowest interest rates, most flexible terms, and quicker approval times. Lenders are eager to approve good credit car loans.

- Bad Credit Car Loans: For those with a lower credit score (typically below 600-620), securing a car loan can be more challenging and expensive. Lenders view you as a higher risk, which translates to higher interest rates to compensate for that risk. While bad credit car loans are available, they often come with less favorable terms, such as higher interest, larger down payment requirements, or shorter loan terms.

Common Mistakes to Avoid:

- Not Checking Your Credit Report: Always review your credit report from all three major bureaus (Experian, Equifax, TransUnion) before applying. Dispute any errors, as they can negatively impact your score. (Internal Link Placeholder: For a deeper dive, read "Understanding Your Credit Score: A Comprehensive Guide" on our blog.)

- Applying to Too Many Lenders Simultaneously: Each hard inquiry on your credit report can slightly lower your score. While multiple inquiries for the same type of loan within a short window (typically 14-45 days) are often grouped as one, it’s still wise to be selective.

- Underestimating Your Debt-to-Income Ratio: Your DTI is the percentage of your gross monthly income that goes towards debt payments. Lenders look for a DTI below 43% (though lower is better for car loans) to ensure you have enough disposable income to comfortably afford your new car payment. A high DTI can signal overextension, even with good credit.

Pro Tips from Us: Boosting Your Chances

If your credit isn’t stellar, don’t despair. Here are ways to improve your credit score before applying for "Lincoln Financial Car Loans" or any robust auto financing:

- Pay Bills on Time: Payment history is the biggest factor in your credit score.

- Reduce Existing Debt: Especially revolving credit like credit cards. Lowering your credit utilization ratio (how much credit you’re using vs. what’s available) can significantly help.

- Avoid New Credit: Don’t open new credit accounts in the months leading up to your car loan application.

- Save for a Larger Down Payment: A substantial down payment reduces the amount you need to borrow, making you a less risky borrower.

The Actual Application and Approval Process

Once you submit your application and supporting documents, the lender will:

- Review Your Application: They’ll assess your income, employment history, and other financial details.

- Pull Your Credit Report: A hard inquiry will be made to evaluate your credit history and score.

- Calculate Your Debt-to-Income Ratio: To ensure affordability.

- Make a Decision: You’ll typically receive an answer within a few hours to a few business days. If approved, you’ll get a loan offer detailing the principal, interest rate, term, and monthly payment.

Careful preparation in this phase directly correlates with a higher chance of approval and more favorable terms, reflecting the meticulous planning associated with Lincoln Financial’s approach to client solutions.

Interest Rates, Loan Terms, and Payments: Decoding Your Financial Commitment

Once you’re approved for a car loan, the next critical step is to understand the precise details of your financial commitment. This involves scrutinizing interest rates, weighing the pros and cons of different loan terms, and accurately budgeting for your monthly payments. This is where the true cost of your "Lincoln Financial Car Loan"-level financing becomes clear.

Understanding Interest Rates: The Cost of Borrowing

The interest rate is perhaps the single most impactful factor on the total cost of your car loan. A lower rate means you pay less over time. Several elements influence the rate you’re offered:

- Your Credit Score: As discussed, this is paramount. Excellent credit unlocks the lowest rates.

- Current Market Rates: The overall economic environment and central bank interest rates can influence what lenders charge.

- Loan Term: Shorter loan terms often come with slightly lower interest rates because the lender’s risk exposure is reduced.

- Down Payment Amount: A larger down payment reduces the principal, thus lowering the lender’s risk and potentially earning you a better rate.

- Vehicle Type: New cars often qualify for lower rates than used cars due to their higher value and perceived reliability.

Lenders typically offer two types of interest rates:

- Fixed-Rate Loans: The interest rate remains the same for the entire life of the loan. This provides predictable monthly payments, making budgeting easier. Most car loans are fixed-rate.

- Variable-Rate Loans: The interest rate can fluctuate over the loan term, usually tied to a benchmark index. While they might start lower, your payments could increase if rates rise. Variable rates are less common for car loans due to their inherent uncertainty.

The Loan Term Dilemma: Shorter vs. Longer

Choosing the right loan term is a balancing act between affordability and total cost.

- Shorter Terms (e.g., 36 or 48 months):

- Pros: You pay significantly less interest over the life of the loan, build equity faster, and become debt-free sooner.

- Cons: Monthly payments will be higher, which might strain your budget.

- Longer Terms (e.g., 60, 72, or 84 months):

- Pros: Lower monthly payments make the car more affordable in the short term, freeing up cash flow.

- Cons: You pay substantially more interest over the loan’s life, risk becoming "upside down" (owing more than the car is worth) for longer, and the car will be older and potentially less reliable by the time it’s paid off.

Pro Tip from Us: While lower monthly payments from longer terms are tempting, always calculate the total interest paid for different terms. Sometimes, a slightly higher monthly payment for a shorter term can save you thousands. Use an online car loan calculator to compare scenarios.

The Power of a Down Payment

A down payment is the initial sum of money you pay upfront for the car, reducing the amount you need to borrow. Its impact is significant:

- Lower Principal: Less money borrowed means less interest accrues over time.

- Reduced Monthly Payments: With a smaller loan amount, your monthly installments will be lower.

- Better Interest Rates: Lenders see a down payment as a sign of your commitment and reduced risk, potentially offering you a better rate.

- Avoid Being "Upside Down": A substantial down payment helps ensure you have immediate equity in the vehicle, preventing you from owing more than the car is worth, especially during the rapid depreciation of new cars.

Budgeting for Monthly Payments and Beyond

Once you have your principal, interest rate, and term, you can accurately calculate your monthly car loan payment. However, your car-related expenses don’t stop there.

- Insurance Requirements: Lenders typically require full coverage (comprehensive and collision) insurance on financed vehicles to protect their collateral. This can be a significant monthly cost that must be factored into your budget.

- Maintenance and Repairs: Even new cars require routine maintenance. Older cars will inevitably need repairs. Set aside a monthly amount for these inevitable costs.

- Fuel Costs: Don’t forget the ongoing expense of gasoline or charging for EVs.

- Registration and Taxes: Annual fees and potential sales tax need to be considered.

(Internal Link Placeholder: For a holistic view of managing your finances, check out "Budgeting for Your Next Big Purchase: A Step-by-Step Approach" on our site.)

By meticulously planning for all these expenses, you ensure that your "Lincoln Financial Car Loan"-level financing remains manageable and contributes positively to your overall financial well-being.

Beyond the Approval: Managing Your Car Loan Responsibly

Securing a car loan is just the first leg of the journey; responsible management is what truly defines a positive financial outcome. A well-managed car loan, much like the prudent financial strategies advocated by Lincoln Financial, contributes positively to your credit health and overall stability.

Making Timely Payments: The Golden Rule

This might seem obvious, but consistently making your car loan payments on time is the single most important aspect of responsible borrowing. Late payments can lead to:

- Late Fees: Additional charges that add to your debt.

- Credit Score Damage: Late payments are heavily weighted in credit scoring models and can severely impact your score for years.

- Default and Repossession: Repeated late payments or non-payment can ultimately lead to the lender repossessing your vehicle.

Set up automatic payments if possible, or create calendar reminders to ensure you never miss a due date. This simple discipline will safeguard your financial health.

Understanding Prepayment Penalties (If Any)

While many car loans allow you to pay off your loan early without penalty, some lenders, particularly those dealing with bad credit car loans, might include a prepayment penalty clause. This is a fee charged if you pay off your loan before the agreed-upon term.

- Always read your loan agreement carefully to identify any such clauses.

- If a penalty exists, weigh the cost of the penalty against the interest you’d save by paying early. Often, the savings from reduced interest still outweigh the penalty, but it’s essential to calculate.

- Most reputable lenders, aiming for a "Lincoln Financial Car Loan" standard of transparency, will clearly disclose these terms.

Refinancing Options: When and Why to Consider Them

Life circumstances and market conditions can change, potentially offering you an opportunity to improve your existing car loan. Refinancing means taking out a new loan to pay off your current car loan, ideally at a better rate or with more favorable terms.

You might consider refinancing if:

- Your Credit Score Has Improved: A significantly higher score since you first took out the loan could qualify you for a much lower interest rate.

- Interest Rates Have Dropped: If overall market rates have declined, you might be able to secure a better deal.

- You Need Lower Monthly Payments: While not always advisable due to increased total interest, extending your loan term through refinancing can lower monthly payments if you’re experiencing financial hardship.

- You Want to Change Loan Terms: Perhaps you want to shorten the term to pay off the car faster, or remove a co-signer.

Based on My Experience: Many people overlook refinancing, thinking their original loan is set in stone. However, proactively reviewing your loan every 12-18 months, especially if your financial situation has improved, can lead to substantial savings over the life of the loan. It’s a key component of savvy financial planning.

The Importance of Ongoing Financial Planning

A car loan is a significant financial commitment, but it’s just one piece of your overall financial puzzle. Integrating your car loan management into a broader financial plan is crucial. This includes:

- Emergency Fund: Ensure you have savings to cover unexpected expenses or job loss, preventing you from defaulting on your car payments.

- Debt Management: Keep an eye on your overall debt-to-income ratio to avoid overextension.

- Savings Goals: Don’t let your car payment derail other important savings, such as retirement or a down payment for a home.

Responsible borrowing isn’t just about paying bills; it’s about making choices that strengthen your long-term financial health, a philosophy that resonates deeply with the comprehensive financial strategies of leading institutions.

Conclusion: Driving Towards Smart Financial Decisions

Navigating the world of car loans requires diligence, knowledge, and a strategic approach. From understanding the core components of a loan to meticulously preparing for the application process, and finally, managing your debt responsibly, every step plays a vital role in securing a vehicle financing solution that genuinely works for you.

We’ve explored how aspiring for the standards implied by "Lincoln Financial Car Loans" means seeking out transparency, competitive rates, and reliable service from your chosen lender. It’s about being an informed consumer who knows their credit score, understands the impact of interest rates and loan terms, and leverages tools like pre-approval to gain leverage.

Remember, the goal isn’t just to get a car; it’s to acquire a vehicle in a way that enhances, rather than burdens, your financial future. By applying the in-depth insights shared in this guide, you are well-equipped to make intelligent, informed decisions, ensuring your journey to car ownership is as smooth and financially sound as possible. Drive confidently, knowing you’ve made choices that reflect a truly robust approach to personal finance.

External Link: For more general guidance on understanding and comparing auto loans, visit the Consumer Financial Protection Bureau (CFPB) website: https://www.consumerfinance.gov/consumer-tools/auto-loans/