Unlocking Your Ride: A Comprehensive Guide to Your $33,000 Car Loan Payment

Unlocking Your Ride: A Comprehensive Guide to Your $33,000 Car Loan Payment Carloan.Guidemechanic.com

Buying a new or used car is an exciting milestone, but for many, the financial aspect can feel like navigating a complex maze. If you’re considering a vehicle that costs around $33,000, understanding your potential car loan payment is paramount. This isn’t just about the monthly number; it’s about grasping the underlying factors that shape your financial commitment and ensuring you make a smart, sustainable decision.

As an expert blogger and SEO content writer with years of experience in personal finance and automotive insights, I’ve seen firsthand how a lack of understanding can lead to costly mistakes. This article is designed to be your ultimate guide, transforming complex financial jargon into clear, actionable advice. We’ll delve deep into everything you need to know about a $33,000 car loan payment, from calculation to smart strategies, ensuring you drive away with confidence, not buyer’s remorse.

Unlocking Your Ride: A Comprehensive Guide to Your $33,000 Car Loan Payment

The Big Question: What Influences Your $33,000 Car Loan Payment?

Your monthly car loan payment isn’t a fixed number; it’s a dynamic figure influenced by several critical factors. Understanding each of these components is the first step toward accurately estimating and ultimately managing your auto financing. Let’s break down the key players that dictate how much you’ll pay each month for that $33,000 vehicle.

Interest Rate (APR): The Silent Cost Driver

The interest rate, often expressed as Annual Percentage Rate (APR), is arguably the most significant factor affecting your car loan payment. This is the cost of borrowing money from a lender, and it’s added to your principal loan amount. A higher interest rate means you pay more for the privilege of borrowing, directly increasing your monthly installments and the total cost of the loan over its lifetime.

Several elements converge to determine the interest rate you’ll be offered. Your credit score is paramount; a higher score signals less risk to lenders, often resulting in lower APRs. Market conditions, the specific lender you choose, and even the loan term can also play a role in shaping this crucial percentage.

Based on my experience, even a small difference in APR can translate into hundreds, if not thousands, of dollars saved over the life of your loan. For instance, on a $33,000 loan, moving from a 7% to a 5% APR could save you a substantial amount, making diligent rate shopping absolutely essential. Never settle for the first offer you receive.

Loan Term (Duration): The Time-Payment Trade-off

The loan term refers to the length of time you have to repay your loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This factor presents a direct trade-off: a longer loan term generally leads to lower monthly payments, but you’ll pay more in total interest over time. Conversely, a shorter term means higher monthly payments but less overall interest paid.

For a $33,000 car loan, extending the term from 60 to 72 months might reduce your monthly burden by a noticeable amount. However, this convenience comes at a cost. You’ll be paying interest for an additional year, increasing the total amount you repay significantly.

Common mistakes to avoid are automatically opting for the longest possible term just to achieve the lowest monthly payment. While it might seem appealing in the short term, this strategy can lead to you paying much more for the vehicle than its original price and potentially being "upside down" on your loan (owing more than the car is worth) for a longer period. Always balance affordability with the total cost.

Down Payment: Your Initial Investment

A down payment is the amount of cash you pay upfront toward the purchase price of the vehicle. This immediate contribution directly reduces the principal amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll accrue. It’s one of the most effective ways to influence your loan terms positively.

For a $33,000 car, a significant down payment of, say, $5,000, means you’re only financing $28,000. This smaller loan amount naturally results in lower monthly payments and less interest paid over the life of the loan. It also helps you build equity in the vehicle faster, reducing the risk of being upside down on your loan.

Pro tips from us: Aim for at least a 10-20% down payment on a new car, if feasible. For used cars, a larger down payment is often even more beneficial, as used vehicles typically depreciate faster. A substantial down payment also signals financial stability to lenders, potentially leading to better interest rate offers.

Credit Score: Your Financial Report Card

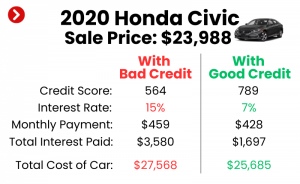

Your credit score is a numerical representation of your creditworthiness, based on your borrowing and repayment history. Lenders use this score to assess the risk of lending money to you. A higher credit score (typically 700+) indicates a responsible borrower, making you eligible for the most competitive interest rates. Conversely, a lower score (below 600) suggests a higher risk, often resulting in higher interest rates or even loan denial.

When applying for a $33,000 car loan, your credit score will directly impact the APR you’re offered. Excellent credit can secure rates as low as 3-5%, while fair or poor credit might see rates climbing into the double digits. This difference dramatically alters your monthly payment and the overall cost of your loan.

It’s crucial to check your credit score and report before you start car shopping. This allows you to identify any errors and understand where you stand. If your score isn’t where you want it to be, taking steps to improve it can save you thousands. offers practical advice on boosting your credit profile.

Other Fees and Taxes: Hidden Additions to Your Loan

Beyond the sticker price of the car, several additional costs can be rolled into your loan, increasing the total amount financed. These typically include sales tax, registration fees, documentation fees, and sometimes even extended warranties or GAP insurance. While not directly part of the car’s initial price, they can inflate your loan principal.

Sales tax varies by state and can be a significant addition. For example, a 7% sales tax on a $33,000 car adds $2,310 to the cost. Registration and title fees, while smaller, are mandatory. Documentation fees cover the paperwork involved in the sale. All these charges, if not paid out of pocket, get added to your loan amount, impacting your monthly payment.

Understanding these additional costs is vital for an accurate payment estimate. Always ask the dealership for a detailed breakdown of all fees before signing any agreement. Being aware of what’s included in your total financed amount prevents unwelcome surprises down the line.

Calculating Your $33,000 Car Loan Payment: A Step-by-Step Guide

Estimating your monthly car payment might seem daunting, but with the right tools and understanding, it’s straightforward. The goal is to get a realistic picture of what your financial commitment will look like before you commit to a $33,000 vehicle.

Understanding Loan Calculators: Your Best Friend in Auto Financing

Online car loan calculators are indispensable tools for prospective car buyers. They allow you to input the principal loan amount, interest rate, and loan term to instantly generate an estimated monthly payment. These calculators provide a quick and easy way to experiment with different scenarios.

While most calculators provide a solid estimate, remember they are based on the information you provide. They don’t account for every specific fee or tax unless you manually add them to the principal. Always use reputable calculators from financial institutions or well-known financial advice websites. For an accurate estimate, you can use a tool like NerdWallet’s Auto Loan Calculator.

Example Scenario: Putting Numbers to the Test

Let’s walk through a concrete example to illustrate how these factors come together to determine your $33,000 car loan payment.

Scenario A: Good Credit, Moderate Term, Some Down Payment

- Vehicle Price: $33,000

- Down Payment: $3,000

- Amount Financed (Principal): $30,000 (after down payment, assuming no other fees rolled in for simplicity)

- Interest Rate (APR): 5.0% (for a borrower with good credit)

- Loan Term: 60 months (5 years)

Using a standard loan payment formula or an online calculator, your estimated monthly payment for this scenario would be approximately $566.00. Over the 60 months, you would pay a total of $33,960, meaning $3,960 in interest.

Scenario B: Excellent Credit, Shorter Term, Larger Down Payment

- Vehicle Price: $33,000

- Down Payment: $6,000

- Amount Financed (Principal): $27,000

- Interest Rate (APR): 3.5% (for a borrower with excellent credit)

- Loan Term: 48 months (4 years)

In this scenario, your estimated monthly payment would be approximately $604.00. While the monthly payment is higher, the total paid over 48 months is $29,000, with only $2,000 in interest. This demonstrates the power of a larger down payment and a shorter term.

Scenario C: Average Credit, Longer Term, No Down Payment

- Vehicle Price: $33,000

- Down Payment: $0

- Amount Financed (Principal): $33,000

- Interest Rate (APR): 9.0% (for a borrower with average credit)

- Loan Term: 72 months (6 years)

Here, your estimated monthly payment would be around $588.00. However, the total amount paid over 72 months would be $42,336, resulting in a staggering $9,336 in interest. This clearly illustrates how higher interest rates and longer terms significantly increase your total cost, even if the monthly payment seems manageable.

These examples highlight how crucial it is to manipulate these variables to find a payment that fits your budget without incurring excessive interest. Even minor adjustments can have a substantial impact on your long-term financial health.

Strategies to Lower Your $33,000 Car Loan Payment (and Total Cost)

Understanding the factors that influence your car loan is just the beginning. The next step is to proactively implement strategies that can reduce your monthly payment and, more importantly, the overall cost of your $33,000 car loan. These tips are based on years of observing successful financing practices.

Boost Your Credit Score Before Applying

As we’ve discussed, your credit score is a major determinant of your interest rate. Taking steps to improve it even a few months before applying can yield significant savings. Pay down existing debts, especially high-interest credit card balances, and ensure all your bills are paid on time.

Avoid opening new credit accounts or making large purchases that require credit during the pre-car-buying period. Each point you add to your credit score could translate into a lower APR, directly reducing both your monthly payment and the total interest you’ll pay on your $33,000 loan.

Increase Your Down Payment

This is one of the most straightforward and effective ways to reduce your loan principal and, consequently, your monthly payment. Every dollar you put down is a dollar you don’t have to borrow and pay interest on. If you can save an extra $1,000, that could shave a noticeable amount off your monthly payment and total interest.

Consider trading in your current vehicle. The value of your trade-in acts as a down payment, directly reducing the amount you need to finance. Be sure to research your car’s trade-in value beforehand to negotiate effectively.

Shop Around for Lenders (Get Pre-Approved!)

Never assume the dealership offers the best financing. Banks, credit unions, and online lenders often have more competitive rates. It’s highly advisable to get pre-approved for a loan from a few different financial institutions before you even set foot in a dealership.

Pre-approval gives you a clear understanding of the interest rate you qualify for, empowering you to negotiate with the dealership from a position of strength. If the dealer can’t beat your pre-approved rate, you can confidently go with your outside financing. This competitive shopping can save you hundreds, if not thousands, on your $33,000 car loan.

Consider a Shorter Loan Term (If Affordable)

While a longer loan term offers lower monthly payments, it costs you more in total interest. If your budget allows, opting for a shorter term (e.g., 48 or 60 months instead of 72 or 84) can significantly reduce the total amount you pay for the car.

Carefully evaluate your monthly budget to see if you can comfortably afford the higher payments associated with a shorter term. The financial discipline required for a quicker payoff often translates to substantial long-term savings. It’s a trade-off worth considering seriously.

Negotiate the Car Price

The most direct way to reduce your loan payment is to reduce the amount you need to borrow in the first place. Don’t be afraid to negotiate the selling price of the $33,000 vehicle. Research market values, be prepared to walk away, and aim for a fair deal.

Every dollar you shave off the purchase price is a dollar less you finance. A $1,000 discount on the car means $1,000 less principal, which directly translates to lower monthly payments and less interest over the entire loan term. Negotiation is a skill that can truly pay off.

Refinancing Your Car Loan

If you’ve already secured a $33,000 car loan but your credit score has improved, or interest rates have dropped since your initial purchase, refinancing could be an excellent option. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms.

This strategy can significantly reduce your monthly payment and/or the total interest paid. However, evaluate the costs associated with refinancing (e.g., application fees) to ensure the savings outweigh these expenses. It’s a powerful tool for those whose financial situation has improved post-purchase.

Common Mistakes to Avoid When Financing a $33,000 Car

Based on years of advising car buyers, I’ve observed several recurring pitfalls that can turn the dream of a new car into a financial nightmare. Avoiding these common mistakes is as important as implementing smart strategies.

- Focusing Only on the Monthly Payment: This is perhaps the biggest mistake. While a low monthly payment is appealing, it often comes at the cost of a longer loan term and significantly more total interest paid. Always consider the total cost of the loan, not just the monthly figure.

- Not Getting Pre-Approved: Walking into a dealership without a pre-approval from your bank or credit union puts you at a disadvantage. You lose your negotiating power and are more susceptible to accepting the dealer’s potentially higher interest rate.

- Ignoring the Total Cost of the Loan: Many buyers only look at the monthly payment multiplied by the number of months. This ignores the substantial amount of interest you’ll pay. Always ask for the total amount you’ll repay over the loan’s life.

- Extending the Loan Term Unnecessarily: While a longer term lowers monthly payments, it increases the total interest and the risk of being upside down on your loan. Only extend the term if absolutely necessary for budget reasons, and understand the financial implications.

- Not Understanding All Fees: Don’t just skim the paperwork. Read every line item to understand all the fees, taxes, and additional products (like extended warranties or GAP insurance) included in your loan. Question anything you don’t understand or didn’t agree to.

- Buying More Car Than You Can Afford: Just because a lender approves you for a $33,000 car doesn’t mean you should buy it. Factor in all ownership costs (insurance, fuel, maintenance) and adhere to a realistic budget.

- Rolling Negative Equity into a New Loan: If you owe more on your trade-in than it’s worth (negative equity), rolling that amount into a new $33,000 loan immediately puts you further underwater. It’s almost always better to pay off the negative equity separately if possible.

The Long-Term Impact of Your $33,000 Car Loan

A car loan is a significant financial commitment that extends far beyond the dealership lot. Understanding its long-term implications is crucial for responsible financial planning.

Impact on Your Budget and Financial Flexibility

Your monthly car payment will become a fixed expense for several years. This reduces your discretionary income and can impact your ability to save for other goals, pay down other debts, or handle unexpected expenses. Ensure your $33,000 car loan payment leaves enough room in your budget for other necessities and emergencies.

A high car payment can also limit your financial flexibility, potentially delaying other major life purchases like a home or furthering your education. It’s an opportunity cost that needs to be factored into your decision-making process.

Resale Value and Depreciation: The Upside-Down Trap

Cars begin to depreciate the moment they are driven off the lot. For a $33,000 car, this depreciation can be substantial in the first few years. If your loan balance depreciates slower than the car’s value, you could find yourself "upside down" or "underwater" on your loan, meaning you owe more than the car is worth.

This becomes problematic if you need to sell the car or if it’s totaled in an accident. In such cases, your insurance payout might not cover the full loan balance. This is where GAP (Guaranteed Asset Protection) insurance can be beneficial, covering the difference between your car’s value and your loan balance.

Building Credit History

On the positive side, a car loan, when managed responsibly, can be an excellent way to build a strong credit history. Consistent, on-time payments demonstrate reliability to credit bureaus, positively impacting your credit score. This can open doors to better rates on future loans and credit products.

Conversely, missed or late payments on your $33,000 car loan can severely damage your credit score, making it harder and more expensive to borrow money in the future. Treat your car loan as a serious financial obligation that directly impacts your credit health.

Is a $33,000 Car Loan Right for You? Assessing Affordability

Before you commit to a $33,000 car, it’s essential to realistically assess whether it fits comfortably within your overall financial picture. Affordability isn’t just about the monthly payment; it’s about the holistic cost of ownership.

The 20/4/10 Rule: A Good Guideline

A popular guideline for car affordability is the 20/4/10 rule:

- 20% Down Payment: Aim for at least 20% of the car’s purchase price ($6,600 on a $33,000 car).

- 4-Year Loan Term: Keep your loan term to four years (48 months) or less to minimize interest paid and avoid being upside down.

- 10% of Gross Income: Your total monthly car expenses (loan payment, insurance, fuel, maintenance) should not exceed 10% of your gross (pre-tax) monthly income.

While this rule is a guideline, it provides a solid framework for responsible car buying. If a $33,000 car doesn’t fit within these parameters, it might be an indication to reconsider your budget or look for a less expensive vehicle.

Budgeting for More Than Just Payments

Remember that your car loan payment is only one part of the total cost of car ownership. You must also budget for:

- Car Insurance: This can be a significant monthly expense, varying based on your age, driving record, location, and the vehicle itself.

- Fuel Costs: Estimate your average monthly fuel consumption based on your driving habits and current gas prices.

- Maintenance and Repairs: Cars require regular maintenance (oil changes, tire rotations) and can incur unexpected repair costs. Setting aside a small amount each month for this is wise.

- Registration and Licensing Fees: Annual fees are required to keep your car legally on the road.

Ignoring these additional costs can quickly turn an "affordable" $33,000 car loan into a financial strain. For a detailed breakdown, explore .

Conclusion: Drive Away with Confidence

Understanding your potential payment on a $33,000 car loan is more than just crunching numbers; it’s about making an informed financial decision that aligns with your overall budget and long-term goals. By grasping the impact of interest rates, loan terms, down payments, and your credit score, you empower yourself to negotiate better deals and avoid common pitfalls.

Remember, a lower monthly payment isn’t always the best deal if it means paying significantly more in total interest. Prioritize getting pre-approved, shopping around for the best rates, and making a substantial down payment. By taking these proactive steps, you can ensure your $33,000 car loan is a manageable and positive addition to your financial life.

Start planning your car purchase wisely today, and drive away not just in a new car, but with the peace of mind that comes from smart financial choices.