Unlocking Your Ride: A Deep Dive into Credit One Car Loans for Smart Auto Financing

Unlocking Your Ride: A Deep Dive into Credit One Car Loans for Smart Auto Financing Carloan.Guidemechanic.com

The dream of owning a car is a powerful one, representing freedom, convenience, and a significant step forward for many. However, securing the right auto financing can often feel like navigating a complex maze, especially if your credit history isn’t picture-perfect. Many individuals find themselves searching for lenders who understand their unique financial situations, and in this journey, Credit One Bank frequently emerges as a potential option.

This comprehensive guide is designed to cut through the confusion, offering an in-depth look at Credit One car loans. We’ll explore who they’re for, how they work, the application process, and what you need to know to make an informed decision. Our goal is to equip you with the knowledge to approach your auto financing journey with confidence, ensuring you understand every facet of Credit One’s offerings.

Unlocking Your Ride: A Deep Dive into Credit One Car Loans for Smart Auto Financing

What Exactly is a Credit One Car Loan?

Credit One Bank is primarily known for its credit card offerings, often catering to individuals who are rebuilding their credit or have limited credit histories. However, their lending portfolio extends beyond credit cards to include auto loans, providing another pathway for consumers to access necessary financing. A Credit One car loan is essentially a secured loan specifically designed to help you purchase a vehicle, with the car itself serving as collateral.

Unlike prime lenders who typically target borrowers with excellent credit scores, Credit One often positions itself to assist a broader spectrum of credit profiles. This means they may be more accessible to those with fair, poor, or even no credit history, offering an opportunity to finance a vehicle when other traditional lenders might decline. Understanding this core distinction is vital when evaluating if Credit One aligns with your financial needs.

Who Should Consider a Credit One Car Loan?

Based on my experience in the auto financing landscape, Credit One car loans are primarily geared towards a specific demographic. They are often a viable option for individuals who:

- Have Fair to Poor Credit: If your FICO score falls below the "good" range (typically below 670), or if you’re actively working to rebuild your credit after past financial difficulties, Credit One may be more willing to consider your application than a conventional bank.

- Are First-Time Car Buyers with Limited Credit History: Building credit from scratch can be challenging. A Credit One auto loan can serve as a stepping stone, helping you establish a positive payment history.

- Have Been Denied by Traditional Lenders: For those who have explored other financing avenues without success, Credit One offers an alternative solution, broadening the possibilities for vehicle ownership.

It’s important to recognize that while Credit One provides accessibility, it’s crucial to weigh this against the potential terms and conditions, which we will delve into further.

The Advantages and Disadvantages: A Balanced View

Every financial product comes with its own set of pros and cons, and Credit One car loans are no exception. A balanced perspective is essential to determine if this is the right path for your auto financing needs.

Potential Benefits of Credit One Auto Financing

One of the most significant advantages of Credit One auto financing is its accessibility. They often have more flexible underwriting criteria compared to prime lenders, making car ownership a reality for many who might otherwise be excluded. This inclusivity is a cornerstone of their offering.

Furthermore, securing and responsibly managing a Credit One car loan can be a powerful tool for credit rebuilding. Making consistent, on-time payments on a secured installment loan like a car loan demonstrates financial reliability. Pro tips from us: Each timely payment reported to the credit bureaus contributes positively to your payment history, which is the largest factor in your credit score calculation. Over time, this can significantly improve your credit standing, opening doors to better financial products in the future.

Another benefit often cited is the streamlined application process. While detailed, Credit One aims to make the journey as straightforward as possible, recognizing that borrowers may already face hurdles.

Drawbacks and Considerations

While accessible, Credit One car loans often come with higher interest rates. This is a common characteristic of lending to individuals with lower credit scores, as lenders perceive a greater risk. A higher interest rate translates directly to a greater total cost of the loan over its lifetime.

Another consideration is the potential for additional fees. These can include origination fees, administrative fees, or even prepayment penalties, depending on the specific loan agreement. Common mistakes to avoid are focusing solely on the monthly payment without fully understanding the total cost of the loan, including all associated fees. Always ask for a complete breakdown of all charges.

Lastly, depending on your credit profile and the lender’s current offerings, there might be limited vehicle options. Some lenders for subprime borrowers may have restrictions on the age, mileage, or type of vehicle they are willing to finance.

Understanding Eligibility: What Credit One Looks For

To be approved for a Credit One car loan, you’ll need to meet specific eligibility criteria. While these can be more flexible than prime lenders, they are still critical for approval.

Credit Score Requirements

Credit One doesn’t typically publish a strict minimum credit score, unlike some prime lenders. Instead, they operate on a broader spectrum. If your credit score is in the fair (580-669) or even poor (300-579) range, you still have a chance. However, it’s important to understand that a lower credit score will almost certainly result in a higher interest rate and potentially less favorable terms.

Based on my experience, lenders like Credit One perform a comprehensive review of your credit report, looking beyond just the score. They assess your payment history, current debts, and any past delinquencies to get a full picture of your financial behavior. For a deeper understanding of how your credit score impacts lending decisions, you might find our article on "Understanding Your Credit Score: A Comprehensive Guide" helpful.

Income and Employment Stability

Demonstrating a stable and sufficient income is paramount. Lenders want assurance that you can consistently make your monthly loan payments. This usually means having a steady job for a certain period (e.g., 6 months to 1 year) and meeting a minimum income threshold.

Your debt-to-income (DTI) ratio is also a significant factor. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new debt. Lenders prefer a DTI ratio that shows you aren’t overextended financially. If you’re looking for ways to improve this aspect of your financial profile, consider reviewing our article "Tips for Improving Your Debt-to-Income Ratio for Better Loan Prospects."

Down Payment Considerations

While it’s sometimes possible to secure a car loan with no money down, making a down payment can significantly improve your chances of approval and lead to better loan terms. A down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. It can also help you avoid being "upside down" on your loan (owing more than the car is worth) early in the loan term.

Lenders also consider the loan-to-value (LTV) ratio, which compares the loan amount to the vehicle’s market value. A lower LTV (meaning you’ve put more money down) is generally more appealing to lenders.

Other Factors

Beyond credit and income, Credit One will also consider other factors such as your age (must be 18 or older), residency status, and the type of vehicle you intend to purchase. Some lenders have restrictions on the age or mileage of the car they will finance, especially for subprime loans. Based on my experience, honesty and transparency throughout the application process are crucial; any discrepancies can lead to delays or denial.

The Credit One Car Loan Application Process: Step-by-Step

Applying for a Credit One car loan typically involves a straightforward process, often initiated online or through a dealership partnered with Credit One. Here’s a general overview of what you can expect:

- Online Pre-qualification (Optional but Recommended): Many lenders, including Credit One, offer a pre-qualification option. This usually involves a soft credit pull, which doesn’t impact your credit score, and gives you an idea of your potential eligibility and estimated terms. It’s a great way to gauge your options without commitment.

- Full Application Submission: If pre-qualified or ready to proceed, you’ll complete a more detailed application. This requires comprehensive personal, financial, and employment information.

- Required Documents: Be prepared to provide documentation such as:

- Proof of identity (Driver’s License, State ID)

- Proof of residency (Utility bill, lease agreement)

- Proof of income (Pay stubs, bank statements, tax returns)

- Employment verification (Employer contact information)

- Vehicle information (if you’ve already chosen a car)

- Credit Review and Underwriting: Credit One will conduct a hard credit inquiry, which may temporarily ding your credit score by a few points. Their underwriting team will then review all submitted information to assess your creditworthiness and determine loan terms.

- Offer and Review: If approved, you’ll receive a loan offer detailing the interest rate, loan term, monthly payment, and any associated fees. This is your opportunity to meticulously review every aspect of the agreement.

- Finalization and Funding: Once you accept the terms, you’ll sign the loan documents, and the funds will be disbursed, typically directly to the dealership.

Pro tips from us: Gather all necessary documents before you start the application. This proactive step can significantly speed up the process and prevent unnecessary delays.

Decoding Your Loan Terms: Interest Rates, APR, and Fees

Understanding the terminology in your loan agreement is paramount. Don’t just look at the monthly payment; delve into the details that truly define the cost of your Credit One car loan.

Interest Rates Explained

The interest rate is the percentage charged by the lender for borrowing money. It’s expressed as an annual percentage of the loan amount. For car loans, interest rates can be fixed (stay the same throughout the loan) or variable (fluctuate with market conditions). Most auto loans are fixed.

How your interest rate is determined depends heavily on your credit score, credit history, the loan term, the down payment, and the vehicle itself. Borrowers with lower credit scores will almost always face higher interest rates because they are perceived as a greater risk.

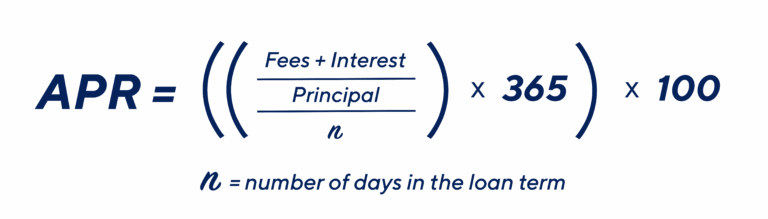

Annual Percentage Rate (APR)

The Annual Percentage Rate (APR) is a more comprehensive measure of the cost of borrowing money than the interest rate alone. It includes not only the interest rate but also most of the fees associated with the loan, expressed as a single annual percentage.

For example, if a loan has an interest rate of 8% but also includes a $500 origination fee, the APR will be higher than 8% to reflect that additional cost. The APR provides a more accurate picture of the total cost of your Credit One car loan. Always compare APRs when shopping for loans, not just interest rates, to get an apples-to-apples comparison. For more on understanding APR, the Consumer Financial Protection Bureau (CFPB) offers excellent resources on their website.

Potential Fees

Beyond interest, be aware of various fees that could be part of your loan agreement. These might include:

- Origination Fees: A charge for processing the loan.

- Documentation Fees: Costs associated with preparing loan documents.

- Late Payment Fees: Penalties for missing a payment deadline.

- Prepayment Penalties: Some loans might charge a fee if you pay off the loan early. This is less common with auto loans but always worth checking.

Common mistakes to avoid are signing loan documents without thoroughly reading and understanding every single fee listed. Don’t hesitate to ask for clarification on any charge you don’t understand.

Loan Duration and Monthly Payments

The loan duration, or term, is the length of time you have to repay the loan. Common terms for car loans range from 36 to 72 months, and sometimes even longer. A longer loan term typically results in lower monthly payments, which can seem appealing.

However, a longer term also means you’ll pay more in total interest over the life of the loan. Conversely, a shorter term will have higher monthly payments but will save you money on interest in the long run. It’s a balance between affordability and total cost.

Maximizing Your Chances: Pro Tips for Approval and Better Terms

Securing a Credit One car loan, especially with favorable terms, often comes down to preparation and strategy. Here are some pro tips from us to boost your approval odds and potentially lower your costs:

- Improve Your Credit Score First: Even a slight improvement in your credit score can significantly impact your interest rate. Pay down existing debts, dispute errors on your credit report, and make all payments on time for a few months before applying.

- Save for a Larger Down Payment: As discussed, a substantial down payment reduces the loan amount and the lender’s risk, making you a more attractive borrower. Aim for at least 10-20% of the vehicle’s purchase price.

- Consider a Co-signer: If your credit is particularly challenged, a co-signer with good credit can significantly strengthen your application. Their creditworthiness acts as a guarantee, often leading to approval or better terms. Ensure both parties understand the responsibilities involved.

- Shop Around for Rates: Don’t limit yourself to the first offer you receive. Apply with a few different lenders within a short timeframe (usually 14-45 days, depending on the credit scoring model) so that multiple hard inquiries count as one for credit scoring purposes. This allows you to compare offers and choose the best one.

- Know Your Budget: Before you even start shopping for a car or a loan, determine how much you can realistically afford for a monthly car payment, insurance, fuel, and maintenance. This prevents you from overextending yourself.

Based on my experience, thorough research and proactive steps before applying are the most effective ways to navigate the auto loan market, regardless of your credit score.

Managing Your Credit One Car Loan Responsibly

Once you’ve secured your Credit One car loan, responsible management is key to protecting your financial health and continuing to build positive credit.

- Make On-Time Payments: This is the most critical aspect. Set up automatic payments or calendar reminders to ensure you never miss a due date. Every on-time payment helps improve your credit score and avoids late fees.

- Monitor Your Account: Regularly check your Credit One loan account online or via their app. This allows you to track your payment history, see your remaining balance, and catch any potential discrepancies early.

- Communicate if You Face Difficulties: If you anticipate trouble making a payment, contact Credit One before you miss it. They may offer options like payment deferrals or adjusted plans, though these are not guaranteed and depend on your situation and their policies. Ignoring the problem will only worsen it.

- Benefits of Early Payoff (if applicable): If your loan doesn’t have prepayment penalties and you find yourself with extra funds, paying off your loan early can save you a significant amount in interest. Always confirm with your lender if there are any associated fees for early payoff.

Exploring Alternatives to Credit One Car Loans

While Credit One can be a viable option, it’s always wise to explore alternatives to ensure you’re getting the best possible deal for your situation. Pro tip: Never limit yourself to just one lender without comparing.

- Credit Unions: Often offer competitive interest rates and more flexible terms than traditional banks, particularly for members. They are member-focused and may be more willing to work with individuals with challenging credit.

- Local Banks: Even if you have fair credit, your local bank or a bank where you already have an account might be willing to offer you a loan, especially if you have a long-standing relationship.

- Dealership Financing (Other Lenders): Many dealerships work with a network of lenders, including both prime and subprime options. They can sometimes secure rates you might not find on your own, but always compare their offers with independent financing.

- Other Online Auto Lenders: There are numerous online platforms specializing in auto loans for various credit types. Companies like Capital One Auto Finance, Carvana, or specialized subprime lenders might offer different terms.

- Secured Personal Loans: In some cases, if you have other assets, a secured personal loan might be an option, but this involves putting up collateral other than the car itself.

Common Pitfalls and How to Avoid Them

Navigating the auto loan process can be tricky, and several common mistakes can cost you time and money.

- Not Budgeting Properly: Many people focus solely on the monthly payment without considering the total cost of the car (purchase price, interest, fees, insurance, maintenance). Common mistake: Falling in love with a car before knowing if you can truly afford it.

- Ignoring the APR: As discussed, the APR gives you the full cost. Don’t be swayed by a seemingly low interest rate if hidden fees inflate the true cost.

- Applying for Too Many Loans at Once (Indiscriminately): While shopping around is good, submitting applications to dozens of lenders within a short period can negatively impact your credit score. Stick to a few well-researched options.

- Not Understanding the Vehicle’s True Value: Research the market value of the car you’re interested in using resources like Kelley Blue Book (KBB) or Edmunds. This ensures you’re not paying more than the car is worth and helps prevent getting upside down on your loan.

- Overlooking the Importance of a Down Payment: While not always mandatory, skipping a down payment can lead to higher interest rates, larger monthly payments, and a greater risk of negative equity.

Conclusion: Empowering Your Auto Financing Journey

Securing a car loan, especially when navigating credit challenges, requires diligence, understanding, and a strategic approach. Credit One car loans can certainly offer a viable pathway to vehicle ownership for many individuals, particularly those looking to rebuild their credit or facing initial credit hurdles.

By thoroughly understanding their offerings, eligibility requirements, and the nuances of loan terms like APR, you empower yourself to make informed decisions. Remember to compare all your options, read every line of the loan agreement, and prioritize responsible financial management once your loan is approved. Your journey to owning a car should be one of confidence, not confusion. Start your research today, and drive away with the knowledge that you’ve made the best choice for your financial future.