Unlocking Your Ride: A Deep Dive into Payments for a $10,000 Car Loan

Unlocking Your Ride: A Deep Dive into Payments for a $10,000 Car Loan Carloan.Guidemechanic.com

Securing a new set of wheels is an exciting prospect, and for many, a $10,000 car loan represents a practical and accessible entry point into vehicle ownership. While this amount might seem straightforward, understanding the intricacies of your monthly payments is crucial for a smooth financial journey. This isn’t just about a number; it’s about making an informed decision that aligns with your budget and long-term financial health.

As an expert blogger and professional SEO content writer, my mission is to demystify the process of determining your payment for a $10,000 car loan. We’ll explore every variable, provide actionable strategies, and equip you with the knowledge to navigate the financing landscape with confidence. This comprehensive guide will serve as your ultimate resource, ensuring you make the smartest choices for your automotive investment.

Unlocking Your Ride: A Deep Dive into Payments for a $10,000 Car Loan

Understanding the Core Elements: What Shapes Your $10,000 Car Loan Payment?

Calculating your exact monthly payment isn’t a one-size-fits-all equation. Several critical factors work in tandem to determine how much you’ll owe each month. Grasping these elements is the first step toward smart car financing. Based on my experience, neglecting any of these can lead to unexpected financial strain down the road.

Let’s break down the key components that influence your $10,000 car loan payment.

1. The All-Important Interest Rate

The interest rate is arguably the most significant factor affecting your car loan payment. It represents the cost of borrowing money, expressed as a percentage of the principal loan amount. A higher interest rate means you’ll pay more over the life of the loan, while a lower rate saves you money.

Several variables dictate the interest rate you’re offered. Your credit score is paramount, but the lender you choose, current market conditions, and even the loan term can also play a role. Understanding these dynamics allows you to strategically position yourself for the best possible rate.

2. The Impact of Your Credit Score

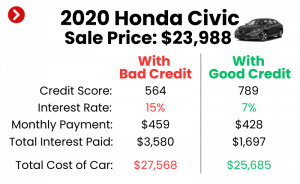

Your credit score acts as a financial report card, indicating your reliability as a borrower. Lenders use it to assess the risk of lending you money. A higher credit score (typically 700+) signals lower risk, often translating into lower interest rates and more favorable loan terms. Conversely, a lower score might lead to higher rates to compensate for perceived risk.

Pro tips from us: Before even thinking about a car loan, obtain a copy of your credit report from all three major bureaus (Equifax, Experian, Transunion). Review it for any inaccuracies and dispute them immediately. Improving your credit score, even by a few points, can significantly reduce the overall cost of your $10,000 car loan.

3. The Loan Term (Repayment Period)

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). This factor has a direct, inverse relationship with your monthly payment. A longer loan term generally results in lower monthly payments, making the car seem more affordable upfront.

However, there’s a trade-off. Extending the loan term also means you’ll pay more in total interest over the life of the loan. A shorter term, while resulting in higher monthly payments, saves you money on interest and allows you to own the car outright much faster. Common mistakes to avoid are extending the loan term purely for a lower payment without considering the increased total cost.

4. The Power of a Down Payment

A down payment is an upfront cash payment you make towards the purchase price of the car. It directly reduces the amount you need to borrow, thus lowering your monthly payments and the total interest paid over the loan term. Even a modest down payment can make a noticeable difference in your $10,000 car loan payment.

Beyond the financial benefits, a down payment also demonstrates your commitment to the loan, which can sometimes help you secure a better interest rate from lenders. Based on my experience, putting down at least 10-20% is often recommended, though even a smaller amount is better than none.

5. Trade-In Value: Leveraging Your Old Vehicle

If you have an existing vehicle, trading it in can act much like a down payment. The value of your trade-in is subtracted from the purchase price of the new car, reducing the principal amount you need to finance. This can significantly impact your $10,000 car loan payment.

It’s always a good idea to get an independent appraisal of your trade-in’s value before heading to the dealership. Knowing its worth empowers you to negotiate a fair price and ensures you’re getting the most out of your old car. This proactive step can save you hundreds, if not thousands, on your new loan.

6. Additional Fees, Taxes, and Insurance

Beyond the car’s price and interest, several other costs can be rolled into your loan, impacting the total amount financed. These include sales tax, registration fees, documentation fees, and sometimes even an extended warranty or GAP insurance. While some of these are unavoidable, others are optional.

It’s crucial to understand all these charges and decide which ones you truly need. Paying these fees upfront, if possible, can keep your principal loan amount lower, leading to smaller monthly payments. Always ask for an itemized list of all costs before finalizing your loan agreement.

Calculating Your $10,000 Car Loan Payments: Real-World Examples

To illustrate how these factors come together, let’s look at some hypothetical scenarios for a $10,000 car loan. While these are examples, they provide a clear picture of how different variables affect your monthly outlay. Remember, actual rates and payments can vary.

The general formula for calculating loan payments is complex, involving the principal amount, interest rate, and number of payments. However, for practical purposes, online car loan calculators are your best friend. They quickly do the math for you.

Let’s assume a principal amount of $10,000 (after any down payment or trade-in).

Example 1: Excellent Credit, Shorter Term

- Principal Loan Amount: $10,000

- Credit Score: Excellent (760+)

- Interest Rate: 4.0% APR

- Loan Term: 48 months (4 years)

In this scenario, your estimated monthly payment would be approximately $225.79. The total interest paid over 4 years would be around $837.92. This approach offers a lower total cost due to the favorable interest rate and shorter term, but with a slightly higher monthly commitment.

Example 2: Good Credit, Standard Term

- Principal Loan Amount: $10,000

- Credit Score: Good (670-739)

- Interest Rate: 6.5% APR

- Loan Term: 60 months (5 years)

Here, your estimated monthly payment would be around $196.56. The total interest paid over 5 years would be approximately $1,793.60. While the monthly payment is lower, the longer term and slightly higher interest rate result in significantly more interest paid over time.

Example 3: Average Credit, Longer Term

- Principal Loan Amount: $10,000

- Credit Score: Average (600-669)

- Interest Rate: 9.0% APR

- Loan Term: 72 months (6 years)

For this scenario, your estimated monthly payment would be about $183.05. However, the total interest paid over 6 years would skyrocket to approximately $3,179.60. This illustrates the significant cost of a higher interest rate combined with an extended loan term. While the monthly payment seems very affordable, you’re paying a substantial premium for it.

Pro tip: Use an online car loan calculator to play with different scenarios. Input various interest rates and loan terms to see how your monthly payment and total interest change. A reliable tool can be found on sites like NerdWallet’s Car Loan Calculator or your preferred bank’s website. This will give you a realistic expectation of your $10,000 car loan payment.

Strategies to Secure the Best $10,000 Car Loan Deal

Getting a car loan isn’t just about accepting the first offer you receive. Smart strategies can significantly improve your terms and save you money. Based on my experience, proactive planning is key to unlocking the best possible deal.

1. Shop Around for Lenders (Get Pre-Approved!)

Don’t limit yourself to dealership financing alone. Explore options from various sources:

- Banks: Traditional banks often offer competitive rates to their existing customers.

- Credit Unions: These member-owned institutions are known for offering some of the lowest interest rates.

- Online Lenders: Companies like LightStream or Capital One Auto Finance provide quick online applications and competitive offers.

The most powerful tool here is getting pre-approved before you even step foot on a dealership lot. Pre-approval gives you a firm offer for a specific loan amount and interest rate, allowing you to negotiate the car’s price separately and with confidence. It transforms you into a cash buyer in the eyes of the dealer.

2. Prioritize Improving Your Credit Score

As we discussed, your credit score is a major determinant of your interest rate. If your score isn’t where you want it to be, take steps to improve it before applying for a loan. Pay all your bills on time, reduce existing debt, and avoid opening new credit accounts just before applying for a car loan.

Even a few months of focused effort can significantly boost your score, potentially shaving percentage points off your interest rate. This might seem like a small detail, but it translates into hundreds, if not thousands, of dollars saved on your $10,000 car loan.

3. Make a Meaningful Down Payment

Even with a $10,000 loan, a down payment makes a huge difference. Aim for at least 10-20% of the vehicle’s purchase price. This reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest you’ll accrue.

A substantial down payment also reduces your loan-to-value (LTV) ratio, which can make you a more attractive borrower to lenders. This might even help you qualify for a better interest rate. Every dollar you put down upfront is a dollar you don’t pay interest on.

4. Opt for a Shorter Loan Term (If Affordable)

While a longer loan term offers lower monthly payments, it costs you more in the long run due to increased interest. If your budget allows, choose the shortest loan term you can comfortably afford. This strategy minimizes the total interest paid, saving you money and getting you out of debt faster.

Balance affordability with total cost. A slightly higher monthly payment for a shorter term can lead to significant savings over the life of your $10,000 car loan.

5. Negotiate the Car Price Separately

Always negotiate the purchase price of the car independently from the financing terms. Dealerships sometimes try to bundle these discussions, which can obscure the true cost. Focus on getting the best "out-the-door" price for the vehicle first.

Once you’ve agreed on a price, then you can discuss financing. Since you’re pre-approved, you’ll already have a strong negotiating position. This two-step approach ensures you’re getting a fair deal on both the vehicle and the loan.

6. Carefully Consider Add-Ons

Dealerships often offer additional products like extended warranties, GAP insurance, or paint protection packages. While some might be worthwhile, others are not. Be critical and only purchase what you genuinely need.

If you decide to purchase an add-on, try to pay for it upfront rather than rolling it into your $10,000 car loan. Financing these extras means you’ll pay interest on them for the entire loan term, significantly increasing their overall cost.

Budgeting for Your $10,000 Car Loan Payment and Beyond

Securing a car loan is only one part of the equation. A truly informed decision involves understanding the full cost of car ownership. Many people focus solely on the monthly payment and overlook the other recurring expenses.

1. The True Cost of Car Ownership

Beyond your monthly $10,000 car loan payment, remember to budget for:

- Car Insurance: This is a non-negotiable expense and can vary widely based on your vehicle, location, driving record, and coverage.

- Fuel Costs: Estimate your weekly or monthly fuel consumption based on your driving habits and current gas prices.

- Maintenance and Repairs: Cars need regular oil changes, tire rotations, and occasional repairs. Set aside a small amount each month for these inevitable costs.

- Registration and Licensing Fees: These are annual or biennial expenses that vary by state.

Ignoring these costs can quickly lead to financial stress, even if your monthly loan payment seems affordable. Pro tips from us: Create a dedicated "car expense" category in your budget to track all these outlays.

2. Adopting a Realistic Budgeting Approach

A popular guideline is the "20/4/10 rule": aim for a 20% down payment, a 4-year (48-month) loan term, and ensure your total car expenses (loan payment, insurance, fuel, maintenance) don’t exceed 10% of your gross monthly income. While a $10,000 loan might not always require a 20% down payment, the spirit of this rule—affordability and a shorter term—remains valuable.

Create a detailed personal budget that accounts for all your income and expenses. This will help you identify how much you can realistically afford for a car payment without compromising other financial goals. For more tips on effective personal finance and budgeting, check out our article on .

Common Mistakes to Avoid When Financing a $10,000 Car Loan

Even with the best intentions, it’s easy to fall into common traps when getting a car loan. Being aware of these pitfalls can save you from costly errors.

- Focusing Only on the Monthly Payment: This is perhaps the biggest mistake. A low monthly payment often comes with a longer loan term and higher total interest. Always consider the total cost of the loan.

- Not Getting Pre-Approved: Walking into a dealership without pre-approval puts you at a disadvantage. You lose your negotiating power on the financing side.

- Ignoring Your Credit Score: Your credit score is your financial superpower. Not checking it or working to improve it means you’re likely leaving money on the table in the form of higher interest rates.

- Skipping a Down Payment: While not always mandatory, a down payment significantly reduces your loan amount, monthly payments, and total interest. It’s a missed opportunity for savings.

- Extending the Loan Term Unnecessarily: While it lowers monthly payments, a 72 or 84-month loan term for a $10,000 car loan means you’ll pay substantially more in interest and might even be upside down on your loan (owe more than the car is worth) for a significant period.

- Not Budgeting for All Car-Related Expenses: As discussed, insurance, fuel, and maintenance are ongoing costs. Failing to account for them can quickly derail your financial plan.

- Falling for High-Pressure Sales Tactics: Take your time, ask questions, and never feel rushed into a decision. A reputable lender or dealer will give you space to think.

Learn more about protecting your finances from common pitfalls in our guide to .

Refinancing Your $10,000 Car Loan: A Second Chance at Better Terms

Even if you’ve already secured a $10,000 car loan, it’s not too late to potentially improve your terms. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with a more favorable term.

When does refinancing make sense?

- Your Credit Score Has Improved: If your credit score has significantly increased since you took out the original loan, you might qualify for a much better interest rate.

- Interest Rates Have Dropped: General market interest rates might have decreased since your initial purchase, making refinancing attractive.

- You Want a Different Loan Term: You might want to shorten your loan term to save on interest (if you can afford higher payments) or extend it for lower payments (if you’re facing financial difficulty, though this increases total cost).

The process is similar to applying for your original loan: you’ll shop around for lenders, submit an application, and if approved, the new lender will pay off your old loan. Always compare the new offer to your current loan to ensure it truly benefits you after considering any fees associated with refinancing.

Conclusion: Driving Towards Financial Confidence with Your $10,000 Car Loan

Navigating the world of car loans, even for a seemingly modest $10,000, requires diligence and an informed approach. Understanding the critical factors—interest rates, credit scores, loan terms, and down payments—empowers you to make smart decisions that align with your financial goals. By actively shopping for lenders, working on your credit, and strategically planning your budget, you can secure the best possible payment for your $10,000 car loan.

Remember, a car loan is a significant financial commitment. Don’t let the excitement of a new vehicle overshadow the importance of careful planning and research. By avoiding common mistakes and being proactive, you can ensure your journey into car ownership is not only enjoyable but also financially sound. Drive confidently, knowing you’ve made the smartest choices for your wallet.

What has been your experience with car loans? Share your thoughts and tips in the comments below!