Unlocking Your Ride: A Deep Dive into Your $14,000 Car Loan Monthly Payment

Unlocking Your Ride: A Deep Dive into Your $14,000 Car Loan Monthly Payment Carloan.Guidemechanic.com

Embarking on the journey to purchase a car is an exciting milestone, but navigating the financial aspects can often feel daunting. For many, a $14,000 car loan represents an accessible entry point into vehicle ownership, whether for a reliable used car or a budget-friendly new model. However, understanding what your monthly payment will look like, and more importantly, how to manage it effectively, is crucial for a smooth financial ride.

This comprehensive guide will break down every element influencing your $14,000 car loan monthly payment. We’ll explore the critical factors, provide calculation insights, and offer expert strategies to ensure you secure the best possible deal. Our goal is to equip you with the knowledge to make informed decisions, transforming potential stress into confidence.

Unlocking Your Ride: A Deep Dive into Your $14,000 Car Loan Monthly Payment

Understanding What a $14,000 Car Loan Entails

A $14,000 car loan typically puts you in the market for a well-maintained used vehicle or a very basic new car, depending on current market conditions and available incentives. It’s a common loan amount that many first-time buyers or those looking for a secondary vehicle often consider. Securing this loan involves borrowing money from a lender and agreeing to repay it, along with interest, over a set period.

The principal amount of $14,000 is just the starting point. Your actual monthly outflow will be significantly shaped by a series of interconnected financial variables. These factors work in tandem to determine the final number you’ll see on your monthly statement. Understanding each one individually is the first step towards financial clarity.

Let’s dive into the core components that dictate how much you’ll pay each month for your $14,000 car loan.

Key Factors Influencing Your Monthly Payment

Calculating your exact $14,000 car loan monthly payment isn’t as simple as dividing $14,000 by the number of months in your loan term. Several crucial elements play a significant role. Ignoring any of these could lead to unexpected financial strain down the road.

1. The Loan Amount Itself

While we’re discussing a $14,000 loan, remember this is the financed amount. It’s not necessarily the total price of the car. The final financed amount directly impacts your payment.

A higher financed amount naturally leads to a higher monthly payment, assuming all other factors remain constant. Conversely, reducing the amount you need to borrow will bring your monthly obligation down. This is where down payments and trade-ins become incredibly powerful tools.

2. The Interest Rate (APR)

The Annual Percentage Rate (APR) is arguably the most significant factor affecting your monthly car payment after the principal itself. This is the cost of borrowing money, expressed as a yearly percentage. A higher APR means you pay more in interest over the life of the loan.

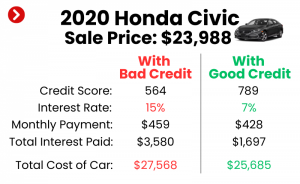

How APR is Determined: Your credit score is the primary driver of your APR. Lenders assess your creditworthiness to determine the risk involved in lending to you. A strong credit history, typically a score above 700, will qualify you for the most favorable rates. Conversely, a lower credit score often results in a higher APR, reflecting the increased risk perceived by the lender. Market conditions and the specific lender you choose also play a role.

Impact of APR: Even a slight difference in APR can translate into significant savings or additional costs over the loan term. For instance, the difference between a 4% and an 8% APR on a $14,000 loan can easily add tens of dollars to your monthly payment and hundreds or thousands to the total cost. Based on my experience, securing the lowest possible APR is paramount to managing your overall car loan expense effectively.

Pro Tips for Securing a Lower Rate: Always shop around with multiple lenders, including banks, credit unions, and online lenders. Don’t just accept the dealership’s first offer. Improve your credit score before applying by paying bills on time and reducing existing debt. Consider a co-signer with excellent credit if your own score is less than ideal.

3. The Loan Term (Duration)

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). This factor has a direct, inverse relationship with your monthly payment.

Short vs. Long Terms: A shorter loan term means fewer payments, which translates to higher individual monthly payments. However, you’ll pay significantly less interest over the life of the loan. Conversely, a longer loan term reduces your monthly payment, making it seem more affordable in the short term. The trade-off here is that you’ll end up paying substantially more in total interest.

Common Mistakes to Avoid: A common mistake is extending the loan term purely to achieve a lower monthly payment without considering the total cost. While a 72-month loan for $14,000 might look appealing on a monthly basis, you could end up paying thousands more in interest compared to a 48-month term. This is especially true for a $14,000 car, which might depreciate faster than you pay it off, leading to being "upside down" on your loan.

Our Recommendation: Aim for the shortest loan term you can comfortably afford. This strategy minimizes the total interest paid and helps you build equity in your vehicle faster. For a $14,000 loan, terms between 36 and 60 months are generally advisable.

4. Your Down Payment

A down payment is the initial amount of money you pay upfront when purchasing a car, reducing the amount you need to finance. This directly lowers your principal loan amount.

How it Reduces the Principal: If you put down $2,000 on a $14,000 car, you’ll only need to finance $12,000. This smaller financed amount immediately translates to a lower monthly payment. It also reduces the total interest you’ll pay, as interest is calculated on the principal balance.

Benefits of a Larger Down Payment: Beyond lowering your monthly payment, a significant down payment can help you secure a better interest rate. Lenders view a larger down payment as a sign of financial stability and commitment, reducing their risk. It also helps prevent you from owing more than the car is worth (being "underwater" or "upside down") as depreciation takes its toll.

5. Trade-in Value

If you’re replacing an existing vehicle, its trade-in value can act just like a cash down payment. The dealership will deduct the agreed-upon trade-in amount from the purchase price of your new car.

How it Acts Like a Down Payment: For example, if you trade in a car worth $3,000, and you’re buying a $14,000 car, your effective loan amount becomes $11,000 (assuming no additional cash down payment). This directly reduces the principal and, consequently, your monthly payment and total interest.

Maximizing Trade-in Value: To get the best trade-in value, ensure your car is clean, well-maintained, and has all service records. Research its market value using online tools like Kelley Blue Book or Edmunds before heading to the dealership. Being informed gives you leverage in negotiations.

Calculating Your Potential Monthly Payment for a $14,000 Car Loan

While an exact calculation requires a financial calculator or specific software, we can illustrate how the variables combine. The basic formula for an amortizing loan payment is complex, but online car loan calculators make it simple.

Here’s a simplified way to understand the components:

- Principal: The $14,000 (minus any down payment/trade-in).

- Interest: Added to the principal over the loan term.

Let’s look at some examples for a $14,000 car loan (assuming no down payment) to give you a clearer picture:

| Loan Term (Months) | Interest Rate (APR) | Estimated Monthly Payment | Total Interest Paid | Total Cost of Loan |

|---|---|---|---|---|

| 36 | 4.0% | $412.35 | $844.60 | $14,844.60 |

| 36 | 8.0% | $438.90 | $1,800.40 | $15,800.40 |

| 48 | 4.0% | $317.07 | $1,219.36 | $15,219.36 |

| 48 | 8.0% | $341.38 | $2,386.24 | $16,386.24 |

| 60 | 4.0% | $257.67 | $1,460.20 | $15,460.20 |

| 60 | 8.0% | $283.47 | $3,008.20 | $17,008.20 |

As you can see, even for the same $14,000 loan, the monthly payment can vary significantly based on the term and interest rate. A difference of just a few percentage points in APR can add hundreds or even thousands to your total loan cost. Always use an online car loan calculator to get precise figures based on your specific terms.

Beyond the Monthly Payment: The True Cost of Car Ownership

While your $14,000 car loan monthly payment is a major component, it’s just one piece of the puzzle. Overlooking other essential expenses is a common pitfall that can lead to financial strain. Based on my experience, many people get fixated on the monthly loan payment and forget the broader picture.

1. Car Insurance

This is a non-negotiable expense for any vehicle owner. The cost of car insurance varies widely based on factors like your age, driving record, location, the car’s make and model, and the coverage you choose. For a $14,000 car, you’ll likely need comprehensive and collision coverage if you have a loan, as required by lenders.

Proactively research insurance quotes before finalizing your car purchase. A car that seems affordable on paper might come with surprisingly high insurance premiums. For a deeper dive, you might want to read our comprehensive guide on Choosing the Right Car Insurance Policy (Internal Link Placeholder).

2. Maintenance and Repairs

Every car, especially a used one, requires regular maintenance and occasional repairs. Budgeting for oil changes, tire rotations, brake pad replacements, and unforeseen issues is crucial. A good rule of thumb is to set aside $50-$100 per month for maintenance, even if you don’t use it every month.

For a $14,000 car, which might be older or have higher mileage, the likelihood of needing repairs can be higher. Always factor this into your overall budget.

3. Fuel Costs

Unless you’re purchasing an electric vehicle, fuel will be a recurring expense. Your fuel costs depend on the car’s fuel efficiency (MPG), current gas prices, and how much you drive.

Calculate an estimate of your weekly or monthly fuel consumption to get a realistic picture. Don’t underestimate this cost, especially if you have a long commute.

4. Registration and Taxes

Vehicle registration fees are typically annual and vary by state. Sales tax on your car purchase is usually a one-time expense, paid at the time of sale or registration, and can add several hundred to over a thousand dollars to your initial costs.

These are mandatory expenses that must be accounted for in your overall car ownership budget.

5. Extended Warranties (Exercise Caution)

Dealerships often push extended warranties, sometimes rolling them into your loan. While they offer peace of mind, they can be expensive and may not always be worth the cost, especially on a $14,000 used car.

Carefully evaluate the coverage, exclusions, and cost. Often, setting aside a monthly amount in a "car repair fund" can be a more financially sound strategy than paying for an expensive extended warranty.

Strategies for Securing and Managing Your Car Loan

Successfully navigating a $14,000 car loan involves more than just finding a car; it’s about smart financial planning and execution.

1. Improve Your Credit Score

Your credit score is your financial report card, and a higher score unlocks better loan terms. Before applying for a loan, take steps to boost your score. Pay all your bills on time, reduce outstanding debt, and avoid opening new lines of credit.

Even a modest improvement can shift you into a better interest rate tier, saving you hundreds of dollars. For more in-depth strategies, explore our article on Boosting Your Credit Score for a Car Loan (Internal Link Placeholder).

2. Get Pre-Approved

Pre-approval means a lender has reviewed your financial information and agreed to lend you a specific amount at a particular interest rate, before you even step foot in a dealership. This is a powerful negotiation tool.

Benefits: You’ll know exactly what you can afford and what your monthly payment will be. It allows you to focus on negotiating the car price, rather than the financing. You can then use the pre-approval offer to leverage a better rate from the dealership’s finance department.

3. Budget Wisely: Understand Your Affordability

Before you even look at cars, sit down and honestly assess your monthly budget. Factor in all your income and expenses. A general rule of thumb is that your total car expenses (loan payment, insurance, fuel, maintenance) should not exceed 10-15% of your net monthly income.

Consider your debt-to-income (DTI) ratio. Lenders look at this to determine your ability to take on new debt. A DTI below 36% is generally favorable.

4. Negotiate Both the Car Price and the Interest Rate

Many buyers focus solely on the car price, but remember that the interest rate also impacts your total cost. With a pre-approval in hand, you can negotiate with confidence.

Don’t be afraid to walk away if the terms aren’t favorable. There are always other cars and other lenders.

5. Consider Refinancing Your Loan

If market rates drop, your credit score improves significantly after purchasing your car, or you initially secured a high-interest loan, refinancing could be an option. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms.

This can significantly reduce your monthly payment or the total interest paid over the life of the loan. Always compare the new loan’s terms, including any fees, against your current loan.

Common Mistakes to Avoid When Taking a $14,000 Car Loan

Based on my years of observing car buyers, certain pitfalls repeatedly trip people up. Avoiding these can save you considerable stress and money.

-

Focusing Solely on the Monthly Payment: This is perhaps the most common mistake. Dealerships often try to "sell" you on a monthly payment, extending the loan term to make it seem more affordable. Always look at the total cost of the loan, including all interest. A low monthly payment might mean paying significantly more over time.

-

Ignoring the Total Cost of Ownership: As discussed, the monthly loan payment is only one part of the equation. Failing to budget for insurance, fuel, maintenance, and registration can quickly lead to financial strain and buyer’s remorse. Always calculate the all-in monthly cost before committing.

-

Not Shopping Around for Rates: Accepting the first loan offer you receive, especially from the dealership, can be a costly error. Lenders compete for your business, and taking the time to compare offers from various banks, credit unions, and online lenders can save you hundreds, if not thousands, in interest.

-

Extending the Loan Term Excessively: While a longer term lowers your monthly payment, it dramatically increases the total interest paid. For a $14,000 car, a 72-month or longer loan can mean you owe more than the car is worth for a significant portion of the loan, making it difficult to sell or trade in.

-

Skipping Pre-Approval: Going into a dealership without a pre-approved loan puts you at a disadvantage. You lose your leverage in negotiations and might end up with a less favorable rate offered by the dealership’s finance department, who may have marked up the interest rate for profit.

Pro Tips from an Expert Blogger

Based on my experience in the financial and automotive world, here are some actionable pro tips to help you navigate your $14,000 car loan:

- Do Your Homework Thoroughly: Research not just the car, but also average interest rates for your credit score, and common loan terms. The more informed you are, the better equipped you’ll be to negotiate.

- Separate the Car Price from the Loan Terms: When at the dealership, try to negotiate the price of the car first, before discussing financing. This prevents the dealer from shifting money around between the car price and the loan terms.

- Read Every Document Carefully: Before signing anything, read all the fine print of your loan agreement. Understand the interest rate, term, any prepayment penalties, and all fees. Don’t be afraid to ask questions.

- Consider the "Why" of Your Purchase: For a $14,000 car, think about its intended purpose. Is it a reliable daily driver or a temporary solution? This helps align your financial commitment with your needs.

Always approach car buying with a clear head and a well-researched plan. This disciplined approach is your best defense against overpaying.

Conclusion: Drive Confidently with a Smart $14,000 Car Loan Plan

Securing a $14,000 car loan can be a straightforward process when you understand all the contributing factors. Your monthly payment isn’t just a number; it’s a reflection of your loan amount, interest rate, term, and any upfront payments you make. By diligently researching, improving your credit, getting pre-approved, and negotiating wisely, you put yourself in a prime position to secure favorable terms.

Remember to look beyond the monthly payment and account for the full spectrum of car ownership costs. A holistic financial perspective ensures that your new vehicle brings joy and convenience, not unexpected financial burdens. Plan smartly, drive confidently, and enjoy the open road ahead!