Unlocking Your Ride: Navigating Car Loan APR with a 650 Credit Score

Unlocking Your Ride: Navigating Car Loan APR with a 650 Credit Score Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used car is exciting, but the financial aspect can often feel like navigating a complex maze. One of the most crucial elements to understand is your Annual Percentage Rate (APR), especially when your credit score hovers around the 650 mark. A 650 credit score sits right in the "fair" to "good" range, a position that opens doors to financing but also requires a strategic approach to secure the best possible terms.

Many prospective car buyers wonder what kind of interest rate they can realistically expect and how to improve their chances of approval with favorable conditions. This comprehensive guide will demystify car loan APRs for individuals with a 650 credit score, offering actionable insights, expert tips, and a clear roadmap to help you drive away with a deal you feel confident about. We’ll explore everything from understanding your credit standing to advanced strategies for lowering your interest rate and avoiding common pitfalls.

Unlocking Your Ride: Navigating Car Loan APR with a 650 Credit Score

Decoding Your 650 Credit Score: What It Means for Car Loans

Your credit score is essentially a financial report card, summarizing your creditworthiness based on your borrowing and repayment history. A 650 credit score, as categorized by FICO and VantageScore, generally falls into the "Fair" category, though it’s on the cusp of "Good" for some lenders. This means you’ve demonstrated some responsible credit behavior, but there might be a few areas for improvement, or your credit history might simply be shorter.

From a lender’s perspective, a 650 score indicates a moderate level of risk. You’re not considered a high-risk borrower who might default, but you’re also not in the prime tier that automatically qualifies for the absolute lowest interest rates. This position is often a tipping point. Some lenders will view it favorably, while others might offer higher APRs to compensate for the perceived risk. Understanding this perception is the first step in preparing for your car loan application.

Realistic Expectations: Average Car Loan APRs for a 650 Credit Score

When you have a 650 credit score, it’s essential to set realistic expectations for your car loan APR. While you won’t typically qualify for the rock-bottom rates advertised for borrowers with excellent credit (750+), you’re also unlikely to face the extremely high rates reserved for those with very poor credit.

Based on my experience and industry data, for borrowers with a 650 credit score, you can generally expect the following average APR ranges:

- New Cars: For a new car loan, an average APR for a 650 credit score typically ranges from 7.5% to 12.0%. This can fluctuate based on market conditions, the specific lender, and the loan term you choose. New cars often come with slightly lower APRs than used cars because they are perceived as less risky by lenders due to warranties and predictable depreciation.

- Used Cars: Used car loans often carry a slightly higher risk for lenders, which translates to a higher average APR. For a 650 credit score, you might see rates ranging from 9.0% to 15.0% or even higher depending on the vehicle’s age, mileage, and the loan term. Older vehicles or those with high mileage can push these rates up further.

It’s crucial to remember that these are averages. Your actual rate could be lower or higher depending on a multitude of factors we’ll discuss shortly. Pro tips from us: Don’t just accept the first offer you receive. Shopping around is paramount to finding the best rate available for your credit profile.

Beyond the Score: Key Factors Influencing Your Specific APR

While your 650 credit score is a significant factor, it’s not the only determinant of your car loan APR. Several other variables play a crucial role in the final interest rate you’re offered. Understanding these can empower you to negotiate better terms or prepare adequately.

1. Loan Term: Shorter vs. Longer

The length of your loan, or its term, has a direct impact on your APR. Generally, shorter loan terms (e.g., 36 or 48 months) come with lower interest rates because the lender’s risk is reduced over a shorter period. Longer terms (e.g., 60, 72, or even 84 months) often have higher APRs, though they result in lower monthly payments. While a longer term might seem appealing due to lower monthly costs, it means you’ll pay significantly more in total interest over the life of the loan.

2. Down Payment: Your Financial Cushion

Making a substantial down payment is one of the most effective ways to lower your APR. A larger down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk. When lenders see that you have a significant financial stake in the vehicle, they are often more willing to offer a lower interest rate. Aim for at least 10-20% of the car’s purchase price if possible.

3. Vehicle Type: New vs. Used, and the Car’s Value

The type of vehicle you intend to purchase also influences your APR. As mentioned, new cars generally command lower rates than used cars. Within the used car market, the age, mileage, and overall condition of the vehicle matter. Lenders perceive newer, lower-mileage vehicles as less risky because they are less likely to break down and hold their value better, making them easier to repossess and sell if you default.

4. Lender Type: Where You Apply Matters

Not all lenders are created equal. Different types of financial institutions have varying risk appetites and lending criteria.

- Credit Unions: Often known for offering competitive rates, especially to their members, due to their not-for-profit structure.

- Banks: Traditional banks offer a wide range of loan products and can be a good option, but their rates might be less flexible than credit unions.

- Dealership Financing: Convenient, as you can often get approved on the spot, but their rates might include markups. They often work with multiple lenders, so it’s wise to compare.

- Online Lenders: These can sometimes offer quick approvals and competitive rates, especially for those with fair credit, as they have lower overheads.

Shopping around extensively across these lender types is a strategy we highly recommend.

5. Debt-to-Income Ratio (DTI): Can You Afford It?

Your Debt-to-Income (DTI) ratio is a crucial metric for lenders. It compares your total monthly debt payments (including the proposed car payment) to your gross monthly income. A lower DTI indicates that you have more disposable income to cover your loan payments, making you a less risky borrower. Lenders typically prefer a DTI of 36% or lower, though some might go up to 43%. A high DTI, even with a 650 credit score, can lead to a higher APR or even loan denial.

6. Co-signer: Sharing the Risk

If you have a 650 credit score and want to improve your chances of getting a lower APR, considering a co-signer with excellent credit can be a game-changer. A co-signer legally agrees to take responsibility for the loan if you fail to make payments. This significantly reduces the lender’s risk, often resulting in a lower interest rate. Ensure both you and your co-signer understand the implications before proceeding.

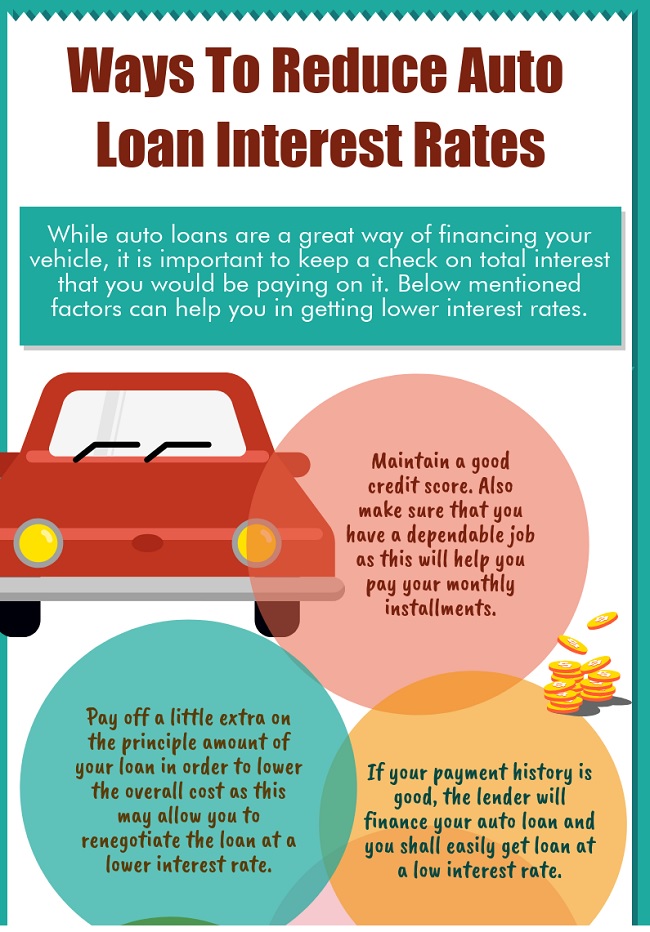

Strategies to Improve Your Car Loan APR with a 650 Credit Score

While a 650 credit score is a decent starting point, there are proactive steps you can take to enhance your loan terms and secure a more favorable APR.

1. Boost Your Credit Score (Even Slightly)

Even a small bump in your credit score can make a difference.

- Pay Bills on Time: This is the single most impactful action. Lenders want to see a consistent history of timely payments.

- Reduce Credit Card Balances: Lowering your credit utilization (the amount of credit you use compared to your total available credit) can quickly improve your score. Aim to keep it below 30%, ideally below 10%.

- Check for Errors: Review your credit report for any inaccuracies. Disputing and correcting errors can sometimes lead to a score increase.

2. Save for a Larger Down Payment

As discussed, a significant down payment is your best friend when it comes to lowering your APR. If you can save up 20% or more of the car’s price, you’ll not only reduce your monthly payments but also the total interest paid over the life of the loan. It also helps avoid being "upside down" on your loan (owing more than the car is worth) early on.

3. Shop Around and Get Pre-Approved from Multiple Lenders

This is perhaps the most critical strategy. Don’t limit yourself to the dealership’s financing.

- Credit Unions: Start with local credit unions; they often have competitive rates.

- Banks: Check with your current bank and other major banks.

- Online Lenders: Explore reputable online lenders who specialize in car loans.

Getting pre-approved from several lenders allows you to compare offers side-by-side. These pre-approvals typically involve a soft credit inquiry, which doesn’t harm your score, and give you a solid offer to use as leverage at the dealership. Common mistakes to avoid are only getting one offer or waiting until you’re at the dealership to think about financing.

4. Consider a Co-signer (If Applicable)

If you have a trusted family member or friend with a strong credit history, asking them to co-sign could significantly reduce your APR. Ensure they understand the responsibility, as any missed payments will negatively affect both your credit scores.

5. Choose a Shorter Loan Term

While a longer loan term offers lower monthly payments, a shorter term often comes with a lower APR. If your budget allows, opting for a 36 or 48-month loan over a 60 or 72-month one can save you thousands in interest. Balance affordability with the total cost of the loan.

6. Negotiate the Car’s Price

Remember that your loan APR is applied to the total amount you borrow. By negotiating a lower purchase price for the car itself, you reduce the principal amount of your loan, which in turn reduces the total interest you’ll pay, regardless of the APR.

The Car Loan Application Process: What to Expect

Navigating the application process can be smooth if you’re prepared. Here’s a quick overview:

- Gather Your Documents: Lenders will typically require proof of identity (driver’s license), proof of income (pay stubs, tax returns), proof of residence (utility bill), and possibly bank statements.

- Understand Pre-qualification vs. Pre-approval:

- Pre-qualification: A preliminary check, often with a soft credit pull, that gives you an estimate of what you might qualify for. It’s not a guaranteed offer.

- Pre-approval: A more thorough review, usually with a hard credit pull, resulting in a firm offer from a lender. This is your most powerful tool for negotiating.

- Read the Fine Print: Carefully review all loan offers, paying close attention to the APR, loan term, total interest paid, and any fees. Don’t rush this step.

For more details on preparing your documents and navigating the initial stages, check out our guide on .

Common Pitfalls and How to Avoid Them

Even with a 650 credit score, it’s easy to fall into traps that can lead to a less-than-ideal car loan. Based on my experience working with countless car buyers, here are some common mistakes to avoid:

- Focusing Only on Monthly Payments: While monthly affordability is important, fixating solely on it can lead you to accept longer loan terms with higher overall interest. Always look at the total cost of the loan.

- Not Getting Pre-Approved: Walking into a dealership without pre-approval puts you at a disadvantage. You lose your negotiation power and might settle for a higher APR simply out of convenience.

- Accepting Unnecessary Add-ons: Dealerships often try to sell extended warranties, GAP insurance, and other add-ons. While some might be beneficial, others are overpriced or unnecessary. Research these thoroughly and only accept what you truly need.

- Ignoring Your Budget: Don’t let the excitement of a new car push you beyond what you can comfortably afford. Factor in not just the loan payment, but also insurance, maintenance, and fuel costs.

- Making Multiple Hard Credit Inquiries Over an Extended Period: While rate shopping within a 14-45 day window typically counts as a single inquiry for scoring purposes, spreading your applications over several months can negatively impact your score. Concentrate your shopping within a short period.

When is Refinancing a Good Option?

Even if you secure a car loan with a 650 credit score and feel the APR is decent for your current situation, it doesn’t have to be permanent. If you improve your credit score significantly (e.g., to 700+) after a year or two of on-time payments, or if market interest rates drop, refinancing your car loan could be an excellent strategy to lower your APR and monthly payments.

Refinancing involves taking out a new loan to pay off your existing car loan. If your credit has improved, you’ll likely qualify for a much better interest rate. This can lead to substantial savings over the remaining term of your loan. It’s always worth reviewing your loan terms periodically to see if refinancing makes financial sense for you. If you’re considering refinancing down the road, our article on provides a deeper dive into the process and benefits.

To understand more about how your credit score impacts various financial products, including loans, the Consumer Financial Protection Bureau offers excellent resources on credit and lending practices. You can find valuable information on their official website.

Driving Forward with Confidence

Securing a car loan with a 650 credit score is entirely achievable, and with the right approach, you can even lock in a very competitive APR. The key lies in understanding your credit position, knowing the factors that influence your interest rate, and proactively implementing strategies to strengthen your application. By shopping around, considering a substantial down payment, and maintaining a healthy financial profile, you significantly increase your chances of getting a car loan with an APR that aligns with your budget and financial goals.

Don’t let a "fair" credit score deter you from pursuing your dream car. With diligence, preparation, and the insights provided in this guide, you can navigate the complexities of car financing and drive away with confidence, knowing you’ve made an informed and strategic decision about your car loan APR. Start planning today, check your credit report, and empower yourself with knowledge before you step onto the dealership lot.