Unlocking Your Ride: The Definitive Guide to In-House Car Loans for Every Buyer

Unlocking Your Ride: The Definitive Guide to In-House Car Loans for Every Buyer Carloan.Guidemechanic.com

Dreaming of a new set of wheels but worried your credit history might stand in the way? You’re not alone. Many aspiring car owners face hurdles when seeking traditional auto financing, often due to past financial challenges, a thin credit file, or even no credit history at all. This is where the world of in-house car loans steps in, offering a unique pathway to vehicle ownership that bypasses conventional banking gatekeepers.

In this super comprehensive guide, we’ll dive deep into the intricate world of in-house car loans. We’ll explore exactly what they are, how they work, their distinct advantages and disadvantages, and crucial tips for securing the best possible deal. Our aim is to equip you with the knowledge to make an informed decision, ensuring you drive away not just with a car, but with confidence.

Unlocking Your Ride: The Definitive Guide to In-House Car Loans for Every Buyer

What Exactly is an In-House Car Loan? Demystifying Dealer Financing

At its core, an in-house car loan, often referred to as "dealer financing" or "buy here, pay here" (BHPH), is a type of auto loan where the dealership itself acts as the lender. Unlike traditional financing where a bank, credit union, or third-party financial institution provides the funds, with an in-house loan, you’re making your payments directly to the car lot where you purchased the vehicle.

This model fundamentally differs from securing a loan through an external financial institution. When you get a loan from a bank, the bank evaluates your creditworthiness, approves the loan, and then pays the dealer for the car. You then repay the bank. With an in-house loan, the dealership essentially cuts out the middleman, taking on the role of both seller and financier.

The "buy here, pay here" moniker aptly describes the operational structure. You buy your car at the dealership, and you make your payments right there as well. This direct relationship can simplify the process for certain buyers, but it also comes with its own set of considerations that are vital to understand.

This financing option primarily targets individuals who might struggle to obtain approval from conventional lenders. This includes people with low credit scores, those who have experienced bankruptcy, or even young buyers with no established credit history. The dealership takes on a higher risk, which is often reflected in the loan terms.

The Mechanics of How In-House Loans Work: A Step-by-Step Breakdown

Understanding the operational flow of an in-house car loan is key to navigating this unique financing landscape. The process typically begins much like any car purchase, but with a few distinct differences in the financing stage.

1. The Application Process:

When you visit a dealership offering in-house financing, the application process tends to be more streamlined and less reliant on a perfect credit score. Instead of solely focusing on your FICO score, these dealers often place a greater emphasis on your ability to make payments. They’ll look at your income stability, employment history, and residency.

You’ll typically be asked to provide proof of income, such as recent pay stubs or bank statements, and proof of residence, like utility bills. The goal is to establish a consistent income flow that demonstrates your capacity to meet weekly or bi-weekly payment obligations. This focus on current financial stability rather than past credit issues is a hallmark of the in-house model.

2. Approval Criteria Beyond Credit Score:

One of the most appealing aspects of in-house financing is its flexible approval criteria. While traditional lenders heavily weigh your credit score, in-house dealers often prioritize other factors. They understand that a low credit score doesn’t always equate to an inability to pay, especially if recent financial situations have improved.

Key factors for approval include a steady job, a verifiable income, and a reasonable down payment. Some dealerships might also consider your debt-to-income ratio, but generally, the bar for approval is lower than with conventional banks, making car ownership accessible to a broader demographic.

3. Vehicle Selection and Inventory:

The vehicles available for in-house financing are typically drawn from the dealership’s existing inventory, which often consists of used cars. While some larger BHPH dealerships may offer a wide array of options, the selection might be more limited compared to what you’d find at a new car dealership or through traditional financing.

It’s important to remember that these vehicles have often been acquired at a lower cost, allowing the dealership to finance them directly. Therefore, while you might find a reliable car, it’s crucial to manage expectations regarding luxury features or the latest models.

4. Payment Structure and Schedule:

A distinguishing feature of in-house loans is their payment structure. Payments are frequently scheduled on a weekly or bi-weekly basis, rather than the traditional monthly cycle. This aligns with common payroll schedules, making it easier for borrowers to manage their budgets and ensure timely payments.

This frequent payment schedule can be a double-edged sword. On one hand, it can help prevent large, overwhelming monthly payments. On the other hand, it requires diligent budgeting and consistent cash flow to avoid falling behind, as missed payments can quickly accumulate.

The Advantages of Opting for In-House Financing: A Pathway to Ownership

For many individuals, in-house car loans represent a viable, and sometimes the only, path to vehicle ownership. There are several distinct advantages that make this financing option appealing, particularly for those facing credit challenges.

1. Accessibility for Bad or No Credit:

This is arguably the most significant advantage. If your credit score has taken a hit due to unforeseen circumstances, or if you’re a young adult just starting to build your financial history, traditional lenders can be unforgiving. In-house dealerships are designed to cater to these specific needs, often approving loans when banks would outright refuse.

Based on my experience, many individuals who’ve faced bankruptcy, foreclosure, or multiple late payments find a lifeline with in-house financing. It provides an opportunity to get transportation when other doors are closed.

2. Faster Approval Process:

Because the dealership is making the lending decision directly, the approval process is often significantly quicker than with a bank. You can walk into a BHPH lot, apply, get approved, and potentially drive away in a car all on the same day. This speed can be incredibly beneficial for those who need a vehicle urgently.

There’s no waiting for external underwriting departments or dealing with multiple layers of bureaucracy. The decision is made on-site, which can alleviate the stress and uncertainty associated with traditional loan applications.

3. Convenience and One-Stop Shop:

The convenience of an in-house loan cannot be overstated. You handle the car selection, financing, and often even the registration all under one roof. This integrated approach saves time and effort, eliminating the need to visit separate financial institutions and dealerships.

For busy individuals, or those who prefer a simpler transaction, the "one-stop shop" model of in-house financing is a distinct draw. It streamlines what can often be a complex and fragmented car-buying journey.

4. Potential for Credit Rebuilding (If Reported):

One of the hidden benefits, if handled correctly, is the potential to rebuild your credit score. If the in-house dealership reports your payment history to the major credit bureaus (Equifax, Experian, TransUnion), making timely payments can positively impact your score.

This is a crucial point to verify, as not all in-house lenders report payments. However, for those that do, it offers a tangible way to demonstrate financial responsibility and improve your creditworthiness for future endeavors.

5. Flexibility in Terms (Sometimes):

While often associated with rigid terms, some in-house dealers might offer a degree of flexibility, especially regarding payment schedules. Because they manage the loans directly, they might be more amenable to adjusting payment dates to align with your specific pay cycle, though this is not a universal guarantee.

This personalized approach can be a benefit for borrowers with non-traditional income streams or those who need a payment plan tailored more closely to their unique financial rhythm. Always discuss payment flexibility upfront.

The Disadvantages and Potential Pitfalls: Navigating the Challenges

While in-house car loans offer a valuable solution for many, it’s equally important to be aware of their potential downsides. Understanding these challenges will help you approach the process with caution and make well-informed decisions.

1. Higher Interest Rates:

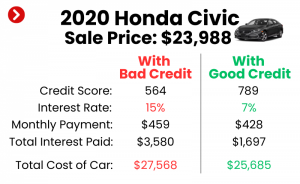

Perhaps the most significant disadvantage of in-house financing is the typically higher interest rates. Because these dealerships take on a greater risk by lending to individuals with poor or no credit, they compensate for that risk by charging higher Annual Percentage Rates (APRs).

It’s not uncommon to see APRs ranging from 15% to 25% or even higher, depending on your credit profile and the state’s regulations. This means you’ll end up paying significantly more for the car over the life of the loan compared to traditional financing options.

2. Limited Vehicle Selection:

As mentioned earlier, the inventory at BHPH lots is usually comprised of used vehicles. While you might find a reliable car, the choices can be more restricted in terms of make, model, year, and features. You might not have the same breadth of options as you would shopping at multiple dealerships or through a traditional lender.

This limitation means you might have to compromise on certain preferences, and it’s essential to ensure the available vehicles meet your fundamental transportation needs rather than settling for something unsuitable.

3. Shorter Loan Terms and Higher Payments:

In an effort to mitigate risk and recoup their investment faster, in-house loans often come with shorter loan terms, typically ranging from 24 to 48 months. While a shorter term means you pay off the loan faster, it also translates to higher weekly or bi-weekly payments.

These elevated payments can strain your budget, especially when combined with the higher interest rates. It’s crucial to accurately assess your ability to consistently afford these payments without jeopardizing other financial obligations.

4. Potential for Predatory Practices:

Unfortunately, the in-house financing sector is not immune to less reputable actors. Some dealerships may engage in predatory lending practices, such as selling overpriced vehicles, charging excessive fees, or not clearly disclosing all terms. This is a common mistake to avoid.

It’s paramount to research the dealership thoroughly, read reviews, and carefully scrutinize every aspect of the loan agreement before signing. Transparency and clear communication are non-negotiable from a trustworthy lender.

5. Lack of Credit Reporting (A Key Concern):

As noted, a significant benefit of in-house loans can be credit rebuilding. However, this only happens if the dealership reports your payment history to the major credit bureaus. Many smaller BHPH lots do not report payments, which means even if you make every payment on time, it won’t positively impact your credit score.

Before committing, always ask directly and get written confirmation that the dealership reports to all three major credit bureaus. Without this, you miss a crucial opportunity to improve your financial standing.

Who Benefits Most from an In-House Car Loan? Identifying the Ideal Candidate

While not for everyone, in-house car loans serve a specific demographic exceptionally well. Understanding if you fall into this category can help you determine if this is the right financing avenue for your needs.

1. Individuals with Low or Subprime Credit Scores:

This is the primary target audience. If your credit score is below 600, or you’ve been repeatedly denied by traditional banks, in-house financing offers a viable alternative. Dealers are often more lenient, focusing on your current income and down payment rather than past credit missteps.

2. First-Time Buyers with No Credit History:

Young adults or new immigrants who haven’t had the opportunity to establish a credit history often find themselves in a "catch-22" situation: you need credit to get a loan, but you need a loan to build credit. In-house loans can break this cycle, providing an entry point into the credit world.

3. Those with Unique Financial Situations:

Self-employed individuals with irregular income, people who have recently filed for bankruptcy, or those with past repossessions often face an uphill battle with conventional lenders. In-house dealers are often more understanding of these circumstances and willing to work with unique financial profiles.

4. Anyone Needing a Car Quickly and Without Hassle:

If you’re in urgent need of transportation and don’t have the time or patience for a lengthy traditional loan application process, in-house financing offers speed and simplicity. The expedited approval can get you on the road much faster.

Navigating the In-House Loan Process: What to Look For and Ask

Securing an in-house car loan requires diligence and careful consideration. To protect yourself and ensure a fair deal, follow these essential guidelines.

1. Research Reputable Dealers:

Not all in-house dealerships are created equal. Pro tips from us: Look for dealers with positive online reviews, a strong track record, and a transparent sales process. Check their ratings with the Better Business Bureau (BBB) and read customer testimonials to gauge their reputation.

A reputable dealer will be upfront about all terms and fees, and won’t pressure you into a decision. Trust your gut feeling about the establishment and its staff.

2. Understand the Total Cost: APR and Fees:

Do not focus solely on the monthly payment. Demand to know the full Annual Percentage Rate (APR) and any associated fees (origination fees, documentation fees, etc.). The APR reflects the true cost of borrowing, incorporating both interest and certain fees.

A common mistake to avoid is overlooking these additional costs. Insist on a clear breakdown of the total amount you will pay over the life of the loan.

3. Verify Credit Reporting:

As highlighted, this is critical for credit rebuilding. Before you sign anything, get written confirmation from the dealer that they report all payments to at least two, preferably all three, major credit bureaus. If they don’t, understand that your on-time payments won’t help your credit score, which might diminish one of the key potential benefits.

4. Get a Pre-Purchase Vehicle Inspection:

Since BHPH inventory is typically used cars, a pre-purchase inspection by an independent mechanic is non-negotiable. This is perhaps one of the most crucial pro tips we can offer. Do not skip this step. The mechanic can identify any hidden issues that could lead to costly repairs down the road, saving you immense headaches and expenses.

This inspection can also give you leverage for negotiation if minor issues are found. You want to be confident in the vehicle’s reliability, especially when committing to a loan.

5. Down Payment Considerations:

Most in-house loans require a down payment. The larger your down payment, the less you’ll need to finance, which can reduce your overall interest paid and potentially lower your weekly/bi-weekly payments. Be prepared to put down a significant amount, if possible.

6. Negotiate Terms:

While some aspects might be fixed, don’t be afraid to negotiate. Discuss the interest rate, the down payment amount, and even the loan term if you feel comfortable with higher payments for a shorter duration. Every little bit of negotiation can save you money in the long run.

Alternatives to In-House Car Loans: Exploring Other Avenues

Before committing to an in-house loan, it’s always wise to explore other potential financing options. You might be surprised at what’s available, especially if your credit isn’t as dire as you think.

1. Credit Unions:

Often more forgiving than large banks, credit unions are non-profit organizations that prioritize their members. They may offer more flexible lending criteria and lower interest rates for individuals with less-than-perfect credit. It’s worth checking if you qualify for membership.

2. Online Lenders Specializing in Bad Credit:

A growing number of online lenders cater specifically to individuals with bad credit. Companies like Capital One Auto Finance, myAutoloan, or Carvana (for their financing arm) may offer competitive rates even for subprime borrowers. Always compare their offers with in-house options.

3. Seeking a Co-Signer:

If you have a trusted family member or friend with good credit who is willing to co-sign your loan, this can significantly improve your chances of approval with traditional lenders and secure a much lower interest rate. However, remember that a co-signer is equally responsible for the debt.

4. Saving Up for a Cash Purchase:

While not always feasible for urgent needs, saving up to buy a reliable used car outright is the ideal scenario. It eliminates interest payments, frees you from loan obligations, and often allows you to get a better deal on the vehicle itself.

5. Secured Personal Loans:

If you have an asset (like a savings account or another paid-off vehicle) that you can use as collateral, a secured personal loan might be an option. These typically come with lower interest rates because the lender’s risk is reduced.

Rebuilding Your Credit with an In-House Loan: A Strategic Approach

If you’ve confirmed that your chosen in-house dealer reports to credit bureaus, this loan can be a powerful tool for credit repair. However, it requires a strategic and disciplined approach.

1. The Power of On-Time Payments:

This cannot be stressed enough: make every single payment on time, without fail. Payment history is the most significant factor in your credit score, accounting for about 35% of your FICO score. Consistent, timely payments will demonstrate reliability and positively impact your credit.

Set up reminders, automate payments if possible, or mark your calendar to ensure you never miss a due date. This commitment is vital for leveraging the loan for credit building.

2. Verifying Credit Reporting:

After a few months, request a free copy of your credit report from each of the major bureaus (Equifax, Experian, TransUnion) to ensure the loan is accurately reflected and that your payments are being reported. The official site for free credit reports is AnnualCreditReport.com.

If you find discrepancies or that payments aren’t being reported, contact the dealership and the credit bureaus to rectify the issue. This proactive approach ensures your efforts are being recognized.

3. How It Impacts Your Score Over Time:

With consistent on-time payments over the loan term, you should see a gradual but significant improvement in your credit score. This improved score will then open doors to better financing options in the future, including lower interest rates on subsequent car loans, mortgages, or credit cards.

View your in-house car loan as an investment in your financial future, using it as a stepping stone to greater financial freedom and more favorable lending terms down the road.

The Future of Dealer Financing: Evolving Landscape

The landscape of dealer financing is continually evolving. As technology advances and consumer demands shift, we can expect to see further changes in how in-house loans are offered and managed.

Increased transparency is a growing trend, with more regulations pushing for clearer disclosure of loan terms and fees. This will benefit consumers by making it easier to compare offers and identify reputable lenders.

Technological advancements, such as AI-driven credit assessment and digital payment platforms, are also streamlining the application and payment processes, making in-house loans even more accessible and efficient. The "buy here, pay here" model is adapting, integrating more sophisticated tools to serve its unique customer base.

Conclusion: Making an Informed Decision on Your In-House Car Loan

An in-house car loan can be an incredibly valuable option for individuals who have been turned away by traditional lenders. It offers a direct, often swift, path to vehicle ownership, particularly for those looking to rebuild or establish their credit. However, it’s crucial to approach this financing method with a clear understanding of both its advantages and its inherent challenges.

By diligently researching dealerships, scrutinizing loan terms, understanding the total cost of borrowing, and verifying credit reporting, you can navigate the in-house loan process successfully. Remember, an informed buyer is an empowered buyer. Do not rush into a decision, and always prioritize transparency and fairness.

Your journey to car ownership, even with credit challenges, is absolutely possible. By weighing your options, asking the right questions, and being prepared, you can secure a reliable vehicle and potentially use this opportunity to build a stronger financial future. Explore your choices, empower yourself with knowledge, and drive away confidently!