Unlocking Your Ride: The Ultimate Guide to Securing a $10,000 Car Loan

Unlocking Your Ride: The Ultimate Guide to Securing a $10,000 Car Loan Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect, but navigating the world of car financing can often feel overwhelming. For many, a $10,000 car loan represents a sweet spot – enough to secure a reliable vehicle without committing to a massive debt. This comprehensive guide will demystify the process, offering expert insights, practical tips, and strategic advice to help you secure an affordable and favorable 10k car loan.

As an expert blogger and SEO content writer with years of experience in personal finance, I understand the nuances of securing vehicle financing. My goal is to equip you with the knowledge to make informed decisions, ensuring you drive away with not just a car, but also a smart financial choice. We’ll delve deep into everything from eligibility to application, and even how to manage your loan effectively.

Unlocking Your Ride: The Ultimate Guide to Securing a $10,000 Car Loan

Why a $10,000 Car Loan Might Be Your Perfect Fit

A $10,000 car loan is often sought by individuals looking for practical, budget-friendly transportation. It’s a popular option for first-time car buyers, students, those needing a second family vehicle, or anyone aiming to avoid high monthly payments. This specific loan amount opens up a wide market of quality used cars that can serve you reliably for years.

The affordability of a 10k car loan means lower monthly payments compared to larger loans, which can significantly ease the strain on your budget. It allows you to access a diverse range of vehicles, from compact sedans known for fuel efficiency to slightly older SUVs offering more space. This financial sweet spot ensures you can find a dependable car without overextending yourself.

However, it’s crucial to approach this with realistic expectations. While $10,000 can get you a great used car, it’s unlikely to buy a brand-new model. The focus should be on finding a well-maintained vehicle that meets your needs and offers good value for money. Careful research and inspection are paramount when shopping in this price range.

Understanding Your Eligibility for a $10,000 Car Loan

Before you even start browsing cars, understanding your eligibility is the first and most crucial step. Lenders assess several factors to determine if you qualify for a $10,000 car loan and, more importantly, what interest rate they’ll offer. Knowing these elements upfront can significantly improve your chances of approval and help you secure better terms.

Your credit score is arguably the most influential factor. A strong credit history demonstrates your reliability as a borrower and typically unlocks the best interest rates. Lenders view a higher score as lower risk, which translates to more favorable loan terms for you. Even with a lower score, a 10k car loan is often still accessible, though the terms might be less ideal.

Income stability and your debt-to-income (DTI) ratio also play a significant role. Lenders want to see that you have a consistent income stream sufficient to cover your monthly loan payments, in addition to your existing financial obligations. A lower DTI ratio indicates you have more disposable income to dedicate to your new car payment, making you a more attractive borrower.

Based on my experience, even with a solid credit score and stable income, a down payment can dramatically improve your loan application. A down payment reduces the amount you need to borrow, thereby lowering your monthly payments and potentially securing a better interest rate. It also signals to lenders that you are financially committed to the purchase.

Types of Lenders for Your $10,000 Car Loan

When seeking a $10,000 car loan, you have several avenues to explore, each with its own advantages. Comparing offers from different types of lenders is a pro tip from us; it ensures you get the most competitive rates and terms. Don’t settle for the first offer you receive, as even a slight difference in interest rate can save you hundreds over the life of the loan.

Traditional banks are a common choice, offering structured loan products and often competitive rates for well-qualified borrowers. If you already have an established relationship with a bank, they might offer you special perks or a streamlined application process. It’s always worth checking with your current bank first.

Credit unions, on the other hand, are member-owned non-profit organizations, which often translates to more personalized service and potentially lower interest rates compared to traditional banks. Their focus is on serving their members, making them an excellent option for a 10k car loan, especially if you qualify for membership. Many credit unions have broad eligibility requirements, so it’s worth investigating.

Online lenders have emerged as a popular choice due to their convenience and speed. They offer quick application processes and fast approval times, often providing competitive rates without the need for an in-person visit. These platforms are particularly useful for comparing multiple offers simultaneously, allowing you to easily find the best deal from the comfort of your home.

Finally, dealership financing offers the convenience of a one-stop shop. You can browse cars and arrange financing all in the same location. While this is incredibly convenient, it’s crucial to remember that dealerships often work with multiple lenders and may mark up interest rates. Always compare their offer with pre-approvals you’ve secured elsewhere to ensure you’re getting a fair deal.

The Application Process: A Step-by-Step Guide

Applying for a $10,000 car loan doesn’t have to be daunting. By following a structured approach, you can navigate the process smoothly and confidently. Being prepared is key to a successful application and securing favorable terms.

Step 1: Check Your Credit Score and Report. Before approaching any lender, obtain a copy of your credit report and score. This gives you an accurate picture of your financial standing and allows you to identify any errors that could negatively impact your application. You can get free copies of your credit reports annually from AnnualCreditReport.com.

Step 2: Determine Your Budget. Beyond the loan amount, consider all associated costs: insurance, registration, maintenance, and fuel. A $10,000 car loan is just one piece of the puzzle. Understand your total monthly vehicle budget before committing to a loan payment.

Step 3: Gather Necessary Documents. Lenders will require documentation to verify your identity, income, and residence. This typically includes a government-issued ID, proof of income (pay stubs, tax returns), proof of residence (utility bill), and possibly bank statements. Having these ready will expedite your application.

Step 4: Get Pre-Approved. This is a pro tip that can save you time and money. Pre-approval involves a lender reviewing your financial information and offering you a conditional loan amount and interest rate before you even choose a car. It gives you significant bargaining power at the dealership and helps you shop within your true budget.

Step 5: Shop for Your Car. With pre-approval in hand, you know exactly how much you can afford. This allows you to focus on finding the best car that fits your needs and budget without the pressure of financing negotiations at the dealership. Remember to consider reliability and future maintenance costs.

Step 6: Finalize Your Loan. Once you’ve chosen your car, you’ll finalize the loan with your chosen lender. Carefully review all terms and conditions, including the interest rate, loan term, and any fees, before signing. Ensure there are no hidden clauses or unexpected charges.

Common mistakes to avoid are not checking your credit score beforehand, rushing into the first loan offer, and not comparing rates from multiple lenders. These oversights can lead to higher interest rates and less favorable loan terms, costing you more in the long run.

Key Factors Affecting Your $10,000 Car Loan Terms

The specific terms of your $10,000 car loan are influenced by several critical factors. Understanding these can help you strategize and potentially secure a more advantageous deal. Each element plays a significant role in determining your monthly payment and the total cost of the loan.

The interest rate (APR) is perhaps the most impactful factor. It’s the cost of borrowing money, expressed as a percentage of the loan amount. A lower interest rate means lower monthly payments and less money paid overall. Your credit score is the primary driver of the interest rate you’ll be offered. A higher score typically unlocks the lowest rates available for a 10k car loan.

The loan term, or the duration over which you repay the loan, also significantly affects your payments. Shorter terms (e.g., 36 months) result in higher monthly payments but less interest paid over time. Longer terms (e.g., 60 months) offer lower monthly payments but accumulate more interest over the loan’s lifespan. It’s a balance between affordability and total cost.

As mentioned earlier, a down payment is incredibly powerful. Even a modest down payment on a $10,000 car loan can reduce your principal, lower your monthly payments, and demonstrate your commitment to the lender. It also decreases the loan-to-value (LTV) ratio, which can positively influence your interest rate.

The age and mileage of the vehicle you choose also factor into the loan terms, especially for used cars. Lenders view older, higher-mileage vehicles as higher risk because they might be less reliable and depreciate faster. This can sometimes lead to slightly higher interest rates or shorter loan terms. For a $10,000 car, most options will be used, so this is an important consideration.

Navigating a $10,000 Car Loan with Less-Than-Perfect Credit

Securing a $10,000 car loan with a less-than-perfect credit score can be more challenging, but it is certainly not impossible. Many lenders specialize in providing financing to individuals with fair or bad credit. The key is to understand your options and prepare for potentially different terms.

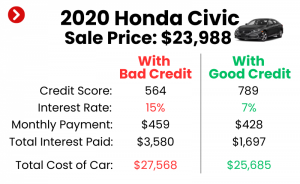

Based on my experience, securing a $10,000 car loan with bad credit often means you’ll face higher interest rates. Lenders perceive a lower credit score as a higher risk, and they compensate for that risk by charging more for the loan. This means your monthly payments and the total cost of the loan will be higher than for someone with excellent credit.

One effective strategy is to provide a larger down payment. A substantial down payment reduces the amount you need to borrow, thereby lowering the lender’s risk and potentially making you a more attractive applicant. It also shows your financial commitment to the purchase, which can sway a lender.

Consider adding a co-signer with good credit to your loan application. A co-signer essentially guarantees the loan, promising to make payments if you default. This significantly reduces the lender’s risk and can help you qualify for a loan you otherwise wouldn’t, or secure a much better interest rate. However, ensure your co-signer understands their responsibilities.

Exploring secured loans is another option. Some lenders might offer a car loan that is "secured" by another asset you own, though this is less common for car loans themselves as the car serves as collateral. More relevant are "credit-builder" loans or programs specifically designed to help those with poor credit establish a payment history, which can indirectly help with future car loans.

Finally, be prepared to shop around and compare offers from multiple lenders, including those specializing in subprime auto loans. While the rates may be higher, comparing several offers ensures you still get the best available terms for your situation. Avoid predatory lenders who offer extremely high rates and unfavorable terms.

What to Look for in a $10,000 Car

Once your financing for a $10,000 car loan is in order, the fun part begins: car shopping! When working with a budget of around $10,000, focusing on reliability, maintenance costs, and thorough inspection is crucial. You want to maximize the value you get for your money.

Prioritize reliability. Certain car brands and models have a well-deserved reputation for durability and longevity. Research consumer reports and owner reviews for vehicles in your price range. Opting for a car known for its robust engineering can save you significant money on repairs down the line.

Beyond the purchase price, consider the potential maintenance costs. European luxury cars, for example, often have higher parts and labor costs compared to their Japanese or American counterparts, even if their initial used price is attractive. Research common issues for the specific make and model you’re considering. A pre-purchase inspection by an independent mechanic is a non-negotiable step. This small investment can uncover hidden problems that might cost thousands to fix.

Don’t forget to factor in insurance costs. Premiums vary wildly based on the make, model, age, and safety features of the vehicle, as well as your driving record and location. Get insurance quotes for specific cars you’re considering before making a final decision. A car that seems cheap to buy might be expensive to insure.

Common mistakes to avoid when shopping for a $10,000 car include falling for cosmetic appeal without checking mechanical integrity, skipping a test drive, and neglecting to get a vehicle history report (like CarFax or AutoCheck). These reports can reveal past accidents, title issues, and service history, providing crucial insights into the car’s true condition.

Pro Tips for Managing Your $10,000 Car Loan

Securing your $10,000 car loan is just the beginning; effective loan management is key to maintaining good financial health and potentially saving money. A well-managed loan can also improve your credit score, opening doors to better financial opportunities in the future.

Set up automatic payments. This is one of the easiest ways to ensure you never miss a payment, which is critical for maintaining a good credit score. Late payments can incur fees and negatively impact your credit history. Automating your payments removes the risk of forgetfulness.

Consider making extra payments. If your budget allows, making additional payments towards your principal can significantly reduce the total interest paid over the life of the loan. Even small extra payments, like rounding up your monthly payment or making an extra payment annually, can make a big difference. This strategy helps you pay off your 10k car loan faster.

Explore refinancing options. If your credit score has improved since you initially took out your $10,000 car loan, or if interest rates have dropped, you might be able to refinance your loan for a lower interest rate. Refinancing can lead to lower monthly payments or a shorter loan term, saving you money in the long run. Always compare the new offer with your existing loan terms, including any refinancing fees.

Maintain good credit habits. Your car loan payments contribute to your credit history. Making timely payments on your 10k car loan will positively impact your credit score. Continue to monitor your credit report regularly to ensure accuracy and spot any potential issues early.

Finally, budget for unexpected car costs. Even the most reliable used cars will eventually require maintenance or repairs. Set aside a small amount each month for a "car emergency fund." This ensures you’re prepared for unforeseen expenses without derailing your budget or falling behind on your loan payments.

Drive Away with Confidence

Securing a $10,000 car loan is a highly achievable goal that can put you behind the wheel of a reliable vehicle without breaking the bank. By understanding the factors that influence your eligibility, exploring various lending options, and meticulously preparing for the application process, you empower yourself to make the best financial decisions. Remember, knowledge is power, especially when it comes to your money.

From checking your credit score to wisely choosing your vehicle and diligently managing your loan, every step contributes to a smoother, more affordable car ownership experience. Don’t rush the process, compare your options, and always prioritize long-term financial health. With the insights shared in this guide, you are now well-equipped to navigate the world of car financing and secure your ideal 10k car loan.

Start your journey today with confidence, knowing you have the tools and information to make a smart and informed decision. Happy driving!