Unlocking Your Wheels: Navigating the Car Loan Landscape with a 670 FICO Score

Unlocking Your Wheels: Navigating the Car Loan Landscape with a 670 FICO Score Carloan.Guidemechanic.com

Securing a car loan can feel like a daunting task, especially when you’re unsure where your credit stands. If your FICO score hovers around 670, you’re in what’s often termed the "fair" credit range. But what does a 670 FICO score truly mean for your car loan aspirations? Can you get approved? What kind of rates can you expect?

The good news is, a 670 FICO score for a car loan is far from a dead end. In fact, it places you squarely in a position where approval is very possible, though perhaps with a bit more strategic planning than someone with excellent credit. This comprehensive guide is designed to empower you with the knowledge, strategies, and insider tips needed to not just get approved, but to secure the best possible terms for your next vehicle purchase. Let’s dive deep and transform your 670 FICO score into a key for your dream car.

Unlocking Your Wheels: Navigating the Car Loan Landscape with a 670 FICO Score

Understanding Your 670 FICO Score: What Lenders See

Before you even start browsing vehicles, it’s crucial to understand how lenders perceive a 670 FICO score. Your credit score is essentially a snapshot of your financial reliability, a numerical representation of your creditworthiness. A 670 FICO score falls within the "Fair" credit category, typically ranging from 580 to 669. While you’re just above that threshold, it still signals a moderate level of risk to potential lenders.

Lenders use FICO scores to assess the likelihood of you repaying your loan obligations. A score in the fair range suggests that while you likely have a history of managing credit, there might be some areas for improvement. Perhaps you’ve had a late payment or two in the past, a high credit utilization ratio, or a relatively short credit history. These factors, though not catastrophic, prompt lenders to proceed with a degree of caution.

Based on my experience, lenders are more willing to approve loans for individuals with a 670 FICO score compared to those in the "poor" category. However, they will also typically offer higher interest rates to compensate for the perceived increased risk. This is a fundamental aspect of lending – the higher the risk, the higher the cost of borrowing. Understanding this dynamic is your first step toward effective negotiation.

Lender’s Perspective: Risk vs. Reward

For a bank or credit union, every loan decision involves a careful calculation of risk versus potential reward. A 670 FICO score indicates that you are not a prime borrower (typically 700+), but you’re also not a subprime borrower (below 620-640). This puts you in a middle ground, where lenders will scrutinize other aspects of your financial profile more closely. They want to see stability and a clear ability to repay.

They will look beyond just the number. Your income, employment history, debt-to-income ratio, and the size of your down payment will all play significant roles in their final decision. A 670 FICO score is an indicator, but it’s not the only factor. A strong application elsewhere can often compensate for a less-than-perfect score.

What to Expect: Interest Rates and Loan Terms

With a 670 FICO score, you should generally expect interest rates that are higher than those offered to borrowers with excellent credit. While someone with a 750+ score might qualify for rates under 5%, you might see offers in the 8-12% range, or even higher, depending on market conditions and the specific lender. These rates reflect the lender’s assessment of the additional risk they’re taking on.

Loan terms might also be slightly less flexible. You might find lenders offering longer loan terms (e.g., 72 or 84 months) to lower your monthly payments, making the loan more affordable. However, a longer loan term means you’ll pay significantly more in interest over the life of the loan. It’s a trade-off that requires careful consideration of your budget and long-term financial goals.

Preparing for Your Car Loan Application: Laying the Groundwork

Success in securing a car loan with a 670 FICO score largely hinges on thorough preparation. This isn’t just about collecting documents; it’s about strategically positioning yourself as a reliable borrower. By taking these proactive steps, you can significantly improve your chances of approval and potentially secure better terms.

Know Your Credit Report Inside Out

Your FICO score is derived from the information in your credit report. Before applying for any loan, obtain a copy of your credit report from all three major bureaus (Experian, Equifax, and TransUnion). You can do this for free annually at AnnualCreditReport.com. This step is non-negotiable.

Scrutinize every detail on these reports. Look for any errors, inaccuracies, or outdated information that could be negatively impacting your score. Common mistakes include incorrect addresses, accounts that aren’t yours, or debts that have already been paid off. Disputing these errors can lead to an increase in your score, sometimes quite quickly.

Budgeting Realistically: Understanding Affordability

Before you fall in love with a particular car, determine how much you can truly afford to pay each month. This isn’t just about the car payment. Remember to factor in insurance, fuel, maintenance, and potential repair costs. These "total cost of ownership" expenses can add up quickly.

Pro tips from us: Use an online car loan calculator to estimate payments based on different interest rates, loan terms, and down payment amounts. This will give you a clear picture of what fits comfortably within your monthly budget without stretching your finances too thin. Over-extending yourself on a car loan is a common mistake that can lead to financial stress down the line.

The Power of a Down Payment

A substantial down payment is one of your most potent tools when applying for a car loan with a 670 FICO score. It directly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan. More importantly, it signals to lenders that you are serious about the purchase and have a financial stake in the vehicle.

Lenders view a larger down payment as a sign of reduced risk. It shows you have financial discipline and reduces the loan-to-value (LTV) ratio, meaning the car is less likely to be "underwater" (where you owe more than it’s worth) early in the loan term. Aim for at least 10-20% of the car’s purchase price, if possible.

Your Debt-to-Income (DTI) Ratio Matters

Your debt-to-income (DTI) ratio is a critical metric lenders use to assess your ability to manage monthly payments. It’s calculated by dividing your total monthly debt payments (including rent/mortgage, credit cards, student loans, etc.) by your gross monthly income. A lower DTI ratio indicates less financial strain and a greater capacity to take on new debt.

For a car loan, lenders typically prefer a DTI ratio of 36% or lower, though some might go up to 43% for fair credit borrowers. If your DTI is high, consider paying down some existing debts before applying for a car loan. This demonstrates responsible financial management and improves your overall borrowing profile.

Strategies for Securing a Car Loan with a 670 FICO Score

With your preparation complete, it’s time to strategize your approach to securing the best possible car loan. This involves smart shopping for lenders and understanding how to leverage your financial position.

Get Pre-Approved First: Your Negotiation Superpower

One of the most powerful moves you can make is to get pre-approved for a car loan before you step foot in a dealership. This involves applying to banks, credit unions, or online lenders to see what loan amount and interest rate you qualify for. A pre-approval provides several key advantages.

Firstly, it gives you a concrete understanding of your borrowing power and expected interest rate. You walk into the dealership with a firm offer in hand, which acts as a powerful negotiating tool. Secondly, it separates the financing process from the car-buying process, allowing you to focus on getting the best price for the car itself. Finally, pre-approvals typically involve a "soft inquiry" on your credit, which doesn’t harm your score, until you finalize the loan.

Explore Different Lender Types

Don’t limit yourself to just one type of lender. Different institutions cater to different credit profiles and offer varying rates. Broadening your search can uncover better deals.

- Traditional Banks: Your local bank or a national bank where you have an existing relationship might offer competitive rates, especially if you have a history of on-time payments with them.

- Credit Unions: Often known for offering more favorable interest rates and terms, credit unions are member-owned and tend to be more flexible, especially for borrowers in the fair credit range. They often look beyond just your score.

- Online Lenders: A growing number of online lenders specialize in fair credit car loans. They often have streamlined application processes and can provide quick decisions. Companies like Capital One Auto Finance or LightStream are good starting points.

- Dealership Financing: While convenient, dealership financing (often called "captive finance" if it’s through the manufacturer’s own finance arm) might not always offer the best rates, especially for fair credit. However, they sometimes have special promotions or relationships with various lenders that could work in your favor. Always compare their offer to your pre-approval.

Consider a Co-signer: When it Makes Sense

If you’re struggling to get approved for favorable terms, or if your interest rates are excessively high, a co-signer could be a viable option. A co-signer is someone with excellent credit who agrees to take on the legal responsibility for the loan if you fail to make payments. This significantly reduces the risk for the lender.

However, choosing a co-signer is a serious decision. It directly impacts their credit score and financial standing. If you miss payments, it affects both your credit and theirs, and they will be legally obligated to pay the loan. Only consider this option if you are absolutely confident in your ability to make every payment on time. It’s a common mistake to underestimate the risk involved for the co-signer.

Negotiating Your Best Deal

With a 670 FICO score, negotiation is key. Don’t just accept the first offer. You have several points of leverage:

- Your Pre-Approval: Use it to show the dealership you have other options.

- Down Payment: Highlight your substantial down payment.

- Trade-in Value: If you have a trade-in, ensure you get a fair price for it.

- Interest Rate: Negotiate the interest rate. Even a half-percent reduction can save you hundreds over the life of the loan.

- Loan Term: Be wary of excessively long loan terms that lower monthly payments but dramatically increase total interest paid. Aim for the shortest term you can comfortably afford.

Pro tip: Negotiate the car price separately from the financing. First, agree on the car’s price, then discuss financing options. This prevents dealers from masking a high interest rate with a lower car price, or vice-versa.

What to Expect: Realistic Interest Rates and Loan Terms

Managing expectations is crucial when seeking a car loan with a 670 FICO score. While you won’t qualify for the absolute lowest rates reserved for prime borrowers, you can still secure a manageable loan.

Realistic Interest Rate Expectations

As mentioned, interest rates for borrowers with a 670 FICO score typically fall in the "fair credit" range. This could mean anywhere from 8% to 15% APR (Annual Percentage Rate), depending on the current economic climate, the specific lender, the age of the vehicle (new vs. used), and your overall financial profile. Newer cars generally command slightly lower rates due to their lower depreciation risk.

It’s important to shop around and compare offers from multiple lenders. Even a 1-2% difference in interest rate can translate into significant savings over a 5-7 year loan term. Don’t be afraid to leverage competing offers to try and get a better deal.

Understanding the Impact of Loan Term

The loan term, or the length of time you have to repay the loan, directly affects your monthly payment and the total interest you’ll pay. For instance, a longer term (e.g., 72 or 84 months) will result in lower monthly payments, which can make a more expensive car seem affordable. However, this convenience comes at a cost.

With a longer term, you’ll pay substantially more in total interest. For a 670 FICO score, where interest rates are already higher, extending the term significantly amplifies the total cost of the car. Always calculate the total amount you’ll pay back, including all interest, for different loan terms before committing. Sometimes, a slightly higher monthly payment for a shorter term is the more financially prudent choice.

Decoding the Fine Print

Once you receive a loan offer, take the time to read every single detail of the loan agreement. Don’t rush this step. Pay close attention to:

- APR (Annual Percentage Rate): This is the true cost of borrowing, including interest and any fees.

- Total Loan Amount: The principal you are borrowing.

- Total Repayment Amount: The total sum of principal and interest you will pay over the life of the loan.

- Prepayment Penalties: Check if there are any penalties for paying off your loan early. Ideally, you want a loan without these.

- Late Fees: Understand the penalties for missed or late payments.

If anything is unclear, ask questions until you fully understand. This is your financial commitment, and clarity is paramount.

Improving Your Credit Score (Even After Getting the Loan)

Getting a car loan with a 670 FICO score is a significant achievement, but your credit journey shouldn’t end there. Continually working to improve your credit score will open doors to even better financial opportunities in the future, including lower interest rates on subsequent loans or credit cards.

Why Continuous Improvement Matters

A higher credit score means access to lower interest rates on mortgages, personal loans, and even car loan refinancing. It can also impact things like insurance premiums and rental applications. By demonstrating consistent, responsible credit behavior, you build a stronger financial foundation. Even after you’ve driven off the lot, that car loan becomes an opportunity to build excellent credit.

Effective Strategies for Credit Score Improvement

- Make All Payments On Time, Every Time: Payment history is the most significant factor in your FICO score. Automate payments if possible to avoid missing due dates. This is the single most impactful action you can take.

- Reduce Credit Utilization: Keep your credit card balances low, ideally below 30% of your available credit limit. Lowering your utilization shows lenders that you’re not over-reliant on credit.

- Avoid New Debt (Temporarily): After taking out a car loan, try to avoid opening new credit accounts for a while. This allows your new car loan to establish a positive payment history without adding new inquiries or increasing your overall debt burden.

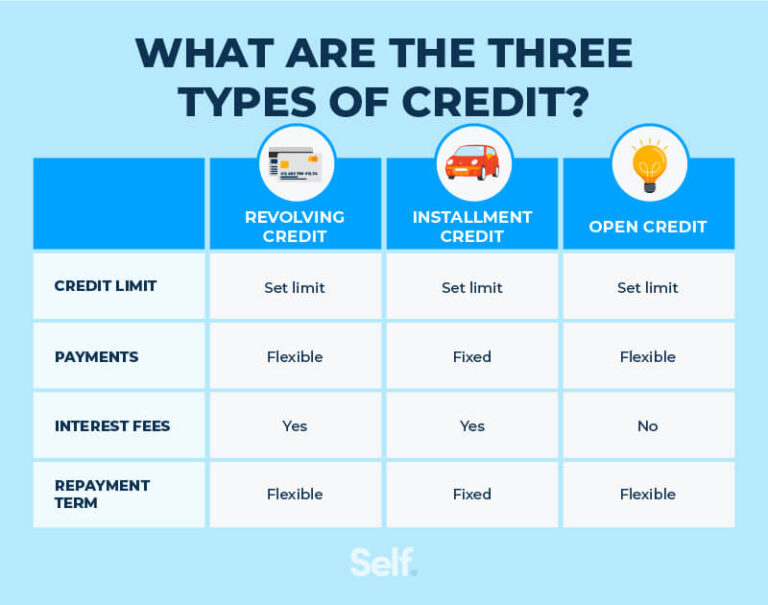

- Maintain a Mix of Credit: Having a healthy mix of credit types (e.g., installment loans like your car loan and revolving credit like credit cards) can positively impact your score over time, assuming you manage them responsibly.

- Monitor Your Credit Regularly: Continue to check your credit report annually for errors and to track your progress. for more in-depth strategies.

Alternatives and Considerations

Sometimes, despite your best efforts, the available loan terms with a 670 FICO score might not align with your financial goals or comfort level. In such cases, considering alternatives can be a smart move.

Buying a Less Expensive Car

It might sound obvious, but opting for a more affordable vehicle can drastically change your loan landscape. A lower principal amount means a smaller loan, which can translate to lower monthly payments and less overall interest paid, even with a slightly higher interest rate. This also reduces the financial pressure, allowing you to focus on improving your credit score for future purchases.

Saving Up Longer

If you’re not in immediate need of a new car, consider postponing your purchase and saving up for a larger down payment. This extra time can also be used to actively improve your credit score, potentially moving you into the "good" credit range (670-739) or even higher. A few months of diligent credit management can significantly reduce the interest rate you’ll be offered.

Refinancing Down the Road

Even if you take a car loan with a higher interest rate now, it’s not a permanent sentence. As you make consistent, on-time payments on your car loan and other debts, your credit score will likely improve. Once your score crosses into the "good" or "excellent" range, you can explore refinancing your car loan. Refinancing allows you to replace your existing loan with a new one, often with a lower interest rate and more favorable terms, saving you a substantial amount of money over time.

Conclusion: Driving Forward with Confidence

Navigating the car loan process with a 670 FICO score requires diligence, preparation, and a strategic approach. It’s a score that puts you in a position where approval is well within reach, but securing the best terms demands proactive steps. By understanding what lenders look for, preparing your finances, shopping strategically, and negotiating effectively, you can absolutely secure a car loan that meets your needs.

Remember, your 670 FICO score is a stepping stone, not a roadblock. Use this opportunity to not only get the car you need but also to demonstrate responsible financial behavior that will continue to build your creditworthiness for years to come. With the right information and a confident approach, you’ll be driving your new car in no time, knowing you made a smart financial decision.

For more information on understanding your credit score and its impact, you can visit a trusted external source like MyFICO.com.

Happy driving!