Unlocking Your Wheels: The Definitive Guide to Getting a Car Loan with a 500 Credit Score

Unlocking Your Wheels: The Definitive Guide to Getting a Car Loan with a 500 Credit Score Carloan.Guidemechanic.com

The dream of owning a reliable car is a common one, offering freedom, convenience, and access to opportunities. However, for many individuals, the reality of a challenging credit score can feel like a significant roadblock. If you’re looking for a car loan 500 credit, you’re likely aware of the hurdles that lie ahead.

But here’s the good news: while difficult, securing financing with a 500 credit score is not impossible. This comprehensive guide is designed to equip you with the knowledge, strategies, and insights needed to navigate the unique landscape of bad credit auto lending. We’ll explore exactly what a 500 credit score means to lenders, the realistic expectations you should have, and actionable steps you can take to significantly boost your approval chances.

Unlocking Your Wheels: The Definitive Guide to Getting a Car Loan with a 500 Credit Score

Our ultimate goal is to provide you with a clear roadmap, transforming a potentially daunting process into a manageable journey towards getting the car you need. Let’s dive in and unlock your wheels, even with a challenging credit history.

1. Understanding Your Credit Score: What Does 500 Really Mean?

Your credit score is a three-digit number that profoundly impacts your financial life, especially when it comes to borrowing money. It’s essentially a summary of your creditworthiness, based on your financial history. When lenders see a 500 credit score, it immediately flags you as a high-risk borrower.

Credit scores typically range from 300 to 850, with higher numbers indicating better credit. A score of 500 falls squarely into the "poor" or "very poor" category, according to major credit scoring models like FICO and VantageScore. This indicates to potential lenders that you’ve likely had difficulties managing credit in the past, such as missed payments, defaults, or high credit utilization.

Based on my experience working with countless individuals, many people misunderstand the direct impact of a 500 score. It’s not just a number; it’s a strong indicator of past financial struggles, making lenders hesitant to extend credit without significant safeguards or higher costs. Understanding this perception is the first step in addressing the challenge effectively.

2. The Reality Check: Can You Really Get a Car Loan with 500 Credit?

Let’s address the elephant in the room directly: yes, it is possible to get a car loan 500 credit. However, it’s crucial to approach this reality with eyes wide open and realistic expectations. This isn’t going to be the same experience as someone with excellent credit.

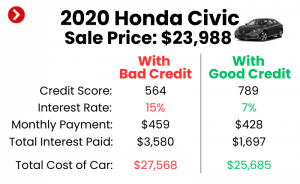

Lenders who approve applications with a 500 credit score are taking on a significantly higher risk. To offset this risk, they typically impose much stricter terms and conditions. This almost always translates into higher interest rates, which means you’ll pay substantially more over the life of the loan compared to someone with a good credit score.

These types of loans are often referred to as "subprime auto loans." They are specifically designed for borrowers with low credit scores or limited credit history. While they offer a pathway to vehicle ownership, they come with a premium. Setting realistic expectations about interest rates and overall loan cost is vital before you even begin your search.

3. Strategic Steps to Boost Your Approval Chances

While a 500 credit score presents challenges, there are concrete strategies you can employ to significantly improve your chances of getting approved for a car loan. These steps are about reducing the lender’s perceived risk and demonstrating your commitment to responsible borrowing.

3.1. The Power of a Down Payment

Perhaps the single most impactful factor in securing a car loan 500 credit is making a substantial down payment. When you put money down upfront, you immediately reduce the amount you need to borrow, which in turn lowers the lender’s risk. It shows commitment on your part.

A larger down payment also often leads to a lower monthly payment, making the loan more affordable and increasing your chances of making timely payments. Furthermore, it can sometimes result in a slightly better interest rate, as the loan-to-value (LTV) ratio is more favorable for the lender.

From a professional perspective, a substantial down payment is often the game-changer for individuals with poor credit. It provides a tangible demonstration of your financial commitment and helps bridge the gap created by your credit score. Aim for at least 10-20% of the vehicle’s purchase price, if possible.

3.2. Enlist a Co-Signer

Another powerful strategy to bolster your application is to apply with a co-signer who has good credit. A co-signer essentially pledges their own creditworthiness and financial stability to guarantee the loan if you default. Their good credit history can significantly improve your chances of approval and potentially secure a more favorable interest rate.

However, choosing a co-signer is a serious decision with significant implications for both parties. Your co-signer becomes equally responsible for the loan. If you miss payments, it negatively impacts both your credit scores, and the lender can pursue payment from them.

It’s crucial to have an open and honest conversation with any potential co-signer about the responsibilities and risks involved. Ensure they fully understand what they are signing up for, and only consider someone you trust implicitly and who trusts you in return.

3.3. Choose the Right Vehicle

When you have a 500 credit score, this is not the time to aspire to a brand-new luxury vehicle. Your focus should be on securing reliable transportation that is affordable. Opting for a more modest, reliable used car can dramatically improve your approval odds.

A lower-priced vehicle means you’re asking to borrow a smaller amount of money, which again reduces the risk for the lender. Additionally, a car that holds its value well is often preferred by lenders, as it provides better collateral in case of default.

Pro tips from us: Research affordable, fuel-efficient models known for their longevity and lower maintenance costs. Focus on function and necessity over features and luxury. This pragmatic approach is key when seeking a car loan 500 credit.

3.4. Demonstrate Income Stability

Lenders want assurance that you have the consistent financial capacity to make your monthly loan payments. Demonstrating a stable employment history and a reliable income stream is paramount. Even with a low credit score, proof of steady income can significantly sway a lender’s decision.

Be prepared to provide documentation such as recent pay stubs, W-2s, bank statements, and potentially even employment verification letters. The longer you’ve been at your current job, the better. Any gaps in employment or frequent job changes can raise red flags for lenders.

Consistency is key here. Lenders are looking for a pattern of financial reliability, even if your credit history has some bumps.

3.5. Address Your Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is a crucial metric lenders evaluate. It compares your total monthly debt payments to your gross monthly income. A high DTI indicates that a significant portion of your income is already allocated to existing debts, leaving less for a new car payment.

Lenders prefer a lower DTI, typically under 43%, as it suggests you have more disposable income to manage additional debt. Before applying for a car loan, try to pay down some existing debts, especially those with high monthly payments. Even a small reduction can make a difference.

For more detailed advice on managing your credit and reducing your DTI, check out our guide on . Understanding and improving your DTI can make your application much more attractive to lenders.

4. Navigating the Lender Landscape for Bad Credit Car Loans

Not all lenders are created equal, especially when it comes to financing for individuals with challenging credit. Knowing where to look and what to expect from different types of lenders is crucial for securing a car loan 500 credit.

4.1. Specialized Bad Credit Lenders

These lenders, sometimes referred to as subprime lenders, specialize in working with borrowers who have low credit scores. Their business model is built around assessing higher risk, which means they are more likely to approve your application. However, this often comes at the cost of higher interest rates.

You’ll find these lenders both online and through finance companies that partner with dealerships. It’s essential to research them thoroughly, read reviews, and compare offers. Be wary of any lender that promises "guaranteed approval" without any credit check, as this can be a sign of a predatory loan.

While they offer a solution, these lenders should be approached with caution and a clear understanding of the terms they offer.

4.2. Dealerships with In-House Financing (Buy Here, Pay Here)

"Buy Here, Pay Here" dealerships offer their own financing directly to customers, often without relying on external banks or credit scores. The primary benefit is that they are often the easiest place to get approved for a car loan 500 credit, as they focus more on your income stability than your credit history.

However, there are significant drawbacks. These dealerships typically charge very high interest rates, sometimes reaching the maximum legal limit. Their vehicle selection might be limited, and the cars may be older or have higher mileage. A common mistake people make is jumping into a Buy Here, Pay Here deal without understanding the full cost and impact on their credit rebuilding journey.

Furthermore, some of these dealerships do not report payments to credit bureaus. While this means missed payments won’t hurt your score, it also means timely payments won’t help you rebuild it, which is a major missed opportunity.

4.3. Credit Unions

Credit unions are member-owned financial institutions that often offer more flexible lending criteria than traditional banks, especially for their members. If you’re a member of a credit union, or eligible to join one, it’s worth exploring their auto loan options.

They are known for being more understanding of individual circumstances and may be willing to work with members who have a 500 credit score, especially if you have a long-standing relationship with them. While rates may still be higher than for excellent credit, they could be more favorable than those from specialized subprime lenders.

5. The Application Process: What to Expect

Once you’ve identified potential lenders and prepared your financial situation, it’s time to navigate the application process. Knowing what to expect can help you feel more confident and prepared.

5.1. Gather Your Documents

Preparation is key. Lenders will require a range of documents to verify your identity, income, and residence. This typically includes a valid driver’s license, proof of income (pay stubs, W-2s, tax returns for self-employed), proof of residence (utility bill, lease agreement), and potentially references.

Having all these documents organized and ready will streamline the application process and demonstrate your seriousness to the lender. It also minimizes delays, which can be frustrating for both parties.

5.2. Pre-Qualification vs. Full Application

It’s important to understand the difference between pre-qualification and a full loan application. Pre-qualification often involves a "soft inquiry" on your credit report, which doesn’t affect your credit score. It gives you an estimate of what you might qualify for, including potential interest rates.

A full application, on the other hand, involves a "hard inquiry," which can temporarily lower your credit score by a few points. Pro tips from us: Always try to pre-qualify with several lenders first. This allows you to compare offers without accumulating multiple hard inquiries, helping you find the best terms for your car loan 500 credit.

5.3. Understanding the Loan Terms

Before you sign any agreement, thoroughly understand all aspects of the loan terms. The Annual Percentage Rate (APR) is the most critical figure, as it represents the true annual cost of borrowing, including interest and certain fees. With a 500 credit score, be prepared for a high APR.

Also, pay close attention to the loan term – the length of time you have to repay the loan. While longer terms mean lower monthly payments, they significantly increase the total amount of interest you’ll pay over time. Always calculate the total cost of the loan by multiplying your monthly payment by the number of months in the term. This will reveal the true financial burden.

Never sign anything until you’ve thoroughly reviewed the APR and calculated the total cost over the loan term. It’s often much higher than people anticipate with a car loan 500 credit, and understanding this upfront is essential.

6. Pitfalls to Avoid When Seeking a Car Loan with 500 Credit

Navigating the world of subprime auto loans requires vigilance. Unfortunately, there are unscrupulous practices and common mistakes that can trap vulnerable borrowers. Being aware of these pitfalls can save you significant financial heartache.

6.1. Excessive Interest Rates

As mentioned, high interest rates are a reality with a 500 credit score. However, there’s a difference between a high rate and a predatory one. Always compare offers from multiple lenders. If an interest rate seems excessively high, even for bad credit, it’s worth questioning.

Don’t let desperation lead you to accept any offer. Shopping around is your best defense against being exploited. Even a few percentage points difference in APR can save you thousands over the life of the loan.

6.2. Loan Scams

Be extremely cautious of loan scams that target individuals with bad credit. Warning signs include guaranteed approval without any credit check, requests for upfront fees before receiving any funds, or high-pressure tactics that rush you into signing. Reputable lenders will always perform a credit check and will not ask for money upfront to "process" your loan.

For more information on identifying and avoiding loan scams, consult trusted resources like the Consumer Financial Protection Bureau (CFPB) website. Staying informed is your best protection against fraudulent schemes.

6.3. Ignoring the Fine Print

Every loan document contains fine print for a reason. It outlines all the terms, conditions, fees, and penalties associated with your loan. Common mistakes we’ve observed people make include failing to read or understand these crucial details. This can lead to unexpected charges, penalties for early repayment, or hidden fees.

Take your time to read every single page of the loan agreement. If you don’t understand something, ask for clarification. Don’t be afraid to ask for a copy of the agreement to review at home or even to have a trusted advisor look over it before you sign.

6.4. Stretching the Loan Term Too Long

While a longer loan term (e.g., 72 or 84 months) can make monthly payments seem more affordable, it comes at a significant cost. You’ll end up paying far more in total interest over the life of the loan. Moreover, it increases the risk of becoming "upside down" on your loan, meaning you owe more than the car is worth.

This can happen quickly, especially with a depreciating asset like a car. If you need to sell the car or it’s totaled, you could be left owing money on a vehicle you no longer own. To delve deeper into the long-term financial implications of different loan terms, consider reading our article on . Aim for the shortest loan term you can realistically afford.

7. Beyond the Loan: Rebuilding Your Credit

Securing a car loan 500 credit shouldn’t be the end goal; it should be a stepping stone towards improving your overall financial health. A successfully managed auto loan can be a powerful tool for rebuilding your credit score and opening doors to better financial opportunities in the future.

7.1. Make Payments On Time, Every Time

This is arguably the most critical step. Your payment history accounts for the largest portion of your credit score. Every on-time payment you make demonstrates responsible financial behavior and will gradually improve your score. Set up automatic payments or calendar reminders to ensure you never miss a due date.

7.2. Keep Credit Utilization Low

While your auto loan is a fixed installment loan, managing your revolving credit (credit cards) is also important. Keep your credit card balances low, ideally below 30% of your credit limit. High utilization can negatively impact your score, even if you’re making car payments on time.

7.3. Monitor Your Credit Score

Regularly check your credit report and score. Many credit card companies and online services offer free credit score monitoring. This allows you to track your progress, identify any potential errors on your report, and see the positive impact of your diligent payments. Seeing your score improve can be incredibly motivating.

Conclusion

The journey to securing a car loan 500 credit can feel daunting, but it is absolutely achievable with a strategic approach, thorough preparation, and realistic expectations. By understanding what your credit score signifies, implementing smart strategies like a substantial down payment or a co-signer, and diligently avoiding common pitfalls, you can significantly increase your chances of approval.

Remember, this loan isn’t just about getting a car; it’s an opportunity to rebuild your financial standing. By making timely payments and managing your other debts responsibly, your new car loan can become a catalyst for a stronger credit profile. Empower yourself with knowledge, make informed decisions, and embark on your journey towards not just a new vehicle, but also a brighter financial future.