Unmasking the True Cost: How Much Will I Pay In Interest On My Car Loan?

Unmasking the True Cost: How Much Will I Pay In Interest On My Car Loan? Carloan.Guidemechanic.com

Buying a new or used car is an exciting milestone, often one of the biggest purchases we make after a home. While the thrill of a new ride is undeniable, many drivers overlook a critical component of their car loan: the interest. It’s not just about the monthly payment; it’s about understanding the total cost, and a significant chunk of that total is the interest you’ll pay over the life of the loan.

As an expert blogger and SEO content writer with years of experience navigating the complexities of personal finance, I’ve seen firsthand how easily consumers can get lost in the jargon. This comprehensive guide is designed to demystify car loan interest, helping you understand exactly how much you might pay, why, and crucially, how you can minimize that cost. We’ll delve deep into the mechanics, reveal the factors at play, and equip you with strategies to make smarter financial decisions.

Unmasking the True Cost: How Much Will I Pay In Interest On My Car Loan?

The Foundation: What Exactly Is Car Loan Interest?

Before we can calculate "how much will I pay in interest car loan," we need a clear definition. Simply put, interest is the cost of borrowing money. When you take out a car loan, a lender provides you with the funds to purchase your vehicle, and in return, you agree to pay back the original amount (the principal) plus an additional fee – the interest.

This fee compensates the lender for the risk they take by lending you money and for the opportunity cost of not using those funds elsewhere. It’s essentially their profit margin for providing the service. Without interest, lenders wouldn’t have a sustainable business model.

Understanding this fundamental concept is the first step toward becoming a savvy car buyer. It moves you beyond just looking at the sticker price and helps you grasp the full financial commitment.

Principal vs. Interest: A Crucial Distinction

Every car loan payment you make consists of two main components: a portion that goes towards reducing your principal and a portion that covers the interest. The principal is the original amount of money you borrowed to buy the car.

Initially, a larger percentage of your monthly payment goes towards interest, especially in the early stages of an amortized loan. As you continue to make payments, the outstanding principal balance decreases, and consequently, a greater portion of each subsequent payment is applied to the principal. This shift means you build equity in your car more quickly towards the end of your loan term.

The Major Players: Factors That Dictate Your Car Loan Interest

The question of "how much will I pay in interest car loan" doesn’t have a single answer because numerous variables come into play. Each factor can significantly influence the interest rate you qualify for and, by extension, the total amount of interest you’ll pay over time. Let’s break down the most impactful elements.

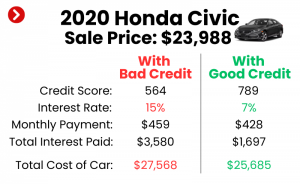

Your Credit Score: The Ultimate Game Changer

Your credit score is arguably the most critical determinant of the interest rate you’ll receive. It’s a three-digit number that reflects your creditworthiness – essentially, how reliable you are at repaying debts. Lenders use this score to assess the risk associated with lending you money.

A high credit score (typically above 700) indicates a low risk, leading lenders to offer more favorable interest rates. Conversely, a lower credit score suggests a higher risk, prompting lenders to charge higher interest rates to compensate for the increased potential of default. Based on my experience, consistently maintaining a good credit score is the single most effective way to secure a lower interest rate on any loan, including a car loan.

The Loan Term: Length Matters More Than You Think

The loan term, or the length of time you have to repay the loan, directly impacts both your monthly payment and the total interest paid. Common car loan terms range from 36 months to 84 months, or even longer in some cases.

While a longer loan term (e.g., 72 or 84 months) might offer a lower monthly payment, making the car seem more affordable, it almost always results in paying significantly more interest over the life of the loan. This is because the interest accrues for a longer period. Pro tips from us: always consider the total cost, not just the monthly installment, when choosing a loan term.

The Loan Amount (Principal): More Borrowed, More Interest

This factor is straightforward: the more money you borrow, the more interest you will pay, assuming the interest rate remains constant. A higher principal balance means a larger sum on which the interest rate is applied.

Therefore, reducing the amount you need to borrow is a powerful strategy for cutting down on total interest. This can be achieved through a larger down payment or by choosing a less expensive vehicle.

Your Down Payment: A Powerful Shield Against Interest

Making a substantial down payment is one of the smartest financial moves you can make when buying a car. A down payment directly reduces the principal amount you need to borrow. Less principal means less interest will accrue over the life of the loan.

Furthermore, a larger down payment can sometimes signal to lenders that you are a lower-risk borrower, potentially helping you qualify for a slightly better interest rate. It also provides you with instant equity in your vehicle, protecting you against depreciation.

The Type of Interest Rate: Fixed vs. Variable

For car loans, the vast majority are offered with a fixed interest rate. This means your interest rate remains constant throughout the entire loan term, providing predictable monthly payments. This is generally preferred by consumers as it offers stability and makes budgeting easier.

While less common, some lenders might offer variable interest rates, which can fluctuate based on market conditions. If the rate increases, your payments could go up, leading to more total interest. Common mistakes to avoid are not confirming whether your rate is fixed or variable before signing.

New vs. Used Car: Often Different Rate Structures

Lenders often apply different interest rates to new versus used cars. Generally, new cars tend to have slightly lower interest rates than used cars. This is partly due to the perception of lower risk for new vehicles (less chance of immediate mechanical issues) and sometimes due to manufacturer incentives.

However, a used car’s lower purchase price often means a lower principal amount, which can still lead to less total interest paid despite a potentially higher rate. It’s a balance between the rate and the amount borrowed.

Lender Type and Market Conditions

Where you get your loan from can also impact the rate. Banks, credit unions, and dealership financing arms all have different lending criteria and competitive rates. Credit unions, being not-for-profit, often offer some of the most competitive rates.

Beyond individual factors, broader economic market conditions, such as the Federal Reserve’s interest rate policies, influence the general cost of borrowing across the board. When interest rates are low nationwide, car loan rates tend to follow suit.

Calculating Your Car Loan Interest: A Practical Approach

So, how do we actually figure out "how much will I pay in interest car loan"? While the exact calculation for an amortized loan can be complex, understanding the basic principle and utilizing readily available tools makes it accessible.

Most car loans use a simple interest calculation method applied to the remaining principal balance. Each month, interest is calculated on the outstanding principal before your payment is applied.

The Amortization Schedule: Your Loan’s Roadmap

An amortization schedule is a table detailing each payment over the life of your loan. It breaks down how much of each payment goes toward interest and how much goes toward principal, along with your remaining balance.

In the initial months, a larger portion of your payment covers the interest, while less goes towards the principal. As time progresses, this ratio gradually shifts, with more of your payment attacking the principal. This structure is crucial to understanding the total interest burden.

Using Online Car Loan Calculators: Your Best Friend

The easiest and most accurate way to estimate your total interest is by using an online car loan calculator. These tools are widely available on bank websites, financial blogs, and independent finance sites. You simply input the loan amount, interest rate, and loan term, and the calculator instantly provides your estimated monthly payment and the total interest you’ll pay.

Pro Tip: Play around with different scenarios on these calculators. See how increasing your down payment, shortening your loan term, or securing a lower interest rate dramatically changes the "total interest paid" figure. This visual representation can be incredibly enlightening.

A Simple Example for Illustration:

Let’s imagine you’re considering a loan for $25,000 at an interest rate of 6% over a 60-month (5-year) term.

- Using an online calculator, your estimated monthly payment would be around $483.32.

- Over 60 months, you would pay a total of $483.32 * 60 = $28,999.20.

- The total interest paid would be $28,999.20 (total paid) – $25,000 (principal) = $3,999.20.

Now, what if you got a 4% interest rate instead?

- Monthly payment: ~$460.40

- Total paid: $460.40 * 60 = $27,624

- Total interest paid: $27,624 – $25,000 = $2,624.

That’s a savings of over $1,300 just by securing a 2% lower interest rate! This clearly illustrates the power of understanding and influencing these factors.

The True Cost of Your Car Loan: Beyond the Sticker Price

Many car buyers focus solely on the monthly payment, often stretching the loan term to achieve a lower figure. However, this narrow focus can lead to significantly higher overall costs. The true cost of your car loan isn’t just the purchase price; it’s the principal plus the total interest paid over the loan’s duration.

Ignoring the total interest means you’re not fully grasping the financial commitment. A car that seems affordable with a low monthly payment over 7 or 8 years might end up costing you thousands more in interest than a slightly higher monthly payment over 4 or 5 years. This "hidden" cost is what catches many consumers by surprise.

Strategies to Significantly Reduce the Interest You Pay

Empowering yourself with knowledge about "how much will I pay in interest car loan" is only half the battle. The other half is taking proactive steps to minimize that interest. Here are some proven strategies:

1. Improve Your Credit Score Before Applying

As discussed, your credit score is paramount. Before you even step foot in a dealership or apply for a loan, check your credit report. Dispute any errors and work on improving your score. This might involve paying down existing debts, making all payments on time, and avoiding opening new credit accounts.

A strong credit score can unlock access to the lowest advertised interest rates. Even a small improvement can make a difference in your total interest. For a deeper dive, consider reading our article: Understanding Your Credit Score: A Comprehensive Guide.

2. Make the Largest Down Payment You Can Afford

Every dollar you put down upfront is a dollar you don’t have to borrow and, therefore, a dollar on which you won’t pay interest. Aim for at least 10-20% of the car’s purchase price if possible.

A substantial down payment also reduces your risk of being "upside down" on your loan, where you owe more than the car is worth. This is particularly important with new cars that depreciate rapidly.

3. Choose the Shortest Loan Term You Can Comfortably Afford

While a longer term means lower monthly payments, it also means more interest. Challenge yourself to take on the shortest loan term that fits your budget.

For example, a 48-month loan will almost always result in significantly less total interest paid than a 72-month loan, even if the monthly payment is a bit higher. It’s a trade-off that often saves you thousands.

4. Shop Around and Compare Offers from Multiple Lenders

Never accept the first loan offer you receive, especially from a dealership. Dealerships often mark up interest rates as an additional profit center. Pro tips from us: get pre-approved for a loan from a bank, credit union, or online lender before you visit the dealership.

This pre-approval gives you a benchmark. You can then use it as leverage to negotiate a better rate with the dealership’s financing department. Having multiple offers in hand puts you in a much stronger negotiating position.

5. Consider Refinancing Your Car Loan

If you already have a car loan but your credit score has improved, or market rates have dropped since you took out the loan, refinancing could save you money. Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or a more favorable term.

This strategy can reduce your monthly payments and/or the total interest paid. To learn more about this option, check out our detailed article: Refinancing Your Car Loan: Is It Right For You?.

6. Make Extra Payments Whenever Possible

Even small extra payments can have a significant impact on reducing your total interest. When you make an extra payment, specify that you want it applied directly to the principal. This reduces the outstanding balance on which future interest is calculated.

You can do this by rounding up your monthly payment, making a bi-weekly payment, or applying unexpected windfalls like tax refunds or bonuses directly to your loan principal.

7. Avoid Financing Unnecessary Add-ons

Dealerships often offer various add-ons like extended warranties, rustproofing, paint protection, or gap insurance. While some of these might be valuable, financing them into your car loan means you’re paying interest on them for the entire loan term.

If you want these extras, try to pay for them upfront in cash. If you must finance them, understand the additional interest cost they will incur.

Common Mistakes to Avoid When Getting a Car Loan

Understanding "how much will I pay in interest car loan" also means recognizing pitfalls. Common mistakes to avoid are those that can needlessly inflate your interest costs and lead to financial strain.

- Focusing Only on the Monthly Payment: This is perhaps the biggest pitfall. A low monthly payment achieved by stretching the loan term can hide a much higher total interest cost. Always ask for the total cost of the loan.

- Not Checking Your Credit Score: Going into a loan application blind is a mistake. Knowing your score allows you to anticipate offers and correct errors beforehand.

- Skipping the Down Payment: While sometimes unavoidable, making no down payment means financing 100% of the car, leading to maximum interest charges and negative equity.

- Accepting the First Loan Offer: Especially from the dealership. Always compare offers to ensure you’re getting a competitive rate.

- Financing Too Many Extras: As mentioned, rolling warranties and other add-ons into your loan increases the principal and, consequently, the interest you pay on those items.

- Ignoring the Fine Print: Always read your loan agreement carefully. Understand all fees, prepayment penalties (rare for car loans but worth checking), and terms before signing.

Real-World Scenarios: Putting It All Together

Let’s illustrate with two different car loan scenarios to highlight the impact of the factors we’ve discussed. Both scenarios are for a $30,000 car purchase.

Scenario A: Less Prepared Buyer

- Loan Amount: $30,000 (no down payment)

- Credit Score: Average (650-699)

- Interest Rate: 8%

-

Loan Term: 72 months (6 years)

- Estimated Monthly Payment: ~$540

- Total Paid Over Loan Term: $38,880

- Total Interest Paid: $8,880

Scenario B: Savvy Buyer

- Loan Amount: $24,000 (after $6,000 / 20% down payment)

- Credit Score: Excellent (750+)

- Interest Rate: 4%

-

Loan Term: 48 months (4 years)

- Estimated Monthly Payment: ~$546

- Total Paid Over Loan Term: $26,208

- Total Interest Paid: $2,208

Notice how the savvy buyer has a slightly higher monthly payment but saves a whopping $6,672 in total interest! This difference is a powerful testament to the importance of a down payment, a good credit score, and a shorter loan term.

Empowering Your Car Buying Journey

Understanding "how much will I pay in interest car loan" is not just about crunching numbers; it’s about making informed, financially sound decisions that benefit your long-term wealth. Interest can be a silent wealth killer if not managed properly, or a manageable cost if approached strategically.

By focusing on your credit score, making a solid down payment, choosing an appropriate loan term, and diligently shopping for the best rates, you can significantly reduce the amount of interest you pay. Remember, knowledge is power, and in the world of car loans, it translates directly into savings.

Take the time to educate yourself, compare offers, and don’t be afraid to negotiate. Your wallet will thank you for it. For additional resources and tools, you can always consult reputable sources like the Consumer Financial Protection Bureau’s Guide to Auto Loans to further enhance your financial literacy. Make your next car purchase not just exciting, but also financially smart.