Unpacking 9% APR for Your Car Loan: Is It a Good Deal? (2024 Expert Guide)

Unpacking 9% APR for Your Car Loan: Is It a Good Deal? (2024 Expert Guide) Carloan.Guidemechanic.com

The journey to buying a new or used car often brings us face-to-face with a sea of numbers, and among the most critical is the Annual Percentage Rate (APR) of your loan. For many car buyers, an offer of 9% APR might appear on the table, sparking a fundamental question: "Is 9% APR good for a car loan?" This isn’t a simple yes or no answer; rather, it’s a nuanced discussion influenced by a myriad of personal financial factors, market conditions, and the specifics of the loan itself.

As an expert blogger and professional SEO content writer, I’ve seen countless individuals navigate this very question. My mission here is to dissect what 9% APR truly means for your car loan, provide a comprehensive framework for evaluating its competitiveness, and equip you with the knowledge to secure the best possible financing for your next vehicle. Let’s dive deep into understanding this pivotal figure and how it impacts your wallet.

Unpacking 9% APR for Your Car Loan: Is It a Good Deal? (2024 Expert Guide)

What Exactly is 9% APR? Demystifying the Rate

Before we can judge whether 9% APR is "good," we first need a clear understanding of what APR represents. APR, or Annual Percentage Rate, is more than just the interest rate; it’s the total cost of borrowing money each year, expressed as a percentage. This means it encompasses not only the interest charged on your principal loan amount but also any additional fees associated with the loan, such as administrative fees or origination charges.

When a lender offers you a 9% APR, they are essentially telling you that the total cost of borrowing will be 9% of the principal loan amount, calculated annually, including all charges. This figure directly influences your monthly payment and, crucially, the total amount you will repay over the life of the loan. A higher APR means a higher overall cost of borrowing, while a lower APR translates to less money paid back to the lender.

For example, consider a $25,000 car loan at 9% APR over 60 months. Your monthly payment would be approximately $518. Over the five-year term, you would pay back a total of around $31,080, meaning roughly $6,080 in interest and fees. Understanding this direct impact on your financial outlay is the first step in evaluating any loan offer.

Is 9% APR "Good" for a Car Loan? The Million-Dollar Question

The core of our discussion revolves around whether 9% APR is a favorable rate. The honest answer, based on extensive experience, is that it depends entirely on your unique financial situation, current market conditions, and the specifics of the loan. There’s no universal "good" or "bad" stamp that applies to every borrower.

Let’s break down the scenarios where 9% APR might be considered acceptable, and conversely, where it’s likely too high.

When 9% APR Might Be Considered Acceptable or Even "Good"

For certain borrowers and under specific market conditions, a 9% APR could be a reasonable offer.

- Average to Below-Average Credit Score: If your FICO credit score falls into the "average" range (typically 600-660) or even slightly below, 9% APR might be among the more competitive rates you’ll receive. Lenders perceive these scores as carrying a higher risk, and they compensate for that risk with a higher interest rate.

- Limited Credit History: Young buyers or those new to credit often haven’t established a robust credit profile. Without a lengthy history of responsible borrowing, lenders view them as higher risk, making a 9% APR a common starting point for car loans.

- High Market Interest Rates: The overall economic landscape plays a significant role. If the Federal Reserve has recently raised interest rates, the average APR for car loans across the board will increase. In such a high-rate environment, 9% might be closer to the national average than it would be during periods of low interest rates.

- Used Car Loans: Generally, used car loans tend to have higher interest rates than new car loans. This is because used vehicles are perceived as having a higher risk of mechanical issues and quicker depreciation, making them less secure collateral for the lender. If you’re financing an older used car, 9% might be typical.

- Longer Loan Terms: Sometimes, borrowers opt for longer loan terms (e.g., 72 or 84 months) to reduce their monthly payments. Lenders might offer a slightly higher APR for these extended terms due to the increased risk over a longer period.

Pro Tip from us: Always compare your offered rate with national averages for your specific credit tier and vehicle type. Websites like Experian or Bankrate often publish these averages, providing a crucial benchmark.

When 9% APR Is Likely Too High

Conversely, for many, 9% APR would be considered a high rate, indicating room for improvement.

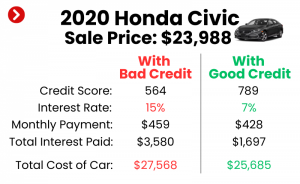

- Excellent Credit Score: If you boast an excellent credit score (typically 700+ FICO), a 9% APR is almost certainly too high. Borrowers with strong credit profiles should aim for significantly lower rates, often in the 3-6% range, depending on market conditions. Lenders are eager to attract low-risk borrowers and will offer better terms.

- New Car Loans: New car financing generally comes with lower interest rates due to the vehicle’s higher value, warranty, and lower perceived risk. A 9% APR on a brand-new vehicle is usually not competitive for most borrowers.

- Low Market Interest Rates: If the economy is in a period of low interest rates, 9% APR would be considered exceptionally high for most qualified borrowers. This indicates you might not have shopped around enough or there might be an issue with your credit profile that needs addressing.

- Short Loan Terms: For shorter loan durations (e.g., 36 or 48 months), lenders typically offer lower APRs because their risk exposure is reduced. If you’re getting 9% for a short term, it’s worth investigating why.

Common mistakes to avoid are accepting the first offer without comparison and not understanding your own credit standing before applying. Knowledge is power in loan negotiations.

Key Factors Influencing Your Car Loan APR

To truly understand why you might be offered 9% APR, or how to get a better rate, it’s essential to grasp the key determinants of car loan interest rates.

- Your Credit Score and History: This is, without a doubt, the single most significant factor. A higher credit score (indicating a history of responsible borrowing and repayment) signals lower risk to lenders, resulting in lower APRs. Conversely, a lower score or a history of missed payments will push your rate higher.

- Based on my experience, borrowers often underestimate the direct impact their credit score has on the total cost of their car. Even a 50-point increase can translate to thousands saved.

- Debt-to-Income (DTI) Ratio: Lenders look at how much of your monthly income goes towards debt payments. A high DTI ratio suggests you might be overextended, increasing the perceived risk and potentially leading to a higher APR.

- Loan Term: The length of your repayment period plays a crucial role. Shorter loan terms (e.g., 36 or 48 months) generally come with lower APRs because the lender’s money is at risk for a shorter period. Longer terms (e.g., 72 or 84 months) often carry higher APRs.

- Loan-to-Value (LTV) Ratio & Down Payment: The LTV ratio compares the loan amount to the car’s value. A larger down payment reduces the loan amount, lowering the LTV, and demonstrating your commitment. This reduces the lender’s risk and can help secure a lower APR.

- New vs. Used Car: As mentioned, new car loans typically have lower rates than used car loans. New cars depreciate slower initially, have warranties, and are generally less risky for lenders.

- Market Interest Rates: The broader economic environment, particularly the Federal Reserve’s benchmark interest rates, significantly influences auto loan rates. When the Fed raises rates, car loan APRs tend to follow suit.

- Lender Type: Different lenders have different risk appetites and rate structures.

- Banks: Traditional banks offer competitive rates, especially to their existing customers.

- Credit Unions: Often known for offering some of the lowest rates due to their member-owned structure.

- Online Lenders: Can provide quick approvals and competitive rates, with a wide range of options.

- Dealership Financing: Convenient, but sometimes marked up by the dealer for profit. It’s crucial to compare.

How to Potentially Get a Better Car Loan Rate (Beyond 9% APR)

If you’re facing a 9% APR offer and believe you deserve better, or simply want to optimize your financial outcome, there are several powerful strategies you can employ.

- Improve Your Credit Score: This is a long-term strategy but incredibly impactful.

- Pay all your bills on time, every time. Payment history is the biggest factor in your score.

- Reduce outstanding debt, especially on credit cards, to lower your credit utilization.

- Check your credit report for errors and dispute any inaccuracies.

- Avoid opening too many new credit accounts in a short period.

- Shop Around Extensively for Lenders: This is perhaps the single most effective immediate step you can take.

- Don’t just rely on the dealership’s financing. Apply to multiple banks, credit unions, and online lenders.

- Get pre-approved from several sources before you even step foot in a dealership. This gives you leverage and a clear benchmark.

- Based on my experience, having a pre-approval in hand can save you thousands. It shifts the power dynamic from the dealer to you.

- Make a Larger Down Payment: The more money you put down upfront, the less you need to borrow. This reduces the loan amount and the lender’s risk, often leading to a lower APR. A 20% down payment is often recommended.

- Choose a Shorter Loan Term: If your budget allows for higher monthly payments, opting for a shorter loan term (e.g., 48 or 60 months instead of 72 or 84) can significantly lower your APR and the total interest paid.

- Consider a Co-signer: If your credit isn’t ideal, but you have a trusted friend or family member with excellent credit, they could co-sign the loan. Their strong credit profile can help you qualify for a much lower APR. Be aware that the co-signer is equally responsible for the debt.

- Negotiate with the Dealership: Armed with pre-approvals from other lenders, you can negotiate with the dealership’s finance department. They might be able to match or even beat external offers to secure your business.

- Refinance Your Loan Later: Even if 9% APR is the best you can get now, it doesn’t have to be forever. If your credit improves, market rates drop, or your financial situation stabilizes, you can explore refinancing your car loan for a lower APR down the line. Many lenders offer competitive refinancing options.

Understanding the True Cost of a 9% APR Loan

It’s easy to focus solely on the monthly payment, but the true cost of a loan lies in the total amount you pay back over its lifetime. A seemingly small difference in APR can translate into thousands of dollars.

Let’s illustrate with an example:

- Loan Amount: $30,000

- Loan Term: 60 months (5 years)

Scenario A: 9% APR

- Monthly Payment: Approximately $622.75

- Total Paid: $37,365

- Total Interest Paid: $7,365

Scenario B: 5% APR (A rate you might achieve with excellent credit)

- Monthly Payment: Approximately $566.14

- Total Paid: $33,968.40

- Total Interest Paid: $3,968.40

As you can see, the difference between 9% and 5% APR on a $30,000 loan over 5 years is a staggering $3,396.60 in interest alone. This nearly $3,400 could be used for other financial goals, like investments, savings, or even a down payment on your next car.

Common mistakes to avoid are not calculating the total interest over the loan’s life and only focusing on the monthly payment. A lower monthly payment achieved by stretching the loan term or accepting a higher APR often means paying significantly more in the long run. Always ask for the total cost of the loan.

When a 9% APR Might Be Your Best Option (And What to Do Then)

It’s crucial to acknowledge that despite your best efforts, 9% APR might genuinely be the most favorable rate available to you at a particular moment. This isn’t a failure; it’s a reality for many borrowers.

Scenarios where 9% APR might be your best bet:

- Recent Credit Challenges: If you’ve recently experienced bankruptcy, foreclosure, or a series of late payments, your credit score will reflect this. Lenders will be hesitant to offer prime rates, and 9% might be a step toward rebuilding your credit.

- Very Limited Credit History: As mentioned, if you’re just starting out with credit, lenders have little data to assess your risk, making higher rates common.

- Urgent Need for a Vehicle: Sometimes, you simply need a car for work, family, or essential transportation, and you can’t wait to improve your credit or shop for months. In such cases, securing transportation might take precedence over an ideal interest rate.

What to do if 9% is your best offer:

If 9% APR is the best rate you can secure, here’s how to manage it strategically:

- Maximize Your Down Payment: Even if you can’t get a lower rate, reducing the principal loan amount through a larger down payment will decrease the total interest you pay. Every dollar you put down is a dollar you don’t borrow at 9%.

- Keep the Loan Term as Short as Possible: While it might mean a higher monthly payment, a shorter loan term will significantly reduce the total interest paid at 9% APR. Don’t stretch the term excessively just to lower your payment.

- Prioritize Credit Improvement: Make a concerted effort to improve your credit score during the loan term. Pay all bills on time, keep credit card balances low, and regularly check your credit report.

- Plan to Refinance: Once your credit score improves (typically after 6-12 months of consistent, on-time payments) or if market rates drop, actively seek to refinance your car loan. This could potentially lower your APR significantly, saving you substantial money over the remaining loan term. Consider checking out resources on car loan refinancing strategies to prepare for this step.

- Budget Diligently: With a 9% APR, your interest payments will be higher. Create a strict budget to ensure you can comfortably meet your monthly payments and avoid further credit issues.

Conclusion: Making an Informed Decision About 9% APR

Ultimately, whether 9% APR is "good" for your car loan is a highly personal determination. It’s not about a fixed number but about context, comparison, and your individual financial standing. For some, it might represent a fair deal given their credit profile or current market conditions. For others with strong credit, it’s a clear signal to keep shopping.

The key takeaway is empowerment through knowledge. By understanding what APR means, recognizing the factors that influence your rate, and proactively implementing strategies to secure better terms, you place yourself in the driver’s seat of your financial future. Always shop around, compare offers, and never hesitate to negotiate. Your car loan is a significant financial commitment, and making an informed decision about your APR is paramount to saving money and achieving your financial goals.

Start comparing rates today and take control of your car buying journey!