Unraveling the Average Car Loan Term: Your Definitive Guide to Smarter Financing

Unraveling the Average Car Loan Term: Your Definitive Guide to Smarter Financing Carloan.Guidemechanic.com

The excitement of a new car is undeniable. That fresh scent, the sleek design, the promise of new adventures on the open road – it’s a powerful feeling. However, beneath the gloss and thrill lies a crucial financial decision that will impact your budget for years to come: the car loan. Specifically, understanding the average car loan term is paramount.

This isn’t just about the monthly payment; it’s about the total cost of ownership, your financial flexibility, and even your peace of mind. As an expert blogger and professional SEO content writer, I’ve delved deep into the nuances of auto financing. My mission today is to equip you with a comprehensive understanding of car loan terms, moving beyond mere statistics to empower you with truly informed choices.

Unraveling the Average Car Loan Term: Your Definitive Guide to Smarter Financing

Choosing the right car loan term is more than just picking a number; it’s about aligning your vehicle purchase with your long-term financial goals. Let’s explore everything you need to know to navigate this critical aspect of car buying.

What Exactly is a Car Loan Term?

At its core, a car loan term refers to the duration, typically expressed in months, over which you agree to repay the money borrowed to purchase a vehicle. Think of it as the timeline for your financial commitment. This period dictates how long you’ll be making regular payments to your lender until the car is fully yours.

Common car loan terms range from 36 months (three years) to 84 months (seven years), and sometimes even longer. Each option comes with its own set of financial implications, directly affecting both your monthly budget and the total amount you’ll ultimately pay for the car. Understanding this fundamental concept is the first step toward smart auto financing.

The Evolving Landscape of the Average Car Loan Term

When we talk about the "average" car loan term, we’re looking at a dynamic figure that reflects current market conditions, vehicle prices, and consumer financial habits. Historically, 48 or 60 months were considered standard. However, in recent years, this average has been steadily increasing.

Based on my experience tracking auto finance trends, it’s clear that longer loan terms, particularly 72 and even 84 months, have become increasingly prevalent. This shift is largely driven by the rising cost of new vehicles, pushing consumers to seek lower monthly payments to fit cars into their budgets. While a lower monthly payment can seem appealing, it often masks a higher total cost over the life of the loan.

This extended average term isn’t just a number; it represents a significant change in how people finance their vehicles. It highlights the importance of looking beyond the monthly payment to the bigger financial picture.

Key Factors Influencing Your Car Loan Term

Several critical factors come into play when determining the appropriate or available car loan term for your situation. These elements intertwine to shape not only the length of your loan but also the interest rate you qualify for. Understanding them is crucial for negotiating the best possible deal.

1. The Vehicle’s Price Tag

Perhaps the most obvious factor is the cost of the car itself. As vehicle prices continue to climb, especially for new models equipped with advanced technology, consumers often gravitate towards longer loan terms. A higher price necessitates borrowing more, and extending the repayment period helps to keep monthly installments manageable.

However, this strategy can be a double-edged sword. While it makes expensive cars seem more "affordable" on a monthly basis, it significantly increases the total interest paid over the life of the loan. It’s a common trade-off that many buyers face when balancing their desire for a specific car with their budget realities.

2. Current Interest Rates

The prevailing interest rate environment plays a substantial role in loan term decisions. When interest rates are low, borrowers might feel more comfortable taking a slightly longer term because the additional interest cost isn’t as steep. Conversely, in a high-interest-rate environment, the impact of extending a loan term becomes far more significant.

A higher interest rate on a longer loan term can drastically inflate the total amount you pay for the vehicle. This is why it’s always wise to shop around for the best rates and understand how they interact with different loan durations. A small difference in APR can translate into hundreds or even thousands of dollars over several years.

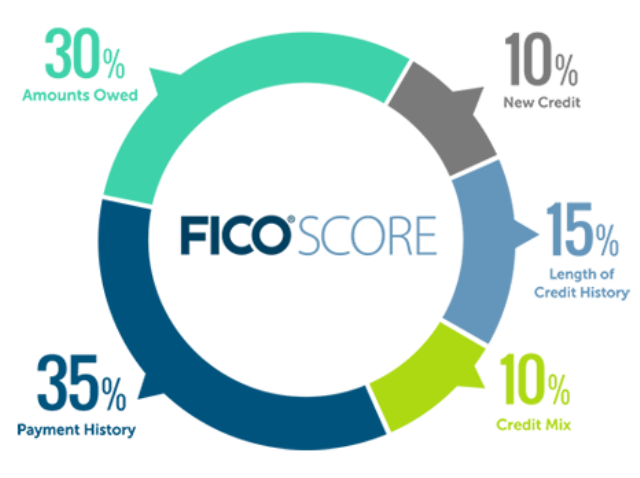

3. Your Credit Score

Your credit score is arguably the most powerful determinant of your loan terms. A high credit score (typically 700+) signals to lenders that you are a reliable borrower, opening the door to the lowest interest rates and a wider array of term options. Lenders are more willing to offer flexible and favorable terms to low-risk applicants.

Conversely, a lower credit score often leads to higher interest rates and potentially fewer term choices. Lenders perceive a higher risk and compensate by charging more for the loan. This makes improving your credit score a valuable step before even starting your car buying journey.

4. New vs. Used Cars

There’s often a notable difference in typical loan terms between new and used vehicles. New cars, with their higher price points, often qualify for longer terms (e.g., 72 or 84 months) from lenders. This helps offset the higher initial cost and makes the monthly payments more palatable for buyers.

Used cars, while generally less expensive, sometimes have slightly shorter maximum loan terms, though 60 or 72 months are still common. Lenders might be more cautious with very long terms on older used vehicles due to potential mechanical issues and faster depreciation, which increases their risk. However, this also depends heavily on the age and condition of the used car.

5. Economic Conditions

Broader economic conditions, such as inflation, employment rates, and overall consumer confidence, also influence loan terms. During periods of economic uncertainty, lenders might tighten their lending standards, potentially offering shorter terms or requiring higher down payments. Conversely, in a strong economy, lending might be more expansive.

Government policies and actions by central banks, like adjusting benchmark interest rates, directly impact the cost of borrowing for lenders, which in turn affects the rates and terms offered to consumers. Staying aware of the economic climate can provide valuable context for your financing decisions.

6. Lender Policies

Finally, each individual lender—whether it’s a bank, credit union, or dealership finance department—has its own set of policies and risk assessment models. Some lenders might specialize in longer terms, while others prefer shorter durations. Their specific criteria regarding credit scores, debt-to-income ratios, and vehicle types will all play a role in the terms they offer you.

This is precisely why shopping around and comparing offers from multiple lenders is a non-negotiable step in the car buying process. Different lenders can present surprisingly varied terms for the exact same car and borrower profile.

The Great Debate: Shorter vs. Longer Car Loan Terms

Choosing your loan term is a balancing act between immediate affordability and long-term financial health. Let’s break down the pros and cons of each approach to help you decide what’s best for your situation.

The Allure of Shorter Car Loan Terms (e.g., 36-60 Months)

Opting for a shorter loan term means you’ll be debt-free faster. This approach often makes the most financial sense for those who can manage higher monthly payments. It offers several significant advantages.

Pros of Shorter Terms:

- Lower Total Interest Paid: This is the most compelling benefit. Because you’re paying off the principal balance quicker, less interest accrues over time. The difference can be substantial, saving you hundreds or even thousands of dollars.

- Faster Equity Building: You’ll build equity in your vehicle much more quickly. This means the car’s market value will likely exceed the amount you owe sooner, reducing the risk of being "upside down" on your loan.

- Reduced Risk of Negative Equity: Negative equity, or being "underwater," occurs when you owe more on your car than it’s worth. Shorter terms significantly mitigate this risk, especially given how quickly new cars depreciate.

- Less Exposure to Depreciation: Cars lose value rapidly. A shorter loan term means you own the car outright before its value plummets too dramatically, protecting your investment.

- Quicker Financial Freedom: Imagine being free of a car payment! A shorter term gets you there faster, freeing up cash flow for other financial goals.

Cons of Shorter Terms:

- Higher Monthly Payments: The most obvious drawback is the larger chunk of your budget that goes towards your car payment each month. This requires careful budgeting and a stable income.

- Potentially Harder to Qualify: Lenders might require a stronger credit profile or a higher income-to-debt ratio to approve you for a higher monthly payment.

Based on my experience, shorter terms are often the financially savvier choice for those who can comfortably afford the higher monthly payments. It’s a disciplined approach that pays off in the long run by minimizing the total cost of the vehicle.

The Appeal of Longer Car Loan Terms (e.g., 72-84+ Months)

Longer loan terms have gained popularity primarily due to their ability to offer lower monthly payments. This makes more expensive vehicles seem accessible to a broader range of budgets. However, this convenience comes with its own set of significant financial drawbacks.

Pros of Longer Terms:

- Lower Monthly Payments: This is the primary driver for choosing a longer term. Smaller installments make it easier to fit a car payment into a tight budget, potentially allowing you to afford a more expensive vehicle or simply reduce your immediate financial burden.

- Increased Cash Flow: By lowering your fixed monthly expenses, you have more disposable income for other needs, savings, or investments.

Cons of Longer Terms:

- Significantly Higher Total Interest Paid: This is the biggest hidden cost. Extending the loan term means you’re paying interest for a much longer period, and the total amount of interest can accumulate dramatically. It effectively makes the car more expensive.

- Prolonged Negative Equity: You’re much more likely to be "upside down" on your loan for a longer period. Cars depreciate quickly, and a long loan term means your principal balance shrinks slower than the car’s value. This is a critical risk if you need to sell or trade in the car early.

- Risk of Outliving the Warranty: Many longer car loans extend beyond the typical manufacturer’s warranty. This means you could still be making payments on a car that is no longer covered for major repairs, leading to unexpected out-of-pocket expenses.

- Higher Depreciation Impact: The longer you hold the loan, the more the car’s value will decline. When you eventually pay it off, the car will be significantly older and worth less, meaning a larger portion of your money went into a depreciating asset.

Common mistakes to avoid include stretching a loan too far just for a lower monthly payment without fully understanding the long-term financial implications. It’s easy to get fixated on the monthly number and overlook the thousands of extra dollars in interest you might be paying.

Calculating Your Ideal Car Loan Term

There isn’t a single "perfect" car loan term for everyone. Your ideal term will be a highly personal decision based on your unique financial situation and priorities. Here’s how to approach this critical calculation.

1. Assess Your Comfortable Monthly Budget

Start by honestly evaluating what you can comfortably afford to pay each month for a car. This isn’t just about what lenders say you qualify for; it’s about what fits into your overall financial picture without straining your budget or preventing you from reaching other financial goals like saving for a home or retirement. Factor in insurance, fuel, maintenance, and potential repair costs as well.

2. Focus on the Total Cost, Not Just Monthly Payments

This is a pro tip from us: Always ask to see the total cost of the loan, including all interest, fees, and the principal. While a lower monthly payment might seem attractive, a 72-month loan could end up costing you thousands more than a 48-month loan for the same car. Use online car loan calculators to compare different scenarios (different terms, interest rates, and down payments) to visualize the impact on total cost.

3. Leverage Your Down Payment

A substantial down payment can significantly reduce the amount you need to borrow, which in turn can shorten your loan term or reduce your monthly payments. Even a 10-20% down payment can make a noticeable difference, immediately reducing your risk of negative equity. The more you put down, the less interest you’ll pay over time.

4. Consider Your Trade-In Value

If you’re trading in your current vehicle, its value can act as a down payment. Ensure you get a fair valuation for your trade-in and understand how it impacts the overall financing. Be wary of dealerships that inflate trade-in values only to hide the difference elsewhere in the deal.

By taking a holistic view and using available tools, you can pinpoint a loan term that aligns with both your immediate cash flow needs and your long-term financial wisdom.

The Pitfalls of Negative Equity (Being Upside Down)

Negative equity is a financial trap that many car owners fall into, particularly with longer loan terms. It occurs when the outstanding balance on your car loan is greater than the car’s current market value. In simpler terms, you owe more on the car than it’s worth.

This situation is exacerbated by rapid vehicle depreciation. Most new cars lose a significant portion of their value (20-30%) within the first year of ownership alone. If you’ve taken out a long loan with a small down payment, your principal balance might not decrease as fast as the car’s market value, leaving you "underwater."

The risks of negative equity are substantial:

- Difficulty Selling or Trading In: If you need to sell or trade in your car while you have negative equity, you’ll have to pay the difference out of pocket. For example, if your car is worth $15,000 but you owe $18,000, you’ll need to come up with $3,000 to clear the loan.

- Rolling Over Debt: A common mistake is rolling the negative equity from your old car into a new car loan. This means you’re starting your new car purchase already owing more than the car is worth, perpetuating the cycle of debt.

- Insurance Shortfall: In the event of a total loss (theft or accident), your standard car insurance policy will typically only pay out the car’s actual cash value. If you have negative equity, you could still owe the lender money even after the insurance payout. This is where GAP insurance becomes crucial.

To avoid negative equity, aim for a substantial down payment, choose the shortest loan term you can comfortably afford, and avoid rolling over previous car debt.

The Role of Interest Rates and APR

Understanding the difference between an interest rate and the Annual Percentage Rate (APR) is fundamental to smart car financing. The interest rate is simply the percentage charged on the principal amount borrowed. The APR, however, is a more comprehensive measure of the cost of borrowing. It includes the interest rate plus any additional fees or charges associated with the loan, expressed as an annual percentage.

When comparing loan offers, always look at the APR, as it gives you the truest picture of the total cost of borrowing. A lower APR directly translates to less money paid over the life of the loan.

The impact of interest rates becomes profoundly evident when comparing different loan terms. On a longer loan, even a seemingly small interest rate means you’re paying that percentage on a larger outstanding balance for a longer duration. This compounding effect significantly inflates the total cost. For example, a 6% APR on an 84-month loan will result in far more total interest paid than a 6% APR on a 48-month loan, purely due to the extended period of accrual.

Beyond the Term: Other Critical Car Loan Considerations

While the loan term is vital, several other elements significantly impact your overall car financing experience. Overlooking these can lead to missed savings or unexpected costs.

1. The Power of a Down Payment

As touched upon earlier, a down payment is your best friend in car financing. It reduces the principal amount you borrow, directly lowering your monthly payments and the total interest paid. A substantial down payment also helps you build equity faster and reduces your risk of negative equity. Aim for at least 10-20% of the car’s value if possible.

2. The Foundation: Your Credit Score

We cannot overstate the importance of your credit score. It’s the primary factor lenders use to assess your risk and determine your interest rate. A higher score unlocks lower APRs and more favorable terms. Before you even start shopping for a car, take steps to improve your credit if it’s not where you want it to be. For more detailed guidance, consider reading our article on How to Boost Your Credit Score for a Car Loan (Internal Link).

3. The Game-Changer: Pre-Approval

Getting pre-approved for a car loan from a bank or credit union before stepping into a dealership is a game-changer. It gives you a firm offer with an interest rate and maximum loan amount, effectively turning you into a cash buyer at the dealership. This allows you to negotiate the car’s price separately and avoid getting pressured into less favorable financing options offered by the dealer.

4. The Second Chance: Refinancing

If your financial situation improves after taking out a car loan (e.g., your credit score increases, or interest rates drop), you might be able to refinance your existing loan. Refinancing can secure you a lower interest rate, reduce your monthly payments, or even shorten your loan term, saving you money over time. It’s a smart move to review your loan terms periodically.

5. Essential Protection: GAP Insurance

Especially if you opt for a longer loan term or make a small down payment, GAP (Guaranteed Asset Protection) insurance is a wise investment. It covers the "gap" between what you owe on your loan and what your car is worth if it’s totaled or stolen. Without it, you could be left making payments on a car you no longer own.

Navigating the Car Loan Process Like a Pro

Equipped with this knowledge, you’re ready to tackle the car buying process with confidence. Here are some pro tips from us to ensure you get the best possible deal.

- Research Thoroughly: Don’t just research cars; research lenders. Compare interest rates, fees, and term options from multiple banks, credit unions, and online lenders before you even visit a dealership.

- Shop Around for Lenders: Never settle for the first loan offer. Get at least three to four quotes to ensure you’re getting a competitive rate. All inquiries within a short period (usually 14-45 days) will count as a single hard inquiry on your credit report, so shop confidently.

- Negotiate Car Price Separately: Always negotiate the price of the car first, before discussing financing. Once you’ve agreed on a price, then bring up your pre-approved loan or ask the dealer to beat your pre-approval rate. This prevents them from manipulating numbers between the car price and the loan terms.

- Read the Fine Print: Before signing anything, meticulously review all loan documents. Understand every fee, the total interest, and any prepayment penalties. Don’t be afraid to ask questions until you’re completely clear on all terms.

By following these steps, you’ll be well on your way to securing a car loan that truly works for your financial well-being.

Average Car Loan Term for New vs. Used Vehicles

While we’ve touched on this, it’s worth a dedicated look at the specific differences in loan terms between new and used cars, as this often influences buyer expectations.

For new vehicles, the average loan term has notably stretched. According to recent data, many new car loans are now commonly written for 72 or even 84 months. This is primarily to accommodate the increasing average transaction price of new cars, making the monthly payments more manageable for buyers. Lenders are often more willing to offer longer terms on new vehicles because they have a higher initial value and typically come with comprehensive warranties, reducing the lender’s risk of mechanical failure.

For used vehicles, the average loan term tends to be slightly shorter, though 60-72 months are still very common. Lenders might be more conservative with very long terms (e.g., 84 months) on older used cars due to:

- Higher Depreciation Rate: Older cars generally depreciate faster in percentage terms than newer ones, and their value curve flattens out.

- Increased Risk of Mechanical Issues: As cars age, the likelihood of costly repairs increases, which can impact a borrower’s ability to make payments.

- Lower Resale Value: The collateral (the car) is less valuable on an older vehicle, making lenders more cautious about extending repayment over too many years.

It’s crucial to remember that while the average for used cars might be a bit shorter, you can still find lenders offering extended terms, especially for certified pre-owned vehicles or those that are only a few years old. For a deeper dive into the used car market, check out our The Ultimate Guide to Buying a Used Car (Internal Link).

Future Trends in Car Financing

The automotive industry is constantly evolving, and car financing is no exception. We’re seeing several trends that could reshape the average car loan term in the coming years:

- Impact of Electric Vehicles (EVs): EVs often have higher upfront costs but potentially lower running costs. This could push towards longer loan terms to finance the initial purchase, or conversely, shorter terms if lower running costs free up budget.

- Rise of Subscription Models: Car subscription services, which bundle the vehicle, insurance, and maintenance into a single monthly fee, could become more popular, offering an alternative to traditional ownership and loans.

- Economic Shifts: Future economic conditions, interest rate policies, and consumer spending habits will continue to influence lending practices and the average loan terms offered.

Staying informed about these broader trends will help you anticipate changes in the auto finance landscape.

Conclusion: Making Your Car Loan Term Work for You

Navigating the world of car loans can feel overwhelming, but understanding the average car loan term and its implications is your most powerful tool. Remember, the "average" isn’t necessarily the "ideal" for your unique financial situation. Your goal should always be to find a loan term that:

- Fits comfortably within your monthly budget.

- Minimizes the total interest you pay over time.

- Aligns with your long-term financial goals.

- Reduces your risk of negative equity.

By prioritizing financial prudence over immediate gratification, making a solid down payment, leveraging a strong credit score, and diligently shopping for the best rates and terms, you can transform a potentially burdensome car loan into a manageable and smart financial decision. Don’t just accept the first offer; empower yourself with knowledge and negotiate like a pro. Your future self (and your wallet) will thank you.

For more detailed insights into consumer credit trends and their impact on auto loans, you can refer to reports from trusted sources like the Federal Reserve (External Link).