Unraveling the Average Used Car Loan Term: Your Definitive Guide to Smart Financing

Unraveling the Average Used Car Loan Term: Your Definitive Guide to Smart Financing Carloan.Guidemechanic.com

Embarking on the journey to purchase a used car is an exciting prospect. It offers a fantastic opportunity to find a reliable vehicle at a more accessible price point. However, navigating the world of auto financing, especially understanding the "average used car loan term," can feel like deciphering a complex code.

Many buyers focus solely on the monthly payment, overlooking crucial details that impact their overall financial health. This article is your comprehensive guide to understanding used car loan terms, helping you make informed decisions that save you money and stress in the long run. We’ll dive deep into what these terms mean for your wallet, explore common pitfalls, and share expert strategies for securing the best financing deal.

Unraveling the Average Used Car Loan Term: Your Definitive Guide to Smart Financing

What Exactly Is a Car Loan Term?

At its core, a car loan term refers to the length of time you have to repay your loan. This period is typically expressed in months, such as 36, 48, 60, 72, or even 84 months. Think of it as the repayment schedule agreed upon between you and your lender.

This term is a critical component of your auto loan, directly influencing two major aspects: your monthly payment amount and the total interest you will pay over the life of the loan. A shorter term generally means higher monthly payments but less interest paid overall. Conversely, a longer term offers lower monthly payments but accrues significantly more interest over time.

Understanding this fundamental concept is the first step toward smart used car financing. It’s about finding the right balance that aligns with your budget and long-term financial goals. Our professional insight suggests that many buyers underestimate the long-term cost implications of choosing a loan term.

Understanding the "Average" Used Car Loan Term

When we talk about the "average used car loan term," we’re referring to the typical repayment period that most buyers choose or are offered for pre-owned vehicles. This average isn’t static; it fluctuates based on economic conditions, lender policies, and consumer preferences. For instance, during periods of rising interest rates, buyers might gravitate towards longer terms to keep monthly payments manageable.

Based on recent market data and my experience in the auto financing landscape, the average used car loan term has generally extended over the past decade. Many lenders commonly offer terms ranging from 60 to 72 months for used cars. It’s not uncommon, however, to see terms as short as 36 months or as long as 84 months, especially for newer used models.

It’s important to remember that an "average" is just a benchmark. Your specific loan term will be tailored to your individual financial situation and the characteristics of the vehicle you’re purchasing. While the average provides a good starting point, it shouldn’t be the sole factor guiding your decision.

Factors Influencing Your Used Car Loan Term

Several crucial elements come into play when lenders determine the loan term they’re willing to offer you. Understanding these factors can empower you to improve your position before applying for financing. It’s not just about what the market offers, but what you bring to the table.

Your Credit Score

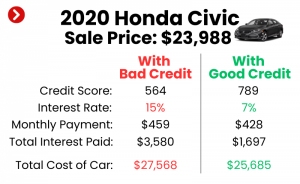

Your credit score is arguably the most significant factor influencing your loan term and interest rate. Lenders use this three-digit number to assess your creditworthiness and the likelihood of you repaying the loan. A high credit score (generally 700+) indicates a responsible borrower, often qualifying you for the most favorable terms, including potentially shorter loan options with lower interest rates.

Conversely, a lower credit score might lead lenders to offer longer terms to reduce your monthly payment, or to approve the loan with a higher interest rate. In some cases, a poor credit history could limit your access to certain loan terms entirely. Our professional insight suggests that improving your credit score before applying can unlock significantly better financing opportunities. For more detailed insights into credit scores, you can visit Experian’s official website.

Your Down Payment

A substantial down payment can dramatically impact the loan terms available to you. When you put more money down upfront, you reduce the amount you need to borrow, which inherently lowers your monthly payments. This also decreases the lender’s risk, making them more inclined to offer competitive terms.

Having a larger down payment can often open doors to shorter loan terms, as your monthly obligation for the remaining balance becomes more manageable. It also helps in avoiding negative equity, a situation where you owe more on the car than it’s worth. Common mistakes to avoid include trying to finance 100% of the vehicle’s cost without a down payment, as this can lead to less favorable terms.

Vehicle Age and Mileage

The age and mileage of the used car you’re interested in play a direct role in available loan terms. Lenders perceive older vehicles with high mileage as having a higher risk of mechanical issues and depreciation. This means their resale value might drop more quickly.

Consequently, lenders are often reluctant to offer very long loan terms for older cars. You might find that vehicles beyond a certain age (e.g., 8-10 years old) or mileage threshold (e.g., 100,000 miles) are restricted to shorter loan terms, perhaps 36 or 48 months. This protects the lender against potential losses if the car’s value declines significantly during the loan period.

Loan Amount

The total amount you need to borrow also affects the available loan terms. For smaller loan amounts, a shorter term might be entirely feasible, keeping monthly payments relatively low. However, for larger loan amounts, such as financing a luxury used car, a longer term might be necessary to spread out the cost and make the monthly payments affordable.

Lenders will assess the loan amount in relation to your income and the car’s value. They want to ensure that the loan is sustainable for you. Based on my experience, trying to push for a very short term on a high loan amount can often lead to unmanageably high monthly payments, making the loan application less likely to be approved.

Interest Rate

While the interest rate isn’t a "factor" that determines the term in the same way your credit score does, it significantly interacts with the loan term. A lower interest rate makes a shorter loan term more financially palatable, as the higher monthly payments are somewhat offset by the reduced cost of borrowing. Conversely, a higher interest rate on a long-term loan can lead to a surprisingly large total cost of ownership.

Savvy buyers understand that a favorable interest rate can make a significant difference. It allows more of your monthly payment to go towards the principal, accelerating your path to ownership. Always compare both the interest rate and the loan term when evaluating financing offers.

Lender Policies

Different lenders – banks, credit unions, and dealership financing arms – have varying policies regarding loan terms. Some may specialize in shorter terms for used cars, while others might be more flexible with longer options, even for older vehicles. Credit unions, for example, are often known for offering competitive rates and more flexible terms to their members.

It’s crucial to shop around and compare offers from multiple lenders. Don’t assume the first offer you receive is the best or only option. Each institution has its own risk assessment models and target customer base, which directly influences their loan product offerings.

Borrower’s Financial Situation

Beyond your credit score, lenders look at your overall financial picture. This includes your income, employment stability, and existing debt-to-income (DTI) ratio. A stable job and a low DTI ratio signal to lenders that you have the capacity to take on new debt.

If your DTI is already high, lenders might be more cautious. They might approve you for a longer term to reduce the monthly impact, or even decline the loan if they perceive too much risk. Demonstrating financial stability through consistent income and responsible debt management can significantly improve your financing options.

The Pros and Cons of Shorter Loan Terms (e.g., 36-48 months)

Choosing a shorter loan term for your used car comes with a distinct set of advantages and disadvantages. It’s a decision that impacts your monthly budget and your long-term financial outlook.

Pros of Shorter Loan Terms

- Lower Total Interest Paid: This is perhaps the biggest financial benefit. By paying off your loan faster, you spend less time accumulating interest charges, leading to significant savings over the life of the loan. You are simply borrowing money for a shorter period.

- Quicker Equity Build-Up: Your car will be paid off sooner, meaning you’ll own it outright more quickly. This allows you to build equity in the vehicle faster, which is beneficial if you plan to sell or trade it in.

- Reduced Risk of Negative Equity: Negative equity, or being "upside down" on your loan, occurs when you owe more than your car is worth. Shorter terms rapidly reduce your principal balance, minimizing the risk of this financially precarious situation.

- Faster Debt Freedom: Imagine the relief of having one less monthly payment! A shorter term means you’re free from car loan debt much sooner, freeing up cash flow for other financial goals or investments.

Cons of Shorter Loan Terms

- Higher Monthly Payments: The primary drawback of a shorter loan term is the higher monthly payment. Spreading the loan amount over fewer months means each payment is larger, which might strain your budget.

- Less Budget Flexibility: These higher payments can reduce your disposable income, making it harder to save for other goals or handle unexpected expenses. It demands a stricter adherence to your monthly budget.

The Pros and Cons of Longer Loan Terms (e.g., 72-84 months)

Longer loan terms have become increasingly popular for used cars, particularly as vehicle prices have risen. They offer immediate relief to monthly budgets but come with their own set of long-term considerations.

Pros of Longer Loan Terms

- Lower Monthly Payments: The most attractive feature of a longer loan term is the reduced monthly payment. By spreading the loan amount over more months, each payment becomes smaller, making car ownership seem more affordable.

- Greater Budget Flexibility: Lower payments can free up cash flow for other expenses, savings, or investments. This can be particularly appealing for those managing a tight budget or wanting to maintain financial liquidity.

Cons of Longer Loan Terms

- Higher Total Interest Paid: This is the most significant financial downside. Extending the repayment period means you’re paying interest for a longer time, often leading to thousands of dollars more in total interest compared to a shorter term.

- Extended Period of Debt: You’ll be making car payments for a much longer time, potentially well after the car starts to show significant wear and tear. This can feel like a perpetual cycle of debt.

- Increased Risk of Negative Equity: Longer terms mean you pay down the principal balance more slowly. This increases your chances of owing more than the car is worth, especially given that cars depreciate fastest in their early years. Our comprehensive article on "Understanding Car Depreciation" delves deeper into this topic.

- Higher Depreciation Risk: As cars age, they depreciate. With a longer loan term, you risk paying off a car that has significantly lost value, making it harder to sell or trade in for a fair price. You might find yourself upside down for a considerable portion of the loan.

Common Mistakes to Avoid When Choosing a Used Car Loan Term

Navigating car financing can be tricky, and it’s easy to fall into common traps. Based on my experience working with countless car buyers, here are some mistakes to actively avoid when selecting your used car loan term:

Focusing Solely on the Monthly Payment

This is perhaps the most prevalent mistake. While a low monthly payment is appealing, it can mask a significantly higher total cost due to a longer term and more interest paid. Always consider the full financial picture, not just the immediate monthly outlay. Lenders know this is a common trap and will often present the lowest monthly payment first.

Ignoring Total Interest Paid

Many buyers overlook the total amount of interest they’ll pay over the life of the loan. A seemingly small difference in interest rate or term can translate into thousands of dollars over several years. Always ask for the total cost of the loan, including all interest and fees.

Not Understanding Negative Equity

Getting "upside down" on your loan (owing more than the car is worth) is a serious financial risk, especially with longer terms on used cars. This can make it difficult to sell or trade in your car before the loan is fully paid off. It’s crucial to understand how quickly your car’s value might depreciate versus how quickly you’re paying down the principal.

Skipping a Down Payment

While it might seem convenient to finance the entire purchase, not making a down payment increases your loan amount and the risk of negative equity. It also often leads to less favorable loan terms and higher interest rates. A down payment shows commitment and reduces the lender’s risk.

Not Shopping Around for Rates and Terms

Accepting the first financing offer you receive, especially from a dealership, can be a costly mistake. Different lenders offer different rates and terms based on their specific risk assessments and business models. Always get pre-approved from multiple banks and credit unions before stepping into a dealership. This empowers you with negotiating leverage.

Pro Tips for Optimizing Your Used Car Loan Term

Choosing the right used car loan term is a strategic decision that can save you a substantial amount of money. Here are some pro tips from us to help you optimize your financing and make the most informed choice:

1. Know Your Budget Inside and Out

Before you even start looking at cars, understand exactly what you can comfortably afford for a monthly payment, not just for the car, but for insurance, fuel, and maintenance too. Don’t let a low monthly payment lure you into a longer, more expensive loan. Create a detailed budget and stick to it.

2. Boost Your Credit Score

Your credit score is your financial superpower. Before applying for a loan, take steps to improve it. Pay down existing debts, make all payments on time, and review your credit report for errors. A higher score translates directly into better interest rates and more flexible loan term options. Read our guide on "Boosting Your Credit Score for a Car Loan" for in-depth strategies.

3. Save for a Significant Down Payment

The more you put down upfront, the less you need to borrow. A substantial down payment not only reduces your monthly payments but also helps you secure a shorter loan term and a lower interest rate. Aim for at least 10-20% of the used car’s purchase price if possible.

4. Shop Around for Lenders

Never settle for the first loan offer. Get pre-approved by multiple financial institutions—your bank, credit unions, and online lenders. Compare their interest rates, fees, and available loan terms side-by-side. This competitive shopping can reveal significantly better deals and give you leverage during negotiations at the dealership.

5. Consider Refinancing Down the Road

If you’re unable to secure ideal terms initially, perhaps due to a lower credit score or market conditions, don’t despair. You can often refinance your used car loan later. If your credit score improves or interest rates drop, refinancing can help you secure a lower rate or a more favorable term, potentially saving you money.

6. Read the Fine Print (All of It!)

Before signing any loan agreement, meticulously read every line of the contract. Understand all terms, conditions, fees, and penalties. Ask questions about anything that is unclear. Being fully informed prevents unpleasant surprises later on. This includes understanding pre-payment penalties, if any, though they are less common with auto loans today.

Based on My Experience: Real-World Scenarios and Advice

Having advised many individuals on their car financing, I’ve noticed a recurring pattern: the allure of a low monthly payment often overshadows the long-term financial implications. For instance, I’ve seen clients extend their used car loan term from 60 to 72 months to save just $30-$50 a month, only to end up paying hundreds, sometimes thousands, more in total interest.

My professional insight suggests that for most used car buyers, a term between 48 and 60 months strikes a good balance. This period allows for manageable monthly payments while minimizing the total interest paid and reducing the risk of negative equity. For newer used cars (1-3 years old), a 60-month term is often reasonable. For older models, it’s prudent to aim for an even shorter term, if your budget allows.

Always consider the expected lifespan of the vehicle. If you’re financing a car that’s already 7 years old, committing to an 84-month loan means you’ll still be making payments when the car is 14 years old. Will it still be reliably running then? This is a crucial question many buyers overlook. Prioritize paying off the car while it still has significant value and reliability.

Future Trends in Used Car Financing

The landscape of used car financing is constantly evolving. We’re seeing increasing digitalization of the loan application process, allowing for quicker approvals and more personalized offers. Data analytics are becoming more sophisticated, enabling lenders to assess risk with greater precision.

Additionally, as the average age of vehicles on the road increases, and with electric vehicles entering the used market, we might see new financing products and term structures emerge. The emphasis will likely remain on flexibility and transparency, empowering consumers with more choices and clearer understanding of their loan terms. Staying informed about these trends will be key to smart financing in the years to come.

Conclusion: Make an Informed Decision on Your Used Car Loan Term

Understanding the average used car loan term is far more than just knowing a number; it’s about grasping the intricate relationship between your monthly payments, total interest paid, and long-term financial health. While a longer term might offer immediate relief with lower monthly payments, it often comes at the cost of significantly more interest and an increased risk of negative equity.

By focusing on your credit score, making a solid down payment, comparing offers from multiple lenders, and prioritizing total cost over just the monthly payment, you can make a truly informed decision. Don’t let the "average" dictate your choices. Empower yourself with knowledge, apply our expert tips, and choose a used car loan term that aligns perfectly with your financial goals and ensures a smooth ride ahead.

Your used car purchase is a significant investment. Make sure your financing strategy is as smart as your car choice.