Unveiling the Truth: Essential Car Loan Facts You Must Know Before Buying Your Next Ride

Unveiling the Truth: Essential Car Loan Facts You Must Know Before Buying Your Next Ride Carloan.Guidemechanic.com

The excitement of purchasing a new car is undeniable – the smell of fresh upholstery, the sleek design, the promise of new adventures. However, for most of us, this dream ride comes with a crucial financial step: securing a car loan. Navigating the world of auto financing can feel like a complex maze, filled with jargon and hidden traps.

But what if you could approach this process armed with clarity, confidence, and a deep understanding of how car loans truly work? That’s precisely our mission today. We’re diving deep into the essential car loan facts that every prospective buyer needs to know. This isn’t just about getting approved; it’s about securing the best possible terms, saving money, and making an informed decision that benefits your financial future.

Unveiling the Truth: Essential Car Loan Facts You Must Know Before Buying Your Next Ride

Based on my extensive experience in consumer finance, understanding these fundamental principles can transform your car buying journey from stressful to strategic. Let’s peel back the layers and uncover the critical insights that will empower you.

The Foundation: What Exactly is a Car Loan?

At its core, a car loan is a sum of money borrowed from a lender to purchase a vehicle, with the agreement that you will repay the borrowed amount, plus interest, over a specified period. This repayment typically occurs through fixed monthly installments. Think of it as a specialized type of installment loan.

Unlike an unsecured personal loan, a car loan is a secured loan. This means the vehicle itself acts as collateral for the loan. If you fail to make your payments, the lender has the legal right to repossess the car to recover their losses. This collateralized nature is precisely why car loan interest rates are generally lower than those for unsecured loans, as the lender’s risk is mitigated.

The three primary components of any car loan are the principal, the interest, and the loan term. The principal is the original amount of money you borrow to buy the car. Interest is the cost of borrowing that money, expressed as a percentage of the principal. Finally, the loan term refers to the duration over which you agree to repay the loan, usually measured in months. Understanding how these elements interact is the first critical step toward smart financing.

Decoding the Key Players: Where Can You Get a Car Loan?

When you decide to finance a car, you’ll quickly realize there are several avenues available for securing a loan. Each option comes with its own set of advantages and disadvantages, and knowing them empowers you to shop around effectively. Don’t assume the first offer is the best; competition among lenders can significantly benefit your wallet.

Dealership Financing: The Convenience Factor

For many buyers, securing a loan through the dealership where they’re purchasing the car seems like the most straightforward option. Dealers act as intermediaries, working with a network of banks and financial institutions to find a loan for you. This "one-stop shop" convenience is undeniably appealing, simplifying the car buying process significantly.

Often, dealers can offer special promotional rates, particularly on new vehicles, which can seem very attractive. They might also be able to approve you quickly, sometimes even on the spot, making the purchase feel seamless. The appeal of driving off the lot the same day with your new car and its financing all sorted is a powerful draw.

However, there are potential drawbacks. While dealers present you with an offer, they might not always show you the absolute lowest rate available from their entire network. Their incentive is often to maximize their profit, which can sometimes come at your expense in the form of a slightly higher interest rate or less favorable terms. Pro tips from us: Always remember that the dealer is also a salesperson; their goal is to make a sale, and financing is a significant profit center for them.

Banks and Credit Unions: Your Traditional Lenders

Traditional financial institutions like banks and credit unions are often excellent sources for car loans. These lenders typically offer competitive interest rates, particularly to customers with strong credit profiles. If you already have a banking relationship, starting there can sometimes simplify the application process.

Credit unions, in particular, are member-owned and often prioritize offering lower interest rates and more flexible terms to their members. Based on my experience, credit unions frequently provide some of the most competitive auto loan rates available, making them a wise place to check first. They are known for their customer-centric approach and transparency.

The process of applying through a bank or credit union usually involves a separate application and approval process before you even step onto a dealership lot. While this requires a bit more effort upfront, it gives you a pre-approval letter, which is a powerful negotiating tool. You arrive at the dealership with your own financing in hand, essentially making you a cash buyer in the dealer’s eyes.

Online Lenders: Speed and Comparison at Your Fingertips

The digital age has brought a new player to the car loan market: online lenders. Websites and platforms dedicated solely to car financing allow you to apply for a loan from the comfort of your home, often receiving multiple offers from various lenders within minutes. This convenience and speed are a major draw for many.

Online lenders provide an excellent opportunity to compare rates from a broad spectrum of financial institutions quickly. You can often pre-qualify with a "soft inquiry" on your credit, which doesn’t impact your credit score, allowing you to gauge your potential rates without commitment. This transparency and ease of comparison are significant advantages.

However, it’s crucial to exercise caution. While many online lenders are legitimate and reputable, the digital landscape also harbors less scrupulous operations. Always verify the lender’s credentials, read reviews, and ensure they are licensed in your state. Common mistakes to avoid are rushing into an offer from an unknown online entity without proper due diligence, as this could lead to unfavorable terms or even scams.

Essential Car Loan Facts: What Influences Your Loan?

Understanding the factors that lenders consider when evaluating your loan application is paramount. These elements directly impact whether you’re approved, and more importantly, the interest rate and terms you receive. Being prepared and knowing how to optimize these factors can save you thousands over the life of your loan.

Your Credit Score – The Ultimate Game Changer

Your credit score is arguably the most influential factor in determining your car loan’s interest rate. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. Lenders use this three-digit number to assess the risk of lending money to you. A higher score signals lower risk, translating into lower interest rates.

Individuals with excellent credit scores (generally 720+) typically qualify for the lowest advertised rates. Those with good credit (660-719) will still get favorable rates, though slightly higher. If your credit score is fair (600-659) or poor (below 600), you’ll likely face significantly higher interest rates, as lenders perceive you as a greater risk. This can add substantially to the total cost of your vehicle.

Pro tips from us: Before you even start car shopping, pull your credit report and score. If your score isn’t where you want it to be, take steps to improve it. Pay down existing debts, make all payments on time, and dispute any errors on your report. A few months of diligent effort can make a big difference in your loan terms. For more detailed strategies on improving your credit score, check out our comprehensive guide: .

The Power of the Down Payment

A down payment is the initial amount of money you pay upfront for the car, reducing the total amount you need to borrow. This is a critical element often overlooked when buyers focus solely on monthly payments. A larger down payment immediately reduces your principal, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

Beyond reducing your financial burden, a substantial down payment signals to lenders that you are a serious and responsible borrower. It also decreases the loan-to-value (LTV) ratio, which is the amount you’re borrowing compared to the car’s value. A lower LTV means less risk for the lender, potentially leading to better interest rates.

While there’s no mandatory amount, most financial experts recommend a down payment of at least 10-20% for a new car and 20% or more for a used car. This helps protect you against negative equity, which occurs when you owe more on the car than it’s worth. Aiming for a healthy down payment is one of the smartest financial moves you can make when buying a car.

Understanding Interest Rates (APR): Beyond the Percentage

The interest rate is the cost you pay for borrowing the principal amount, but it’s crucial to look at the Annual Percentage Rate (APR). The APR is a more comprehensive measure of the cost of your loan because it includes not only the interest rate but also any additional fees or charges associated with the loan. This gives you the true annual cost of borrowing.

Car loans are typically fixed-rate loans, meaning your interest rate remains constant throughout the loan term, providing predictable monthly payments. The APR you qualify for is heavily influenced by your credit score, the loan term you choose, and prevailing market conditions. Lenders often adjust rates based on the economy and the federal funds rate.

Always compare APRs, not just interest rates, when evaluating loan offers. A seemingly lower interest rate might hide higher fees that ultimately make the APR less favorable. Common mistakes to avoid are focusing solely on the interest rate number without understanding what the APR truly represents.

Loan Term – The Length of Your Commitment

The loan term, or the duration over which you repay the loan, is a double-edged sword. Shorter loan terms (e.g., 36 or 48 months) mean higher monthly payments because you’re paying off the principal faster. However, the significant advantage is that you pay substantially less interest over the life of the loan. You also build equity in the car more quickly.

Conversely, longer loan terms (e.g., 60, 72, or even 84 months) offer lower monthly payments, which can make a more expensive car seem affordable. The trade-off, however, is that you end up paying significantly more in total interest over the longer duration. Additionally, longer terms increase your risk of being "upside down" on your loan, meaning the car depreciates faster than you pay it off.

Finding the right balance depends on your budget and financial goals. While lower monthly payments might be tempting, always consider the total cost of the loan. Based on my experience, extending a loan term purely to afford a more expensive car than you need is a common pitfall that leads to financial strain down the road.

Debt-to-Income (DTI) Ratio: A Lender’s Perspective

Your Debt-to-Income (DTI) ratio is another crucial metric lenders use to assess your ability to manage monthly payments and repay debt. It’s calculated by dividing your total monthly debt payments (including the proposed car loan) by your gross monthly income. Lenders use this ratio to determine if you have enough disposable income to comfortably afford the new loan.

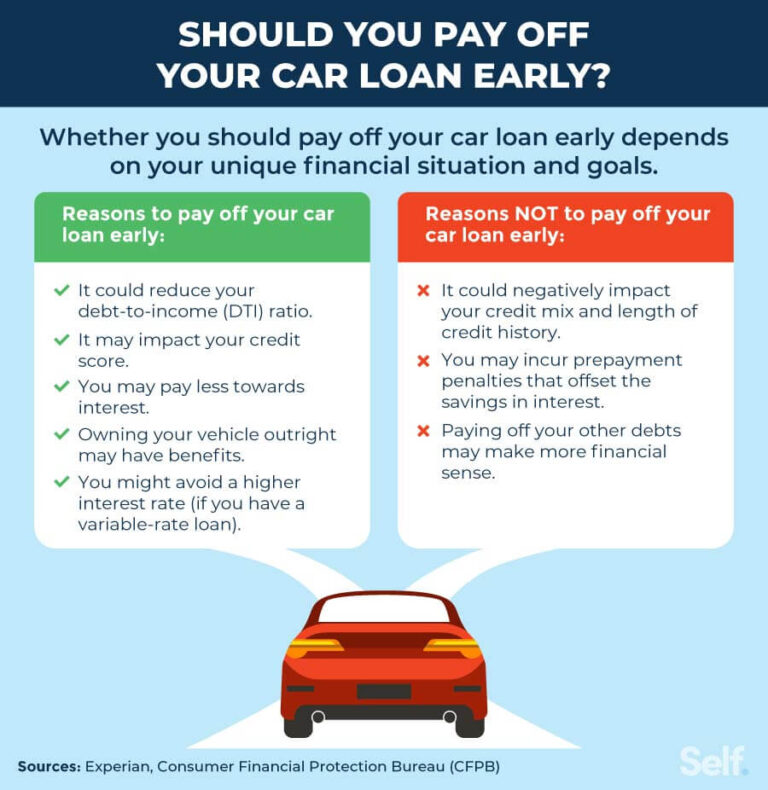

A lower DTI ratio indicates that you have more income relative to your debt obligations, making you a less risky borrower. Most lenders prefer a DTI ratio of 36% or less, though some might go higher depending on other factors like your credit score and the loan amount. If your DTI is too high, it signals to lenders that you might be overextended financially.

Before applying for a car loan, calculate your DTI. If it’s on the higher side, consider paying down other debts or increasing your income to improve this ratio. A healthy DTI not only helps with loan approval but also ensures you’re not taking on more debt than you can realistically handle.

The Car Loan Application Journey: Steps to Success

Navigating the car loan process effectively requires a strategic approach. It’s not just about filling out forms; it’s about being prepared, understanding your options, and making informed decisions at each stage. Following a structured journey can alleviate stress and lead to a more favorable outcome.

Research & Budgeting: Know What You Can Afford

Before you even start looking at cars, it’s vital to determine your budget. This isn’t just about the monthly car payment; it’s about the total cost of ownership. Factor in potential insurance costs, fuel, maintenance, and registration fees, all of which can add significantly to your monthly expenses.

Research different car models that fit your lifestyle and, more importantly, your budget. Don’t fall in love with a vehicle that stretches your finances thin. Using online calculators can help you estimate monthly payments based on different car prices, down payments, and interest rates. This preliminary research is your shield against overspending.

Knowing what you can truly afford, not just what a lender might approve you for, is a cornerstone of responsible car buying. It prevents buyer’s remorse and financial strain down the line.

Get Pre-Approved: Your Negotiating Superpower

One of the most powerful steps you can take is to get pre-approved for a car loan before you visit a dealership. This means applying for a loan with a bank, credit union, or online lender and receiving an offer that specifies the maximum loan amount, interest rate, and terms you qualify for. It’s a conditional approval, contingent on the final car and your income verification.

A pre-approval letter transforms you into a cash buyer in the eyes of the dealership. You walk in knowing exactly how much you can spend and at what interest rate. This removes the financing variable from the negotiation for the car’s price, allowing you to focus solely on getting the best deal on the vehicle itself. It also provides a benchmark against which you can compare any financing offers from the dealer.

Be aware that getting pre-approved typically involves a "hard inquiry" on your credit report, which can slightly ding your score. However, multiple inquiries for the same type of loan within a short window (usually 14-45 days) are often grouped as a single inquiry by credit bureaus, minimizing the impact.

Reviewing the Loan Offer: Look Beyond the Monthly Payment

Once you have loan offers in hand – whether from pre-approvals or the dealership – it’s crucial to review them meticulously. Common mistakes to avoid are focusing solely on the monthly payment amount. While important, it doesn’t tell the whole story. You need to scrutinize the Annual Percentage Rate (APR), the total loan amount, and the full loan term.

Compare the APRs from different lenders. A lower APR means you’ll pay less interest over time. Also, examine any fees included in the loan, such as origination fees or documentation fees, which can inflate the total cost. Understand the full repayment schedule and the total amount you will pay back over the life of the loan.

Pro tip from us: Don’t be afraid to ask questions. If something isn’t clear, demand clarification. Take your time to read the fine print; don’t let anyone rush you into signing. It’s your money and your long-term commitment.

The Closing Process: Understanding Your Obligations

The final stage involves signing the loan documents. By this point, you should have a clear understanding of all the terms and conditions. The loan agreement is a legally binding contract, so ensure every detail matches what you’ve agreed upon. This includes the vehicle identification number (VIN), the loan amount, the APR, the monthly payment, and the loan term.

You’ll also review and sign documents related to the vehicle title, which typically names the lender as a lienholder until the loan is fully repaid. Understand your responsibilities regarding insurance requirements, late payment penalties, and any clauses related to defaulting on the loan.

Once all documents are signed and the loan is funded, the car is yours, and your repayment journey begins. Keep copies of all signed documents for your records. This complete set of paperwork is essential for future reference, whether for taxes, insurance claims, or if you ever decide to refinance.

Beyond the Basics: Advanced Car Loan Facts & Considerations

While the core mechanics of car loans are important, there are additional considerations that can significantly impact your financial well-being throughout the ownership of your vehicle. Being aware of these advanced facts can help you make even smarter decisions and avoid common pitfalls.

Negative Equity (Upside Down Loans): A Financial Trap

Negative equity, often referred to as being "upside down" or "underwater" on your loan, occurs when you owe more on your car loan than the car is currently worth. This is a surprisingly common situation, especially in the early years of a loan, due to rapid depreciation of new vehicles. If your car is totaled or stolen, your insurance payout might be less than your loan balance, leaving you responsible for the difference.

Several factors contribute to negative equity, including a small or no down payment, a long loan term, and buying a car that depreciates quickly. If you trade in a car with negative equity, the outstanding balance is often rolled into your new car loan, creating a cycle of increasing debt.

To mitigate this risk, aim for a substantial down payment, choose a shorter loan term, and consider cars with better resale values. Avoiding the cycle of rolling negative equity into new loans is crucial for long-term financial health.

GAP Insurance: Is It Worth It?

Guaranteed Asset Protection (GAP) insurance is an optional add-on that covers the "gap" between what your car is worth (and what your standard auto insurance would pay out) and the remaining balance on your loan, in the event your car is declared a total loss due due to an accident or theft. Since cars depreciate quickly, especially new ones, this gap can be substantial.

For example, if you owe $25,000 on your car but its market value is only $20,000 when it’s totaled, your collision insurance would pay $20,000, leaving you responsible for the remaining $5,000. GAP insurance would cover that $5,000.

GAP insurance is particularly beneficial if you made a small down payment, financed for a long term, or purchased a vehicle that depreciates rapidly. You can often buy it from the dealership, but it’s usually cheaper to get it from your auto insurance provider or a credit union. Based on my experience, comparing prices for GAP insurance is essential, as dealership markups can be significant.

Refinancing Your Car Loan: Unlocking Better Terms

Refinancing a car loan means taking out a new loan to pay off your existing car loan. People typically consider refinancing for several reasons, most commonly to secure a lower interest rate, reduce monthly payments, or change the loan term. This can be a smart financial move if market rates have dropped, your credit score has improved since you first took out the loan, or if you’re struggling with your current payments.

The process usually involves applying to various lenders, much like when you first got your car loan. If approved, the new lender pays off your old loan, and you begin making payments to the new lender under the new terms. This can lead to substantial savings over the remaining life of the loan. If you’re considering refinancing, our article provides an in-depth look at the process.

Before refinancing, compare the new loan’s total cost, including any fees, against your potential savings. Ensure the new terms genuinely benefit you and don’t just extend your repayment period without significant interest savings.

Understanding Fees and Charges: The Hidden Costs

Beyond the interest rate, car loans can come with various fees and charges that can increase your overall cost. These might include origination fees, documentation fees, processing fees, or even late payment penalties. While some fees are legitimate, others might be negotiable or even questionable.

Common mistakes to avoid are not asking for a full breakdown of all fees before signing. Dealerships, in particular, might try to bundle various fees into the total price without explicit explanation. Always inquire about each fee and its purpose. If a fee seems excessive or unclear, challenge it.

Some fees, like a pre-payment penalty (though rare for car loans), could cost you money if you pay off your loan early. Always read the fine print of your loan agreement to understand all potential charges and obligations.

Beware of Add-ons: Separating Value from Profit

When finalizing your car purchase, dealerships often present a range of add-ons, such as extended warranties, paint protection, fabric protection, anti-theft devices, or VIN etching. While some of these might offer legitimate value, many are heavily marked up and add significantly to your loan principal and, consequently, your total interest paid.

Based on my experience, these add-ons are often highly profitable for dealers and may not always be in your best interest. An extended warranty, for instance, might duplicate coverage you already have from the manufacturer or be cheaper to purchase from a third party directly. Paint protection might be something you can easily do yourself for a fraction of the cost.

Always evaluate each add-on independently. Research its actual value and consider if you genuinely need it. It’s often best to negotiate the car price and the loan terms separately from these additional products. Decline anything you don’t need or can get cheaper elsewhere.

Common Car Loan Mistakes to Avoid

Even with the best intentions, buyers often fall into common traps that can lead to more expensive loans or financial stress. Being aware of these pitfalls is your first line of defense.

- Focusing Only on Monthly Payments: This is perhaps the most frequent mistake. A low monthly payment can be achieved by extending the loan term significantly, leading to much higher total interest paid and a greater risk of negative equity. Always consider the total cost of the loan.

- Not Getting Pre-Approved: Without a pre-approval, you lose significant negotiating power at the dealership. You’re effectively relying on the dealer to find you the best financing, which may not align with their profit motives.

- Ignoring Your Credit Score: Your credit score is your financial resume. Neglecting it means you’re walking into negotiations blind, unaware of the rates you truly qualify for, potentially accepting a higher rate than you deserve.

- Extending the Loan Term Too Much: While a longer term reduces monthly payments, it drastically increases the total interest paid and exacerbates the risk of being upside down on your loan. Aim for the shortest term you can comfortably afford.

- Skipping the Fine Print: Loan agreements are legal documents. Failure to read and understand every clause, fee, and condition can lead to unpleasant surprises down the road. Take your time, and don’t be pressured.

- Buying More Car Than You Can Afford: It’s easy to get swept up in the emotion of a new car. Stick to your budget, considering not just the payment but also insurance, maintenance, and fuel. Overspending on a car is a common cause of financial strain.

Pro Tips for Securing the Best Car Loan

Armed with these car loan facts, you’re well on your way to making an informed decision. Here are some final pro tips to help you secure the most advantageous financing terms possible:

- Boost Your Credit Score: Start early! Pay bills on time, reduce credit card balances, and check your credit report for errors. A higher score translates directly to lower interest rates.

- Save for a Substantial Down Payment: The more you put down, the less you borrow, which means lower monthly payments and less interest over time. Aim for 10-20% for new cars, and 20% or more for used cars.

- Shop Around for Lenders: Don’t just accept the first offer. Get pre-approvals from multiple banks, credit unions, and online lenders. Compare their APRs, not just their interest rates. The Consumer Financial Protection Bureau (CFPB) offers excellent resources on understanding auto loans and comparison shopping.

- Negotiate the Car Price and the Loan Terms Separately: Treat these as two distinct negotiations. First, agree on the car’s price. Then, compare the dealer’s financing offer against your pre-approvals.

- Understand the Total Cost: Always look beyond the monthly payment. Calculate the total amount you will pay over the life of the loan, including all interest and fees. This gives you the true cost of borrowing.

Conclusion: Drive Away with Confidence

Understanding car loan facts isn’t just about financial literacy; it’s about empowerment. It’s about approaching one of life’s significant purchases with clarity, confidence, and control. By dissecting the nuances of credit scores, down payments, interest rates, and loan terms, you’re no longer a passive recipient of a loan offer. Instead, you become an active, informed participant, capable of negotiating the best possible deal.

Remember, the goal is not just to get a car, but to get a car on terms that support your financial health, not hinder it. By avoiding common mistakes and applying these expert strategies, you can drive away not only with your dream car but also with the peace of mind that you’ve made a truly smart financial decision. Your journey to car ownership should be exciting, not financially draining. Equip yourself with these facts, and you’ll be well on your way to a successful and savvy car loan experience.