What Car Loan Can I Get Approved For? Your Ultimate Guide to Navigating Auto Loan Approval

What Car Loan Can I Get Approved For? Your Ultimate Guide to Navigating Auto Loan Approval Carloan.Guidemechanic.com

The dream of a new set of wheels is often accompanied by a crucial question: "What car loan can I get approved for?" For many, securing an auto loan feels like navigating a complex maze. It’s a common concern, whether you’re eyeing a brand-new sedan or a reliable pre-owned SUV. Understanding the factors that influence car loan approval is the first step towards confidently driving off the lot.

This comprehensive guide is designed to demystify the auto loan process. We’ll explore every facet of eligibility, from your credit score to your income, helping you understand precisely what lenders look for. By the end of this article, you’ll have a clear roadmap to secure the best possible car loan approval for your situation, empowering you to make informed financial decisions.

What Car Loan Can I Get Approved For? Your Ultimate Guide to Navigating Auto Loan Approval

Understanding the Car Loan Landscape

Before diving into the specifics of approval, it’s helpful to grasp the basics of car loans. An auto loan is essentially an agreement where a lender provides you with funds to purchase a vehicle, and you agree to repay that amount, plus interest, over a set period. This repayment structure involves regular monthly installments until the loan is fully satisfied.

The approval process isn’t just a formality; it’s a critical assessment lenders undertake to determine their risk. They want to ensure you have the capacity and willingness to repay the borrowed money. Your ability to secure a loan, and the terms you receive, hinge on several key financial indicators.

The Core Pillars of Car Loan Approval: What Lenders Really Look For

Securing a car loan approval isn’t a single-factor equation. Lenders consider a holistic view of your financial health. Based on my experience, focusing on these core pillars will significantly improve your chances and lead to better loan terms.

1. Your Credit Score: The Ultimate Gatekeeper

Your credit score is arguably the most influential factor in car loan approval. It’s a three-digit number that summarizes your creditworthiness, reflecting your history of borrowing and repayment. Lenders use this score to quickly assess the likelihood of you defaulting on a loan.

FICO and VantageScore are the two primary credit scoring models. They analyze information from your credit reports, which are maintained by the three major credit bureaus: Experian, Equifax, and TransUnion. These scores range typically from 300 to 850, with higher scores indicating lower risk.

How Your Credit Score Impacts Approval and Rates:

- Excellent Credit (780+): With excellent credit, you are considered a prime borrower. You’ll likely qualify for the lowest interest rates and the most favorable loan terms available. Lenders view you as a very low risk.

- Good Credit (670-779): Most borrowers fall into this category. You’ll still qualify for competitive rates, though they might be slightly higher than those with excellent credit. Approval is generally straightforward if other factors are strong.

- Fair Credit (580-669): This range indicates some past credit challenges or a limited credit history. You can still get approved for a car loan, but expect higher interest rates and potentially stricter terms. Lenders will scrutinize other aspects of your application more closely.

- Poor Credit (Below 580): Getting a car loan with poor credit is more challenging but not impossible. You’ll likely face significantly higher interest rates, require a larger down payment, or need a co-signer. Lenders perceive you as a high-risk borrower.

Pro Tips from Us: Before you even start car shopping, check your credit score. Many credit card companies offer free access to your score, or you can use services like Credit Karma. Knowing your score empowers you to understand your position and identify any errors. Common mistakes to avoid are applying for a loan without any idea of your credit standing, which can lead to disappointment or accepting unfavorable terms.

2. Income and Employment Stability: Can You Afford It?

Lenders need to be confident that you have a consistent and sufficient income to cover your monthly car loan payments. Your income directly impacts your ability to repay the loan and demonstrates financial stability. This is a fundamental aspect of car loan approval.

Proof of employment and income is standard practice. You’ll typically be asked to provide recent pay stubs (usually 1-2 months’ worth), W-2 forms from previous years, or even tax returns if you’re self-employed. These documents verify your stated income and employment history.

For self-employed individuals, lenders often require more extensive documentation, such as two years of tax returns and bank statements, to establish a reliable income pattern. Lenders want assurance you can consistently make payments, regardless of your employment type. A stable job history, ideally with the same employer for at least two years, strengthens your application.

3. Debt-to-Income (DTI) Ratio: Your Financial Balancing Act

Your Debt-to-Income (DTI) ratio is a crucial metric that reveals how much of your gross monthly income goes towards paying your existing debts. Lenders use this ratio to determine if you have enough disposable income to comfortably take on another monthly payment, like a car loan.

To calculate your DTI, simply add up all your monthly debt payments (mortgage/rent, student loans, credit card minimums, personal loans, etc.) and divide that sum by your gross monthly income. For example, if your debts total $1,500 and your gross income is $4,500, your DTI is 33%.

An ideal DTI for car loan approval is generally below 36%, though some lenders may accept up to 43% or even higher for very strong applicants. A lower DTI indicates less financial strain and a greater ability to manage additional debt. If your DTI is too high, it signals to lenders that you might be overextended, making you a higher risk.

Pro Tips from Us: If your DTI is on the higher side, consider paying down some existing debts before applying for a car loan. Even small reductions in credit card balances can make a noticeable difference. This proactive step can significantly improve your car loan approval chances and potentially secure better terms.

4. Down Payment: Showing Your Commitment

A down payment is the initial sum of money you pay upfront towards the purchase of a car. It reduces the total amount you need to borrow, thereby lowering your monthly payments and the total interest paid over the life of the loan. From my vantage point, a substantial down payment often signals a lower risk to lenders.

The benefits of a down payment are numerous. Not only does it decrease your loan amount, but it also creates immediate equity in the vehicle. This means you owe less than the car is worth from day one, reducing the risk of being "upside down" on your loan (owing more than the car’s market value).

While there’s no mandatory down payment for all car loans, a general recommendation is to put down at least 10% for a used car and 20% for a new car. For borrowers with fair or poor credit, a larger down payment (e.g., 20-30%) can significantly improve their approval odds and help secure a more reasonable interest rate, compensating for a weaker credit profile.

5. Vehicle Choice: Does the Car Matter?

Surprisingly, the specific vehicle you choose can indeed impact your car loan approval. Lenders consider the car itself as collateral for the loan. If you default, they need to be able to repossess and sell the vehicle to recoup their losses.

New cars generally pose less risk to lenders. They hold their value better initially, are less prone to mechanical issues, and their market value is more predictable. This often translates to more favorable loan terms and easier approval.

Used cars can be approved, but lenders will assess their age, mileage, and overall condition. Very old or high-mileage vehicles might be considered higher risk due to depreciation and potential maintenance issues. Some lenders have restrictions on the age or mileage of vehicles they will finance, especially for longer loan terms.

6. Loan Term and Interest Rate: The Cost of Borrowing

The loan term is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, 84 months). The interest rate is the cost of borrowing money, expressed as a percentage of the loan amount. Both factors are intrinsically linked and heavily influence your monthly payment and the total cost of the loan.

A shorter loan term means higher monthly payments but less interest paid over time. Conversely, a longer loan term results in lower monthly payments, making the car seem more affordable, but you’ll pay significantly more in total interest. Common mistakes to avoid are focusing solely on the monthly payment without considering the overall cost. A lower monthly payment can be attractive, but an extended loan term can drastically increase the total amount you pay for the car.

Your credit score plays a direct role in the interest rate you’re offered. Borrowers with excellent credit receive the lowest rates, while those with poor credit face much higher rates. It’s a balancing act: find a loan term that offers manageable monthly payments without accumulating excessive interest over the life of the loan.

Strategies for Improving Your Chances of Car Loan Approval

Even if your financial situation isn’t perfect, there are proactive steps you can take to significantly bolster your car loan approval prospects.

Boost Your Credit Score

Improving your credit score is one of the most effective ways to enhance your eligibility and secure better rates. Start by consistently paying all your bills on time, as payment history is the largest factor in your score. Reduce your existing credit card balances to lower your credit utilization ratio, which is another key factor. Avoid opening new credit accounts just before applying for a car loan, as this can temporarily ding your score. Finally, obtain copies of your credit reports and dispute any errors you find; even small inaccuracies can negatively impact your score.

Save for a Larger Down Payment

As discussed, a larger down payment signals less risk to lenders and can significantly improve your loan terms. Start a dedicated savings fund for your car down payment as early as possible. Even an extra few hundred or thousand dollars can make a substantial difference in your monthly payments and total interest. Consider selling an old car or other assets to boost your down payment fund.

Get Pre-Approved

Getting pre-approved for a car loan is a game-changer in the car buying process. It means a lender has already reviewed your financial information and tentatively approved you for a specific loan amount at a particular interest rate, before you even step foot in a dealership. This transforms you into a cash buyer, giving you significant negotiating power on the car’s price.

Pre-approval also sets a clear budget, preventing you from falling in love with a car you can’t truly afford. You can obtain pre-approval from various sources, including your local bank, credit union, or reputable online lenders. For more in-depth insights, read our guide on The Benefits of Car Loan Pre-Approval.

Consider a Co-Signer

If you have a limited credit history or a less-than-stellar credit score, a co-signer might be the key to getting approved. A co-signer is someone with good credit who agrees to be equally responsible for the loan if you fail to make payments. Their strong credit history essentially "lends" credibility to your application, reducing the lender’s risk.

While beneficial for the primary borrower, it’s important to understand the significant risks for the co-signer. Their credit score will be impacted by the loan, and they are legally obligated to repay the full amount if you default. This arrangement should only be entered into with someone you trust implicitly, like a family member, and with a clear understanding of the responsibilities involved.

Explore Dealership Financing vs. Direct Lenders

When seeking a car loan, you generally have two main avenues: direct lenders (banks, credit unions, online lenders) or dealership financing. Each has its pros and cons. Direct lenders often allow you to get pre-approved, giving you a strong negotiating position at the dealership. They may also offer slightly better rates if you have good credit, as they specialize in lending.

Dealership financing, while convenient, can sometimes come with higher interest rates if you’re not careful. However, dealerships often have access to a wide network of lenders, including those who specialize in subprime loans, which can be advantageous for buyers with less-than-perfect credit. Sometimes they also offer special manufacturer incentives or low APR deals that direct lenders cannot match. Always compare offers from both types of lenders to secure the best deal.

What if You Have Bad Credit?

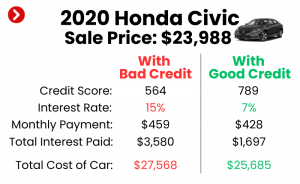

Having bad credit doesn’t necessarily close the door on car loan approval, but it does make the journey more challenging. It’s crucial to approach this situation with realistic expectations. Lenders view bad credit as a higher risk, which means you’ll likely face less favorable terms.

You can still get approved for a car loan, often through subprime lenders or specialized programs at dealerships. These lenders are willing to take on higher-risk borrowers but compensate for that risk by charging significantly higher interest rates. This means your monthly payments will be higher, and the total cost of the car will increase substantially over the loan term.

In addition to higher interest rates, you might be required to make a larger down payment to offset the lender’s risk. The loan term might also be shorter, leading to higher monthly payments but reducing the overall risk period for the lender. While getting a car with bad credit is possible, it should be seen as an opportunity to rebuild your credit. Consistently making on-time payments on a bad credit car loan can significantly improve your credit score over time, paving the way for better financial opportunities in the future. For more information on managing finances with a lower credit score, you might find valuable resources on sites like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.

The Application Process: What to Expect

Once you’ve done your research and prepared your finances, the actual loan application process is relatively straightforward.

- Gathering Documents: Be ready to provide personal identification (driver’s license), proof of income (pay stubs, tax returns), proof of residence (utility bill), and potentially bank statements.

- Filling Out the Application: Whether online or in person, you’ll complete a form detailing your personal, employment, and financial information. Be honest and accurate.

- Waiting for a Decision: Lenders typically provide a decision within hours or a few business days. They will conduct a "hard inquiry" on your credit report, which can temporarily lower your score by a few points.

- Understanding the Loan Offer: Carefully review the loan amount, interest rate, loan term, and any associated fees. Don’t hesitate to ask questions for clarification.

Common Mistakes to Avoid During Your Car Loan Journey

From my vantage point, these errors can significantly derail your approval or lead to financial regret. Being aware of them can save you time, money, and stress.

- Applying to Too Many Lenders at Once: Each loan application results in a "hard inquiry" on your credit report. Too many hard inquiries in a short period can lower your credit score, making you seem desperate to lenders. Group your applications within a 14-45 day window so they count as a single inquiry for scoring purposes.

- Not Reading the Fine Print: Always read the entire loan agreement before signing. Understand all terms, conditions, and potential penalties. Don’t just skim the document.

- Overlooking Additional Fees: Be aware of any origination fees, documentation fees, or prepayment penalties. These can add to the overall cost of your loan.

- Buying More Car Than You Can Afford: It’s easy to get carried away at the dealership. Stick to your budget and don’t let a salesperson convince you to stretch beyond your comfortable monthly payment, even if you technically "get approved" for a higher amount.

Pro Tips for a Smooth Car Loan Experience

To ensure your car loan journey is as seamless and advantageous as possible, keep these expert tips in mind:

- Negotiate the Car Price Separately from the Loan: Always finalize the purchase price of the vehicle before discussing financing options. This prevents the dealership from moving numbers around to make it seem like you’re getting a good deal on one while losing out on the other.

- Shop Around for the Best Rates: Don’t settle for the first loan offer you receive. Compare interest rates and terms from multiple lenders – banks, credit unions, and online providers – to ensure you’re getting the most competitive deal.

- Understand the Total Cost of Ownership: Beyond the monthly loan payment, factor in insurance, fuel, maintenance, and potential registration fees. A low monthly car payment doesn’t mean the car is cheap to own. For more insights, check out our article on Smart Car Buying Strategies.

Conclusion: Drive Away with Confidence

Understanding "what car loan can I get approved for" is about more than just a quick yes or no. It’s about empowering yourself with knowledge of your financial standing and the lending process. By focusing on your credit score, managing your income and debt, preparing a down payment, and wisely choosing your vehicle and lender, you significantly increase your chances of securing favorable car loan approval.

The path to a new car doesn’t have to be daunting. With careful preparation, strategic planning, and an informed approach, you can confidently navigate the world of auto loans and drive away with a vehicle that fits both your needs and your budget. Remember, an informed borrower is a powerful borrower. Take control of your car buying journey today!