What Car Loan Would I Qualify For? Your Ultimate Guide to Auto Loan Eligibility

What Car Loan Would I Qualify For? Your Ultimate Guide to Auto Loan Eligibility Carloan.Guidemechanic.com

Dreaming of a new set of wheels but wondering if you can actually afford it? The journey to car ownership often begins with a crucial question: "What car loan would I qualify for?" This isn’t just a simple query; it’s the gateway to understanding your financial readiness and securing the best possible financing. Navigating the world of auto loans can seem daunting, but with the right knowledge, you can approach lenders with confidence and secure terms that fit your budget.

In this comprehensive guide, we’ll demystify the car loan qualification process, breaking down every factor lenders consider. We’ll explore how your financial profile impacts your eligibility, what steps you can take to strengthen your application, and common pitfalls to avoid. By the end, you’ll have a clear roadmap to securing the car loan you deserve. Let’s dive in and unlock the secrets to auto loan approval!

What Car Loan Would I Qualify For? Your Ultimate Guide to Auto Loan Eligibility

Understanding the Foundation: Key Factors Lenders Evaluate

When you apply for a car loan, lenders assess your financial health to determine your risk level. They want to ensure you have the capacity and willingness to repay the borrowed amount. Several key factors come into play, each contributing significantly to whether you’ll qualify and, crucially, what interest rate you’ll be offered.

The Unseen Score: Your Credit History and Score

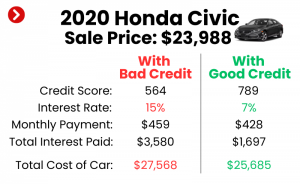

Your credit score is often the first thing lenders look at, and for good reason. It’s a three-digit number that summarizes your entire borrowing and repayment history, offering a snapshot of your financial responsibility. A higher score signals less risk to lenders.

Based on my experience as a financial expert, this is often the single most influential factor in car loan qualification. A strong credit score not only increases your chances of approval but also directly impacts the interest rate you’ll receive, potentially saving you thousands over the life of the loan.

What is a Credit Score?

Credit scores, like FICO and VantageScore, are calculated using various data points from your credit report. These include your payment history, the amount of debt you owe, the length of your credit history, new credit inquiries, and the types of credit you use. Each of these elements contributes to your overall score.

Your credit report, which forms the basis of your score, details every credit account you’ve ever had. It shows whether you’ve paid on time, how much you owe, and how long accounts have been open. Lenders use this information to predict your future payment behavior.

Credit Score Ranges and Their Impact on Car Loans

Credit scores typically range from 300 to 850, with different ranges indicating varying levels of creditworthiness:

- Excellent (780-850): Borrowers in this range qualify for the absolute best interest rates and loan terms. Lenders view them as very low risk.

- Good (670-779): These borrowers generally receive favorable rates and have a high chance of approval. They are considered reliable.

- Fair (580-669): Qualification is possible, but interest rates will be higher to compensate for the increased risk. More lenders might offer subprime loans.

- Poor (300-579): Getting approved for a traditional car loan can be challenging with a poor credit score. If approved, interest rates will be significantly higher, and terms might be less flexible.

How to Check Your Credit Score and Report

It’s crucial to know your credit standing before applying for a car loan. You can obtain a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, TransUnion) once every 12 months at AnnualCreditReport.com. Many credit card companies and banks also offer free credit score monitoring services.

Pro tips from us: Review your credit report carefully for any errors or inaccuracies. Disputing and correcting these can often boost your score, potentially improving your car loan qualification prospects. A clean report ensures lenders see your true financial picture.

Your Financial Backbone: Income and Employment Stability

Beyond your credit score, lenders need assurance that you have a steady and sufficient income to cover your monthly car loan payments. Your income and employment history demonstrate your ability to consistently make payments without financial strain. This is a fundamental aspect of determining what car loan you would qualify for.

Why Income Matters

Lenders use your income to calculate your debt-to-income ratio (which we’ll discuss next) and to simply ensure you earn enough to support the new debt. They want to see that your car payment, along with your other existing obligations, doesn’t consume too large a portion of your monthly earnings. A higher, stable income naturally makes you a more attractive borrower.

Types of Income Considered

Lenders typically consider various forms of verifiable income, including:

- Salary and Wages: This is the most common and straightforward type of income. Pay stubs and W-2s serve as proof.

- Self-Employment Income: If you’re self-employed, lenders will usually require tax returns (often for the past two years) to verify your income stability and average earnings.

- Retirement Income: Pensions, 401(k) distributions, and Social Security benefits are generally accepted.

- Disability Benefits: Long-term disability payments can be counted as income.

- Alimony or Child Support: These can be considered if they are consistent and court-ordered, though some lenders may be hesitant.

Employment History and Stability

Lenders prefer to see a consistent employment history, ideally with the same employer for at least two years. This indicates stability and a reliable income stream. Frequent job changes or gaps in employment can raise red flags, as they suggest potential instability in your earning capacity.

Common mistakes to avoid are applying for a loan right after starting a new job, especially if it’s in a different industry. While not always a deal-breaker, it can sometimes make lenders pause. If you’ve recently changed jobs, be prepared to provide a detailed explanation and demonstrate the new role’s stability and income potential.

Balancing the Books: Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is a critical metric that lenders use to assess your ability to manage monthly payments. It reveals how much of your gross monthly income is consumed by your existing debt obligations. A lower DTI indicates that you have more disposable income to take on new debt, making you a less risky borrower.

What is DTI?

Your DTI ratio is calculated by dividing your total monthly debt payments by your gross monthly income (before taxes and deductions). The result is expressed as a percentage. For example, if your total monthly debt payments (credit cards, student loans, mortgage, etc.) are $1,500 and your gross monthly income is $4,000, your DTI is $1,500 / $4,000 = 0.375 or 37.5%.

Why It’s Crucial

Lenders use DTI to gauge how much financial strain you’re under. A high DTI suggests that you’re already heavily burdened by debt, making it riskier for you to take on an additional car loan payment. This ratio helps them determine if you have enough wiggle room in your budget to comfortably afford a new monthly car payment.

Ideal DTI for Car Loans

While specific requirements vary by lender, a general guideline is that lenders prefer a DTI ratio below 40-45%. Some might even prefer it to be under 36% for prime borrowers. If your DTI is higher, you might still qualify, but you could face higher interest rates or stricter terms.

How to Calculate and Improve Your DTI

To calculate your DTI, sum up all your recurring monthly debt payments:

- Credit card minimum payments

- Student loan payments

- Mortgage or rent payments

- Personal loan payments

- Any other recurring loan payments

Then, divide that total by your gross monthly income.

To improve your DTI, you can:

- Reduce Existing Debt: Pay down credit card balances or other loans to lower your monthly debt obligations.

- Increase Your Income: While not always immediately feasible, finding ways to boost your gross income will directly lower your DTI.

- Avoid Taking on New Debt: Before applying for a car loan, refrain from opening new credit cards or taking out other loans that would increase your monthly debt.

Your Upfront Investment: The Down Payment

A down payment is the initial amount of money you pay upfront when purchasing a vehicle. It reduces the total amount you need to borrow, directly impacting your loan terms and overall qualification. Lenders view a significant down payment favorably, as it demonstrates your financial commitment and reduces their risk.

Benefits of a Down Payment

- Lower Loan Amount: The more you pay upfront, the less you need to finance, leading to smaller monthly payments.

- Reduced Interest Paid: A smaller loan balance means you’ll pay less interest over the life of the loan.

- Better Loan Terms: Lenders are more likely to offer lower interest rates and more flexible terms to borrowers who make a substantial down payment.

- Reduced Loan-to-Value (LTV) Ratio: LTV compares the loan amount to the car’s value. A lower LTV means less risk for the lender, as there’s more equity in the vehicle from the start.

- Protection Against Negative Equity: Cars depreciate rapidly. A down payment helps prevent you from owing more than the car is worth, a situation known as being "upside down" on your loan.

Recommended Down Payment

While any down payment is better than none, generally, financial experts recommend:

- New Cars: Aim for at least 10-20% of the vehicle’s purchase price.

- Used Cars: Consider putting down 20% or more, as used cars tend to depreciate faster and may have a higher risk of mechanical issues.

Pro tips from us: Saving aggressively for a down payment is one of the smartest financial moves you can make when buying a car. It not only improves your qualification chances but also significantly reduces your long-term costs.

The Vehicle Itself: Age, Make, Model, and Value

It might surprise you, but the specific car you intend to purchase also plays a role in what car loan you would qualify for. Lenders don’t just assess you; they also assess the collateral – the vehicle itself. The car’s characteristics influence the perceived risk and its value as security for the loan.

Why the Car Matters (Collateral)

In a secured loan like an auto loan, the vehicle serves as collateral. If you default on your payments, the lender can repossess and sell the car to recover their losses. Therefore, lenders are keen on the car’s market value and how well it holds that value over time. They want to ensure the car’s value adequately covers the loan amount.

Impact on Loan Terms and Approval

- New vs. Used Cars: New cars generally qualify for lower interest rates and longer loan terms due to their higher initial value and perceived reliability. Used cars, especially older ones or those with high mileage, might come with higher rates and shorter terms, as their depreciation rate is higher and mechanical risks are greater.

- Make and Model: Certain brands and models retain their value better than others. Lenders are more comfortable financing vehicles with a strong resale market, as they are easier to sell if repossession becomes necessary.

- Loan-to-Value (LTV) Ratio Revisited: This ratio is crucial. It compares the amount you’re borrowing to the car’s actual market value. A high LTV (e.g., borrowing 120% of the car’s value, which can happen if you roll negative equity from a trade-in into a new loan) makes the loan riskier for the lender. A lower LTV, often achieved with a substantial down payment, improves your qualification.

Lenders might have specific restrictions on the age or mileage of vehicles they are willing to finance. For instance, some may not finance cars older than 10 years or with more than 100,000 miles. Always check these criteria before falling in love with a specific older model.

Boosting Your Chances: Strategies for Stronger Qualification

Understanding the factors lenders consider is the first step. The next is proactively strengthening your financial profile to improve your chances of approval and secure the best possible terms. These strategies can make a significant difference in what car loan you would qualify for.

Pre-Approval: Your Secret Weapon

Pre-approval is a powerful tool that puts you in a much stronger position when shopping for a car. It involves getting a conditional loan offer from a lender before you even set foot in a dealership. This process provides you with a clear understanding of what car loan you would qualify for in terms of loan amount and interest rate.

What is Pre-Approval?

During pre-approval, a lender reviews your credit, income, and DTI ratio. If approved, they’ll issue a letter stating the maximum amount you can borrow and the estimated interest rate, often valid for a specific period (e.g., 30-60 days). This is a "soft inquiry" on your credit, meaning it won’t significantly impact your score.

Benefits of Pre-Approval

- Negotiating Power: Armed with a pre-approval, you become a cash buyer in the eyes of the dealership. This allows you to negotiate the car’s price more effectively, separate from the financing.

- Realistic Budget: You’ll know exactly how much car you can afford before you start shopping, preventing you from falling in love with a vehicle outside your budget.

- Identifies Issues Early: If you’re denied pre-approval, you’ll understand why, giving you time to address any credit or income issues before committing to a specific car.

- Saves Time: You can streamline the car-buying process, as financing is already largely handled.

How to Get Pre-Approved

Contact banks, credit unions, and online lenders directly to inquire about their pre-approval process. Compare offers from multiple lenders to find the most competitive rates and terms. This comparison shopping within a short window (usually 14-45 days) counts as a single hard inquiry on your credit, minimizing impact.

Improving Your Credit Score (Before You Apply)

If your credit score isn’t where you want it to be, taking steps to improve it before applying for a car loan can significantly enhance your qualification. Even a modest increase can lead to better interest rates. For a deeper dive into improving your credit score, check out our comprehensive guide on .

Here are key strategies:

- Pay Bills On Time, Every Time: Payment history is the most significant factor in your credit score. Set up reminders or automatic payments to avoid missing due dates.

- Reduce Existing Debt: Pay down credit card balances to lower your credit utilization ratio (the amount of credit you’re using compared to your total available credit). Aim to keep this ratio below 30%.

- Dispute Errors on Your Credit Report: Regularly check your credit reports for inaccuracies. If you find any, dispute them immediately with the credit bureau. Errors can unfairly lower your score.

- Avoid New Credit Applications: Refrain from opening new credit accounts in the months leading up to your car loan application. Each new application results in a hard inquiry, which can temporarily ding your score.

- Maintain Low Credit Utilization: Keep your credit card balances as low as possible relative to your credit limits. This demonstrates responsible credit management.

The Power of a Co-Signer

If your credit isn’t strong enough or your income is borderline, a co-signer can be a valuable asset. A co-signer is someone with good credit and a stable financial history who agrees to be equally responsible for the loan if you cannot make payments.

When It’s Useful

- Poor Credit History: A co-signer can help you qualify for a loan you otherwise wouldn’t get.

- Limited Credit History: First-time buyers or young adults with little to no credit history can benefit greatly from a co-signer.

- Low Income: If your income alone isn’t sufficient to meet lender requirements, a co-signer’s income can bolster the application.

Risks for the Co-Signer

While beneficial for the primary borrower, co-signing carries significant risks:

- Equal Responsibility: The co-signer is legally obligated to repay the loan if the primary borrower defaults.

- Credit Impact: The loan appears on the co-signer’s credit report, impacting their DTI and credit score, especially if payments are missed.

- Strained Relationships: If the primary borrower struggles to pay, it can severely strain the relationship with the co-signer.

It’s vital for both parties to understand the full implications before entering a co-signing agreement.

Considering Different Lender Types

Not all lenders are created equal, and where you apply for a car loan can significantly impact your approval odds and the terms you receive. Exploring various lender types can help you find the best fit for your financial situation.

- Banks: Traditional banks offer a wide range of auto loan products, often competitive rates for borrowers with good credit. They have established processes and often offer online applications.

- Credit Unions: These member-owned financial institutions are known for offering competitive interest rates and more flexible terms, especially for members. From my experience, credit unions often offer competitive rates to a broader range of credit profiles compared to large banks.

- Dealership Financing: Dealerships act as intermediaries, working with multiple lenders (both captive lenders like Toyota Financial Services and third-party banks) to find you financing. While convenient, always compare their offers to those you’ve secured independently.

- Online Lenders: A growing number of online-only lenders specialize in auto loans. They often offer quick pre-approvals and competitive rates, sometimes catering to specific credit tiers (e.g., bad credit auto loans).

Pro tips from us: Always shop around and compare at least three to five loan offers. This competition ensures you get the most favorable interest rate and terms for which you qualify.

Navigating Special Situations

Not everyone has a perfect credit score or a long, pristine financial history. Fortunately, there are still pathways to car ownership for those in specific circumstances.

Qualifying for a Car Loan with Bad Credit

If you have a low credit score (generally below 620), qualifying for a traditional car loan can be challenging. However, it’s not impossible. The key is to have realistic expectations and target the right lenders.

- Realistic Expectations: Expect higher interest rates, potentially shorter loan terms, and a requirement for a larger down payment. Lenders view bad credit as a higher risk, and the interest rate reflects that.

- Subprime Lenders: These lenders specialize in working with borrowers who have less-than-perfect credit. While their rates are higher, they are often more willing to approve loans for individuals who have been turned down elsewhere.

- Secured Loans or Buy-Here-Pay-Here: Some lenders offer secured loans that require collateral beyond the car itself, or "buy-here-pay-here" dealerships that finance directly, often at very high interest rates. Exercise extreme caution with these options due to predatory potential.

- Focus on Improving Credit for the Future: Use this loan as an opportunity to rebuild your credit. Make all payments on time, and your score will gradually improve, paving the way for better rates on future loans.

First-Time Car Buyer Loans

If you’re a first-time car buyer with little to no credit history, qualifying can be tricky because lenders lack data to assess your risk. However, many lenders offer specific programs designed for first-time buyers.

- Specific Programs: Many banks and credit unions have programs tailored for first-time buyers, sometimes with slightly relaxed credit requirements if you meet other criteria (e.g., stable employment, down payment).

- Importance of Building Credit History: If you have no credit, consider getting a secured credit card or a small credit-builder loan a few months before applying for a car loan. This establishes a payment history.

- Co-Signer Option: As mentioned, a co-signer with good credit can significantly boost your chances of approval and help you secure a better interest rate.

The Application Process: What to Expect

Once you’ve done your homework and understand what car loan you would qualify for, the actual application process is relatively straightforward. Being prepared can make it even smoother.

-

Gathering Documents: Lenders will ask for documentation to verify your identity, income, and residence. This typically includes:

- Government-issued ID (driver’s license)

- Proof of income (pay stubs, W-2s, tax returns)

- Proof of residence (utility bill, lease agreement)

- Social Security number

- Trade-in title (if applicable)

-

Filling Out the Application: You’ll complete a detailed application providing personal, employment, and financial information. Be honest and accurate, as lenders will verify the details.

-

Understanding the Loan Offer: If approved, you’ll receive a loan offer outlining the Annual Percentage Rate (APR), the loan term (number of months), and your estimated monthly payment. The APR includes both the interest rate and any fees, giving you the true cost of borrowing.

-

Reading the Fine Print: Before signing, carefully review all terms and conditions. Understand any prepayment penalties, late fees, and what happens if you miss a payment. Don’t hesitate to ask questions.

Common Pitfalls to Avoid

Even with all the right information, it’s easy to make mistakes that can hinder your car loan qualification or lead to unfavorable terms. Awareness is your best defense.

Don’t Make These Mistakes When Applying for a Car Loan

- Applying Everywhere: Each car loan application typically results in a "hard inquiry" on your credit report, which can temporarily lower your score. While multiple inquiries for the same type of loan within a short period (usually 14-45 days) are often grouped as one for scoring purposes, spreading them out over months can be detrimental. Focus on getting pre-approved from a few reputable lenders.

- Not Checking Your Credit First: Going into the process blind is a common mistake. You won’t know your standing or if there are errors until it’s too late. Always check your credit report and score before you apply.

- Overstretching Your Budget: It’s tempting to buy more car than you can comfortably afford. Remember to factor in not just the monthly loan payment, but also insurance, fuel, maintenance, and potential repairs. One common mistake I’ve seen is buyers focusing solely on the monthly payment without considering the total cost of ownership. For an in-depth look at this, read our article on .

- Ignoring the Total Cost of Ownership: Beyond the loan, cars come with ongoing expenses. Don’t forget to budget for gas, insurance, registration, routine maintenance, and potential repairs. These costs can quickly add up and strain your budget.

- Falling for Predatory Loans: Be wary of "guaranteed approval" lenders or those promising exceptionally low rates without checking your credit. If an offer seems too good to be true, it likely is. Always research lenders thoroughly and read reviews.

Conclusion: Empowering Your Car Loan Journey

Understanding "What car loan would I qualify for" is the essential first step towards driving away in your next vehicle. By focusing on your credit score, income stability, debt-to-income ratio, and making a solid down payment, you can significantly enhance your position as a borrower. Remember, knowledge is power in the car-buying process.

Take the time to check your credit, get pre-approved, and compare offers from various lenders. By being proactive and informed, you not only increase your chances of approval but also secure the most favorable terms, saving you money and stress in the long run. Drive confidently into your car-buying journey, knowing you’re well-equipped to qualify for the car loan that fits your needs.