What Is A Good Credit Score For A Car Loan? Your Ultimate Guide to Driving Away with the Best Deal

What Is A Good Credit Score For A Car Loan? Your Ultimate Guide to Driving Away with the Best Deal Carloan.Guidemechanic.com

Driving a new (or new-to-you) car off the lot is an exciting milestone. But before you can feel the thrill of the open road, there’s a crucial step: securing a car loan. And at the heart of that process lies your credit score. Many aspiring car owners wonder, "What is a good credit score for a car loan?"

This isn’t just a simple number; it’s a powerful indicator that can dramatically influence the terms of your auto financing. From the interest rate you pay to the size of your monthly payments, your credit score holds significant sway. Understanding this number and how lenders perceive it is your first step towards unlocking the best possible deal.

What Is A Good Credit Score For A Car Loan? Your Ultimate Guide to Driving Away with the Best Deal

In this comprehensive guide, we’ll dive deep into what constitutes a "good" credit score for a car loan. We’ll explore why it matters so much, how to find your score, strategies to improve it, and what options are available if your score isn’t quite where you’d like it to be. Our goal is to empower you with the knowledge to navigate the auto loan landscape confidently and secure financing that fits your budget.

Unpacking the Fundamentals: What Exactly is a Credit Score?

Before we define what’s "good," let’s ensure we’re all on the same page about what a credit score actually is. Simply put, a credit score is a three-digit number that represents your creditworthiness to lenders. It’s a quick snapshot of your financial history and how reliably you’ve managed debt in the past.

The most commonly used credit scores are FICO Scores and VantageScores. While they use slightly different algorithms, both aim to predict how likely you are to repay borrowed money. They factor in aspects like your payment history, the amount of debt you owe, the length of your credit history, and your credit mix.

Lenders rely heavily on these scores to assess risk. A higher score signals to them that you are a responsible borrower and are less likely to default on a loan. Conversely, a lower score suggests a higher risk, which often translates into less favorable loan terms or even denial.

Defining "Good": What’s the Ideal Credit Score Range for a Car Loan?

When it comes to car loans, what constitutes a "good" credit score can vary slightly between lenders and economic conditions. However, based on my experience in the automotive finance industry, there’s a widely accepted range that opens the door to competitive rates and favorable terms.

Generally, a FICO Score of 660 or higher is often considered "good" for an auto loan. If your score falls into this category, you’re likely to qualify for standard interest rates and have a decent selection of lenders to choose from. However, to unlock the absolute best rates and terms, you’ll want to aim even higher.

Let’s break down the typical credit score tiers and what they mean for your car loan prospects:

Excellent Credit: 780-850

Borrowers with excellent credit are the cream of the crop. This score range indicates a stellar payment history, low credit utilization, and a long track record of responsible borrowing. Lenders view these applicants as extremely low risk.

If your score is in this range, you can expect to qualify for the absolute lowest interest rates available. This means significant savings over the life of your loan and the most flexible terms. You’ll also likely have your pick of lenders and vehicle options.

Very Good Credit: 740-779

While not quite perfect, a very good credit score is still highly desirable. It demonstrates a strong history of financial responsibility and reliability. You’re considered a low-risk borrower by most auto lenders.

With a score in this range, you’ll still qualify for excellent interest rates, very close to those with excellent credit. Your loan terms will be highly favorable, and you’ll have ample choice when it comes to financing options.

Good Credit: 670-739

This is the sweet spot for many car buyers. A "good" credit score indicates a solid track record of managing credit responsibly, though there might be a minor hiccup or two in your past. Lenders are generally comfortable approving loans for individuals in this range.

If your score falls within the good range, you’ll typically qualify for competitive interest rates, though they might be slightly higher than those with excellent or very good credit. You’ll have access to a wide array of loan products and won’t face significant hurdles in getting approved.

Fair Credit: 580-669

Borrowers with fair credit present a moderate risk to lenders. This range often reflects some past credit challenges, such as late payments or higher credit utilization. While it’s tougher to get the absolute best rates, securing a car loan is still very possible.

If your credit is fair, expect to pay higher interest rates compared to those with good or excellent credit. Lenders might also require a larger down payment or offer less flexible terms. It’s crucial to shop around and compare offers if you’re in this category.

Poor Credit: 300-579

A poor credit score indicates a significant history of financial difficulties, including defaults, bankruptcies, or numerous late payments. Lenders consider these applicants high risk, making it challenging to secure traditional auto loans.

While getting a car loan with poor credit is difficult, it’s not impossible. You’ll likely face very high interest rates, require a substantial down payment, and may need a co-signer. Subprime lenders specialize in this area, but their terms are significantly less favorable.

Why Your Credit Score Is Absolutely Crucial for Car Loans

Your credit score isn’t just a number; it’s a powerful tool that dictates the cost and accessibility of your car loan. Understanding its impact can save you thousands of dollars and a lot of frustration.

From years of observing loan applications, I can tell you that the difference a few points on your credit score can make is truly astounding. It’s not just about getting approved; it’s about getting approved on your terms, not the lender’s.

1. The Gateway to Lower Interest Rates

This is arguably the most significant impact of your credit score. A higher score tells lenders you’re a reliable borrower, meaning they see less risk in lending to you. In return, they offer lower interest rates. A lower interest rate translates directly into less money paid over the life of the loan.

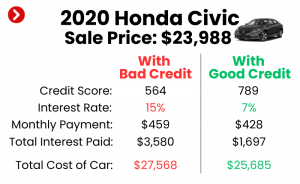

Even a difference of a few percentage points can mean thousands of dollars saved. For example, on a $30,000 car loan over 60 months, the difference between a 4% and an 8% interest rate could be over $3,000 in total interest paid.

2. Influences Your Monthly Payment

Naturally, a lower interest rate directly leads to a lower monthly payment. This makes budgeting easier and frees up more money for other expenses. Conversely, a higher interest rate from a lower credit score will inflate your monthly payments, potentially straining your finances.

This is why aiming for the best possible credit score before applying is a smart financial move. It directly impacts your ongoing financial commitment.

3. Determines Your Chances of Approval

Lenders use your credit score as a primary filter for loan applications. While other factors play a role, a strong credit score significantly increases your chances of outright approval. You’ll have more lenders willing to work with you.

With a lower score, you might face outright rejections from traditional lenders. This forces you to explore subprime options, which come with their own set of challenges.

4. Affects Loan Terms and Flexibility

Beyond interest rates, your credit score can influence other loan terms. With excellent credit, you might qualify for longer loan terms without a huge jump in interest, or even receive special promotional rates. Lenders may also be more flexible regarding down payment requirements.

For those with lower scores, lenders might impose stricter terms. This could include shorter loan terms (leading to higher monthly payments), mandatory larger down payments, or specific vehicle restrictions.

5. Can Impact Down Payment Requirements

While not always a direct correlation, a higher credit score can often reduce the required down payment. Lenders are more confident in your ability to repay, so they don’t need as much upfront capital to mitigate their risk.

Conversely, if you have a lower credit score, lenders might require a substantial down payment to approve your loan. This reduces the loan amount and their exposure to potential default.

Beyond the Score: Other Factors Lenders Consider

While your credit score is undeniably central to the car loan process, it’s not the only thing lenders look at. They want a holistic view of your financial health to make an informed decision. Based on my experience, these additional factors can significantly sway their approval decision and the terms they offer.

It’s crucial to present the strongest overall financial picture possible. Your credit score gets your foot in the door, but these other elements help seal the deal.

1. Debt-to-Income Ratio (DTI)

Your DTI ratio is a percentage that compares your total monthly debt payments to your gross monthly income. Lenders use it to assess your ability to manage monthly payments and take on additional debt. A lower DTI indicates you have more disposable income to cover new loan payments.

Generally, lenders prefer a DTI of 36% or lower, though some auto lenders might go up to 43-50%. If your DTI is too high, it signals that you might already be stretched too thin financially, regardless of your credit score.

2. Loan-to-Value Ratio (LTV)

The LTV ratio compares the amount you want to borrow to the actual value of the car you’re purchasing. If you’re borrowing more than the car is worth, you have a high LTV, which can be seen as risky by lenders. This often happens if you roll negative equity from a trade-in into a new loan.

A lower LTV (meaning you’re borrowing less relative to the car’s value, often achieved with a larger down payment) makes your loan more attractive to lenders. It reduces their risk in case of default.

3. Employment History and Stability

Lenders want to see a stable source of income. They’ll typically look for consistent employment for at least two years. A steady job history indicates reliability and a continuous ability to make loan payments. Frequent job changes or gaps in employment can raise red flags.

Providing proof of income, such as pay stubs or tax returns, is a standard part of the application process. This helps them verify your ability to pay.

4. Down Payment Amount

The size of your down payment is a significant factor. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. It also shows your commitment to the purchase and your financial stability.

Pro tips from us: Aim for at least 10-20% of the car’s purchase price as a down payment if possible. This not only makes your application more appealing but also reduces your monthly payments and the total interest paid.

5. Vehicle Age and Type

The car itself also plays a role. Newer, more reliable vehicles often qualify for better loan terms because they hold their value better and are less likely to break down, leaving you with a non-functional asset. Older cars, or those with very high mileage, might be seen as higher risk.

Certain specialty or luxury vehicles might also be subject to different lending criteria. Lenders consider the resale value of the car as collateral.

How to Find Out Your Credit Score

Knowing your credit score is the essential first step before even thinking about a car loan. You can’t improve what you don’t know! Fortunately, accessing your credit score is easier and more accessible than ever before.

Don’t guess; get the actual numbers. It’s a quick process that provides valuable insight into your financial standing.

1. AnnualCreditReport.com

You are legally entitled to one free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) every 12 months. While these reports don’t always include your score, they provide all the underlying data that calculates your score. Reviewing these reports is crucial for accuracy.

You can request all three reports at once or space them out throughout the year. Checking them helps you spot errors that could be dragging down your score.

2. Credit Monitoring Services

Many websites offer free credit scores and credit monitoring services. Popular options include Credit Karma (VantageScore), Credit Sesame, and NerdWallet. Your bank or credit card company might also provide free FICO scores as a benefit.

These services are excellent for regularly tracking your score and understanding the factors influencing it. Remember that the score they provide might be a VantageScore, which can differ slightly from the FICO Score most auto lenders use.

3. Directly from FICO

You can purchase your FICO Score directly from MyFICO.com. This ensures you’re seeing the same score models that lenders use. While there’s a fee, it can be worth it if you want the most accurate picture before a major loan application.

Some credit card companies, like Discover or Chase, also offer free FICO scores to their cardholders, often directly on your monthly statement or online portal.

Pro Tips: Improving Your Credit Score Before Applying

If your credit score isn’t quite in the "good" or "excellent" range, don’t despair! There are actionable steps you can take to boost it before you apply for a car loan. A few months of diligent effort can make a significant difference in your loan terms.

Based on my experience, even a 30-50 point increase can shift you into a better rate tier, saving you hundreds or even thousands. It’s an investment in your financial future.

1. Pay Your Bills On Time, Every Time

Payment history is the most significant factor in your credit score, accounting for about 35% of your FICO Score. Even one late payment can have a substantial negative impact. Set up automatic payments or reminders to ensure you never miss a due date.

Consistency is key here. A long history of on-time payments demonstrates reliability to lenders.

2. Reduce Your Credit Utilization Ratio

Your credit utilization is the amount of credit you’re using compared to your total available credit. For example, if you have a credit card with a $5,000 limit and a $2,000 balance, your utilization is 40%. Experts recommend keeping this ratio below 30%, and ideally even lower (10% or less) for the best scores.

Paying down credit card balances is one of the quickest ways to see a positive impact on your score. It shows you’re not overly reliant on borrowed money.

3. Avoid Opening New Credit Accounts

While you’re planning to apply for a car loan, resist the urge to open new credit cards or take out other loans. Each new application results in a "hard inquiry" on your credit report, which can temporarily ding your score. New accounts also lower the average age of your credit history.

It’s best to keep your credit profile stable in the months leading up to a major loan application.

4. Check Your Credit Report for Errors

Mistakes on your credit report are surprisingly common and can unfairly drag down your score. Regularly review your reports from all three bureaus for inaccuracies, such as accounts that aren’t yours, incorrect payment statuses, or outdated negative information.

If you find an error, dispute it immediately with the credit bureau. Correcting inaccuracies can lead to a quick score boost.

5. Become an Authorized User (Carefully)

If you have a trusted family member with excellent credit and a long history of on-time payments, they might add you as an authorized user on one of their credit cards. Their positive payment history could then appear on your credit report, boosting your score.

However, this strategy should be used with caution. Ensure the primary cardholder is financially responsible, as their mistakes could also affect your score.

6. Consider a Secured Credit Card or Credit-Builder Loan

If you have very limited or poor credit, a secured credit card can be a great tool. You deposit money into an account, and that deposit acts as your credit limit. By using the card responsibly and paying on time, you build positive credit history.

A credit-builder loan works similarly. You take out a small loan, but the money is held in a savings account until you’ve paid off the loan. Your on-time payments are reported to credit bureaus, establishing good credit.

What If Your Credit Score Isn’t "Good"? Options for Fair/Poor Credit

Even if your credit score isn’t in the ideal range, getting a car loan is still possible. It might require a different approach, more research, and potentially higher costs, but don’t give up on your car ownership dreams. Common mistakes to avoid are settling for the first offer you receive and not exploring all your options.

It’s about being strategic and understanding the landscape of financing for less-than-perfect credit. Here are some avenues to explore:

1. Explore Subprime Lenders

These lenders specialize in working with individuals who have fair or poor credit scores. They are willing to take on higher risk, but in exchange, they charge significantly higher interest rates. You might also find less flexible terms.

While they can be a lifeline, it’s crucial to compare offers from multiple subprime lenders to ensure you’re getting the most reasonable terms available for your situation. Be wary of predatory rates.

2. Consider a Co-signer

A co-signer is someone with good or excellent credit who agrees to take legal responsibility for the loan if you fail to make payments. Their strong credit profile can help you get approved and potentially secure a better interest rate.

This is a serious commitment for the co-signer, as their credit will also be affected if you miss payments. Ensure both parties understand the risks and responsibilities involved.

3. Make a Larger Down Payment

A substantial down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. If you can put down 20% or more, you’ll be a more attractive applicant, even with a lower credit score.

This shows commitment and reduces the LTV ratio, making the loan less risky for the lender. It also directly lowers your monthly payments.

4. Opt for a Less Expensive or Older Car

Borrowing less money inherently reduces the risk for lenders. If your credit is challenging, consider purchasing a more affordable used car rather than a brand-new model. The lower loan amount might make approval easier.

An older, more budget-friendly car can also serve as a stepping stone. You can use it to build your credit with on-time payments, then upgrade later.

5. Check with Credit Unions

Credit unions are member-owned financial institutions known for their customer-centric approach. They often have more flexible lending criteria and may be more willing to work with members who have fair credit, sometimes offering better rates than traditional banks.

If you’re eligible to join a credit union, it’s definitely worth exploring their auto loan options.

6. Secured Car Loans

Some lenders offer secured car loans, where the car itself acts as collateral. This reduces the lender’s risk, making them more likely to approve applicants with lower credit scores. However, be aware that if you default, the car can be repossessed.

While this is an option, it’s often a last resort due to the high risk involved. Always understand the terms fully.

The Power of Pre-Approval: A Smart Move

Before you even step foot on a car dealership lot, getting pre-approved for a car loan is one of the smartest strategies you can employ. It transforms you from a casual browser into a powerful, informed buyer.

Based on my experience, car buyers who arrive with pre-approval in hand have significantly more negotiating leverage. It puts you in the driver’s seat of the buying process.

What is Pre-Approval?

Pre-approval is when a lender reviews your credit and financial information and tentatively agrees to lend you a specific amount of money at a certain interest rate. This is usually based on a "soft inquiry" into your credit, which doesn’t negatively impact your score.

You’ll receive a pre-approval letter stating the loan amount, interest rate, and terms. This letter is your financial firepower when you go car shopping.

Benefits of Pre-Approval:

- Know Your Budget: You’ll know exactly how much you can afford, preventing you from falling in love with a car outside your price range. This brings clarity to your search.

- Negotiating Power: With a pre-approval, you’re essentially walking into the dealership with cash in hand. You can negotiate the car’s price based on the best financing you’ve already secured, rather than letting the dealer dictate terms.

- Focus on the Car, Not the Loan: You can concentrate on finding the right vehicle for your needs and budget, knowing your financing is already in place. This simplifies the buying process.

- Spot Bad Deals: If the dealership tries to offer you a higher interest rate than your pre-approval, you’ll immediately know it’s not a good deal. It provides a benchmark.

- Hard Inquiry Timing: When you get pre-approved, lenders perform a soft inquiry. Once you’re ready to finalize, a hard inquiry is made. Doing all your car loan shopping within a 14-45 day window (depending on the credit scoring model) means multiple hard inquiries for the same type of loan will typically only count as one for your score.

Comparing Loan Offers: Look Beyond the Interest Rate

Once you have multiple loan offers (ideally from pre-approvals), it’s tempting to just pick the one with the lowest interest rate. However, a truly savvy car buyer looks at the bigger picture.

Pro tips from us: Always compare the total cost of the loan, not just the monthly payment or interest rate in isolation.

1. Annual Percentage Rate (APR) vs. Interest Rate

The interest rate is the cost of borrowing money, expressed as a percentage. The APR (Annual Percentage Rate) includes the interest rate plus any additional fees associated with the loan, such as origination fees or application fees. The APR gives you a more accurate representation of the total annual cost of your loan.

Always compare APRs when evaluating different loan offers to get a true apples-to-apples comparison.

2. Loan Term

The loan term is the length of time you have to repay the loan (e.g., 36, 48, 60, or 72 months). A longer loan term generally means lower monthly payments but results in paying more interest over the life of the loan. A shorter term means higher monthly payments but less overall interest.

Choose a loan term that balances affordability with the total cost. Don’t extend the term unnecessarily just to lower the monthly payment if you can comfortably afford a shorter one.

3. Fees and Charges

Read the fine print for any hidden fees. These could include application fees, documentation fees, prepayment penalties (though less common for auto loans), or late payment fees. These can add to the overall cost of your loan.

Ensure you understand every charge before signing the loan agreement.

4. Total Cost of the Loan

The best way to compare offers is to calculate the total amount you will pay back over the entire loan term, including interest and fees. This gives you the clearest picture of which loan is truly the most economical.

Conclusion: Drive Towards Financial Confidence

Understanding "what is a good credit score for a car loan" is far more than just knowing a number. It’s about empowering yourself with knowledge that can save you significant money and stress when purchasing a vehicle. A strong credit score is your ticket to lower interest rates, more flexible terms, and a smoother buying experience.

By actively monitoring your credit, taking steps to improve it, and leveraging strategies like pre-approval, you put yourself in a prime position to secure the best possible auto loan. Even if your credit isn’t perfect, there are pathways to car ownership, especially if you’re proactive and informed.

Remember, your credit score is a dynamic entity. With consistent, responsible financial habits, you can steadily improve it over time, opening doors to even better financial opportunities in the future. Don’t let uncertainty hold you back; take control of your credit and drive away with confidence.

For more information on credit scores and reports, visit the Consumer Financial Protection Bureau (CFPB) website.