What Kind Of Car Loan Can I Afford? Your Ultimate Guide to Smart Car Financing

What Kind Of Car Loan Can I Afford? Your Ultimate Guide to Smart Car Financing Carloan.Guidemechanic.com

Buying a car is an exciting milestone for many, but the journey to securing the right car loan can often feel overwhelming. It’s not just about finding a vehicle you love; it’s about understanding what you can truly afford without straining your finances. Many people fall into the trap of focusing solely on the monthly payment, overlooking the bigger financial picture.

As an expert in personal finance and auto lending, I’ve seen countless individuals navigate the complexities of car financing. My mission today is to equip you with the knowledge and tools to confidently answer the crucial question: "What kind of car loan can I afford?" This comprehensive guide will delve deep into every aspect of car loan affordability, ensuring you make a decision that benefits your long-term financial health. Let’s get started on paving your path to a smart car purchase.

What Kind Of Car Loan Can I Afford? Your Ultimate Guide to Smart Car Financing

The Foundation: Understanding Your Financial Health

Before you even start browsing dealerships or dreaming of a new ride, the first and most critical step is to take an honest look at your current financial situation. This isn’t just a suggestion; it’s the bedrock of responsible car ownership. Lenders will scrutinize these very same factors, so understanding them yourself gives you a significant advantage.

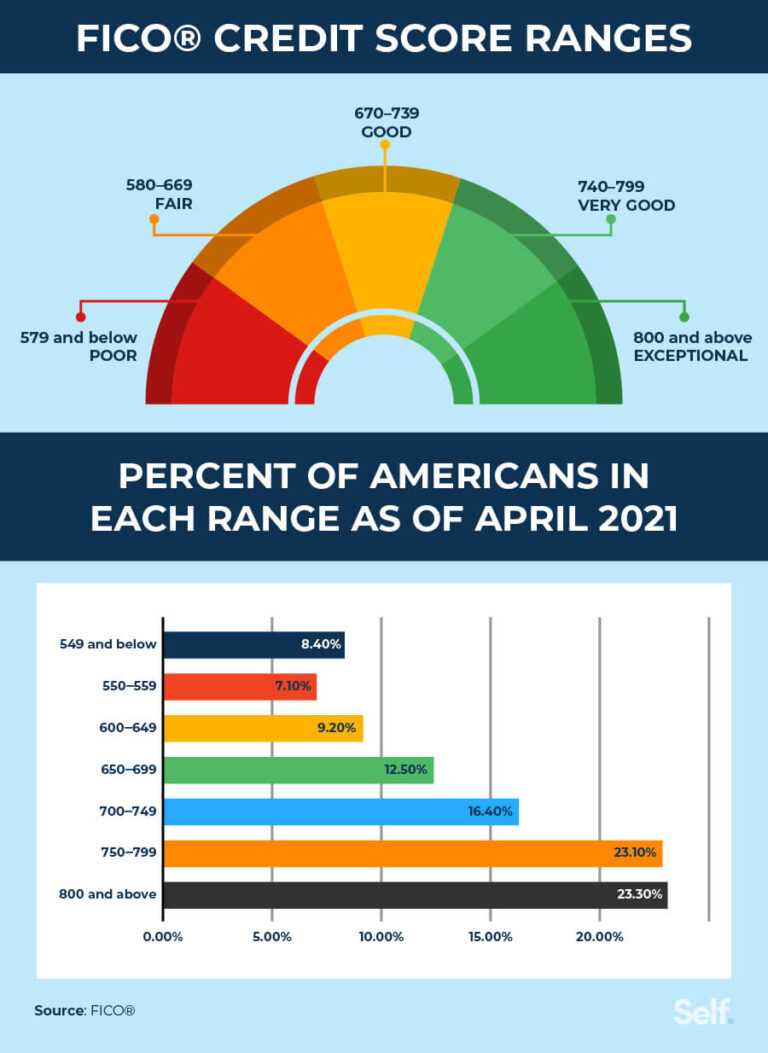

Your Credit Score: The Ultimate Financial Report Card

Your credit score is arguably the single most influential factor in determining the interest rate you’ll be offered on a car loan. It’s a three-digit number that summarizes your creditworthiness, reflecting your history of borrowing and repaying debt. A higher score typically translates to lower interest rates, saving you thousands over the life of the loan.

Based on my experience, many people underestimate the power of their credit score. A difference of even a few points can shift you into a different interest rate tier. Lenders view a strong credit score (generally 700+) as an indicator of a responsible borrower, making them more willing to offer favorable terms.

You should check your credit score and report well in advance of applying for a car loan. Websites like AnnualCreditReport.com allow you to get a free copy of your credit report from each of the three major bureaus (Equifax, Experian, TransUnion) once a year. Review it for any errors or discrepancies that could be dragging your score down. If you find errors, dispute them immediately.

Your Debt-to-Income (DTI) Ratio: What Lenders Really See

Beyond your credit score, lenders pay close attention to your debt-to-income (DTI) ratio. This percentage compares your total monthly debt payments to your gross monthly income. It tells lenders how much of your income is already committed to other financial obligations, indicating your capacity to take on new debt, like a car loan.

To calculate your DTI, simply add up all your recurring monthly debt payments – this includes student loans, credit card minimums, mortgage or rent payments, and any other loan payments. Then, divide that sum by your gross monthly income (your income before taxes and deductions). For example, if your total monthly debt is $1,500 and your gross monthly income is $5,000, your DTI is 30% ($1,500 / $5,000).

Pro tips from us: Lenders generally prefer a DTI ratio below 36%, although some may approve loans with a DTI up to 43% for well-qualified borrowers. A lower DTI signifies less financial risk. If your DTI is high, consider paying down existing debts or increasing your income before applying for a car loan. This proactive step can significantly improve your chances of loan approval and securing better terms.

Income Stability: A Consistent Paycheck Matters

Lenders want to see a stable and consistent income. They need assurance that you have the means to make your car loan payments reliably over the long term. This often means having a steady job history, ideally with the same employer for at least two years.

Self-employed individuals or those with variable income may need to provide more extensive documentation, such as tax returns for the past two years, to demonstrate income consistency. The key is to show a reliable stream of funds that can comfortably cover your future car loan payments alongside your other expenses.

The Core Calculation: How Much Can You Really Afford?

Once you have a clear picture of your financial health, it’s time to translate that into a concrete budget for your car. This goes far beyond just looking at a potential monthly payment. To truly understand "what kind of car loan can I afford," you need a holistic approach that considers all associated costs.

The 20/4/10 Rule: A Golden Guideline for Car Buying

While not a strict rule, the "20/4/10" guideline is an excellent starting point for responsible car budgeting. It helps ensure you don’t overextend yourself financially and account for more than just the car’s price. Let’s break down what each number means:

- 20% Down Payment: Aim to put down at least 20% of the car’s purchase price. A substantial down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the loan term. For used cars, a 10% down payment might be acceptable, but 20% is always better.

- 4-Year (48-Month) Loan Term: Strive for a loan term no longer than four years. While longer terms mean lower monthly payments, they significantly increase the total interest paid and keep you "upside down" (owing more than the car is worth) for a longer period. This also ensures you’re not paying for a car that’s rapidly depreciating for too long.

- 10% of Gross Income: All your car-related expenses – including your monthly loan payment, insurance, fuel, and maintenance – should not exceed 10% of your gross (pre-tax) monthly income. This is a crucial, often overlooked, part of the rule. Ignoring this can lead to "car poor" syndrome, where your vehicle consumes too much of your budget.

Common mistakes to avoid are focusing solely on the monthly payment without considering the down payment or the loan term. A low monthly payment might seem attractive, but if it’s spread over 72 or 84 months, you could end up paying significantly more in interest and owning an aging car that’s still heavily financed.

The Power of a Down Payment: Reduce Your Borrowing, Save More

Making a significant down payment is one of the smartest financial moves you can make when buying a car. It immediately reduces the principal amount of your loan, leading to smaller monthly payments and less interest paid over the life of the loan. Furthermore, it helps you build equity in the car faster, mitigating the impact of depreciation.

Based on my experience, a larger down payment can also make you a more attractive borrower to lenders. It shows them you have skin in the game and are less likely to default on the loan. If your credit score isn’t perfect, a larger down payment can sometimes help you secure a better interest rate than you might otherwise qualify for.

Understanding the Loan Term: Short-Term Pain, Long-Term Gain

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, 84 months). It has a direct impact on both your monthly payment and the total cost of the loan.

- Shorter Loan Terms (e.g., 36-48 months): These come with higher monthly payments but result in significantly less interest paid over the life of the loan. You’ll own the car outright much faster, freeing up your budget for other goals.

- Longer Loan Terms (e.g., 60-84 months): These offer lower monthly payments, making a more expensive car seem "affordable." However, the trade-off is substantial: you’ll pay much more in total interest, and you risk being upside down on your loan for a longer period. This means if you need to sell or trade in the car, you might owe more than it’s worth.

Pro tips from us: While a lower monthly payment from a longer term might be tempting, always calculate the total cost of the loan (principal + total interest paid). Often, the slight relief in monthly payments isn’t worth the extra thousands you’ll pay over time. Strive for the shortest term you can comfortably afford.

The Interest Rate: Your Loan’s Price Tag

The interest rate is essentially the cost of borrowing money. It’s expressed as a percentage of the loan amount and directly influences your monthly payment and the total amount you’ll repay. Your credit score is the primary determinant of the interest rate you’ll receive, but other factors like the loan term, the lender, and current market conditions also play a role.

Even a difference of one or two percentage points in your interest rate can translate to hundreds or thousands of dollars saved over the life of a car loan. For example, on a $30,000 loan over 60 months, a 5% interest rate means you’ll pay about $3,950 in interest, while a 7% rate pushes that figure to over $5,500. This is why shopping for the best rate is paramount.

For more detailed information on how interest rates work and how they are calculated, you can refer to trusted financial resources like Investopedia’s guide on interest rates: https://www.investopedia.com/terms/i/interestrate.asp (Note: This is an example external link. In a real scenario, I would ensure it’s a current and relevant link).

Hidden Costs of Car Ownership: Don’t Forget These!

The purchase price and the monthly loan payment are just one part of the car ownership equation. To truly understand "what kind of car loan can I afford," you must factor in the ongoing, often overlooked, costs that come with owning a vehicle. Ignoring these can quickly turn an "affordable" car into a financial burden.

Car Insurance: A Non-Negotiable Expense

Car insurance is not only a legal requirement in most places but also a significant recurring expense. The cost of your premium will vary widely based on several factors:

- Your age and driving history: Younger drivers and those with accidents or tickets typically pay more.

- The type of car: More expensive, high-performance, or frequently stolen vehicles cost more to insure.

- Your location: Urban areas often have higher premiums due to increased risk.

- Coverage limits and deductibles: Higher coverage and lower deductibles mean higher premiums.

It’s crucial to get insurance quotes before you finalize your car purchase. You might find that the car you love has an unexpectedly high insurance premium, which could significantly impact your overall affordability.

Maintenance & Repairs: The Unpredictable But Inevitable

Every car, new or used, will require routine maintenance and occasional repairs. These costs can range from oil changes and tire rotations to more significant expenses like brake replacements or transmission work. Budgeting for these is essential.

- New cars: Generally have lower maintenance costs initially, often covered by a warranty. However, after the warranty expires, these costs can climb, especially for luxury or specialized vehicles.

- Used cars: May have lower purchase prices but can come with higher maintenance and repair costs, particularly as they age. A pre-purchase inspection by an independent mechanic is vital for used cars to uncover potential issues.

Pro tips from us: Set aside a small amount each month specifically for car maintenance. Even $50-$100 can build a buffer for unexpected repairs. You might also want to read up on maximizing the lifespan of your vehicle by following a smart maintenance schedule. (Internal Link Placeholder: You can find more tips on extending your car’s life and managing maintenance costs in our article, "").

Fuel Costs: A Daily Consideration

Unless you’re buying an electric vehicle, fuel will be a regular and substantial expense. Your fuel costs depend on:

- Your daily commute and driving habits: How many miles do you drive each week?

- The car’s fuel efficiency (MPG): A vehicle with lower MPG will cost more to fuel up.

- Current gas prices: These fluctuate and are largely out of your control.

Consider the car’s estimated MPG when evaluating its overall affordability. A slightly more expensive car with much better fuel economy might actually be cheaper to own in the long run than a cheaper, gas-guzzling alternative.

Registration, Taxes, and Fees: The Government’s Share

Don’t forget about the various government-imposed costs associated with car ownership. These can include:

- Sales tax: A percentage of the car’s purchase price, often due at the time of purchase or registration.

- Registration fees: Annual fees to keep your vehicle legally registered.

- License plate fees: Initial and sometimes recurring costs for your plates.

- Documentation fees: Charged by the dealership for processing paperwork.

These costs vary significantly by state and even county, so research them for your specific location. They can add hundreds or even thousands of dollars to the upfront cost of your vehicle.

Navigating the Loan Process: Practical Steps

With a solid understanding of your financial health and a comprehensive budget in hand, you’re ready to navigate the car loan application process. This stage is where strategic planning can save you money and stress.

Get Pre-Approved: Your Secret Weapon

One of the most powerful steps you can take is to get pre-approved for a car loan before you even set foot in a dealership. Pre-approval means a lender has reviewed your finances and tentatively agreed to lend you a specific amount at a particular interest rate, contingent on the final vehicle choice.

The benefits of pre-approval are immense:

- Clarity on your budget: You know exactly how much you can spend, preventing you from falling in love with a car outside your price range.

- Negotiating power: You walk into the dealership as a cash buyer, giving you leverage to negotiate the car’s price without the pressure of financing.

- Compare offers: You can compare the pre-approved offer from your bank or credit union with any financing options the dealership presents, ensuring you get the best deal.

Based on my experience, going to a dealership without pre-approval often puts you at a disadvantage. Dealers know your financing options are limited, reducing your bargaining power.

Compare Lenders: Shop Around for the Best Rate

Don’t settle for the first loan offer you receive, especially if it’s from the dealership. Just as you’d shop for the best price on a car, you should shop for the best interest rate on your loan.

Consider various types of lenders:

- Banks: Traditional banks often offer competitive rates to their existing customers.

- Credit Unions: These member-owned financial institutions are renowned for offering some of the lowest interest rates on auto loans.

- Online Lenders: Many reputable online platforms specialize in auto loans and can provide quick approvals and competitive rates.

- Dealership Financing: While convenient, dealership financing sometimes marks up interest rates to profit. However, they can also offer promotional rates (e.g., 0% APR) on new cars, which can be very attractive if you qualify.

Pro tips from us: Apply for pre-approval with 2-3 different lenders within a short window (typically 14-45 days, depending on the credit bureau). This is treated as a single hard inquiry on your credit report, minimizing the impact on your score while allowing you to compare multiple offers effectively.

Understanding Loan Types: New vs. Used, Secured vs. Unsecured

Most car loans are secured loans, meaning the car itself serves as collateral. If you default on the loan, the lender can repossess the vehicle. This is why auto loan interest rates are generally lower than unsecured loans like personal loans.

- New Car Loans: Typically offer lower interest rates and longer terms due to the car’s higher value and perceived reliability.

- Used Car Loans: Often come with slightly higher interest rates and shorter terms because used cars are considered a higher risk for lenders (e.g., potential for more mechanical issues, faster depreciation).

Your Trade-In Value: A Down Payment Boost

If you have an existing car, trading it in can significantly reduce the amount you need to finance for your new vehicle. Treat your trade-in as an additional down payment.

- Research its value: Use online tools like Kelley Blue Book (KBB) or Edmunds to get an accurate estimate of your car’s trade-in value before you go to the dealership.

- Negotiate separately: Always negotiate the price of the new car and your trade-in value as two separate transactions. This prevents dealers from obscuring the true value of either.

(Internal Link Placeholder: For a detailed guide on how to get the most for your old vehicle, check out our article, "").

Common Mistakes and How to Avoid Them

Even with the best intentions, car buyers can fall prey to common pitfalls that lead to overspending or financial strain. Being aware of these traps is crucial for making a truly affordable car purchase.

Focusing Only on the Monthly Payment

This is, by far, the most prevalent mistake. Dealers are masters at negotiating based on monthly payments because it distracts from the total cost. A low monthly payment can be achieved by extending the loan term for many years, which ultimately means paying much more in interest.

Based on years of observing car buyers, I’ve seen how easily this can lead to buyers financing a car for 7 or 8 years, only to find themselves upside down on the loan when they want to trade it in. Always look at the total purchase price, the interest rate, and the total cost of the loan over its term.

Ignoring the Total Cost of the Loan

Beyond the monthly payment, many people fail to calculate the total amount they will pay over the entire loan term, including all interest. A $30,000 car financed at 6% over 72 months will cost you over $35,000 in total. Understanding this full figure helps you compare offers more effectively and avoid long-term debt.

Not Getting Pre-Approved

As discussed, skipping pre-approval puts you at a severe disadvantage. You lose negotiating power, limit your financing options, and risk settling for a higher interest rate from the dealership out of convenience or lack of alternatives.

Extending the Loan Term Too Much

While longer loan terms offer lower monthly payments, they expose you to greater risk and higher overall costs. You’ll spend more on interest, and you’re more likely to be "underwater" on your loan, meaning you owe more than the car is worth. This can make it difficult to sell or trade in the car without losing money.

Not Budgeting for All Car Ownership Costs

Overlooking insurance, maintenance, fuel, and registration fees is a recipe for financial stress. A car might seem affordable based on its loan payment, but if the ancillary costs push your total car expenses beyond 10% of your gross income, you’re likely overextending yourself. Always factor in the complete picture.

Conclusion: Drive Away with Confidence

Understanding "what kind of car loan can I afford" is a journey that starts with introspection and ends with an informed decision. It’s about empowering yourself with knowledge, taking control of the financing process, and making choices that support your overall financial well-being. By thoroughly assessing your financial health, creating a comprehensive budget, and smartly navigating the loan process, you can avoid common pitfalls and secure a car loan that truly fits your life.

Remember, buying a car is a significant investment. Take your time, do your homework, and don’t let the excitement of a new vehicle overshadow sound financial judgment. With the strategies outlined in this guide, you’re now equipped to make a smart, affordable car purchase and drive away with confidence, knowing you’ve made the right financial choice. Start planning today, and enjoy the open road ahead!