What Kind of Credit Is a Car Loan? Your Ultimate Guide to Auto Financing and Its Credit Impact

What Kind of Credit Is a Car Loan? Your Ultimate Guide to Auto Financing and Its Credit Impact Carloan.Guidemechanic.com

Navigating the world of personal finance can often feel like deciphering a complex code, especially when it comes to understanding different types of credit. One of the most common forms of borrowing for many individuals is a car loan. But have you ever stopped to consider: what kind of credit is a car loan, really? Understanding its fundamental nature is not just academic; it’s crucial for making smart financial decisions, managing your credit health, and ultimately, securing the best terms for your next vehicle purchase.

This comprehensive guide will demystify car loans, breaking down their specific credit classification, exploring their profound impact on your credit score, and offering expert insights to help you manage this significant financial commitment wisely. By the end, you’ll have a clear roadmap to understanding auto financing and how it shapes your financial future.

What Kind of Credit Is a Car Loan? Your Ultimate Guide to Auto Financing and Its Credit Impact

What Exactly Is Credit? A Fundamental Understanding

Before we delve into the specifics of a car loan, let’s establish a clear understanding of what "credit" entails. In its simplest form, credit is the ability to borrow money or access goods or services with the understanding that you will pay later. It’s essentially a lender’s trust in your promise to repay a debt.

This trust is built upon your credit history, which is a detailed record of how you’ve managed past debts. Major credit bureaus like Experian, Equifax, and TransUnion collect this information, compiling it into your credit report. This report then informs your credit score, a three-digit number that lenders use to assess your creditworthiness.

The Two Main Types of Credit: A Foundational Look

All forms of credit generally fall into one of two primary categories: revolving credit or installment credit. Understanding these two types is the first step to grasping what kind of credit a car loan is.

Revolving Credit: The Flexible Line

Revolving credit is characterized by a credit limit that you can borrow against repeatedly, pay down, and then borrow from again. There isn’t a fixed end date for repayment, and your minimum payment often varies depending on your outstanding balance.

The most common example of revolving credit is a credit card. You have a set credit limit, and as you make purchases, your available credit decreases. When you make payments, your available credit replenishes, allowing you to use it again. Other examples include home equity lines of credit (HELOCs).

A key aspect of revolving credit is credit utilization, which is the amount of credit you’re using compared to your total available credit. High utilization can negatively impact your credit score.

Installment Credit: The Fixed Term Loan

In contrast to revolving credit, installment credit involves borrowing a fixed amount of money that you repay over a predetermined period through regular, scheduled payments. Each payment typically includes both principal and interest.

Once the loan is fully repaid, the account is closed. You cannot "revolve" the credit by borrowing more from the same account without applying for a new loan. Common examples of installment credit include mortgages, student loans, and, you guessed it, car loans.

The predictability of fixed payments and a clear end date makes installment credit a powerful tool for large purchases and long-term financial planning.

Unpacking the Car Loan: It’s Both an Installment and a Secured Loan

Now, let’s answer the core question: what kind of credit is a car loan? A car loan is unequivocally a form of installment credit. However, it carries another crucial characteristic that significantly impacts its risk profile and terms: it’s also a secured loan.

Car Loan as Installment Credit: Predictability and Progress

As an installment loan, a car loan provides a structured repayment plan. You borrow a specific sum, such as $25,000, and agree to repay it over a set number of months, typically 36, 48, 60, or even 72 or 84 months. Your monthly payment remains consistent throughout the loan term, assuming a fixed interest rate.

This fixed structure is beneficial for budgeting, as you know exactly how much you need to pay each month. More importantly, making these fixed, on-time payments consistently is an excellent way to build a positive payment history, which is the most significant factor in your credit score. Each successful payment demonstrates your reliability as a borrower.

Car Loan as Secured Credit: The Collateral Factor

The "secured" aspect of a car loan means that the loan is backed by an asset – in this case, the car itself. The vehicle acts as collateral for the loan. This arrangement provides a layer of security for the lender.

If you, as the borrower, fail to make your payments as agreed (default on the loan), the lender has the legal right to repossess the car. They can then sell the car to recover their losses. Because there’s collateral involved, secured loans generally pose less risk to lenders than unsecured loans (like personal loans or credit cards without collateral). This reduced risk often translates into more favorable interest rates for borrowers, especially those with good credit.

Pro Tip from us: Always remember that the car isn’t truly yours until the loan is fully paid off. The lender holds the title until that final payment. Understanding this collateral implication is vital before committing to a car loan.

The Profound Impact of a Car Loan on Your Credit Score

Taking out a car loan, and more importantly, managing it, has a significant and multi-faceted impact on your credit score. This impact is generally positive if managed well, but can be severely negative if mismanaged. Let’s break down how it affects the five key factors that make up your FICO score.

Payment History (35% of FICO Score): The Most Crucial Factor

This is the bedrock of your credit score. When you take out a car loan, you commit to making regular, on-time payments. Each payment you make punctually contributes positively to your payment history. It demonstrates to lenders that you are a responsible borrower who honors their financial obligations.

Conversely, missing payments, even by a few days, can severely damage your credit score. A payment reported 30, 60, or 90 days late can cause a significant drop, and multiple late payments can make it very difficult to secure future credit at favorable terms. Based on my experience, consistently making on-time payments on an installment loan like a car loan is one of the most effective ways to build and maintain excellent credit.

Amounts Owed / Credit Utilization (30% of FICO Score): A Different Calculation

For installment loans, the "amounts owed" factor works differently than with revolving credit. With a car loan, you start with a high balance, which gradually decreases with each payment. This is generally viewed positively, as you’re actively reducing your debt.

Unlike revolving credit where keeping utilization low is key, with installment loans, the focus is on the original loan amount and its steady reduction. Lenders also consider your overall debt-to-income (DTI) ratio, which is how much of your monthly gross income goes towards debt payments. A high DTI, even with responsible car loan payments, could signal that you’re overextended.

Length of Credit History (15% of FICO Score): A Long-Term Asset

When you open a new car loan, it adds to the average age of your credit accounts. Initially, this might slightly reduce your average age if your existing accounts are very old. However, over time, a long-standing car loan that you manage responsibly becomes a valuable asset.

A loan that remains open and in good standing for many years demonstrates a long history of responsible credit management. This contributes positively to the "length of credit history" factor, showing stability and reliability to potential lenders.

Credit Mix (10% of FICO Score): Diversifying Your Portfolio

Your credit mix refers to the variety of credit accounts you have. Lenders like to see that you can responsibly manage different types of credit, such as both revolving credit (credit cards) and installment credit (car loans, mortgages).

Adding a car loan to your credit profile, especially if you previously only had credit cards, can diversify your credit mix. This demonstrates your ability to handle different financial commitments, which can positively influence this portion of your credit score. Based on my experience, a balanced credit mix shows a more robust and adaptable financial management style.

New Credit (10% of FICO Score): Short-Term Impact for Long-Term Gain

When you apply for a car loan, the lender performs a "hard inquiry" on your credit report. This inquiry temporarily dings your credit score by a few points for a short period (usually a few months). Multiple hard inquiries in a short timeframe can signal to lenders that you might be desperate for credit or taking on too much debt, which can be detrimental.

However, FICO models often recognize "rate shopping" for auto loans. If you have several hard inquiries from auto lenders within a short window (typically 14-45 days, depending on the scoring model), they may be treated as a single inquiry, minimizing the negative impact. While there’s a short-term dip, the long-term benefit of establishing a new, well-managed installment account far outweighs this initial minor setback.

Before You Drive Off: Key Considerations for Your Car Loan

Securing a car loan is a significant financial decision. Approaching it strategically can save you money and protect your credit health.

- Understand Your Credit Score: Before you even look at cars, know your credit score. A higher score typically qualifies you for lower interest rates, saving you thousands over the life of the loan.

- Budgeting for Payments: Don’t just consider the monthly car payment. Factor in insurance, fuel, maintenance, and potential repairs. Ensure the total cost fits comfortably within your budget.

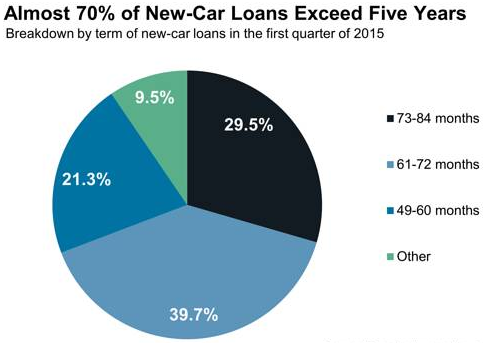

- Loan Term Matters: While a longer loan term (e.g., 72 or 84 months) offers lower monthly payments, you’ll pay significantly more in total interest. Shorter terms mean higher monthly payments but less interest paid overall.

- Make a Down Payment: A larger down payment reduces the amount you need to borrow, which means lower monthly payments and less interest paid. It also helps avoid being "upside down" on your loan, where you owe more than the car is worth.

- Shop Around for Interest Rates: Don’t just accept the financing offered by the dealership. Compare offers from banks, credit unions, and online lenders. A difference of even one percentage point can save you hundreds, if not thousands, of dollars.

- Get Pre-Approved: Getting pre-approved for a loan before visiting dealerships gives you a clear budget, allows you to negotiate with confidence, and shows the dealer you’re a serious buyer. For more tips on improving your credit score before applying for a loan, check out our guide on .

Managing Your Car Loan Responsibly for Optimal Credit Health

Once you’ve secured your car loan, the journey to excellent credit doesn’t end; it begins. Responsible management is key to leveraging this installment credit to your financial advantage.

- Pay On Time, Every Time: This cannot be stressed enough. Set up automatic payments from your checking account to ensure you never miss a due date. Late payments are the quickest way to damage your credit score.

- Avoid Refinancing Too Often: While refinancing can sometimes lower your interest rate, doing it frequently or extending the loan term repeatedly can end up costing you more in interest over the long run. It can also restart the clock on your loan’s age, which isn’t ideal for your credit history length.

- Don’t Let the Car Be Repossessed: If you’re struggling to make payments, communicate with your lender immediately. They may be willing to work with you on a temporary solution. Allowing your car to be repossessed will severely damage your credit score for years.

- Consider Extra Payments: If your financial situation allows, making extra principal payments can significantly reduce the total interest you pay and help you pay off the loan faster. Pro Tip: Even an extra $50 a month can make a big difference over a 5-year loan.

- Keep Your Insurance Current: Since the car is collateral, the lender requires you to carry comprehensive insurance. Letting your policy lapse can lead to forced-place insurance from the lender, which is typically more expensive.

For detailed information on managing debt and improving financial literacy, the Consumer Financial Protection Bureau (CFPB) offers excellent resources. If you’re curious about other types of secured loans, explore our article on .

Common Mistakes to Avoid When Taking Out a Car Loan

Even with the best intentions, it’s easy to fall into common traps when financing a vehicle. Being aware of these pitfalls can save you from costly errors.

- Not Knowing Your Budget: Buying a car that stretches your finances too thin is a recipe for stress and potential payment issues. Always calculate what you can truly afford, not just what you’re approved for.

- Ignoring Your Credit Score: Your credit score is a powerful negotiating tool. Not knowing it means you can’t accurately gauge the fairness of the interest rates offered to you.

- Taking the Longest Term for the Lowest Payment: While a 72 or 84-month loan makes payments seem affordable, you’ll pay substantially more in interest and the car will likely depreciate faster than you pay it off. This leaves you "underwater."

- Not Shopping Around for Rates: Relying solely on the dealership’s financing can mean missing out on better rates from other lenders. Always compare multiple offers.

- Focusing Only on Monthly Payment, Not Total Cost: Salespeople often highlight the monthly payment. Always ask for the total cost of the loan, including all fees and interest, over its full term.

- Buying More Car Than You Need: It’s tempting to get the latest model with all the bells and whistles, but an expensive car means a larger loan and more financial strain. Be practical about your needs.

Conclusion: Your Car Loan – A Powerful Tool for Credit Building

In summary, a car loan is a specific and impactful type of credit. It is an installment loan, meaning you borrow a fixed amount and repay it over a set period with consistent payments. Crucially, it is also a secured loan, with the vehicle itself serving as collateral. This distinction significantly influences the terms and risks associated with auto financing.

Understanding what kind of credit a car loan is empowers you to make informed decisions. When managed responsibly, a car loan can be a powerful tool for building a strong credit history, diversifying your credit mix, and demonstrating your financial reliability to future lenders. By focusing on timely payments, understanding the terms, and avoiding common mistakes, you can leverage your auto financing to drive not just a new car, but also a healthier financial future.