Will My Bank Give Me A Car Loan? Demystifying the Path to Auto Loan Approval

Will My Bank Give Me A Car Loan? Demystifying the Path to Auto Loan Approval Carloan.Guidemechanic.com

Getting a new set of wheels is an exciting prospect, but the journey often begins with a crucial question: "Will my bank give me a car loan?" For many, their personal bank seems like the most natural place to start, offering a sense of familiarity and trust. However, navigating the world of auto loans can feel like deciphering a complex financial puzzle.

This comprehensive guide is designed to pull back the curtain on the bank car loan approval process. We’ll explore exactly what lenders look for, uncover the key factors that influence their decision, and equip you with the knowledge to significantly boost your chances of getting approved. Our ultimate goal is to empower you to approach your bank with confidence, armed with a clear understanding of what it takes to secure that coveted car loan.

Will My Bank Give Me A Car Loan? Demystifying the Path to Auto Loan Approval

Understanding the Bank’s Perspective: What Do Lenders Really Look For?

When you apply for a car loan, your bank isn’t just looking at your enthusiasm for a new vehicle. They are, at their core, assessing risk. Their primary concern is whether you have the financial capacity and willingness to repay the loan on time, every time. This assessment dictates not only whether you’ll be approved, but also the interest rate and terms they’ll offer.

Based on my extensive experience in the financial landscape, banks operate under a principle of prudent lending. They need assurance that their investment in you, the borrower, will yield a return and not result in a loss. This means they meticulously scrutinize several aspects of your financial life to build a comprehensive risk profile. It’s not about being judgmental; it’s about making sound business decisions.

They’re essentially looking for a reliable borrower who demonstrates financial stability and a history of responsible money management. This holistic view is crucial, as a single strong point might not compensate for several weaker areas. Therefore, understanding their perspective is the first step toward aligning your application with their expectations.

Key Factors Influencing Your Car Loan Approval

Let’s dive into the specific elements your bank will evaluate when you apply for a car loan. Each of these components plays a vital role in the overall decision.

1. Credit Score: Your Financial Report Card

Your credit score is arguably the most significant factor in determining your car loan eligibility and the interest rate you’ll receive. It’s a three-digit number, typically ranging from 300 to 850, that summarizes your creditworthiness based on your past borrowing and repayment behavior. A higher score signals less risk to lenders.

Banks categorize credit scores into different tiers. Generally, a score above 700 is considered good to excellent, making you a prime candidate for the best interest rates. Scores between 620 and 699 are often deemed fair or good, still allowing for approval but potentially with slightly higher rates. Below 620, you might face higher interest rates or even outright denial.

Your credit history, which forms the basis of this score, details your payment history, the types of credit you’ve used, the length of your credit history, and your credit utilization. A consistent record of on-time payments and responsible credit usage is incredibly valuable. Lenders see this as a strong indicator of future reliability.

Pro tips from us: Before even thinking about a car loan, check your credit score and report from all three major bureaus (Experian, Equifax, TransUnion). You can do this annually for free at AnnualCreditReport.com. Dispute any errors immediately, as even small inaccuracies can negatively impact your score.

2. Debt-to-Income (DTI) Ratio: Are You Overextended?

Your Debt-to-Income (DTI) ratio is another critical metric banks use to assess your ability to take on new debt. It represents the percentage of your gross monthly income that goes towards paying your monthly debt obligations. This includes credit card minimum payments, student loan payments, mortgage or rent, and other loan payments.

To calculate your DTI, simply add up all your recurring monthly debt payments and divide that sum by your gross monthly income (before taxes and deductions). For instance, if your monthly debts total $1,500 and your gross monthly income is $5,000, your DTI is 30% ($1,500 / $5,000 = 0.30 or 30%).

Banks generally prefer a DTI ratio of 36% or lower, though some might go up to 43% depending on other factors. A lower DTI indicates that you have more disposable income available to comfortably manage a new car payment, reducing the risk of default for the bank. A high DTI, on the other hand, suggests you might be stretched too thin financially, making a new loan a significant burden.

Common mistakes to avoid are applying for a car loan without knowing your DTI, or taking on additional debt right before applying. Any new debt can push your DTI higher, potentially jeopardizing your approval chances. Focus on reducing existing debt if your DTI is on the higher side.

3. Down Payment: Skin in the Game

Making a down payment on your car loan demonstrates your financial commitment and significantly reduces the bank’s risk. It’s essentially the portion of the car’s purchase price that you pay upfront, directly reducing the amount you need to borrow. The larger your down payment, the less money the bank has to lend you, making the loan inherently safer for them.

From a lender’s perspective, a substantial down payment shows that you have "skin in the game." It indicates financial discipline and a genuine intention to fulfill your obligations. Moreover, a larger down payment immediately creates equity in your vehicle, meaning you owe less than the car is worth, which protects the bank if you were to default and they had to repossess and sell the vehicle.

Beyond improving your approval odds, a healthy down payment offers direct benefits to you. It reduces your monthly payments, lowers the total interest paid over the life of the loan, and helps prevent you from being "upside down" on your loan (owing more than the car is worth) early in the ownership period. While 10-20% is often recommended, even a smaller down payment can make a difference.

4. Employment Stability and Income Verification: Can You Pay It Back?

Banks need assurance that you have a consistent and reliable source of income to make your monthly car loan payments. This is where employment stability becomes crucial. Lenders prefer to see a steady work history, ideally with the same employer for at least two years. Frequent job changes or gaps in employment can raise red flags about your income consistency.

When you apply, be prepared to provide extensive documentation to verify your income. This typically includes recent pay stubs (usually the last two or three), W-2 forms from the past two years, and sometimes even tax returns if you’re self-employed or have a more complex income structure. For self-employed individuals, banks often require two years of tax returns to assess average income and business stability.

Common mistakes to avoid are having an inconsistent income stream or being unable to provide adequate documentation. Banks need verifiable proof, not just verbal assurances. Ensure all your financial records are in order before applying to streamline this part of the process.

5. Vehicle Information: The Collateral Matters

The car itself plays a significant role in your loan approval, as it serves as the collateral for the loan. If you fail to make payments, the bank has the right to repossess and sell the vehicle to recover their losses. Therefore, they assess the car’s value and marketability very carefully.

Banks generally prefer newer, lower-mileage vehicles because they hold their value better and are easier to resell if necessary. An older car with high mileage, or one with significant damage, might be considered a higher risk because its resale value is lower and more volatile. This directly impacts the bank’s potential recovery should you default.

Lenders also consider the loan-to-value (LTV) ratio, which compares the amount you want to borrow to the vehicle’s actual market value. If you’re trying to borrow significantly more than the car is worth (e.g., rolling negative equity from a previous car into the new loan), the bank may be hesitant. They want to ensure the collateral adequately covers the loan amount.

6. Relationship with Your Bank: An Existing Connection

While not always a deciding factor, your existing relationship with your bank can sometimes work in your favor. If you’ve been a long-standing customer with checking, savings, or other accounts, and you have a history of responsible financial behavior with them, they already have a wealth of data on your financial habits. This can make the approval process smoother.

Many banks offer pre-qualified or pre-approved offers to their existing customers, which can provide a convenient starting point. This familiarity can translate into slightly more flexible terms or a quicker approval process, as they already trust you as a client. It’s not a guarantee, but it certainly doesn’t hurt.

Check out our guide on Building a Strong Financial Relationship with Your Bank for more insights on how to foster these valuable connections. A solid banking history with your institution can be a subtle but powerful advantage when seeking a car loan.

The Pre-Approval Process: Your Secret Weapon

One of the smartest moves you can make before stepping onto a dealership lot is to get pre-approved for a car loan. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount of money, at a certain interest rate, for a car purchase. It’s a powerful tool that puts you in control.

The benefits of pre-approval are numerous. Firstly, it gives you a clear budget, so you know exactly how much car you can afford without overspending. This prevents the disappointment of falling in love with a car that’s out of your financial reach. Secondly, it transforms you into a cash buyer at the dealership, giving you significant negotiation power. Dealers know you’re serious and already have financing, so they’re more likely to offer better prices on the vehicle itself.

To get pre-approved, you’ll typically fill out an application with your chosen bank, providing details about your income, employment, and debts. The bank will then perform a "hard inquiry" on your credit report. Within a short period (often a day or two), they’ll inform you of the loan amount and terms you qualify for.

Common mistakes to avoid are skipping pre-approval and relying solely on dealership financing. While dealership financing can be convenient, it may not always offer the most competitive rates. Having a pre-approval in hand allows you to compare offers and ensure you’re getting the best deal.

Pro tips from us: Don’t just get pre-approved by one bank. Apply to several lenders (banks, credit unions, online lenders) within a short window (typically 14-45 days, depending on the credit scoring model). Multiple inquiries within this period are usually treated as a single inquiry for credit scoring purposes, minimizing the impact on your score while maximizing your chances of finding the best rate.

Steps to Maximize Your Chances of Car Loan Approval

Now that you understand what banks look for, let’s outline actionable steps you can take to significantly improve your odds of getting that "yes" to your car loan application.

1. Assess Your Financial Health Thoroughly

Before you even think about applying, take an honest look at your complete financial picture. Check your credit reports for accuracy and review your monthly budget meticulously. Understand your income, expenses, and current debt obligations. This self-assessment will highlight areas you might need to improve.

Knowing your financial standing upfront allows you to address potential weaknesses. It’s like preparing for an exam; you wouldn’t go in without studying. This preparation is key to a smooth and successful application process.

2. Improve Your Credit Score

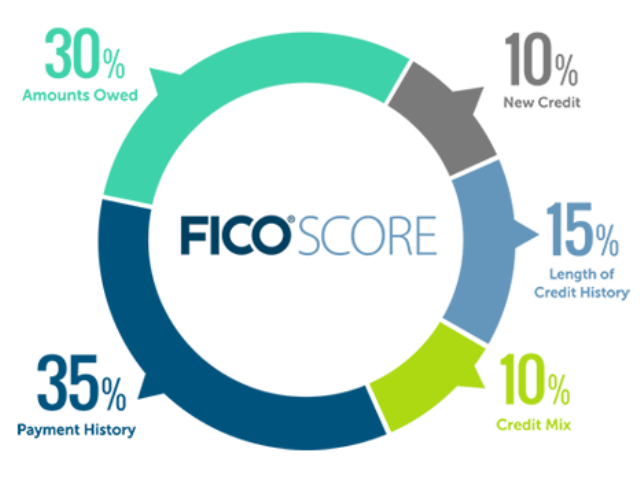

If your credit score isn’t where you want it to be, dedicate time to improving it. The most impactful actions include paying all your bills on time, every time, as payment history accounts for 35% of your FICO score. Reduce your credit card balances to lower your credit utilization ratio, ideally below 30% of your available credit.

Additionally, avoid opening new credit accounts right before applying for a car loan, as this can temporarily lower your score. If you find any errors on your credit report, dispute them immediately with the credit bureaus. A cleaner, higher credit score translates directly into better loan terms.

3. Save for a Substantial Down Payment

Aim to save at least 10-20% of the car’s purchase price for a down payment. The more you put down, the less you need to borrow, which lowers your monthly payments and reduces the overall interest you’ll pay. It also makes your application more attractive to lenders.

A larger down payment signals financial responsibility and significantly reduces the bank’s risk. This "skin in the game" can often compensate for other minor weaknesses in your application.

4. Lower Your Debt-to-Income Ratio

Actively work to reduce your existing debt before applying for a car loan. Focus on paying down high-interest credit card balances or any small personal loans. This will free up more of your monthly income, bringing down your DTI ratio.

A lower DTI shows lenders that you have ample capacity to take on a new car payment without becoming financially strained. It demonstrates sound financial management and increases their confidence in your ability to repay.

5. Gather All Necessary Documentation

Be prepared with all the paperwork your bank will request. This typically includes government-issued ID, proof of residence (utility bill), proof of income (pay stubs, W-2s, tax returns), and bank statements. For the vehicle itself, you’ll need details like the VIN, make, model, year, and mileage.

Having everything organized and ready will make the application process much faster and smoother. It also shows the bank that you are organized and serious about the loan.

6. Consider a Co-Signer (If Necessary)

If your credit score is low, your DTI is high, or you have limited credit history, a co-signer might be an option. A co-signer, typically a trusted family member or friend with excellent credit, agrees to be equally responsible for the loan if you default. This provides an additional layer of security for the bank.

However, understand the implications: if you miss payments, it negatively impacts both your credit and your co-signer’s. This should only be considered if absolutely necessary and with clear communication about responsibilities.

7. Shop Around, But Wisely

As mentioned with pre-approval, don’t just settle for the first offer you receive. Compare rates and terms from various lenders – your bank, credit unions, and online lenders. Each institution has different lending criteria and rates, and what one bank offers might not be the best available.

Remember that applying for multiple loans within a short time frame (typically 14-45 days, depending on the credit scoring model used) will usually only count as a single hard inquiry on your credit report. This allows you to rate shop without significantly harming your credit score. To understand more about how credit inquiries impact your score, you can read this detailed guide from Experian.

What If Your Bank Says No? Don’t Despair!

Receiving a car loan denial can be disheartening, but it’s not the end of the road. The first step is to understand why you were denied. Lenders are legally required to provide you with an Adverse Action Notice explaining the reasons for their decision. This notice is invaluable, as it highlights specific areas you need to address.

Common reasons for denial include a low credit score, high DTI, insufficient income, a short credit history, or issues with the vehicle itself (e.g., too old, too many miles). Once you know the reason, you can formulate a plan. Focus on improving that specific area, whether it’s boosting your credit score, paying down debt, or saving for a larger down payment.

While your primary bank might have said no, other lenders might be willing to approve you. Consider exploring credit unions, which often have more flexible lending criteria and better rates for members. Online lenders are another viable option, as they frequently cater to a broader range of credit profiles, sometimes even offering loans to those with less-than-perfect credit (though usually at higher interest rates). Dealership financing is also an option, but as discussed, it’s often best to secure outside financing first for leverage.

For a deeper dive into other financing avenues, explore our article Alternatives to Traditional Bank Car Loans to discover more options available to you.

Pro Tips from an Expert Blogger

Securing a car loan from your bank is entirely achievable with the right preparation and knowledge. Think of it as a strategic endeavor, not just a simple application. The more informed and prepared you are, the higher your chances of success.

Always be transparent and honest in your application. Attempting to obscure financial details will only backfire. Lenders have sophisticated systems to verify information, and dishonesty can lead to outright denial and even future difficulties.

My final piece of advice: start early. Don’t wait until you’ve found your dream car to begin thinking about financing. The preparation work – checking your credit, saving for a down payment, and understanding your DTI – takes time. The more time you give yourself, the better position you’ll be in to secure the best possible car loan terms.

Conclusion

The question "Will my bank give me a car loan?" is a common one, and the answer, as we’ve seen, depends on a multitude of factors. Your credit score, debt-to-income ratio, down payment, employment stability, and even the vehicle you choose all play critical roles in the bank’s decision. By understanding these key elements and proactively addressing any potential weaknesses, you can significantly enhance your eligibility.

Remember, preparation is paramount. Take the time to assess your financial health, improve your credit, save for a down payment, and explore pre-approval options. With diligent effort and a clear understanding of the lending process, you can confidently approach your bank and drive away with the car loan you need. Start your preparation today, and turn that "will my bank give me a car loan" into a confident "my bank will give me a car loan!"