Will My Credit Union Give Me A Car Loan? A Comprehensive Guide to Auto Loan Approval

Will My Credit Union Give Me A Car Loan? A Comprehensive Guide to Auto Loan Approval Carloan.Guidemechanic.com

Navigating the world of car financing can feel like a complex journey, especially when you’re trying to find the best possible terms. Many car buyers immediately think of traditional banks or dealership financing, but a powerful, often overlooked option lies within your local credit union. The question, "Will my credit union give me a car loan?" is a common one, and the answer is usually a resounding yes – with the right preparation and understanding.

As an expert in financial content, I’ve seen countless individuals successfully secure auto loans through credit unions, often with more favorable conditions than traditional lenders. This comprehensive guide will delve deep into everything you need to know about credit union car loans, from eligibility requirements to application tips, ensuring you’re well-equipped to drive away in your dream car.

Will My Credit Union Give Me A Car Loan? A Comprehensive Guide to Auto Loan Approval

Why Consider a Credit Union for Your Car Loan? Unpacking the Benefits

Before we dive into the specifics of approval, it’s crucial to understand why credit unions are often the preferred choice for car financing. Their unique operational model offers distinct advantages that can save you money and provide a more pleasant borrowing experience.

Lower Interest Rates and Fees

Credit unions are not-for-profit financial institutions, meaning their primary goal isn’t to maximize shareholder profits. Instead, they focus on providing value to their members. This operational philosophy often translates directly into lower interest rates on loans and fewer, if any, hidden fees compared to for-profit banks.

Based on my experience, even a slight reduction in your Annual Percentage Rate (APR) can lead to significant savings over the life of a car loan. These savings can amount to hundreds, or even thousands, of dollars, making your vehicle purchase much more affordable.

Personalized Service and Member Focus

When you walk into a credit union, you’re not just a customer; you’re a member and an owner. This member-centric approach fosters a highly personalized service experience. Credit union loan officers often take the time to understand your individual financial situation and needs.

They are generally more willing to work with you to find a solution that fits your budget, rather than simply applying a rigid set of criteria. This human touch can be incredibly valuable, especially if your financial history isn’t perfectly pristine.

Flexible Loan Terms and Options

Credit unions are known for their flexibility. While they still adhere to responsible lending practices, they often have more leeway in structuring loan terms to meet diverse member needs. This might include a wider range of loan durations, different repayment schedules, or even specialized loan products.

Pro tips from us: Don’t hesitate to discuss your specific financial constraints and preferences with your credit union. They might offer solutions you hadn’t considered, such as slightly longer terms to reduce monthly payments, or even refinancing options down the line.

Community-Oriented Approach

Many credit unions have deep roots in their local communities. This community focus means they are often invested in the financial well-being of their members and the local economy. They tend to be more understanding of local economic conditions and are committed to serving their members effectively.

This local connection can sometimes provide an added layer of trust and support, making the borrowing process feel less transactional and more like a partnership. It’s a key differentiator from large national banks.

Key Factors Credit Unions Consider for Car Loan Approval

Now that we’ve established why credit unions are a great option, let’s address the core question: "Will my credit union give me a car loan?" The answer hinges on several critical factors that lenders, including credit unions, evaluate during the application process. Understanding these will help you prepare and maximize your chances of approval.

1. Your Credit Score and History: The Foundation

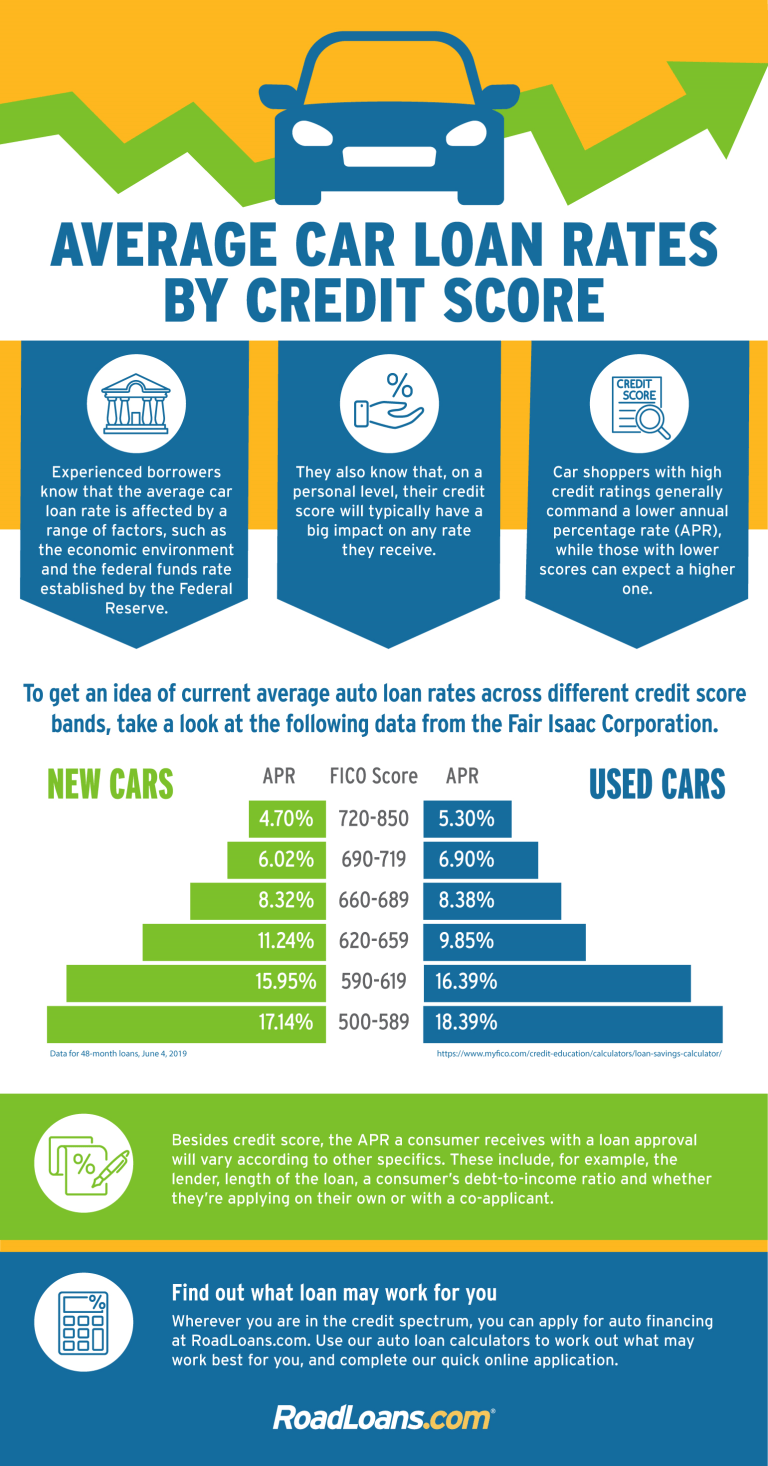

Your credit score is arguably the most significant factor a credit union will consider. It’s a three-digit number that summarizes your creditworthiness, reflecting your payment history, amounts owed, length of credit history, new credit, and credit mix. A higher score indicates a lower risk to the lender.

Generally, a good credit score is considered to be in the range of 670 to 739 (FICO Score). Excellent credit is 740 and above. While these are benchmarks, credit unions often have a bit more flexibility and may approve loans for members with scores slightly below these thresholds, especially if other factors are strong.

Your credit history, which includes details like past bankruptcies, foreclosures, or a history of late payments, will also be thoroughly reviewed. A consistent record of on-time payments across various credit accounts demonstrates financial responsibility. Common mistakes to avoid are having numerous late payments or a very short credit history, as these can signal higher risk.

2. Debt-to-Income (DTI) Ratio: Your Financial Balance

Your Debt-to-Income (DTI) ratio is another crucial metric. It’s a percentage that compares your total monthly debt payments to your gross monthly income. Lenders use DTI to assess your ability to manage monthly payments and take on additional debt, like a car loan.

To calculate your DTI, sum up all your monthly debt payments (credit cards, student loans, mortgage/rent, etc.) and divide that by your gross monthly income (before taxes and deductions). For instance, if your total monthly debt is $1,000 and your gross monthly income is $3,000, your DTI is 33%.

Most lenders prefer a DTI ratio of 36% or lower, though some might go up to 43%, especially if you have a strong credit score. A high DTI indicates that a large portion of your income is already committed to existing debts, which could make it challenging to afford new car payments. For more insights on this, you might find our article on Understanding Your Debt-to-Income Ratio and How It Affects Loans helpful. (Internal Link 1 Placeholder)

3. Income Stability and Employment History: A Steady Stream

Credit unions want assurance that you have a stable source of income to make your monthly car loan payments. They will typically look at your employment history to gauge this stability. A long, consistent employment history with the same employer or within the same industry is generally viewed favorably.

Self-employed individuals or those with fluctuating income might need to provide more extensive documentation, such as tax returns for the past two years, to demonstrate consistent earnings. The goal is to show a reliable income stream that can comfortably cover your loan obligations.

4. Down Payment: Your Commitment

Making a down payment on a car loan significantly improves your chances of approval and can lead to better loan terms. A down payment reduces the amount you need to borrow, which lowers the lender’s risk. It also demonstrates your financial commitment to the purchase.

Based on my experience, a down payment of at least 10% for a used car and 20% for a new car is often recommended. Not only does it make you a more attractive borrower, but it also helps prevent you from being "upside down" on your loan (owing more than the car is worth) early in the loan term.

5. Vehicle Information: The Collateral

The car you intend to purchase also plays a role in the approval process. Credit unions will consider the vehicle’s age, mileage, make, model, and overall value. This is because the car itself serves as collateral for the loan.

Lenders want to ensure that the loan amount doesn’t exceed the car’s actual market value. This is often referred to as the Loan-to-Value (LTV) ratio. A high LTV (e.g., borrowing 120% of the car’s value) can be seen as riskier, especially if you’re trying to roll negative equity from a previous vehicle into the new loan.

6. Membership Status: The Gateway

To get a car loan from a credit union, you generally need to be a member. Credit unions have specific eligibility requirements, often based on where you live, work, or belong to certain organizations. These requirements are typically easy to meet.

Becoming a member usually involves opening a savings account with a small initial deposit (often as low as $5-$25). It’s a straightforward process, and once you’re a member, you gain access to all their financial products and services, including car loans. Don’t let membership requirements deter you; they are designed to be inclusive.

The Application Process: What to Expect and How to Prepare

Understanding the factors for approval is just one part of the equation. Knowing the application process and how to prepare can significantly streamline your journey to getting that car loan.

Gathering Your Documents

Preparation is key. Before you even submit an application, gather all the necessary documents. This proactive step can prevent delays and show the credit union that you are organized and serious.

Commonly required documents include:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (last 2-3 months), W-2s, or tax returns (if self-employed).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Credit Union Membership: Account number or proof of membership.

- Vehicle Information (if you’ve chosen a car): Purchase agreement, VIN, make, model, year, and mileage.

The Power of Pre-Approval

One of the most valuable steps you can take is to apply for pre-approval. Pre-approval means the credit union has reviewed your financial information and tentatively approved you for a specific loan amount at an estimated interest rate, before you’ve even picked out a car.

Pro tips from us: Getting pre-approved empowers you tremendously at the dealership. It turns you into a cash buyer, allowing you to negotiate the car price based on the vehicle itself, rather than getting caught up in monthly payment discussions. It also gives you a clear budget, preventing you from falling in love with a car you can’t truly afford.

Submitting Your Application

Most credit unions offer multiple ways to apply for a car loan: online, over the phone, or in person. Each method has its advantages. Online applications offer convenience, while an in-person application allows for direct interaction with a loan officer who can answer questions and provide immediate feedback.

Based on my experience, submitting a complete and accurate application from the outset is crucial. Any missing information can lead to delays or even a denial. Double-check all details before hitting submit.

Waiting for a Decision

Once your application is submitted, the credit union will review your information, pull your credit report, and assess your financial standing. This process can take anywhere from a few hours to a few business days, depending on the complexity of your application and the credit union’s workload.

If approved, you’ll receive a loan offer outlining the approved amount, interest rate, and terms. If denied, the credit union is required to provide you with an adverse action notice, explaining the reasons for the denial. This information can be valuable for future applications.

"What If My Credit Isn’t Perfect?": Getting a Car Loan with Less-Than-Ideal Credit

Many people shy away from applying for loans if their credit score isn’t stellar. However, credit unions can often be more understanding and flexible than traditional banks when it comes to borrowers with less-than-perfect credit.

Credit Unions: A More Forgiving Approach

While a good credit score is always beneficial, credit unions are often willing to look beyond just the numbers. Because of their member-focused mission, they may consider your overall financial picture, your relationship with the credit union, and your willingness to make good on your commitments.

They might be more inclined to approve a loan for a long-standing member with a slightly lower score, especially if you have a stable job and a low DTI. They might also offer credit-builder loans or resources to help you improve your credit over time.

Consider a Co-Signer

If your credit score is a significant hurdle, a co-signer can dramatically improve your chances of approval. A co-signer is someone with good credit who agrees to be equally responsible for the loan if you fail to make payments. This reduces the risk for the credit union.

Before asking someone to co-sign, ensure both parties fully understand the responsibilities. If you miss payments, it will negatively impact both your credit scores, and the co-signer will be legally obligated to repay the loan.

Building Credit First

Sometimes, the best strategy is to take a step back and actively work on improving your credit score before applying for a car loan. This could involve paying down existing debts, making all payments on time, and disputing any errors on your credit report. For practical steps, consider reading our article on How to Improve Your Credit Score Quickly and Effectively. (Internal Link 2 Placeholder)

Pro tips from us: Be honest and transparent about your credit situation with your credit union. They are there to help their members, and being upfront allows them to offer the most suitable solutions or advice.

Common Mistakes to Avoid When Applying for a Credit Union Car Loan

Even with all the right information, applicants can sometimes make mistakes that hinder their chances of approval or lead to less favorable loan terms. Being aware of these pitfalls can help you navigate the process more smoothly.

Applying to Too Many Lenders

While it’s wise to shop around for the best rates, applying to numerous lenders within a short period can negatively impact your credit score. Each "hard inquiry" on your credit report can cause a slight dip. It’s generally recommended to complete your rate shopping within a 14-45 day window, as multiple inquiries for the same type of loan within this period are often grouped as a single inquiry by credit scoring models.

Not Knowing Your Credit Score

Going into the application process without knowing your credit score is like driving blindfolded. Your credit score is a key indicator of your financial health. Obtain your free credit report from AnnualCreditReport.com and review it for accuracy before applying. This allows you to address any errors and understand where you stand.

Skipping Pre-Approval

As discussed earlier, pre-approval offers significant advantages. Failing to get pre-approved before heading to the dealership can leave you at a disadvantage during negotiations, potentially leading to higher interest rates or less favorable terms. It strips you of your negotiating power.

Not Comparing Offers

Even if your credit union offers excellent rates, it’s always a good idea to compare their offer with at least one or two other lenders (within that short shopping window). This ensures you’re truly getting the most competitive rate available to you. While credit unions are often superior, it never hurts to verify.

Overlooking Membership Requirements

Some individuals get excited about a credit union’s rates only to realize they don’t meet the membership criteria. Always confirm eligibility before getting too far into the application process. Most credit unions have broad eligibility, but it’s a necessary step.

Maximizing Your Chances of Approval

To confidently answer "Yes!" to "Will my credit union give me a car loan?", take proactive steps to present yourself as the best possible borrower.

1. Improve Your Credit Score

This is foundational. Pay bills on time, reduce credit card balances, and avoid opening new credit accounts right before applying for a car loan. A healthier credit score directly translates to better loan offers.

2. Reduce Your Debt

Lowering your existing debt, especially revolving credit like credit cards, will improve your Debt-to-Income ratio. This signals to the credit union that you have more disposable income available to manage a new car payment comfortably.

3. Save for a Down Payment

As highlighted earlier, a substantial down payment reduces the loan amount and the credit union’s risk. It also demonstrates financial discipline and commitment on your part. Aim for at least 10-20% of the vehicle’s purchase price.

4. Research Thoroughly

Before approaching the credit union, research the type of car you want and its approximate value. Having a clear idea of your budget and the vehicle’s cost shows responsibility and preparedness. This also helps you understand a reasonable loan amount.

5. Build a Relationship with Your Credit Union

If you’re already a member, actively using other services offered by the credit union (like checking accounts, savings, or even smaller loans) can sometimes work in your favor. A history of responsible financial behavior within the institution builds trust. They see you as a valued member, not just a loan applicant.

Beyond Approval: Understanding Your Loan Terms

Getting approved is a significant milestone, but the journey doesn’t end there. It’s crucial to thoroughly understand the terms and conditions of your car loan before you sign on the dotted line.

Interest Rate (APR)

The Annual Percentage Rate (APR) is the most critical number to look at. It represents the actual yearly cost of funds over the term of the loan, including any fees. A lower APR means less money you’ll pay in interest over time. Make sure you understand if the rate is fixed (stays the same) or variable (can change). Most auto loans are fixed-rate.

Loan Term

The loan term is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A longer term usually means lower monthly payments but results in paying more interest over the life of the loan. A shorter term means higher monthly payments but less total interest paid. Choose a term that balances affordability with overall cost.

Monthly Payments

Ensure the monthly payment fits comfortably within your budget. Don’t stretch yourself too thin, even if approved for a higher amount. Factor in other car-related expenses like insurance, fuel, and maintenance when calculating your true monthly vehicle cost.

Fees

While credit unions are known for fewer fees, always ask about any potential charges, such as application fees, origination fees, or late payment fees. Understand what they are and how they apply.

Early Payoff Penalties

Most credit union car loans do not have early payoff penalties, meaning you can pay off your loan ahead of schedule without incurring extra charges. This can save you a significant amount in interest. Always confirm this detail, though it’s rare to find such penalties with credit unions.

For a broader understanding of auto loan terms and how they compare across different lenders, the Consumer Financial Protection Bureau offers excellent resources: Understanding Auto Loans. (External Link)

Conclusion: Your Path to a Credit Union Car Loan

So, will your credit union give you a car loan? With the right preparation, a solid understanding of the factors involved, and a proactive approach, the answer is overwhelmingly likely to be yes. Credit unions offer a compelling alternative to traditional banks, often providing lower rates, more flexible terms, and a personalized, member-focused experience.

By focusing on improving your credit score, managing your debt, securing a down payment, and approaching the application process with diligence, you can significantly enhance your chances of approval. Remember, your credit union is there to serve its members. Leverage their expertise, ask questions, and be transparent about your financial situation. Doing so will not only help you secure a great car loan but also build a stronger financial future. Drive confidently towards your next vehicle purchase with a trusted credit union by your side!