Your Credit Score and Car Loans: The Ultimate Guide to Driving Away with the Best Deal

Your Credit Score and Car Loans: The Ultimate Guide to Driving Away with the Best Deal Carloan.Guidemechanic.com

The dream of a new car often comes with the reality of financing. For most people, securing an auto loan is a necessary step, and at the heart of that process lies a crucial three-digit number: your credit score. This little number holds immense power, dictating not just whether you’ll get approved, but also the entire cost of your vehicle over its lifetime. Understanding the intricate relationship between your credit score and car loans is the first gear you need to shift into before stepping onto a dealership lot.

This comprehensive guide will demystify everything you need to know about your car loan credit score, from what constitutes a "good" score to actionable strategies for improving yours. We’ll dive deep into how lenders assess risk, the impact on interest rates, and common pitfalls to avoid, ensuring you’re well-equipped to secure the best possible car financing credit score deal.

Your Credit Score and Car Loans: The Ultimate Guide to Driving Away with the Best Deal

What Exactly is a Credit Score and Why Does It Matter for a Car Loan?

At its core, a credit score is a numerical representation of your creditworthiness. It’s a snapshot of your financial reliability, based on your past borrowing and repayment behavior. While various scoring models exist, the most common are FICO Scores and VantageScores, both ranging from 300 to 850. Lenders use these scores to quickly assess the risk of lending you money. A higher score signals less risk, while a lower score indicates a higher probability of default.

When it comes to securing an auto loan credit score, this number is paramount. Lenders want to know they’ll be repaid, and your credit score is their primary indicator. Based on my experience in the financial sector, lenders aren’t just looking for a "yes" or "no" on an application; they’re calculating the potential for profit versus the risk involved. A strong credit score tells them you’re a responsible borrower, making them more willing to offer you favorable terms. Conversely, a low score makes them hesitant, often leading to higher interest rates or even outright denial.

The Credit Score Tiers: What’s Considered "Good" for a Car Loan?

Credit scores are typically categorized into different tiers, each with its own implications for loan eligibility and terms. While specific ranges can vary slightly between models and lenders, here’s a general breakdown of what’s considered "good" for a car loan credit score:

- Excellent (800-850): This is the top tier. Borrowers in this range are considered exceptionally low-risk and will qualify for the absolute best interest rates and loan terms available.

- Very Good (740-799): Still an excellent range. You’ll likely receive highly competitive interest rates and favorable terms, often very close to those with excellent scores.

- Good (670-739): This is the sweet spot for many borrowers. With a good credit for car loan, you’re considered a reliable borrower and can expect good interest rates, though perhaps not the absolute lowest. Most mainstream lenders will be eager to work with you.

- Fair (580-669): In this range, you might still qualify for a car loan, but you’ll likely face higher interest rates. Lenders perceive a moderate risk. Options might be more limited, and you might need to make a larger down payment.

- Poor (300-579): Obtaining a traditional car loan with a bad credit car loan score in this range can be challenging. Approval is less likely, and if approved, interest rates will be significantly higher, sometimes even predatory. You might need a co-signer or explore specialized lenders.

Understanding these tiers helps you gauge your position before applying. Knowing where you stand can empower you to either seek out the best deals or focus on improving your score before making a significant purchase.

How Your Credit Score Impacts Your Car Loan: Beyond Approval

While approval is the immediate concern, the reach of your credit score to get a car loan extends far beyond a simple yes or no. It profoundly influences every aspect of your loan, ultimately determining how much you pay for your vehicle over time.

Interest Rates: The Cost of Borrowing

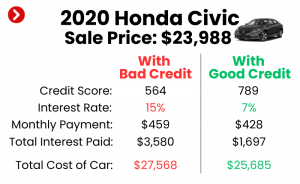

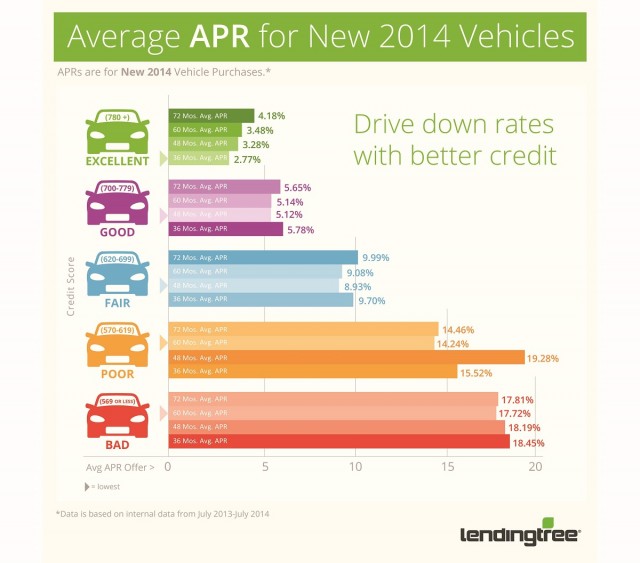

This is arguably the most significant impact. A higher credit score directly translates to a lower interest rate. Even a percentage point difference can save you hundreds, if not thousands, of dollars over a 60-month or 72-month loan term. For example, a borrower with an excellent score might qualify for an APR of 3%, while someone with a fair score could be looking at 8% or even 12% for the exact same car and loan amount. That difference compounds quickly.

Loan Terms: Flexibility and Monthly Payments

Lenders are more willing to offer flexible and favorable loan terms to borrowers with strong credit. This could mean shorter loan durations (which save you money on interest) or more manageable monthly payments if you opt for a slightly longer term at a low rate. Conversely, those with lower scores might be pushed towards longer terms to reduce monthly payments, but this means paying significantly more in interest over the life of the loan.

Down Payment Requirements

While a down payment is always a good idea, it becomes almost essential for those with lower credit scores. Lenders may require a larger down payment to mitigate their risk, as it demonstrates your commitment and reduces the total amount they’re financing. A strong credit score for car loan might allow you to put down less, or even nothing, though we generally advise against zero down payments if possible.

Loan Amount and Vehicle Choice

Your credit score can also influence the maximum amount a lender is willing to finance. If your score is low, lenders might cap the loan amount, limiting your choices to less expensive vehicles. A robust credit score, on the other hand, provides you with more purchasing power and a wider selection of cars.

Pro tips from us: Always aim for the highest possible credit score before applying for an auto loan. The financial savings on interest alone can be substantial, making the effort well worth it. Even a small improvement can shift you into a better rate tier.

Demystifying Your Credit Report: The Foundation of Your Score

Your credit score isn’t some arbitrary number; it’s a reflection of the information contained within your credit report. This detailed document, maintained by the three major credit bureaus (Experian, Equifax, and TransUnion), is what lenders scrutinize to understand your financial behavior. Understanding its components is key to understanding your credit score to get a car loan.

The primary factors influencing your score, weighted differently, typically include:

- Payment History (35%): This is the most critical factor. Paying bills on time consistently demonstrates reliability. Late payments, defaults, bankruptcies, and collections significantly harm your score.

- Amounts Owed (30%): This refers to your total outstanding debt and, crucially, your credit utilization ratio. This ratio compares the amount of credit you’re using to your total available credit. Keeping this ratio low (ideally below 30%) shows you’re not over-reliant on credit.

- Length of Credit History (15%): The longer your accounts have been open and in good standing, the better. It shows a track record of responsible borrowing.

- New Credit (10%): This includes recent credit applications and newly opened accounts. A flurry of new applications in a short period can be seen as risky behavior.

- Credit Mix (10%): Having a healthy mix of different types of credit (e.g., credit cards, installment loans like mortgages or student loans) can positively impact your score, showing you can manage various credit products responsibly.

Before you even think about applying for a car loan, it’s crucial to review your credit report. You’re entitled to a free copy from each of the three major credit bureaus once a year through AnnualCreditReport.com. Check for any inaccuracies, fraudulent activity, or outdated information. Errors can unfairly depress your car financing credit score, and disputing them promptly can lead to a significant boost.

Strategies to Improve Your Credit Score for a Car Loan

If your current credit score for car loan isn’t where you want it to be, don’t despair. There are concrete steps you can take to improve it, sometimes even in a relatively short period. Proactive credit management is your best friend here.

- Pay All Your Bills On Time, Every Time: This is the single most impactful action you can take. Payment history accounts for 35% of your FICO score. Set up automatic payments, use reminders, and prioritize minimum payments if you can’t pay in full. Even one late payment can cause a significant drop.

- Reduce Your Credit Card Debt: High credit card balances negatively impact your credit utilization ratio (amounts owed). Focus on paying down your highest-interest credit cards first, or those closest to their credit limit. Aim to keep your utilization below 30% across all cards, and ideally even lower, around 10%.

- Avoid Opening New Credit Accounts: Resist the urge to open new credit cards or loans just before applying for a car loan. Each new application generates a "hard inquiry" on your report, which can slightly ding your score. Additionally, new accounts lower the average age of your credit, which can also be detrimental.

- Don’t Close Old, Paid-Off Accounts: While it might seem counterintuitive, closing old credit card accounts can actually hurt your score. It reduces your total available credit, which can increase your credit utilization ratio, and shortens the length of your credit history. Keep them open, even if you rarely use them.

- Dispute Any Errors on Your Credit Report: As mentioned, errors can unfairly lower your score. Carefully review your report from each bureau and dispute any inaccuracies immediately. The Fair Credit Reporting Act (FCRA) gives you the right to have incorrect information removed.

- Consider a Secured Credit Card or Credit-Builder Loan: If you have very limited or poor credit, these tools can help you establish or rebuild a positive payment history. A secured credit card requires a deposit, which acts as your credit limit, while a credit-builder loan involves saving money in an account while making regular payments.

Common mistakes to avoid are: Thinking that simply having credit is enough; you must use it responsibly. Also, don’t fall for "credit repair" scams that promise quick fixes – genuine credit improvement takes time and discipline. For more detailed steps on boosting your credit, check out our guide on .

Getting a Car Loan with Less-Than-Perfect Credit

Even if your credit score to get a car loan isn’t in the "good" or "excellent" range, securing an auto loan isn’t impossible. It just requires more strategic planning and a realistic understanding of your options. Getting a bad credit car loan means navigating a different landscape.

- Be Prepared for Higher Interest Rates: This is the unavoidable truth. Lenders take on more risk when approving loans for borrowers with lower scores, and they compensate for that risk with higher interest rates. Factor this into your budget.

- Save for a Larger Down Payment: A substantial down payment can significantly improve your chances of approval and potentially lower your interest rate. It reduces the amount you need to borrow and signals your commitment to the lender.

- Consider a Co-signer: A co-signer with good credit can dramatically increase your chances of approval and help you secure a better interest rate. However, understand that a co-signer is equally responsible for the loan, and their credit will be affected if you miss payments.

- Explore Secured Car Loans: Some lenders offer secured auto loans, where the car itself acts as collateral. While this can make approval easier, understand the risks involved if you default on payments.

- Research Specialized Lenders: Not all lenders are created equal. Some specialize in helping borrowers with less-than-perfect credit. These might include credit unions, subprime lenders, or online auto loan platforms. Be wary of extremely high-interest rates.

- "Buy Here, Pay Here" Dealerships: These dealerships offer in-house financing, often without stringent credit checks. While they can be an option for those with very poor credit, their interest rates are typically very high, and terms can be less favorable. Proceed with extreme caution and read all contracts thoroughly.

- Patience and Research: Don’t jump at the first offer. Shop around and compare rates from multiple lenders. Getting pre-approved from several places allows you to compare offers without impacting your score multiple times (as long as inquiries are made within a certain timeframe, usually 14-45 days, they’ll count as one for scoring purposes).

If you’re navigating the complexities of financing with challenges, our article on provides further insights into various lending scenarios. Remember, getting a car loan with bad credit can be a stepping stone to improving your credit if you make all your payments on time.

The Car Loan Application Process: What to Expect

Once you’ve done your homework on your credit score to get a car loan and prepared your finances, it’s time to approach the application process. Knowing what to expect can reduce stress and help you make informed decisions.

- Check Your Credit Report and Score: Before anything else, pull your credit report and score. This gives you a realistic understanding of your position and allows you to correct any errors.

- Determine Your Budget: Don’t just think about the monthly payment. Consider the total cost of the car, including insurance, fuel, maintenance, and registration.

- Get Pre-Approved: This is a crucial step. Seek pre-approval from multiple banks, credit unions, and online lenders before visiting a dealership. Pre-approval gives you a concrete loan offer (interest rate, loan amount, terms) and empowers you to negotiate with the dealership from a position of strength. It also typically involves a "soft inquiry" on your credit, which doesn’t affect your score.

- Gather Necessary Documents: Lenders will require documentation such as proof of income (pay stubs, tax returns), proof of residence (utility bills), identification (driver’s license), and potentially bank statements.

- Understand Soft vs. Hard Inquiries: Pre-qualification often uses a soft inquiry, which doesn’t impact your score. A formal loan application, however, results in a hard inquiry, which can temporarily lower your score by a few points. Multiple hard inquiries for the same type of loan within a short window (typically 14-45 days, depending on the scoring model) are usually treated as a single inquiry, so comparison shopping for auto loans is encouraged.

- Negotiate Smartly: With a pre-approval in hand, you can focus on negotiating the car’s price at the dealership, rather than simultaneously negotiating the loan. If the dealership can beat your pre-approved rate, great! If not, you have a solid backup.

Pro tips from us: Don’t let the dealership "shop your credit" to dozens of lenders without your explicit consent. This can lead to numerous hard inquiries and unnecessary dings to your score. Be firm and in control of the process.

Conclusion: Driving Towards Financial Freedom

The journey to purchasing a car is multifaceted, but understanding the pivotal role of your credit score to get a car loan is undeniably the most important first step. Your credit score isn’t just a number; it’s a reflection of your financial past that directly shapes your automotive future. From securing the lowest interest rates to dictating your monthly payments, a healthy car financing credit score is your key to unlocking the best possible deal.

By taking the time to understand your credit report, actively work on improving your score, and approaching the loan application process strategically, you empower yourself to make informed decisions. Whether you’re aiming for an excellent score or working to rebuild, proactive credit management will not only benefit your car loan but also pave the way for broader financial stability. Drive away with confidence, knowing you’ve secured a deal that truly benefits your wallet.