Your Credit Score for a Used Car Loan: The Ultimate Guide to Driving Away with Confidence

Your Credit Score for a Used Car Loan: The Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

Securing a used car loan can feel like navigating a complex maze, especially when your credit score comes into play. For many, a reliable vehicle is essential, but the path to financing it often begins and ends with that crucial three-digit number. Understanding how your credit score impacts your ability to get a used car loan, the interest rates you’ll pay, and even the terms you’ll be offered is paramount.

This comprehensive guide will demystify the relationship between your credit score and used car financing. We’ll explore what lenders look for, how to improve your standing, and smart strategies to secure the best possible deal, regardless of your credit history. Our ultimate goal is to empower you to make informed decisions and drive away in your dream used car with confidence.

Your Credit Score for a Used Car Loan: The Ultimate Guide to Driving Away with Confidence

Understanding Your Credit Score: The Foundation of Auto Financing

Before diving into the specifics of used car loans, let’s establish a clear understanding of what a credit score actually is. In essence, it’s a numerical representation of your creditworthiness, a snapshot of your financial responsibility. Lenders use this score to assess the risk associated with lending you money. A higher score indicates a lower risk, suggesting you’re more likely to repay your debts.

The most widely recognized credit scoring models are FICO and VantageScore, both generating scores typically ranging from 300 to 850. These scores are calculated based on the information contained within your credit report, which is compiled by the three major credit bureaus: Experian, Equifax, and TransUnion. Knowing your score, and what it means, is the first critical step in your used car buying journey.

Why Your Credit Score is Crucial for Used Car Loans

Your credit score isn’t just a number; it’s a powerful tool that dictates many aspects of your used car loan. Lenders rely heavily on this metric because used cars, by their nature, carry certain risks. They can depreciate faster, may require more maintenance, and their value can be harder to precisely assess compared to new vehicles. Therefore, lenders need a solid indicator of your repayment reliability.

A strong credit score signals to lenders that you are a responsible borrower with a history of timely payments. This reduces their perceived risk, making them more willing to offer you favorable terms. Conversely, a lower score suggests a higher risk of default, which can lead to higher costs or even outright denial of your loan application. It truly is the gatekeeper to affordable used car financing.

How Your Credit Score Shapes Your Used Car Loan Experience

The impact of your credit score on a used car loan extends far beyond just approval or denial. It influences several key components that determine the overall affordability and convenience of your financing. Understanding these effects can help you prepare and potentially save you thousands of dollars over the life of the loan.

Interest Rates: The Cost of Borrowing

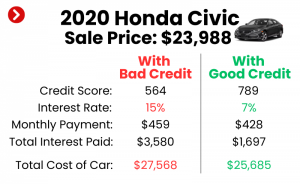

This is perhaps the most significant impact. Your credit score directly correlates with the interest rate you’ll be offered. Borrowers with excellent credit scores typically qualify for the lowest interest rates, often in the single digits. This means a smaller portion of your monthly payment goes towards interest, and more towards paying down the principal of the loan.

On the other hand, individuals with lower credit scores are seen as higher risk, leading lenders to charge higher interest rates to compensate for that risk. These rates can easily climb into the double digits, significantly increasing your total cost of borrowing. A difference of just a few percentage points can add hundreds or even thousands of dollars to the total price of your used car over several years.

Loan Approval: Getting the Green Light

Simply put, a higher credit score drastically increases your chances of loan approval. Lenders have specific criteria they must meet, and your credit score is a primary filter. If your score falls below a certain threshold, some lenders might automatically decline your application, regardless of other factors.

While it’s still possible to get a used car loan with a lower score, your options may be limited to subprime lenders or dealerships that specialize in high-risk loans. These often come with less favorable terms and higher rates. A strong credit score opens doors to a wider range of lenders, giving you more choices and better negotiating power.

Loan Terms: Flexibility and Freedom

Beyond interest rates and approval, your credit score also influences the terms of your loan. With excellent credit, you might have more flexibility in choosing a longer repayment period, which can result in lower monthly payments. You might also be able to secure a loan with a lower, or even no, down payment requirement.

Conversely, a lower credit score might force you into a shorter loan term to reduce the lender’s risk, leading to higher monthly payments. Lenders might also require a substantial down payment to offset their risk, demanding more cash upfront from you. Your credit score essentially dictates how much control you have over the structure of your loan.

Down Payment Requirements: Your Upfront Investment

For borrowers with lower credit scores, lenders often require a larger down payment. This serves two purposes: it reduces the amount the lender has to finance, thereby lowering their risk, and it demonstrates your commitment to the purchase. While a larger down payment is always a good idea to reduce your loan amount and interest, it might become a mandatory hurdle if your credit isn’t stellar.

Based on my experience, a significant down payment, even for those with good credit, can make your application look even stronger. It shows financial prudence and immediately reduces the loan-to-value ratio, which lenders appreciate. For those with fair or poor credit, it can often be the deciding factor in getting approved at all.

Decoding Credit Score Ranges for Used Car Loans

Understanding the general categories of credit scores can help you gauge where you stand and what to expect when applying for a used car loan. While exact thresholds can vary slightly between lenders, these ranges provide a good benchmark.

- Excellent (800-850): Congratulations! With a score in this range, you’re considered a prime borrower. You’ll qualify for the absolute best interest rates, often enjoying promotional offers and highly flexible terms. Lenders will be eager to work with you.

- Very Good (740-799): Still in a fantastic position. You’ll receive very competitive interest rates and favorable loan terms. Most lenders will approve your application without hesitation. Your options for financing will be plentiful.

- Good (670-739): This is generally considered the sweet spot for many borrowers. You’ll qualify for good interest rates, though perhaps not the absolute lowest. Approval is highly likely, and you’ll still have a decent selection of lenders to choose from. This is where most mainstream lenders are comfortable.

- Fair (580-669): This range is where things start to get a bit tougher. You’re likely to be approved for a used car loan, but you’ll face higher interest rates. Lenders might require a larger down payment or a co-signer. Options might be more limited to certain financial institutions or dealership financing.

- Poor (300-579): Securing a used car loan with a score in this range can be challenging. Approval is less certain, and if approved, you’ll likely encounter significantly higher interest rates, stricter terms, and potentially mandatory down payments or co-signer requirements. Your best bet might be specialized subprime lenders.

Factors That Influence Your Credit Score (and How They Relate to Car Loans)

To truly understand your credit score’s impact, it’s essential to know what factors contribute to it. The FICO scoring model, for instance, breaks down these factors into key percentages:

- Payment History (35%): This is the most crucial factor. Consistently paying your bills on time demonstrates reliability. For a car loan, lenders look for a history of timely payments on previous loans and credit cards. Even one late payment can significantly ding your score and raise a red flag.

- Amounts Owed (30%): This refers to your credit utilization – the amount of credit you’re using compared to your total available credit. Keeping your credit utilization low (ideally below 30%) is beneficial. High utilization can indicate financial strain, which makes lenders wary of adding another loan to your plate.

- Length of Credit History (15%): The longer your credit accounts have been open and active, the better. A longer history provides more data for lenders to assess your long-term financial behavior. Newer borrowers might find it slightly harder to get the best rates simply due to a lack of extensive history.

- New Credit (10%): Opening too many new credit accounts in a short period can be seen as risky. Each hard inquiry (when a lender pulls your credit report) can temporarily lower your score. While shopping for a car loan, multiple inquiries within a short window (usually 14-45 days) are often grouped as one for scoring purposes, so it’s wise to do all your rate shopping at once.

- Credit Mix (10%): Having a healthy mix of different types of credit (e.g., credit cards, installment loans like a student loan or mortgage) shows you can manage various forms of debt responsibly. For a used car loan, having a history of successfully managing an installment loan can be particularly beneficial.

Strategies to Boost Your Credit Score Before Applying for a Used Car Loan

If your credit score isn’t where you want it to be, don’t despair! There are actionable steps you can take to improve it. Pro tips from us: start this process well in advance of when you plan to buy a car, ideally six months to a year out, as changes take time to reflect.

- Obtain and Review Your Credit Report: This is your starting point. You’re entitled to a free copy of your credit report from each of the three major bureaus annually via AnnualCreditReport.com. Check for any errors, fraudulent accounts, or outdated information. Disputing inaccuracies can quickly improve your score.

- Pay All Bills On Time, Every Time: This cannot be stressed enough. Set up automatic payments or calendar reminders for all your credit obligations, from credit cards to utility bills. A consistent history of on-time payments is the most powerful way to build good credit.

- Reduce Your Existing Debt: Focus on paying down credit card balances. Lowering your credit utilization ratio (the amount of credit you use compared to your total available credit) can significantly boost your score. Aim to keep balances below 30% of your credit limit, or even lower if possible.

- Avoid Opening New Credit Accounts: Resist the temptation to open new credit cards or take out other loans just before applying for a car loan. Each new application results in a hard inquiry, which can temporarily drop your score. You want your credit profile to look stable.

- Consider Becoming an Authorized User: If a trusted family member with excellent credit is willing, becoming an authorized user on one of their credit card accounts can help. Their positive payment history will then reflect on your report, but only do this if you are absolutely sure they are financially responsible.

- Maintain Old Accounts: Don’t close old credit card accounts, even if you don’t use them. The length of your credit history is a factor, and closing old accounts can shorten your average account age, potentially hurting your score.

Navigating Used Car Loans with Less-Than-Perfect Credit

While a high credit score is ideal, it’s still possible to get a used car loan if your credit isn’t stellar. However, you’ll need to approach the process with realistic expectations and be prepared for certain trade-offs.

Realistic Expectations

Firstly, accept that you will likely face higher interest rates compared to prime borrowers. Your loan terms might be stricter, and you may not have as much flexibility in choosing a longer repayment period. The key is to find a loan that is manageable and allows you to rebuild your credit.

Options to Improve Your Chances

- Secure a Co-signer: A co-signer with good credit can significantly increase your chances of approval and help you secure better terms. This is because the co-signer agrees to be legally responsible for the loan if you default. Choose someone you trust implicitly and who understands the commitment.

- Offer a Larger Down Payment: As discussed, a substantial down payment reduces the lender’s risk. The more money you put down upfront, the less you need to borrow, making you a more attractive applicant. This also reduces your monthly payments and total interest paid.

- Shop Around for Specialized Lenders: Don’t just go to the first dealership. Look into credit unions, online lenders, and financial institutions that specialize in subprime auto loans. Their criteria can vary, and one might offer you a better deal than another.

- Consider a Less Expensive Vehicle: A lower-priced used car means a smaller loan amount, which can be easier to get approved for and more manageable to repay, especially with higher interest rates. It’s often smarter to start with a more affordable option and upgrade later once your credit improves.

- Shorter Loan Term: While this means higher monthly payments, a shorter loan term can sometimes be more appealing to lenders as it reduces their exposure to risk over time. It also means you pay less in total interest.

Common mistakes to avoid when you have less-than-perfect credit include accepting the first offer without comparison, getting talked into expensive add-ons you don’t need, or stretching your budget too thin just to get a car. Always prioritize what you can realistically afford.

The Used Car Loan Application Process: What to Expect

The process of applying for a used car loan can be streamlined if you’re prepared. Knowing what to expect will help you navigate it smoothly.

- Know Your Credit Score and Report: Before you even start car shopping, get your credit score and review your reports. This empowers you to understand your standing and address any issues.

- Get Pre-approved: This is a crucial step. Seek pre-approval from several lenders (banks, credit unions, online lenders) before you visit a dealership. Pre-approval gives you a clear understanding of the interest rate you qualify for and the maximum amount you can borrow. It also gives you leverage when negotiating with the dealer’s financing department.

- Gather Necessary Documents: Lenders will typically require proof of income (pay stubs, tax returns), proof of residence (utility bills, lease agreement), identification (driver’s license), and potentially bank statements. Having these ready will expedite the process.

- Understand All Terms: Don’t just focus on the monthly payment. Pay close attention to the interest rate (APR), the loan term, any fees, and whether there’s a prepayment penalty.

- Read the Fine Print: Always read the entire loan agreement before signing. Ensure all figures match what you were promised and that there are no hidden clauses. If something is unclear, ask for clarification.

- Negotiate: With a pre-approval in hand, you’re in a strong position to negotiate not only the price of the car but also the financing terms. The dealership might try to beat your pre-approved rate, or you might use your pre-approval to negotiate a better price for the vehicle.

For checking your credit report and score, a trusted external source like MyFICO.com or Experian.com can provide valuable insights and tools.

Pro Tips for a Smooth Used Car Loan Experience

Based on my years of observing the auto financing landscape, these tips can make a significant difference in your used car loan journey:

- Don’t Rush the Process: Buying a car is a major financial decision. Take your time to research vehicles, lenders, and understand your financial position. Hasty decisions often lead to regret.

- Set a Realistic Budget: Look beyond just the monthly payment. Consider insurance, maintenance, fuel costs, and potential repairs for a used car. Your total car ownership cost should comfortably fit within your budget.

- Get Multiple Loan Offers: This is non-negotiable. Compare interest rates, fees, and terms from at least 3-5 different lenders. Even a small difference in APR can save you hundreds over the life of the loan.

- Be Aware of "Upselling" at the Dealership: Dealerships often try to sell you extended warranties, GAP insurance, and other add-ons. While some might be beneficial, others are overpriced. Research these options beforehand and decide what you truly need.

- Focus on the Total Cost, Not Just Monthly Payments: A common dealer trick is to extend the loan term to lower monthly payments, making the car seem more affordable. However, a longer term means you pay significantly more in total interest. Always consider the total amount you’ll pay over the life of the loan.

- Consider a Shorter Loan Term if Possible: If your budget allows, opting for a 36- or 48-month loan instead of a 60- or 72-month one will save you a considerable amount in interest, even if your monthly payment is higher.

Maintaining Good Credit After Your Loan

Your journey doesn’t end once you drive off the lot. Successfully managing your used car loan is an excellent opportunity to further build and maintain a strong credit profile.

- Make Payments On Time, Every Time: This is the golden rule. Your car loan is an installment loan, and consistent, on-time payments will be reported to credit bureaus, significantly boosting your payment history and overall score.

- Avoid Defaulting: Missing payments or defaulting on your car loan will severely damage your credit score, making it difficult to secure future loans for a home, another car, or even credit cards.

- Monitor Your Credit Report Periodically: Even after securing your loan, it’s wise to check your credit report once a year to ensure all payments are being reported correctly and there are no new errors or fraudulent activities.

- Understand How a Paid-Off Loan Helps: Once you successfully pay off your used car loan, it remains on your credit report as a positive mark for several years, demonstrating your ability to manage and repay debt responsibly. This contributes to a robust credit history.

Building a strong financial future extends beyond just your car loan. For more insights on financial wellness, you might find our article on "Building a Strong Financial Future: Beyond Your Car Loan" helpful.

Conclusion: Drive Away with Confidence

Your credit score is an undeniably powerful factor in securing a used car loan. It dictates not only your chances of approval but also the critical terms of your loan, from interest rates to down payment requirements. By understanding how your score works, actively working to improve it, and strategically navigating the application process, you can transform a potentially stressful experience into a successful one.

Remember, preparation is key. Know your score, clean up your credit report, get pre-approved, and compare offers diligently. With these strategies, you’re not just buying a used car; you’re investing in your financial future and driving away with the confidence that comes from making an informed decision. Start your journey to a better used car loan today, and take control of your financial destiny.