Your Key to the Road: Unlocking the Power of a $3,000 Car Loan

Your Key to the Road: Unlocking the Power of a $3,000 Car Loan Carloan.Guidemechanic.com

Securing a car loan, especially for a smaller amount like $3,000, might seem like a straightforward task, but it often comes with its own unique set of considerations. Many people assume that lenders are only interested in financing brand-new, high-value vehicles, leaving those in need of a budget-friendly option feeling overlooked. This couldn’t be further from the truth.

A $3,000 car loan can be a game-changer, opening doors to reliable transportation without breaking the bank. Whether you’re a first-time buyer, need a temporary solution, or are looking to rebuild your credit, understanding the ins and outs of securing a 3k car loan is essential. This comprehensive guide will equip you with all the knowledge you need to navigate the process confidently, ensuring you drive away with the best possible deal.

Your Key to the Road: Unlocking the Power of a $3,000 Car Loan

Understanding the $3,000 Car Loan Landscape

The idea of a "small" car loan might seem niche, but a $3,000 car loan is more common and more impactful than many realize. It often represents the perfect financing solution for individuals looking to purchase an affordable, pre-owned vehicle. This amount typically covers the cost of an older, yet still reliable, used car, or it can serve as a substantial down payment on a slightly more expensive model.

Lenders approach smaller loans with a slightly different lens compared to larger, new car financing. While the loan amount is less, the principles of creditworthiness and repayment capacity remain paramount. Understanding this landscape is your first step toward successful approval.

Is a $3k Loan Common? What Are the Typical Scenarios?

Absolutely, a $3,000 car loan is a very common request, particularly in the used car market. Many buyers seek out vehicles in the $3,000 to $7,000 range, and a loan for $3,000 can cover a significant portion, or even all, of the purchase price for a truly budget-friendly car. It’s often the sweet spot for those needing basic transportation without the burden of a large debt.

Typical scenarios include students needing their first car, individuals who’ve had an unexpected vehicle breakdown and require a quick replacement, or someone simply looking for an affordable second car for commuting. It’s also a popular option for those with limited credit history or those actively working to improve their credit scores through responsible borrowing.

Why This Specific Amount Can Be Tricky (and Advantageous)

While common, a $3,000 car loan can sometimes be tricky for lenders. The administrative costs associated with processing any loan, regardless of size, are relatively fixed. For a very small loan, these costs can represent a larger percentage of the total loan value, making it less profitable for some lenders. This means some traditional banks might prefer not to underwrite such small amounts.

However, this amount is also highly advantageous for borrowers. It keeps your monthly payments manageable, reducing your financial strain and making it easier to repay on time. For lenders, it represents a lower risk compared to a $30,000 loan, potentially making them more flexible with approval criteria for certain applicants.

Who Needs a 3k Car Loan? (And Why It’s a Smart Choice for Some)

A 3k car loan serves a diverse range of individuals, each with unique circumstances that make this specific loan amount an ideal fit. Recognizing if you fall into one of these categories can help you articulate your needs to a lender more effectively. It’s not just about the money; it’s about the purpose it serves.

First-Time Buyers on a Budget

For many young adults or individuals purchasing their very first car, a $3,000 car loan offers an accessible entry point into vehicle ownership. They might not have extensive credit history or a large down payment saved, making a more expensive vehicle financially out of reach. This small loan allows them to build credit responsibly while gaining independence.

Those Needing a Temporary Vehicle

Life throws unexpected curveballs. Perhaps your old car unexpectedly broke down beyond repair, or you need a reliable vehicle for a short-term project or move. A 3k car loan can provide the immediate funds to secure a functional, albeit older, car to bridge the gap until a more permanent solution is viable. It’s a practical, immediate fix.

Individuals Rebuilding Credit

A $3,000 car loan can be an excellent tool for credit building. By making consistent, on-time payments, you demonstrate financial responsibility to credit bureaus. This positive payment history can significantly boost your credit score over time, paving the way for better financial opportunities in the future. It’s a stepping stone to better credit.

Students or Those with Limited Income

Students often require transportation for classes, part-time jobs, or internships but have limited income and a tight budget. Similarly, individuals with lower incomes might find a $3,000 car loan to be the most affordable way to secure reliable transport for work and daily life. It’s about practicality and essential access.

Emergency Situations

Sometimes, a car isn’t a luxury but a necessity. In emergency situations, such as needing to transport a sick family member or secure a job that requires a vehicle, a quick $3,000 car loan can provide immediate relief. It’s a solution when time is of the essence and immediate funds are needed for a crucial asset.

Navigating Lender Expectations for Small Loans

Lenders, regardless of the loan size, want assurance that you can and will repay your debt. For a $3,000 car loan, their focus intensifies on certain aspects of your financial profile. Understanding these expectations can significantly improve your chances of approval.

Credit Score Impact

Your credit score is a primary indicator of your financial reliability. For a 3k car loan, its impact is still significant, though some lenders might be more flexible for smaller amounts.

- Good Credit: If you have a strong credit score (typically 670+), you’re in an excellent position. Lenders will see you as a low-risk borrower, making approval easier and securing you the most favorable interest rates. You might even find traditional banks more willing to offer you a $3,000 car loan.

- Fair/Bad Credit: Don’t despair if your credit score is less than ideal. A $3,000 car loan is often more accessible for those with fair (580-669) or even bad credit (below 580) compared to larger loans. However, expect higher interest rates and potentially stricter terms. Based on my experience, lenders are more cautious with small amounts for those with lower scores, so demonstrating stability in other areas is key. You might need to explore specialized lenders or dealerships.

Income Requirements

Even for a small $3,000 car loan, lenders need proof of a stable income source. They want to see that you have sufficient funds coming in regularly to cover the monthly payments comfortably. This doesn’t necessarily mean a high income, but rather consistent income.

You’ll typically need to provide pay stubs, bank statements, or tax returns to verify your earnings. Lenders will assess your income against your existing debts to determine if you can realistically afford the additional car payment.

Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is crucial. This percentage compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available, making you a less risky borrower.

Lenders generally prefer a DTI ratio below 43%, though this can vary. For a $3,000 car loan, having a manageable DTI will greatly improve your approval odds, as it demonstrates that adding a small car payment won’t overextend your finances.

Down Payment

While not always strictly required for a small $3,000 car loan, a down payment can significantly boost your application. Even a modest down payment, say $500 or $1,000, shows a lender that you have skin in the game and are committed to the purchase.

Pro tips from us: A down payment reduces the amount you need to borrow, which can lower your monthly payments and the total interest paid over the life of the loan. It also signals financial responsibility, potentially offsetting a less-than-perfect credit score.

Vehicle Age/Mileage

Lenders are typically financing the vehicle itself, and its value serves as collateral. For a $3,000 car loan, you’ll likely be looking at older, higher-mileage used cars. While lenders understand this, there’s a limit.

Very old cars (e.g., 15+ years) or those with extremely high mileage (e.g., 200,000+ miles) can be difficult to finance through traditional lenders. They may see these vehicles as too high-risk for potential breakdowns, which could impact your ability to repay the loan. Focus on cars that, while affordable, still have some life left in them.

Where to Find a $3,000 Car Loan

Knowing where to look is just as important as knowing what lenders expect. Different types of lenders cater to different credit profiles and loan amounts. Exploring your options will help you find the best fit for your $3,000 car loan.

Banks & Credit Unions

Traditional banks and local credit unions are often the first choice for car loans due to their competitive interest rates. If you have good credit and a solid financial history, they are an excellent option for a $3,000 car loan.

- Banks: While major banks might prefer larger loans, some are willing to offer smaller auto loans, especially if you’re an existing customer with a good relationship.

- Credit Unions: Pro tips from us: Don’t overlook local credit unions; they often have more flexible terms for their members, even for smaller amounts like a 3k car loan. They are member-focused and might be more understanding of individual circumstances.

Online Lenders

The digital age has brought a plethora of online lenders specializing in various loan types, including car loans for a range of credit scores. Many online platforms offer quick approval processes and can be a great resource for a $3,000 car loan.

These lenders often have broader criteria, making them accessible even if you have fair or average credit. Always check their reputation and read reviews before applying, and ensure they are legitimate.

Dealership Financing (Buy Here Pay Here)

For those with challenging credit histories, "Buy Here Pay Here" (BHPH) dealerships can be a viable option. These dealerships directly finance the cars they sell, often without stringent credit checks.

While they can be a lifeline for bad credit, be aware that interest rates are typically much higher than traditional lenders. Carefully read the terms and understand the total cost of the loan before committing. It’s a trade-off between accessibility and cost.

Personal Loans (Unsecured)

An unsecured personal loan is another alternative for securing $3,000. Unlike an auto loan, a personal loan isn’t tied to the car itself, meaning the vehicle isn’t used as collateral.

While this offers flexibility, interest rates for personal loans can often be higher than secured auto loans, especially if your credit isn’t stellar. Weigh the pros and cons carefully. For a deeper dive into understanding the differences, check out our guide on .

The Application Process: Step-by-Step Guide

Applying for a $3,000 car loan doesn’t have to be daunting. By following a structured approach, you can streamline the process and increase your chances of approval. Each step builds on the last, ensuring you’re well-prepared.

Step 1: Assess Your Financial Health

Before approaching any lender, take an honest look at your finances. This includes checking your credit score and report, calculating your monthly income versus expenses, and understanding your existing debt obligations. Knowing your financial standing empowers you to choose the right lenders and anticipate their requirements.

Step 2: Gather Necessary Documents

Preparation is key. Lenders will require several documents to verify your identity, income, and residency. Having these ready will expedite your application.

Common documents include: government-issued ID (driver’s license), proof of income (pay stubs, tax returns, bank statements), proof of residency (utility bill, lease agreement), and sometimes references.

Step 3: Get Pre-Approved

Seeking pre-approval is crucial, especially for a $3,000 car loan. Pre-approval gives you a clear idea of how much you can borrow, at what interest rate, and under what terms. This allows you to shop for a car with confidence, knowing your budget.

It also gives you leverage at the dealership, as you already have financing secured. Many lenders offer pre-qualification with a soft credit check, which won’t impact your score.

Step 4: Shop Smartly for Your Car

With pre-approval in hand, you can focus on finding the right vehicle within your $3,000 budget. Prioritize reliability, safety, and a car that meets your essential needs.

Always aim to get a pre-purchase inspection from an independent mechanic to uncover any hidden issues. For a $3,000 car, this step is non-negotiable to avoid costly repairs down the line.

Step 5: Finalize the Loan

Once you’ve found your car, it’s time to finalize the loan. Carefully review all the terms and conditions, including the interest rate, loan term, monthly payment, and any fees. Don’t hesitate to ask questions if anything is unclear.

Ensure you understand the total cost of the loan, not just the monthly payment. Sign only when you are completely comfortable and have a copy of all documents.

Maximizing Your Chances of 3k Car Loan Approval

Even with a small loan amount, approval isn’t guaranteed. Taking proactive steps to present yourself as a reliable borrower can significantly improve your odds. These strategies are particularly helpful for a $3,000 car loan.

Improve Your Credit Score (Even Slightly)

Even a small boost to your credit score can make a difference. Pay down any outstanding credit card balances, ensure all your bills are paid on time, and dispute any errors on your credit report. For a deeper dive into improving your credit score, check out our guide on .

Every point counts, especially when lenders are evaluating your risk for a $3,000 car loan. Demonstrating recent financial responsibility is key.

Save for a Down Payment

As mentioned, a down payment is a powerful tool. Even $500 or $1,000 on a $3,000 car loan shows a lender your commitment and reduces their risk. It also means you’re financing less, leading to lower monthly payments and less interest over time.

This financial commitment can often sway lenders, especially if your credit history isn’t perfect. It indicates good financial planning on your part.

Consider a Co-signer

If you’re struggling to get approved on your own, a co-signer with good credit can significantly improve your chances. A co-signer essentially guarantees the loan, promising to make payments if you default.

Choose a co-signer wisely, as their credit will also be impacted if you miss payments. Ensure they understand the responsibility and that you both have a clear agreement.

Show Proof of Stability

Lenders favor stability. This includes consistent employment (even if for a short period), a stable residency, and a history of paying bills on time. Providing documentation that proves your stability can reassure lenders.

Long-term employment, even in a modest-paying job, is often viewed more favorably than sporadic employment at higher wages. It signals reliability.

Be Realistic About Vehicle Choice

For a $3,000 car loan, it’s crucial to be realistic about the type of vehicle you can finance. Lenders prefer to finance vehicles that hold their value reasonably well, even if they’re older. Don’t try to get a $3,000 loan for a car that’s only worth $1,000; the loan amount should align with the vehicle’s market value.

Focus on reliable, budget-friendly models known for their longevity and lower maintenance costs. This makes the loan more justifiable to a lender.

Interest Rates and Repayment: What to Expect

Understanding the financial implications of your $3,000 car loan, particularly interest rates and repayment terms, is vital for responsible borrowing. These factors directly impact the total cost of your loan.

Factors Influencing Rates

Several factors determine the interest rate you’ll receive on a $3,000 car loan:

- Credit Score: The higher your score, the lower your interest rate will generally be.

- Loan Term: Shorter loan terms often come with lower interest rates but higher monthly payments.

- Lender: Different lenders have different rate structures and risk appetites.

- Current Market Rates: Broader economic conditions can influence interest rates.

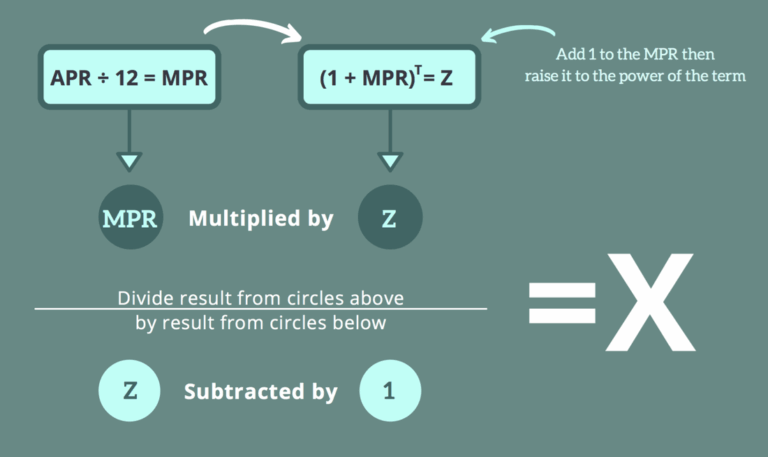

Understanding APR vs. Interest Rate

It’s important to differentiate between the interest rate and the Annual Percentage Rate (APR). The interest rate is simply the cost of borrowing the principal amount. The APR, however, includes the interest rate plus any additional fees or charges associated with the loan, giving you a more accurate picture of the total cost. Always compare APRs when shopping for a loan.

Typical Repayment Periods for Small Loans

For a $3,000 car loan, repayment periods are typically shorter than for larger loans. You might find terms ranging from 12 to 36 months. While a shorter term means higher monthly payments, it also means you pay less interest over the life of the loan.

A longer term, like 48 months, might be offered but is less common for such a small amount. Always consider what you can comfortably afford each month without stretching your budget too thin.

Calculating Monthly Payments

To estimate your monthly payment, you can use online loan calculators. You’ll need the principal loan amount ($3,000), the interest rate (APR), and the loan term in months. For example, a $3,000 loan at 10% APR over 24 months would result in a monthly payment of approximately $138.69. Over 36 months, it would be around $96.81.

Understanding these figures allows you to budget effectively and choose a repayment plan that aligns with your financial capacity.

Common Mistakes to Avoid When Seeking a $3,000 Car Loan

Even experienced borrowers can make missteps, and these can be particularly impactful with smaller loan amounts. Avoiding these common errors will save you time, money, and stress.

- Applying to too many lenders at once: Each hard inquiry on your credit report can slightly lower your score. Shop around, but try to limit full applications to a few well-researched options within a short timeframe (usually 14-45 days, depending on the credit model) to minimize impact.

- Not checking your credit score beforehand: Going into the process blind leaves you at a disadvantage. Know your score so you can target appropriate lenders and anticipate potential challenges.

- Ignoring the car’s condition: A $3,000 car loan means you’re buying an older, used car. Common mistakes to avoid are neglecting a pre-purchase inspection. A seemingly good deal can quickly turn into a financial nightmare with hidden mechanical issues.

- Focusing only on monthly payment, not total cost: While a low monthly payment is appealing, a longer loan term or higher interest rate can mean you pay significantly more over the life of the loan. Always consider the total amount repaid.

- Not reading the fine print: Every loan agreement contains important details about fees, penalties, and terms. Rushing through this can lead to unexpected costs or misunderstandings later on. Read every clause carefully before signing.

- Underestimating the impact of a small down payment: Even for a $3,000 loan, a down payment makes a big difference. Many people mistakenly think it’s not worth the effort for such a small amount, but it can significantly improve approval odds and lower overall costs.

Pro Tips for Smart Car Buying with a Small Loan

Securing a $3,000 car loan is just one part of the equation; buying the right car is equally important. These pro tips will help you make the most of your budget and ensure your purchase is a sound one.

- Get a pre-purchase inspection: This is non-negotiable for any used car, especially one in the $3,000 range. An independent mechanic can identify potential issues that could save you thousands in future repairs. Based on my experience, finding a reliable mechanic for a pre-purchase inspection is paramount for a budget vehicle.

- Negotiate the car price, not just the loan: Your pre-approved loan gives you power. Focus on getting the best possible price for the car first. The lower the car price, the less you need to borrow, which benefits your overall financial picture.

- Factor in insurance and maintenance: Beyond the loan payment, remember to budget for car insurance, registration fees, and potential maintenance costs. Older cars, even reliable ones, will require more frequent upkeep.

- Consider private sellers for better deals on older cars: Dealerships have overheads, which can drive up prices. Private sellers might offer better deals on a $3,000 car, but be extra diligent with inspections and paperwork.

- Look for reliable brands and models: Some car brands and models are known for their longevity and lower maintenance costs. Research these before you start shopping to maximize your chances of getting a dependable vehicle within your budget.

Building Credit with Your 3k Car Loan

One of the significant advantages of a $3,000 car loan, especially for those with limited or poor credit, is its potential to build a strong credit history. This small loan can be a powerful financial tool if managed correctly.

How On-Time Payments Can Boost Your Score

Your payment history is the most crucial factor in your credit score, accounting for 35% of your FICO score. By consistently making your $3,000 car loan payments on time, every time, you demonstrate responsible borrowing behavior. This positive activity is reported to credit bureaus and will gradually improve your credit score.

Even a small loan can have a big impact on your credit profile, establishing a positive track record that will benefit you in future financial endeavors.

The Importance of Consistent Reporting to Credit Bureaus

Ensure that your lender reports your payment activity to all three major credit bureaus (Experian, Equifax, and TransUnion). Most legitimate auto lenders do, but it’s worth confirming, particularly with smaller or non-traditional lenders. Consistent reporting ensures that your diligent payments are recognized across the board, maximizing the credit-building benefits of your $3,000 car loan.

Conclusion

Securing a $3,000 car loan is a perfectly achievable goal that can provide essential transportation and even serve as a valuable tool for building credit. While it requires careful planning and an understanding of lender expectations, the journey to obtaining a small car loan is well within reach for many.

By assessing your financial health, researching lenders, gathering necessary documents, and shopping wisely for a vehicle, you can navigate the process with confidence. Remember to prioritize a pre-purchase inspection, negotiate the car price effectively, and always read the fine print. Your 3k car loan isn’t just about getting a car; it’s about making a smart financial move that can enhance your life and improve your credit profile. With this comprehensive guide, you are now well-equipped to drive your aspirations forward. Share your experiences in the comments below – we’d love to hear them!