Your Keys to the Road: A Comprehensive Guide on How to Get Your First Car Loan

Your Keys to the Road: A Comprehensive Guide on How to Get Your First Car Loan Carloan.Guidemechanic.com

Getting your first car is a monumental step towards independence and freedom. The open road beckons, promising new adventures, easier commutes, and the convenience of personal transportation. However, for many first-time buyers, securing the financing – specifically, a car loan – can seem like a daunting labyrinth. Without an established credit history, the path to approval might appear unclear.

But fear not! This comprehensive guide is designed to demystify the process of getting your first car loan. We’ll walk you through every essential step, from understanding the basics to navigating applications and making smart financial decisions. Our ultimate goal is to equip you with the knowledge and confidence to drive away in your dream car, securing a loan that fits your financial situation and builds a positive credit future. Let’s unlock the secrets to successful auto financing together!

Your Keys to the Road: A Comprehensive Guide on How to Get Your First Car Loan

Section 1: Laying the Foundation – Understanding the Basics of a Car Loan

Before you even begin dreaming about specific car models, it’s crucial to grasp what a car loan entails. Understanding these fundamental concepts will empower you to make informed decisions and approach lenders with confidence. A car loan isn’t just a simple payment; it’s a financial agreement with several moving parts.

What Exactly is a Car Loan?

At its core, a car loan is an agreement where a lender provides you with a sum of money to purchase a vehicle, and you agree to repay that amount, plus interest, over a predetermined period. This period is known as the loan term. The amount you borrow is called the principal. The interest is essentially the cost of borrowing that money.

Your monthly payment is a combination of a portion of the principal and the interest accrued. Over time, as you make these payments, you gradually pay down the loan until the car is entirely yours. It’s a structured way to afford a significant purchase without having to pay the full price upfront.

Why is Getting a First Car Loan Different (and Sometimes Tricky)?

For most first-time car buyers, the biggest hurdle is often a lack of established credit history. Lenders rely heavily on your credit report and score to assess your trustworthiness and ability to repay debt. Without a track record, you’re considered a higher risk, which can lead to higher interest rates or even initial denials.

However, this doesn’t mean it’s impossible. It simply means you’ll need to be more prepared and strategic in your approach. Many lenders have programs specifically designed for first-time buyers, but you’ll need to demonstrate financial stability and responsibility in other ways.

The Importance of Thorough Preparation

Preparation is not just recommended; it’s absolutely essential when seeking your first car loan. Going into the process without understanding your financial standing or what lenders expect can lead to frustration and missed opportunities. Think of it as building the strongest possible case for yourself as a reliable borrower.

By doing your homework upfront, you can identify potential issues, strengthen your application, and ultimately secure more favorable loan terms. This proactive approach saves you time, money, and unnecessary stress in the long run.

Section 2: Building Your Loan-Readiness – Essential Pre-Approval Steps

The key to a successful first car loan application lies in meticulous preparation. This stage is all about understanding your financial health and taking steps to present yourself as an attractive borrower. Skipping these crucial steps can significantly hinder your chances of approval or result in less favorable loan terms.

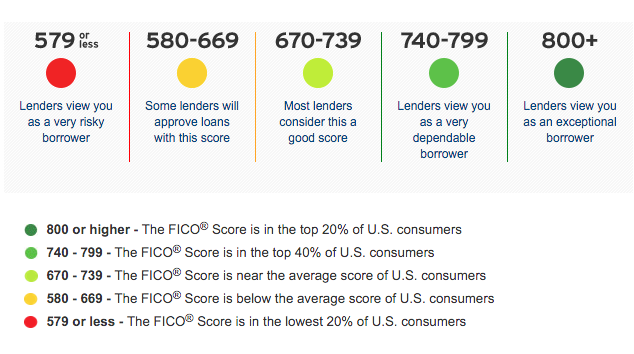

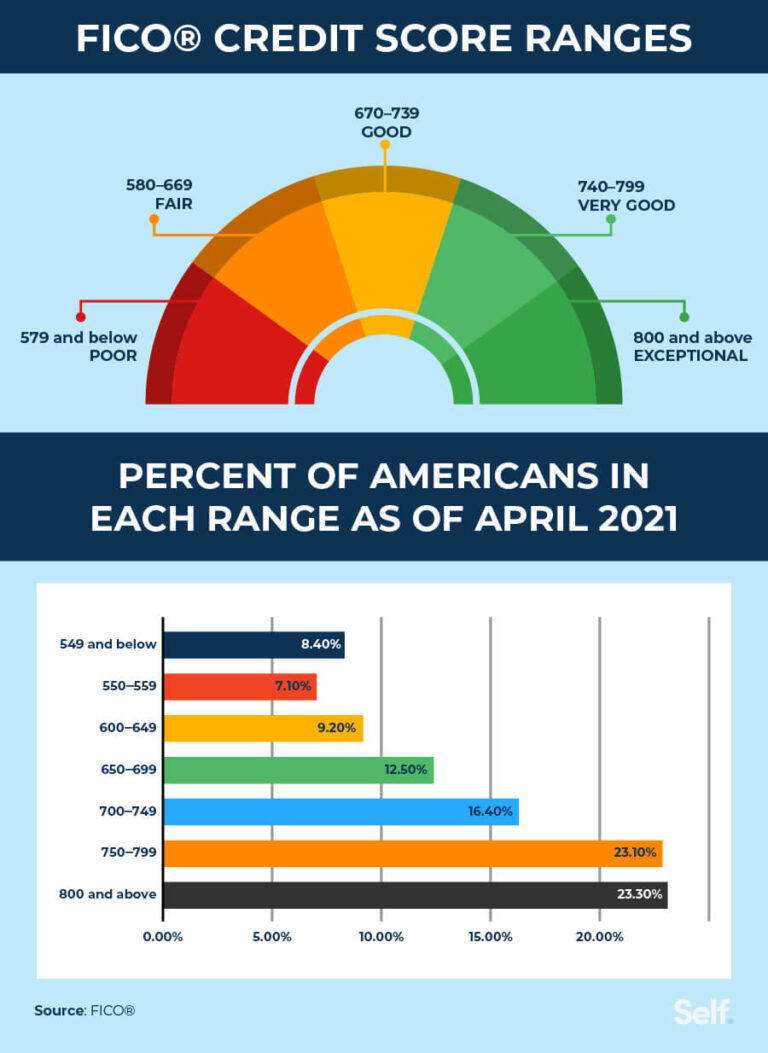

Understanding and Building Your Credit Score & History

Your credit score is a three-digit number that summarizes your creditworthiness, while your credit history details your past borrowing and repayment behavior. For first-time borrowers, establishing this history is paramount. Lenders use this information to gauge the risk associated with lending you money. A good score signals reliability.

If you’re starting from scratch, there are several ways to build credit. Consider opening a secured credit card, where you deposit money as collateral, or becoming an authorized user on a trusted family member’s credit card. Both methods, when managed responsibly with on-time payments, can quickly establish a positive credit footprint.

Based on my experience, many first-time buyers underestimate the power of even a few months of responsible credit use. Start early, even if you’re not planning to buy a car immediately. Regularly check your credit report from all three major bureaus (Equifax, Experian, TransUnion) via annualcreditreport.com. This allows you to identify any errors and understand your current standing.

Budgeting for Affordability and the Power of a Down Payment

Before you even look at cars, create a realistic budget. A car’s cost isn’t just the monthly loan payment; it includes insurance, fuel, maintenance, and potential repair costs. Ensure your total car-related expenses don’t strain your overall financial health. Lenders want to see that you can comfortably afford the loan and the associated costs.

A substantial down payment is one of the most effective ways to improve your chances of approval and secure a better interest rate. Putting money down reduces the amount you need to borrow (the principal), which in turn lowers your monthly payments and the total interest paid over the life of the loan. It also signals to lenders that you’re financially committed and serious about the purchase.

Pro tips from us: Aim for at least 10-20% of the car’s purchase price as a down payment. This not only makes your loan more attractive but also helps prevent you from being "upside down" on your loan (owing more than the car is worth) early on. Start saving aggressively for this upfront cost as soon as you consider buying a car.

Your Debt-to-Income Ratio (DTI): A Lender’s Key Metric

Your Debt-to-Income (DTI) ratio is a critical metric lenders use to assess your ability to manage monthly payments and take on new debt. It’s calculated by dividing your total monthly debt payments (credit cards, student loans, rent, etc.) by your gross monthly income (before taxes and deductions). A lower DTI indicates less financial strain and a greater capacity to handle a new car loan.

Lenders typically prefer a DTI ratio of 36% or less, though some might go higher depending on other factors. To calculate yours, sum up all your fixed monthly debt obligations and divide by your gross monthly income. For example, if your total monthly debt is $1,000 and your gross income is $3,000, your DTI is 33.3%.

If your DTI is high, consider paying down existing debts or increasing your income before applying for a car loan. This demonstrates financial prudence and significantly improves your loan application. It’s about showing lenders you have ample room in your budget for this new responsibility.

Proof of Income and Stability: What Lenders Look For

Lenders need assurance that you have a stable source of income to repay the loan. This means providing documentation that verifies your employment and earnings. They look for consistency and reliability in your financial situation. The longer you’ve been at your current job, the better.

Typically, you’ll need to provide recent pay stubs (usually the last two or three months), W-2 forms from previous years, and potentially tax returns if you’re self-employed. Bank statements can also be requested to show consistent deposits and account activity. Having these documents organized and ready will streamline your application process significantly.

Demonstrating stability goes beyond just income; it also includes your residence history. Lenders prefer applicants who have lived at their current address for an extended period, as it suggests a stable lifestyle. Be prepared to provide proof of residence, such as utility bills or lease agreements.

Section 3: Navigating the Loan Application Process

With your financial house in order, you’re now ready to engage with lenders. This stage involves understanding where to apply, what questions to ask, and how to evaluate different loan offers to find the best fit for your needs. This is where your preparation truly pays off.

Getting Pre-Approved: Your Secret Weapon

One of the most powerful steps you can take is getting pre-approved for a car loan before you even set foot in a dealership. Pre-approval means a lender has conditionally agreed to lend you a specific amount of money at a certain interest rate, based on a preliminary review of your credit and finances. This isn’t a final loan, but a strong indication of what you qualify for.

Why is it so crucial? Pre-approval gives you immense bargaining power at the dealership. You walk in knowing your budget ceiling and your likely interest rate, allowing you to focus solely on negotiating the car’s price. It transforms you from a buyer who needs financing to a buyer who has financing, putting you in a stronger position.

Pro tips from us: Apply for pre-approval with several different types of lenders: your own bank, local credit unions, and reputable online auto lenders. Credit unions often offer very competitive rates, especially for first-time buyers. Submitting multiple applications within a short window (typically 14-45 days, depending on the credit bureau) will count as a single inquiry on your credit report, minimizing the impact.

Understanding and Comparing Loan Offers

Once you receive pre-approval offers, it’s time to meticulously compare them. Don’t just look at the monthly payment; delve into the details of each offer. The key components to scrutinize are:

- Interest Rate (APR): The Annual Percentage Rate (APR) is the true cost of borrowing, encompassing the interest rate and certain fees. A lower APR means less money paid over the life of the loan.

- Loan Term: This is the length of time you have to repay the loan, typically 36, 48, 60, or 72 months. A shorter term means higher monthly payments but less total interest paid. A longer term means lower monthly payments but significantly more interest paid over time.

- Fees: Look for any origination fees, application fees, or prepayment penalties. Some lenders might charge extra for these.

Carefully read the fine print of each offer. Understand the total cost of the loan, not just the monthly payment. A longer loan term might make monthly payments seem more affordable, but it often leads to paying thousands more in interest. Use an online car loan calculator to see how different interest rates and terms impact your total cost.

Choosing the Right Car: Aligning with Your Budget and Loan

With pre-approval in hand, you now have a clear maximum budget. This is the time to choose a car that aligns not only with your needs but also with your financial realities. Resist the temptation to stretch your budget just because you’ve been approved for a higher amount.

For first-time buyers, a reliable used car can often be a more financially prudent choice than a brand-new one. New cars depreciate rapidly, meaning their value drops significantly the moment they’re driven off the lot. A used car allows you to get more car for your money and often comes with lower insurance premiums.

Make sure the car you choose falls comfortably within your pre-approved loan amount and your overall budget, including all associated costs. Don’t forget to factor in insurance quotes for specific models, as these can vary widely and significantly impact your monthly expenses.

Section 4: Common Pitfalls and How to Avoid Them

Even with thorough preparation, the car buying and loan process can present traps for the unwary. Being aware of these common mistakes will help you navigate the journey smoothly and protect your financial well-being. Avoiding these missteps is just as important as taking the right steps.

Common mistakes to avoid are:

- No Down Payment: While some lenders offer "no money down" loans, especially for first-time buyers, these often come with higher interest rates and put you at risk of negative equity. Always aim to make a down payment, even a small one, to show commitment and reduce your overall loan burden.

- Applying to Too Many Lenders at Once (Without Strategy): Each hard inquiry on your credit report can slightly lower your score. While applying to multiple auto lenders within a short "shopping window" (e.g., 14-45 days) generally counts as one inquiry for FICO scores, spreading applications out over months or applying for different types of credit can negatively impact your score. Be strategic with your applications.

- Buying More Car Than You Can Afford: It’s easy to get caught up in the excitement and fall in love with a car outside your budget. Stick to your pre-approved amount and your personal budget. Remember, the monthly payment is just one piece of the puzzle; insurance, maintenance, and fuel add up. Overextending yourself can lead to financial stress down the line.

- Not Reading the Fine Print: Never sign a loan agreement without thoroughly reading and understanding every clause. Pay attention to interest rates, loan terms, fees, and any optional add-ons (like extended warranties or GAP insurance) that might be rolled into the loan. If you don’t understand something, ask for clarification.

- Skipping Pre-Approval: As discussed, pre-approval is your superpower. Going to the dealership without it puts you at a disadvantage. You lose bargaining power, and you might be pressured into dealership financing that isn’t the best deal for you. Always secure your financing first.

- Focusing Only on Monthly Payments: Dealerships often try to sell you on a "low monthly payment." While appealing, this can sometimes be achieved by extending the loan term significantly, leading to you paying much more in interest over the life of the loan. Always ask for the total cost of the car and the loan.

- Ignoring Your Credit Report for Errors: Mistakes on your credit report can significantly hurt your chances of approval or lead to higher interest rates. Always review your reports annually and dispute any inaccuracies immediately. This proactive step can save you a lot of headaches.

Section 5: After Approval – Maintaining Good Standing and Financial Health

Congratulations, you’ve secured your first car loan and driven off in your new vehicle! The journey doesn’t end here, however. This next phase is crucial for building a strong financial future and ensuring your car ownership experience remains positive. Responsible management of your loan can unlock future financial opportunities.

Making Payments On Time, Every Time

This is perhaps the most critical aspect of managing any loan, especially your first one. Every on-time payment you make is a positive entry on your credit report, steadily building your credit score and history. This demonstrates to future lenders that you are a reliable and trustworthy borrower.

Set up automatic payments from your bank account to avoid missing deadlines. If you anticipate any difficulty in making a payment, contact your lender immediately. Most lenders are willing to work with you to find a solution if you communicate proactively, rather than letting a payment default. Consistency is key to a healthy credit profile.

Building Your Credit Further for Future Opportunities

Your first car loan is an excellent tool for establishing and building a robust credit history. As you make consistent, on-time payments, your credit score will gradually improve. This improved score will be invaluable for future financial endeavors, such as securing a mortgage, personal loans, or even better rates on future car loans.

Beyond your car loan, continue to practice responsible credit habits. Keep your credit card balances low, pay all bills on time, and avoid opening too many new credit accounts simultaneously. Diversifying your credit (e.g., a car loan, a credit card) and managing it well shows lenders you can handle various types of debt responsibly. .

Exploring Refinancing Options Later On

As your credit score improves and interest rates fluctuate, you might have the opportunity to refinance your car loan down the line. Refinancing involves taking out a new loan, often with a lower interest rate or different terms, to pay off your existing car loan. This can lead to lower monthly payments or a reduced total cost of the loan.

Typically, you’d consider refinancing after you’ve made 6-12 months of on-time payments, significantly improving your credit profile. Keep an eye on current interest rates and compare them to your original loan. Websites like Bankrate or NerdWallet often provide tools to help you assess if refinancing is a good option for you. .

Conclusion: Your Road to Financial Independence Begins Here

Securing your first car loan is more than just getting a set of keys; it’s a significant milestone on your journey towards financial independence and building a solid credit foundation. While the process might seem complex at first, armed with the knowledge and strategies outlined in this guide, you are well-equipped to navigate it successfully.

Remember, preparation is your most valuable asset. Understand your credit, build a strong financial profile, save for a down payment, and approach lenders with confidence. By taking the time to research, compare offers, and avoid common pitfalls, you can secure a loan that not only puts you behind the wheel but also sets you up for a future of responsible borrowing and financial growth.

We hope this comprehensive guide has provided you with clarity and confidence. The open road awaits, and with smart financial decisions, you’re ready to embark on your next great adventure. What are your biggest takeaways from this guide, or do you have any specific questions about getting your first car loan? Share your thoughts in the comments below!