Your Roadmap to Getting Approved for a $30,000 Car Loan: An Expert’s Guide

Your Roadmap to Getting Approved for a $30,000 Car Loan: An Expert’s Guide Carloan.Guidemechanic.com

Securing a car loan, especially for a significant amount like $30,000, can feel like navigating a complex maze. The thought of owning that dream car, whether it’s a reliable family SUV or a stylish sedan, often comes with the hurdle of financing. But what if we told you that with the right preparation and knowledge, getting approved for a $30,000 car loan is not just a dream, but an achievable reality?

As an expert blogger and professional SEO content writer, I’ve delved deep into the world of auto financing, and I’m here to share a super comprehensive guide that will illuminate your path. This article is designed to be your ultimate resource, providing you with actionable insights and proven strategies to significantly increase your chances of approval. We’ll cover everything from boosting your credit score to understanding the nuances of the application process. Let’s embark on this journey together and transform your car ownership aspirations into a concrete plan.

Your Roadmap to Getting Approved for a $30,000 Car Loan: An Expert’s Guide

Understanding the Landscape of a $30,000 Car Loan

A $30,000 car loan represents a significant financial commitment. Lenders, whether they are traditional banks, credit unions, or dealership finance departments, approach such applications with a keen eye on your financial stability and perceived risk. They’re not just looking at a single number; they’re evaluating a holistic picture of your financial health.

This isn’t merely about affording the monthly payment; it’s about demonstrating reliability and consistency. Think of it as presenting your financial resume. The more robust and consistent your financial history, the more confident lenders will be in approving your application for a substantial amount like $30,000. It’s crucial to understand their perspective before you even begin the application process.

Why $30,000 is a Key Benchmark

For many car buyers, $30,000 sits comfortably in the sweet spot for a new mid-range vehicle or a high-quality used luxury car. It’s a common price point that balances aspiration with affordability for a large segment of the population. This makes getting approved for a $30,000 car loan a frequent goal for many looking to upgrade their ride or make a significant vehicle purchase.

From a lender’s standpoint, a $30,000 loan is substantial enough to warrant thorough scrutiny but typically falls within their standard lending parameters for well-qualified applicants. Understanding this benchmark helps you tailor your preparation to meet these specific financial expectations. It’s not a small personal loan, nor is it a multi-million dollar mortgage; it requires a specific type of financial readiness.

What Lenders Are Truly Looking For

Lenders are primarily concerned with one thing: your ability and willingness to repay the loan. This ability is assessed through several key indicators, often referred to as the "5 Cs of Credit": Character, Capacity, Capital, Collateral, and Conditions. While we’ll delve into each of these in detail, a general overview is essential.

They want to see a history of responsible borrowing, a stable income that can comfortably cover the payments, some personal investment (like a down payment), the value of the car itself, and how current economic conditions might affect your repayment. Based on my experience in analyzing countless loan applications, these foundational elements are non-negotiable for approval. Ignoring any one of them can significantly hinder your chances, especially for a $30,000 car loan.

The Cornerstone: Your Credit Score

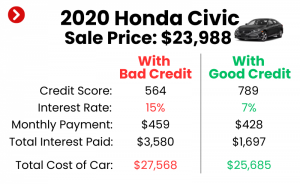

Your credit score is arguably the single most important factor when applying for any loan, and a $30,000 car loan is no exception. It’s a three-digit number that summarizes your entire credit history, telling lenders how risky it might be to lend you money. A higher score signifies a lower risk, making lenders more eager to offer you favorable terms.

Think of your credit score as your financial GPA. Just as a good GPA opens doors to better universities, a strong credit score unlocks access to more competitive loan rates and easier approval processes. This directly impacts not only your approval chances but also the total cost of your loan over its lifetime.

What’s a Good Score for a $30,000 Loan?

While there’s no single magic number, generally, a FICO score of 660 and above is considered good and opens the door to prime lending rates. For a $30,000 car loan, aiming for a score in the 700s or higher will put you in an excellent position to receive the best interest rates and terms. Lenders categorize scores into tiers:

- Excellent: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

If your score falls into the "Fair" category, approval for $30,000 might still be possible, but you’ll likely face higher interest rates and potentially stricter conditions. For those with "Poor" credit, securing a loan of this size becomes significantly challenging without a substantial down payment or a co-signer.

How to Check Your Credit Score and Report

Before you even think about applying, know where you stand. You can get a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months through AnnualCreditReport.com. This is a crucial step.

Review your reports meticulously for any errors or inaccuracies, as these can negatively impact your score. Many credit card companies and banks also offer free credit score monitoring services. Pro tips from us: utilize these tools regularly to keep tabs on your credit health and identify areas for improvement.

Tips to Improve Your Credit Score

Improving your credit score takes time and consistent effort, but the rewards are substantial.

- Pay Your Bills on Time, Every Time: Payment history accounts for 35% of your FICO score. Late payments are a major red flag for lenders. Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce Your Credit Utilization Ratio: This is the amount of credit you’re using compared to your total available credit. Keep this ratio below 30% – ideally even lower, around 10% – to signal responsible credit management. If you have a credit card with a $10,000 limit, try to keep your balance below $3,000.

- Limit New Credit Applications: Each time you apply for new credit, a "hard inquiry" appears on your report, which can temporarily ding your score. Space out your applications and only apply for credit when absolutely necessary.

- Dispute Errors: If you find any inaccuracies on your credit report, dispute them immediately with the credit bureau. Correcting these errors can often lead to a quick bump in your score.

- Don’t Close Old Accounts: The length of your credit history (15% of your score) benefits from older, established accounts. Even if you don’t use a credit card often, keeping it open and active (even with a small purchase now and then) can help your score.

Financial Health Beyond Credit: Income & Debt-to-Income Ratio (DTI)

While your credit score tells lenders about your past financial behavior, your income and debt-to-income (DTI) ratio reveal your current capacity to take on new debt. Even with a stellar credit score, if your income isn’t sufficient to comfortably cover an additional $30,000 car loan payment, lenders will hesitate.

This is where the concept of "affordability" truly comes into play. Lenders want assurance that you won’t be stretched too thin financially, which could lead to missed payments down the road. They look at your income stability and how much of that income is already committed to other debts.

Why Stable Income is Crucial

Lenders prefer to see a consistent, verifiable income stream. This means W-2 employees with a steady paycheck often have an easier time. If you’re self-employed, be prepared to provide more extensive documentation, such as tax returns for the past two years, to prove your income stability.

The higher and more stable your income, the more comfortable lenders will be with a $30,000 loan. They want to ensure that after all your existing obligations, you still have ample disposable income to handle the new car payment without financial strain. This consistency is a major factor in their risk assessment.

What DTI Is and Why It Matters

Your Debt-to-Income (DTI) ratio is a critical metric lenders use to assess your repayment capacity. It’s the percentage of your gross monthly income that goes towards paying your monthly debt obligations. A lower DTI indicates that you have more income available to cover new debt payments, making you a less risky borrower.

Lenders typically prefer a DTI of 36% or lower, though some may go up to 43% for well-qualified applicants. For a significant loan like $30,000, aiming for a DTI well below 36% is highly recommended. Common mistakes to avoid are underestimating your total monthly debt payments or overestimating your gross income. Be realistic and thorough in your calculations.

How to Calculate Your DTI

Calculating your DTI is straightforward:

- Calculate your total monthly debt payments: This includes rent/mortgage, minimum credit card payments, student loan payments, personal loan payments, and any other recurring debt.

- Calculate your gross monthly income: This is your income before taxes and deductions.

- Divide your total monthly debt payments by your gross monthly income.

- Multiply by 100 to get the percentage.

Example: If your gross monthly income is $5,000, and your total monthly debt payments (including your estimated car payment) are $1,500, your DTI would be ($1,500 / $5,000) * 100 = 30%. This would generally be considered a good DTI.

Strategies to Improve Your DTI

If your DTI is higher than desired, there are steps you can take to improve it:

- Pay Down Existing Debts: Prioritize paying off high-interest debts like credit card balances. Even small reductions can make a difference.

- Increase Your Income: If possible, consider side hustles, overtime, or negotiating a raise. More income directly lowers your DTI.

- Avoid Taking on New Debt: Before applying for the car loan, refrain from opening new credit cards or taking out personal loans, as this will only increase your debt obligations.

- Consolidate High-Interest Debts: This can sometimes lower your overall monthly payments, freeing up more of your income.

The Power of a Down Payment

A down payment is your initial contribution to the purchase price of the car. It’s a powerful tool that can significantly strengthen your application for a $30,000 car loan, even if other aspects of your financial profile aren’t perfect. Lenders view a substantial down payment very favorably.

It shows them you have skin in the game, reducing their risk. It also immediately reduces the loan amount you need, making the financing more manageable for both you and the lender. Think of it as a statement of your commitment and financial stability.

Benefits of a Larger Down Payment

- Lower Loan Amount: The more you put down, the less you need to borrow, which means lower monthly payments and less interest paid over the life of the loan.

- Reduced Risk for Lender: A larger down payment means the car’s value is less likely to be "underwater" (where you owe more than the car is worth) early in the loan term. This reduces the lender’s exposure if you default.

- Better Interest Rates: Lenders often offer more attractive interest rates to borrowers who make significant down payments because they are seen as lower risk.

- Easier Approval: For applicants with less-than-perfect credit, a substantial down payment can be the key to getting approved for a $30,000 car loan. It offsets some of the perceived risk associated with their credit history.

How Much Is Ideal for a $30,000 Loan?

While any down payment is better than none, a general rule of thumb for car loans is to aim for 10-20% of the vehicle’s purchase price. For a $30,000 car, this would mean a down payment of $3,000 to $6,000. If you can afford more, even better.

For new cars, 20% is often recommended to help mitigate depreciation, which is steepest in the first year. For used cars, 10% is a common benchmark. Based on my experience, a strong down payment can often sway a lender’s decision from a "maybe" to a "yes," especially when you’re seeking a substantial loan amount.

Sources for a Down Payment

- Savings: The most straightforward source. Start saving early and consistently.

- Trade-in Value: If you have an existing vehicle, its trade-in value can serve as all or part of your down payment. Get an appraisal from multiple dealerships or online platforms to ensure you’re getting a fair price.

- Selling Your Current Car Privately: Often, selling your car yourself can yield a higher return than a trade-in, providing more cash for your down payment.

- Tax Refund: If timed correctly, a tax refund can provide a lump sum for your down payment.

Getting Your Documents in Order (The Pre-Application Checklist)

Organization is key when applying for a loan. Having all your necessary documents ready and easily accessible will streamline the application process and present you as a prepared and serious borrower. This pre-application checklist is your essential guide to ensuring a smooth experience.

Lenders need to verify the information you provide, and having these documents readily available demonstrates your preparedness. It minimizes back-and-forth communication, which can delay your approval. Pro tips from us: create a dedicated folder, either physical or digital, for all your loan documents.

Essential Documents You’ll Need

- Proof of Income:

- W-2 Employees: Recent pay stubs (typically the last 2-3 months) showing year-to-date earnings.

- Self-Employed: Two years of tax returns (IRS Form 1040), profit and loss statements, and bank statements.

- Proof of Residence: Utility bills (electricity, water, gas), a lease agreement, or mortgage statements with your current address.

- Identification: A valid government-issued photo ID, such as a driver’s license or passport.

- Social Security Number: For credit checks.

- Insurance Details: While you might not have the policy yet, be prepared to provide proof of insurance before driving off with the car. Some lenders may require a binder of insurance coverage prior to final approval.

- Trade-in Title (if applicable): If you’re trading in a vehicle, you’ll need its title or registration.

Based on my experience, delays often occur because applicants don’t have all their income documentation or proof of residence immediately on hand. Gathering these proactively will significantly speed up your application for a $30,000 car loan.

The Strategic Advantage: Pre-Approval

Getting pre-approved for a car loan is one of the smartest moves you can make before stepping foot into a dealership. It’s a preliminary commitment from a lender to give you a loan up to a certain amount, with specific terms, before you’ve even chosen a car. This process provides clarity and puts you in a much stronger negotiating position.

Pre-approval transforms you from a casual browser into a cash buyer, giving you significant leverage. It separates the financing aspect from the car-buying aspect, allowing you to focus on getting the best deal on the vehicle itself.

What is Pre-Approval?

Pre-approval means a lender has reviewed your credit, income, and DTI, and has determined you qualify for a loan up to a specific amount, at an estimated interest rate. This involves a "hard inquiry" on your credit report, so it’s important to apply for pre-approval within a short window (typically 14-45 days) to minimize the impact on your credit score if you apply with multiple lenders.

This isn’t a final approval, as it still depends on the specific vehicle and its condition, but it’s a solid offer you can take to the dealership. It empowers you by knowing your budget and what interest rate to expect.

Benefits of Pre-Approval

- Know Your Budget: You’ll know exactly how much you can afford, preventing you from falling in love with a car outside your price range.

- Shop with Confidence: You’ll walk into the dealership with your own financing in hand, allowing you to negotiate the car price more effectively. The dealership knows you’re a serious buyer.

- Better Negotiation Power: With a pre-approval in hand, you can compare the dealer’s financing offer against your pre-approved rate. This encourages dealers to compete for your business, potentially leading to a better deal.

- Faster Purchase Process: Since much of the paperwork is already done, the actual car purchase can be much quicker.

- Focus on the Car, Not the Loan: You can concentrate on finding the right vehicle that meets your needs and budget, rather than stressing about whether you’ll get approved for the loan.

How to Get Pre-Approved

- Banks and Credit Unions: Start with your current bank or credit union. They often offer competitive rates to existing members.

- Online Lenders: Numerous online lenders specialize in auto loans and can provide quick pre-approvals. Websites like Capital One Auto Finance, LightStream, and Carvana offer this service.

- Apply to Multiple Lenders: Apply to 2-3 different lenders within a short timeframe (14-45 days) to compare offers. FICO models treat multiple inquiries for the same type of loan within this window as a single inquiry, minimizing the impact on your score. Pro tips from us: comparing offers is crucial, as even a small difference in APR can save you hundreds or thousands over the life of a $30,000 loan.

Navigating the Application Process & Lender Options

Once you’ve done your homework, gathered your documents, and ideally secured a pre-approval, it’s time for the actual application. This stage involves making informed decisions about where to finance and understanding the terms presented to you. This is where your preparedness truly pays off.

Don’t rush this part. Take your time to compare offers, understand the fine print, and ensure you’re getting the best possible deal for your $30,000 car loan. This diligence can save you a significant amount of money in the long run.

Dealership Financing vs. Banks/Credit Unions

You generally have two main avenues for financing your car:

- Dealership Financing: Dealerships act as intermediaries, working with a network of lenders (banks, credit unions, and captive finance companies like Toyota Financial Services). They can offer convenience and sometimes special promotions. However, their primary goal is to sell you a car, and their financing options might not always be the most competitive. Common mistakes to avoid: focusing solely on the monthly payment without understanding the total cost, interest rate, and loan term.

- Banks and Credit Unions: These are direct lenders. As discussed with pre-approval, they often offer competitive rates, especially to existing customers. Credit unions, in particular, are known for their customer-centric approach and often provide excellent terms.

By securing a pre-approval from a bank or credit union before visiting the dealership, you have a benchmark to compare against. If the dealer can beat your pre-approved rate, great! If not, you have a solid offer to fall back on.

Comparing Loan Offers (APR, Term, Fees)

Don’t just look at the monthly payment. Here’s what to scrutinize:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and any fees. Always compare APRs, not just interest rates, as it gives you the most accurate picture of the loan’s expense. A lower APR means less money paid over time.

- Loan Term: This is the length of the loan (e.g., 36, 48, 60, 72 months). A shorter term means higher monthly payments but less interest paid overall. A longer term means lower monthly payments but significantly more interest paid. For a $30,000 loan, balance affordability with total cost.

- Fees: Look out for origination fees, documentation fees, prepayment penalties, or other hidden costs.

- Total Cost of Loan: Calculate the total amount you’ll pay by multiplying your monthly payment by the number of months in the loan term. This provides the clearest picture of the loan’s true expense.

The Role of a Co-Signer

If your credit score or income isn’t strong enough to secure a $30,000 car loan on your own, a co-signer might be an option. A co-signer is someone with good credit who agrees to be equally responsible for the loan if you default.

- Pros: Can help you get approved or secure a better interest rate.

- Cons: The co-signer is legally obligated to repay the loan if you can’t, and their credit will be affected if you miss payments. It can strain relationships if things go wrong. Use this option judiciously and only with full transparency and understanding from both parties.

Special Considerations & Overcoming Challenges

Even with all the preparation, unique situations can arise. Perhaps your credit isn’t stellar, or you’re a first-time buyer with no credit history. It’s important to address these specific challenges and understand that options still exist to help you get approved for a $30,000 car loan.

This section provides strategies for those who face additional hurdles, ensuring that everyone has a pathway to their desired vehicle. Remember, persistence and creativity are your allies here.

What if You Have Bad Credit?

While challenging, securing a $30,000 car loan with bad credit is not impossible, though it will require more effort and likely come with less favorable terms.

- Larger Down Payment: This is your most powerful tool. A substantial down payment reduces the loan amount and the lender’s risk, making them more willing to approve you.

- Co-Signer: As discussed, a co-signer with excellent credit can significantly improve your chances.

- Subprime Lenders: These lenders specialize in working with borrowers with lower credit scores. Be prepared for higher interest rates, as they take on more risk. Research them thoroughly to ensure they are reputable.

- Secured Loan: Some lenders might offer a secured loan, where the car itself acts as collateral.

- Improve Your Credit First: If possible, take some time to improve your credit score before applying. Even a few months of diligent effort can make a difference.

First-Time Car Buyers

If you have little to no credit history, getting approved for a $30,000 loan can be tricky. Lenders have no data to assess your repayment behavior.

- Start Small: Consider building credit with a smaller loan or a secured credit card first.

- Co-Signer: A parent or trusted individual with good credit can co-sign the loan.

- Establish a Banking Relationship: Your bank or credit union might be more willing to lend to you if you have a long-standing relationship and a history of responsible banking.

- Demonstrate Stability: Show consistent employment history and a stable residence.

The Importance of Budgeting for Total Car Ownership Costs

Getting approved for a $30,000 car loan is just one part of the equation. Many applicants overlook the total cost of car ownership beyond the monthly payment. Based on my experience, this oversight is a common mistake that leads to financial strain down the road.

Remember to factor in:

- Car Insurance: Especially for a $30,000 vehicle, insurance premiums can be significant. Get quotes before you buy.

- Maintenance and Repairs: All cars need maintenance. Factor in oil changes, tire rotations, and potential repairs.

- Fuel Costs: Consider the car’s fuel efficiency and your typical driving habits.

- Registration and Taxes: These vary by state but are recurring costs.

Our article on Ultimate Car Budgeting: Beyond the Monthly Payment provides valuable insights into planning for these ongoing expenses.

Your Journey to $30,000 Car Loan Approval Starts Now!

Getting approved for a $30,000 car loan might seem like a daunting task, but with a strategic approach and thorough preparation, it’s well within your reach. We’ve covered the critical elements: understanding what lenders look for, optimizing your credit score, improving your debt-to-income ratio, leveraging a strong down payment, and streamlining your application with pre-approval.

Remember, knowledge is power in the world of auto financing. By following the advice outlined in this comprehensive guide, you’re not just applying for a loan; you’re presenting yourself as a financially responsible and reliable borrower. Your proactive efforts in preparing your financial profile will not only increase your approval chances but also help you secure the most favorable terms for your $30,000 car loan.

Don’t wait until the last minute. Start today by checking your credit report, assessing your financial health, and planning your strategy. Your dream car is closer than you think. Happy driving!