Your Trusted Guide to Finding a Loan to Fix Your Car: Navigating Unexpected Repairs with Confidence

Your Trusted Guide to Finding a Loan to Fix Your Car: Navigating Unexpected Repairs with Confidence Carloan.Guidemechanic.com

The sudden thud, the ominous check engine light, or the grinding sound from under the hood – these are the unwelcome harbingers of unexpected car repairs. For many, a malfunctioning vehicle isn’t just an inconvenience; it’s a significant disruption to daily life, impacting commutes, work, and family responsibilities. When your car breaks down, the immediate question isn’t just what’s wrong, but how will I pay for it?

This is where understanding your options for a loan to fix my car becomes crucial. Facing an urgent repair without adequate savings can feel overwhelming, but thankfully, there are various financing solutions available. This comprehensive guide will meticulously explore every avenue, helping you make an informed decision to get back on the road safely and without undue financial stress. We’ll delve into the nuances of different loan types, offer practical advice, and share expert insights to empower you through this challenging time.

Your Trusted Guide to Finding a Loan to Fix Your Car: Navigating Unexpected Repairs with Confidence

The Unexpected Reality: Why Car Repairs Hit Hard

Cars, despite their reliability, are complex machines prone to wear and tear. From transmission failures and engine issues to brake replacements and electrical problems, repairs can range from a few hundred to several thousand dollars. These costs often arrive without warning, putting immense pressure on personal finances.

Many households operate on tight budgets, making it difficult to absorb a large, unforeseen expense. When a car is essential for work or daily errands, delaying repairs isn’t an option. This urgency often pushes individuals to seek immediate financial solutions, highlighting the critical need for accessible and understandable financing options.

Understanding Your Options: A Deep Dive into Loans to Fix Your Car

When you need a loan to fix my car, you’re looking for solutions that balance speed, affordability, and suitability for your financial situation. It’s not a one-size-fits-all scenario; what works best for one person might not be ideal for another. Let’s break down the most common and effective financing methods available.

1. Personal Loans: A Flexible Solution for Car Repairs

Personal loans are often a go-to option for unexpected expenses like car repairs. These are typically unsecured loans, meaning you don’t need to put up collateral like your car or home to qualify. Instead, lenders assess your creditworthiness, income, and debt-to-income ratio to determine your eligibility and interest rate.

The flexibility of personal loans is a major advantage. Once approved, the funds are usually deposited directly into your bank account, giving you the freedom to pay any mechanic or repair shop. Repayment terms are fixed, with regular monthly payments over a set period, making budgeting predictable.

Based on my experience in financial advising, individuals with good to excellent credit scores generally qualify for the most favorable interest rates on personal loans. This can make them a very cost-effective way to finance significant car repairs. However, if your credit score is less than ideal, you might face higher interest rates, which could increase the overall cost of the loan. It’s always wise to check your credit score before applying to understand your potential options.

2. Secured Car Repair Loans (Including Title Loans): When Collateral is an Option

Secured loans differ from personal loans because they require collateral. In the context of car repairs, the most common type of secured loan involving your vehicle is a title loan. With a car title loan, you use your car’s title as collateral, meaning the lender can repossess your vehicle if you fail to repay the loan.

The primary appeal of title loans is their accessibility, particularly for those with poor credit or limited income. Approval can be quick, and the funds are often available on the same day. However, this convenience comes at a significant cost. Title loans are notorious for extremely high annual percentage rates (APRs), often in the triple digits, and short repayment terms.

Common mistakes to avoid with title loans include underestimating the repayment burden and the very real risk of losing your vehicle. While they offer immediate cash, the long-term financial implications can be devastating. We strongly advise exploring all other options before considering a title loan due to their predatory nature and high risk.

3. Utilizing Credit Cards: Quick Access, but Beware the Interest

For smaller repairs or when you have an emergency credit card available, using plastic can be a quick and easy solution. If you have an existing credit card with available credit, you can pay for the repairs immediately. Some cards also offer rewards points or cashback, which can be a small bonus.

A particularly attractive option for car repairs is a 0% APR promotional credit card. Many credit card companies offer introductory periods where you pay no interest on purchases for 12, 18, or even 21 months. If you can pay off the entire repair cost within this promotional window, it’s essentially an interest-free loan.

Pro tips from us: If you opt for a 0% APR card, create a strict repayment plan to ensure the balance is paid off before the promotional period ends. Otherwise, you’ll be hit with deferred interest, which can be substantial. Also, be mindful of your credit utilization ratio; using a significant portion of your available credit can negatively impact your credit score.

4. Dealership Financing & Repair Shop Payment Plans: Convenience at the Source

Many car dealerships and independent repair shops understand the financial strain of unexpected repairs. As a result, they often offer their own financing options or payment plans. These can range from in-house payment schedules to partnerships with third-party lenders specializing in auto repair financing.

The main advantage here is convenience. You can often arrange financing directly at the repair shop, streamlining the process. Some plans might offer deferred interest or interest-free periods if paid within a certain timeframe, similar to promotional credit cards.

From our experience assisting clients, it’s crucial to thoroughly compare these offers with other loan types. While convenient, the interest rates or fees associated with repair shop financing might sometimes be higher than what you could secure with a personal loan from a bank or credit union. Always ask for a detailed breakdown of all costs, including interest, fees, and the total amount you’ll repay.

5. Home Equity Loans/Lines of Credit (HELOC): Leveraging Your Home’s Value

If you’re a homeowner with significant equity, a home equity loan or a Home Equity Line of Credit (HELOC) could be an option for large, unexpected car repairs. These are secured loans, using your home as collateral, which typically translates to lower interest rates compared to unsecured personal loans.

A home equity loan provides a lump sum, while a HELOC offers a revolving credit line you can draw from as needed. Both can offer competitive rates and longer repayment terms, making monthly payments more manageable.

However, common mistakes to avoid when considering this option include putting your primary asset at risk. If you default on a home equity loan or HELOC, you could lose your home. The application process can also be longer and more complex than other loan types, which might not be ideal for urgent car repairs. This option is generally more suitable for very expensive, critical repairs and when you have a stable financial outlook.

Beyond Traditional Loans: Alternative Solutions for Car Repairs

Sometimes, a formal loan isn’t the only answer to the question "how can I get a loan to fix my car?" Exploring alternatives can often save you money and stress.

1. Emergency Savings/Rainy Day Fund: The Ideal Scenario

The most financially sound approach to unexpected car repairs is to have an emergency fund specifically designated for such situations. This fund acts as a financial buffer, allowing you to pay for repairs outright without incurring debt or interest.

While building an emergency fund takes time and discipline, its value becomes immeasurable during crises. Even a small dedicated fund can significantly reduce the burden of minor repairs.

2. Borrowing from Friends or Family: A Personal Approach

In times of need, turning to trusted friends or family members can be a viable option. This can often mean interest-free loans or flexible repayment terms, which are huge advantages compared to traditional lenders.

Pro tips from us: If you decide to borrow from loved ones, it’s crucial to treat it as a formal agreement. Draft a simple written agreement outlining the loan amount, repayment schedule, and any agreed-upon terms. This helps prevent misunderstandings and preserves relationships. Clear communication and timely repayment are paramount.

3. Community Assistance Programs: Help for Those in Need

Various local charities, non-profit organizations, and community programs offer assistance for essential car repairs, especially for low-income individuals or families. These programs might have specific eligibility requirements, but they can provide grants or low-interest loans, effectively reducing your financial burden.

A quick search for "car repair assistance programs " can often yield valuable resources. While these options might involve an application process and waiting period, they are worth exploring, particularly if other avenues are challenging.

4. Refinancing Your Auto Loan (with Cash-Out): A Strategic Move

If you have an existing auto loan and your car has sufficient equity, you might be able to refinance it with a "cash-out" option. This involves taking out a new loan for a larger amount than your current outstanding balance, using the difference as cash for your repairs.

This can sometimes result in a lower interest rate on your entire loan, and you get the funds needed for repairs. However, common mistakes to avoid include extending the loan term significantly, which could mean paying more in interest over the life of the loan, even if the monthly payments are lower. Carefully calculate the total cost over the new loan term.

Navigating the Application Process: What You Need to Know

Once you’ve identified a potential loan to fix my car, understanding the application process is key to a smooth and successful experience.

1. Preparing Your Application: Gather Your Documents

Regardless of the loan type, lenders will require specific documentation to assess your financial standing. Typically, you’ll need:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Pay stubs, tax returns, bank statements.

- Proof of Address: Utility bills, lease agreement.

- Bank Account Information: For direct deposit and automatic payments.

Additionally, it’s incredibly helpful to know your current credit score. Many online services offer free credit score checks. Understanding where you stand will help you gauge which loan products you’re most likely to qualify for and at what rates. Pro tips from us: Check your credit report for any inaccuracies before applying. Disputing errors can improve your score and open up better loan opportunities.

2. Comparing Lenders: Look Beyond the First Offer

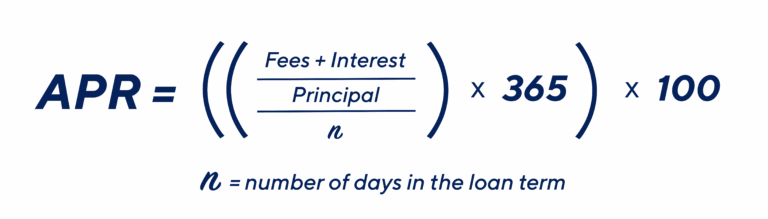

Never accept the first loan offer you receive. It’s essential to shop around and compare offers from multiple lenders – banks, credit unions, and online lenders. Pay close attention to the Annual Percentage Rate (APR), which includes not just the interest rate but also any fees associated with the loan, giving you a truer picture of the total cost.

Look at the repayment terms, monthly payment amounts, and any prepayment penalties. A lower monthly payment might seem attractive, but if it extends the loan term significantly, you could end up paying more in total interest.

Based on my years of helping clients navigate financing decisions, credit unions often offer competitive rates and more personalized service, especially for members. Online lenders can provide quick approvals and a streamlined application process. Take the time to get quotes from at least three different sources.

3. Understanding the Fine Print: Read Before You Sign

Before signing any loan agreement, meticulously read the entire document. Don’t hesitate to ask questions about anything you don’t understand. Pay close attention to:

- Interest Rate and APR: Ensure these match what was discussed.

- Fees: Origination fees, late payment fees, prepayment penalties.

- Repayment Schedule: Exact dates and amounts.

- Default Clauses: What happens if you miss payments.

Common mistakes to avoid include rushing through the paperwork due to urgency. A few extra minutes of careful review can save you from unexpected costs or unfavorable terms down the line. Remember, a reputable lender will be transparent and willing to answer all your questions.

Building Resilience: Preventing Future Car Repair Loan Needs

While finding a loan to fix my car is a crucial skill, an even better strategy is to minimize the need for such loans in the future. Proactive measures can save you stress and money.

1. Regular Maintenance: Prevention is Key

The old adage "an ounce of prevention is worth a pound of cure" holds especially true for car maintenance. Following your car manufacturer’s recommended maintenance schedule – including oil changes, tire rotations, fluid checks, and timely inspections – can significantly extend your vehicle’s lifespan and prevent costly major breakdowns.

Pro tips from us: Keep a detailed record of all maintenance performed. This not only helps you stay on schedule but also adds value if you decide to sell your car later. Neglecting routine care is one of the quickest ways to invite expensive, unexpected repairs.

2. Emergency Fund for Car Repairs: A Dedicated Savings Pot

Beyond a general emergency fund, consider creating a specific savings account for car-related expenses. Even setting aside a small amount each month, perhaps $25-$50, can accumulate over time and provide a safety net for future repairs, tires, or even your next vehicle down payment. This dedicated fund can make a huge difference when the unexpected happens.

3. Understanding Car Insurance: Your Coverage Matters

Review your car insurance policy periodically. While standard liability insurance won’t cover mechanical breakdowns, comprehensive and collision coverage can protect against damages from accidents, theft, or natural disasters. Some policies might also offer roadside assistance, which can be invaluable for unexpected issues on the road. Understanding your coverage limits and deductibles is crucial.

4. Extended Warranties: When Do They Make Sense?

For some drivers, an extended warranty can offer peace of mind against unexpected mechanical failures after the factory warranty expires. These can cover major components like the engine and transmission.

However, extended warranties aren’t for everyone. They can be expensive, and their coverage often has exclusions. Carefully read the terms and conditions, compare prices, and consider your car’s reliability history and your own risk tolerance before investing in one. For reliable vehicles or those you plan to replace soon, an extended warranty might not be cost-effective.

Conclusion: Driving Forward with Confidence

Facing an urgent car repair can be a daunting experience, but it doesn’t have to derail your financial stability. By understanding the diverse options available for a loan to fix my car, you can make an informed decision that best suits your individual circumstances. From personal loans and credit card strategies to exploring community assistance or even leveraging home equity, solutions exist to help you get back on the road.

Remember, the key lies in thorough research, careful comparison of offers, and meticulous attention to the fine print. And looking ahead, cultivating habits of regular vehicle maintenance and establishing a dedicated emergency fund are your strongest defenses against future repair crises. Drive forward with confidence, knowing you’re equipped with the knowledge to navigate life’s unexpected detours.

- Explore our comprehensive guide on budgeting for car maintenance here

- Learn more about improving your credit score to unlock better loan rates

- For trusted advice on consumer financial products, visit the Consumer Financial Protection Bureau (CFPB) website: https://www.consumerfinance.gov/