Your Ultimate Blueprint to Securing a Car Loan: Drive Away with Confidence

Your Ultimate Blueprint to Securing a Car Loan: Drive Away with Confidence Carloan.Guidemechanic.com

The dream of a new car – whether it’s a sleek sedan, a family-friendly SUV, or a rugged pickup – often begins not on the dealership lot, but with a crucial financial step: securing a car loan. For many, purchasing a vehicle outright isn’t feasible, making car financing an essential part of the process. Understanding how to make a car loan work for you, from application to approval, is paramount to driving away happy without financial stress.

This comprehensive guide is designed to demystify the entire car loan process. We’ll dive deep into every stage, providing you with the knowledge and strategies needed to confidently apply for and get approved for an auto loan that fits your budget and lifestyle. Our goal is to equip you with insights that ensure you not only get the car you want but also the best possible financing terms.

Your Ultimate Blueprint to Securing a Car Loan: Drive Away with Confidence

Laying the Foundation: Essential Steps Before You Apply for a Car Loan

Before you even think about test drives or showroom floors, the most critical work happens behind the scenes. Preparing your finances and understanding your capabilities will significantly increase your chances of securing favorable car loan terms. This preparation is your secret weapon.

Understanding Your Financial Health: The Bedrock of Loan Approval

Lenders assess your financial stability to determine their risk in lending you money. A clear picture of your income, expenses, and credit history is non-negotiable. This is where your journey to a successful car loan application truly begins.

1. Your Credit Score: The Unseen Force

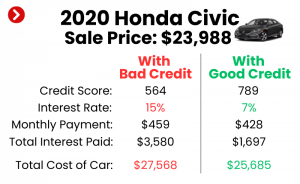

Your credit score is arguably the most influential factor in your car loan application. It’s a numerical representation of your creditworthiness, based on your payment history, outstanding debts, length of credit history, and more. A higher score signals to lenders that you are a responsible borrower, often translating into lower interest rates and better loan terms.

Based on my experience as a financial content specialist, a strong credit score can literally save you thousands of dollars over the life of your car loan. It directly impacts the Annual Percentage Rate (APR) you’ll be offered. Taking the time to understand and potentially improve your score before applying is an investment that pays off handsomely. You can obtain a free copy of your credit report from the three major bureaus (Experian, Equifax, TransUnion) annually. Review these reports carefully for any errors that could be negatively impacting your score and dispute them immediately.

2. Budgeting for Your Dream Car: What You Can Truly Afford

Many people make the mistake of focusing solely on the car’s sticker price or the monthly payment. However, a truly savvy car buyer considers the total cost of ownership. This includes the monthly car loan payment, insurance premiums, fuel costs, maintenance, and potential repair expenses.

Pro tip from us: Don’t just look at the monthly payment in isolation. Use a budgeting tool to understand your entire financial picture. A common guideline, sometimes called the 20/4/10 rule, suggests a 20% down payment, a loan term no longer than four years, and total car expenses (payment, insurance, fuel) not exceeding 10% of your gross monthly income. This framework helps ensure your car doesn’t become a financial burden.

3. The Power of a Down Payment: Boosting Your Equity

A down payment is the initial amount of money you pay upfront for the car, reducing the total amount you need to borrow. Making a significant down payment offers several substantial benefits. It immediately reduces your loan principal, which means you’ll pay less in interest over the life of the loan.

Furthermore, a larger down payment demonstrates your financial commitment to lenders, often leading to more favorable terms. It also helps you build equity in your vehicle faster, reducing the risk of being "upside down" on your loan, where you owe more than the car is worth. Common mistakes to avoid are skipping a down payment entirely or making one that is too small. While 10-20% is often recommended for new cars, any amount you can comfortably put down will positively impact your loan.

Navigating the Loan Landscape: Where to Find Your Car Loan

Once your financial house is in order, the next step is to explore where you can secure your car loan. There are several avenues, each with its own advantages and disadvantages. Understanding these options will empower you to choose the best fit for your circumstances.

Direct Lenders: Banks and Credit Unions

Traditional financial institutions like banks and credit unions are popular choices for car loans. They offer a direct relationship, allowing you to discuss terms, rates, and your financial situation personally with a loan officer.

Banks are well-established and offer a wide range of services, often with competitive rates for well-qualified borrowers. Credit unions, being member-owned non-profits, frequently offer some of the most competitive interest rates and personalized service. From our perspective, credit unions often provide excellent rates because they prioritize their members over maximizing profits. Applying for pre-approval with these lenders can give you a strong negotiating position at the dealership.

Dealership Financing: Convenience at a Cost?

Many car dealerships offer financing options directly through their finance departments. They act as intermediaries, working with a network of banks and captive lenders (financing arms of car manufacturers like Toyota Financial Services or Ford Credit).

The primary advantage here is convenience – you can select your car and arrange financing all in one place. Dealerships might also offer special promotional rates or incentives, especially on new vehicles. However, it’s crucial to be cautious. Dealerships often mark up interest rates to earn a profit, and their initial offer might not be the best available. A common mistake to avoid is assuming the dealership’s first offer is the best you’ll get. Always compare their offer with pre-approvals you’ve secured elsewhere.

Online Lenders: Speed and Variety

The digital age has brought forth a multitude of online lenders specializing in auto loans. These platforms offer a quick and often streamlined application process, allowing you to compare multiple offers from various lenders without leaving your home.

Online lenders can be a great option for finding competitive rates, especially if you have good credit. Their overheads are typically lower, which can sometimes translate into better rates for consumers. However, due to the lack of personal interaction, it’s vital to research any online lender thoroughly to ensure they are reputable. Always check reviews and verify their licensing before sharing personal information.

Private Party Car Loans: Specific Considerations

If you’re buying a car from a private seller instead of a dealership, the financing process differs slightly. Most traditional auto loans are designed for dealership purchases. However, some banks and credit unions do offer specific private party car loans.

These loans often require a bit more due diligence, as the lender will need to assess the car’s value and condition directly. You’ll typically need to provide more information about the vehicle, such as its VIN and mileage. It’s also crucial to ensure the car’s title is clear and transferable, protecting both you and the lender.

The Application Process: Step-by-Step for Loan Approval

With your financial groundwork laid and an understanding of lender types, you’re ready to tackle the application itself. This stage requires attention to detail and a strategic approach to maximize your approval chances and secure the best terms.

Getting Pre-Approved: Your Strategic Advantage

Pre-approval is a game-changer in the car buying process. It means a lender has reviewed your financial information and tentatively agreed to lend you a certain amount of money at a specific interest rate, before you even choose a car. This offer is usually valid for a set period, like 30 to 60 days.

Why is pre-approval so crucial? It transforms you into a cash buyer at the dealership. You walk in knowing exactly how much you can spend and what your interest rate will be, separating the car purchase negotiation from the financing discussion. This significantly enhances your negotiating power, as the dealer knows you have financing in hand and don’t need to rely on theirs. Be aware of the difference between pre-qualification (a soft credit pull, less firm) and pre-approval (a hard credit pull, more definitive).

Gathering Your Documents: Be Prepared

Lenders require specific documents to verify your identity, income, and ability to repay the loan. Having these ready before you apply will streamline the process and prevent delays.

Commonly requested documents include:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs, W-2 forms, or tax returns (especially for self-employed individuals).

- Proof of Residence: Utility bill or lease agreement.

- Proof of Insurance: You’ll need to show proof of auto insurance before driving the car off the lot.

- Vehicle Information: If you’ve already chosen a specific car, be ready with its VIN, make, model, and mileage.

Each document serves to confirm your eligibility and reduce the lender’s risk. Incomplete documentation is a frequent cause for delays or even denials.

Filling Out the Application Accurately: Honesty is Key

When completing the loan application, accuracy and honesty are paramount. Provide all requested information truthfully and double-check for any typos or errors. Discrepancies between your application and supporting documents can raise red flags for lenders.

Even minor errors can lead to processing delays or even the rejection of your application. Lenders will verify the information you provide, so ensure everything aligns perfectly with your financial records and personal details.

Understanding Loan Terms and Conditions: Read the Fine Print

Once you receive loan offers, it’s absolutely critical to understand all the terms and conditions. Don’t just focus on the monthly payment. Key elements to scrutinize include:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including the interest rate and any fees. A lower APR means less money paid over time.

- Loan Term: This is the duration of the loan, typically measured in months (e.g., 36, 48, 60, 72 months). A longer term means lower monthly payments but more interest paid overall.

- Monthly Payment: Ensure this fits comfortably within your budget.

- Fees and Charges: Look out for origination fees, application fees, or prepayment penalties. Some lenders charge extra if you pay off your loan early.

Pro tip: Always read the fine print before signing anything. Ask questions about anything you don’t understand. A reputable lender will be happy to explain all aspects of the loan agreement.

After Approval: Making Smart Choices for Your Purchase

Congratulations, your car loan has been approved! But the journey isn’t over. The decisions you make now, from comparing offers to finalizing the purchase, can significantly impact your overall satisfaction and financial well-being.

Comparing Loan Offers: Don’t Settle for the First

If you’ve applied for pre-approval from multiple lenders, you likely have several loan offers in hand. This is your opportunity to compare them side-by-side and choose the best one. Don’t just compare monthly payments.

Focus on the APR, as it reveals the true cost of the loan. Also, consider the total cost over the loan term. Even a slight difference in APR can translate into hundreds or thousands of dollars saved. Weigh the pros and cons of different loan terms against your budget and long-term financial goals.

Negotiating the Car Price: Separate the Deals

Having a pre-approved car loan gives you immense leverage to negotiate the actual price of the car. When you’re at the dealership, focus on negotiating the vehicle’s purchase price first, as if you were a cash buyer. Do not mention your financing until you’ve settled on the car’s price.

Once you’ve agreed on a price, you can then present your pre-approved financing. This strategy prevents the dealership from manipulating the car price and loan terms together to maximize their profit. You’re in control of both aspects.

Understanding Add-ons and Extras: Are They Worth It?

Dealerships often try to sell you various add-ons and extras during the financing process, such as extended warranties, GAP insurance, paint protection, or service plans. While some of these might offer value, many are high-profit items for the dealership.

- Extended Warranties: Can be useful for long-term peace of mind, but often come with a significant markup. Research third-party warranty providers for better deals.

- GAP Insurance: Covers the "gap" between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen. This can be worthwhile, especially with a small down payment, but often cheaper through your auto insurer.

Common mistakes to avoid are blindly accepting all add-ons without understanding their true cost or necessity. Carefully consider if each add-on provides genuine value and if you can obtain it more affordably elsewhere.

The Final Paperwork: Review Before You Sign

The final step is signing the contract. This is not a formality; it’s a legally binding agreement. Take your time to review every single detail of the final loan agreement and the purchase contract. Ensure that all the terms you agreed upon – the car price, interest rate, loan term, and any agreed-upon add-ons – are accurately reflected in the documents.

Look for any hidden fees or charges that weren’t discussed. If anything seems amiss or if you feel pressured, do not sign. It’s your right to fully understand what you’re committing to. Once you sign, you’re legally bound to the terms.

Special Considerations and Advanced Tips for Your Car Loan

Beyond the standard process, there are specific scenarios and strategies that can further optimize your car loan experience.

Loans for Bad Credit or No Credit: Options and Strategies

If you have bad credit or no credit history, securing a traditional car loan can be challenging, but it’s not impossible. Lenders specializing in subprime auto loans cater to this market, though they typically charge significantly higher interest rates to offset the increased risk.

Strategies for those with less-than-perfect credit include:

- A Co-signer: A family member or friend with good credit can co-sign your loan, making them equally responsible for repayment. This can help you secure approval and better rates.

- Secured Loans: Some lenders offer secured loans where the vehicle itself acts as collateral.

- Smaller, More Affordable Car: Opting for a less expensive used car reduces the loan amount, making it easier to get approved.

- Building Credit First: If possible, take time to improve your credit score before applying.

While these options might come with higher costs, they can be a stepping stone to rebuilding or establishing your credit.

Refinancing Your Car Loan: A Second Chance for Better Terms

You’re not stuck with your initial car loan terms forever. Refinancing your auto loan means taking out a new loan to pay off your existing one, often with a different lender or different terms. This can be a smart move if:

- Your Credit Score Has Improved: A better score can qualify you for a lower interest rate.

- Interest Rates Have Dropped: Market conditions might offer more favorable rates now.

- You Want to Lower Your Monthly Payment: Extending the loan term can reduce your monthly outlay (though you might pay more interest overall).

- You Want to Shorten Your Loan Term: This can save you interest and get you out of debt faster.

Many online lenders and credit unions specialize in car loan refinancing. It’s worth exploring this option if your financial situation has improved since you first bought your car.

The Impact of Your Debt-to-Income (DTI) Ratio: A Lender’s View

Your Debt-to-Income (DTI) ratio is another critical metric lenders use to assess your ability to manage monthly payments and repay debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income.

Lenders prefer a low DTI, typically under 36% to 43%, as it indicates you have sufficient income left after paying debts to cover new loan obligations. A high DTI can signal that you’re overextended financially, making lenders hesitant to approve another loan. To improve your DTI, focus on reducing existing debt or increasing your income before applying for a car loan.

Conclusion: Drive Away with Confidence and Smart Financing

Securing a car loan doesn’t have to be a daunting process. By understanding your financial health, exploring various lending options, meticulously navigating the application, and making informed decisions post-approval, you empower yourself to achieve the best possible outcome. This journey is about more than just getting approved; it’s about securing financing that aligns with your financial goals and contributes to your long-term stability.

Remember, preparation is key. Take the time to build your credit, create a realistic budget, and gather all necessary documents. Compare offers, read every line of the contract, and never be afraid to ask questions. With this comprehensive blueprint, you are well-equipped to make a car loan that not only gets you into your desired vehicle but also provides real value and peace of mind. Start your journey today, armed with knowledge, and drive away with confidence!