Your Ultimate Co-Pilot: Mastering Your $30,000 Car Loan with a Smart Calculator

Your Ultimate Co-Pilot: Mastering Your $30,000 Car Loan with a Smart Calculator Carloan.Guidemechanic.com

The thrill of a new car, the scent of fresh upholstery, the promise of open roads – it’s an exciting prospect! But for most of us, turning that dream into a reality involves navigating the world of car financing. When you’re looking at a $30,000 vehicle, understanding your loan options isn’t just helpful; it’s absolutely crucial.

This isn’t a small purchase, and rushing into it without proper planning can lead to financial strain down the line. That’s where a 30k car loan calculator becomes your indispensable financial co-pilot, guiding you through the complexities and empowering you to make smart decisions. This comprehensive guide will not only show you how to use this powerful tool but also delve deep into every factor influencing your loan, ensuring you drive away with confidence, not buyer’s remorse.

Your Ultimate Co-Pilot: Mastering Your $30,000 Car Loan with a Smart Calculator

Why a $30,000 Car Requires Smart Financing

A $30,000 car represents a significant investment for the average consumer. This price point often includes popular sedans, well-equipped SUVs, or even entry-level luxury vehicles, placing it firmly in the mid-to-upper range of the new car market. Such a substantial purchase demands a meticulous approach to financing.

Without careful consideration, you might find yourself with monthly payments that strain your budget, an interest rate higher than necessary, or a loan term that leaves you "upside down" on your vehicle for too long. Effective financing isn’t just about affording the car; it’s about securing terms that align with your overall financial health. This journey begins with understanding the numbers.

Demystifying the 30k Car Loan Calculator: Your Financial Co-Pilot

At its core, a car loan calculator is a simple yet incredibly powerful online tool designed to estimate your potential monthly car loan payments. For a 30k car loan calculator, it specifically helps you visualize the financial commitment required for a $30,000 vehicle purchase. It takes a few key pieces of information and, with a quick calculation, reveals what your budget needs to look like.

This calculator serves as your personal financial simulator. It allows you to experiment with different scenarios before you even step foot in a dealership. By inputting various figures, you can instantly see how changes to the interest rate, loan term, or down payment impact your monthly obligation.

Based on my experience, many buyers jump into car shopping without this crucial step. They fall in love with a car, and then try to make the numbers work, often settling for less favorable terms. Using a calculator upfront flips this script, putting you in control. It empowers you to approach negotiations with clarity, knowing exactly what you can comfortably afford. This proactive approach not only saves you money but also reduces stress significantly during the car-buying process.

The Core Components: What Goes Into Your 30k Car Loan Calculation?

To accurately calculate your potential monthly payments for a $30,000 car, a few fundamental variables come into play. Understanding each of these components is vital, as even minor adjustments can have a significant impact on your overall financial outlay. Let’s break them down in detail.

The Loan Amount (Your $30,000 Purchase)

This is the principal amount you are borrowing from the lender. When we talk about a "$30,000 car loan," this figure primarily refers to the cost of the vehicle itself. However, it’s important to remember that the actual amount you finance can be influenced by several factors beyond just the sticker price.

The final loan amount will be $30,000 minus any down payment you make, plus any additional fees, taxes, or add-ons (like extended warranties or GAP insurance) that you choose to roll into the loan. It’s crucial to be aware of these extra costs, as they can quickly inflate the total sum you need to borrow, increasing your monthly payments and the total interest paid over the life of the loan. Always focus on the "out-the-door" price when calculating your true borrowing needs.

The Interest Rate (The Cost of Borrowing)

The interest rate, expressed as an Annual Percentage Rate (APR), is essentially the cost you pay to borrow money. It’s not just a small percentage; it’s the most significant factor determining how much extra you’ll pay beyond the car’s sticker price. A lower interest rate means less money spent over the life of the loan.

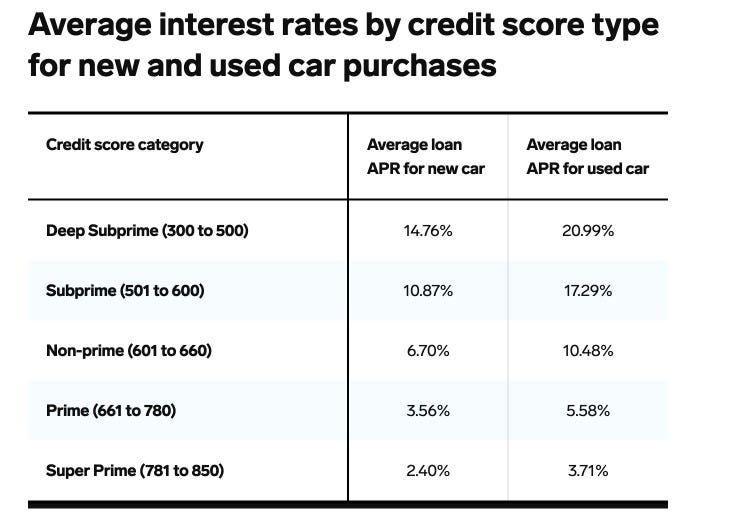

Many elements influence the interest rate you’ll be offered. Your credit score is paramount, with higher scores generally unlocking the best rates. Market conditions, the specific lender (bank, credit union, dealership), and the loan term you choose also play a role. Pro tips from us: Even a small difference in APR, say from 5% to 6%, can save you thousands of dollars over a 60-month loan on a $30,000 car. Always strive for the lowest possible APR, and don’t be afraid to shop around and compare offers from multiple lenders.

The Loan Term (How Long You’ll Pay)

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, or 72 months). This variable directly affects your monthly payment and the total amount of interest you’ll pay. It’s a classic trade-off: lower monthly payments versus higher total cost.

A shorter loan term (e.g., 36 or 48 months) means higher monthly payments but significantly less interest paid over time, leading to a lower total cost for the car. Conversely, a longer loan term (e.g., 60 or 72 months) results in lower, more "affordable" monthly payments, but you’ll pay substantially more in total interest. Common mistakes to avoid are stretching out a loan too long to afford a car you can’t truly afford. While a 72-month loan might seem appealing due to lower payments, you risk being "underwater" (owing more than the car is worth) for a longer period, and the cumulative interest can be shocking. We often advise finding a "sweet spot" that balances manageable monthly payments with a reasonable total cost, typically in the 48- to 60-month range for a $30,000 vehicle.

The Down Payment (Your Upfront Investment)

Your down payment is the amount of money you pay upfront towards the purchase of the car, reducing the total amount you need to borrow. This initial investment is incredibly crucial and offers multiple financial benefits.

Firstly, a larger down payment directly lowers your monthly loan payments, making the car more affordable on a day-to-day basis. Secondly, it reduces the total interest you’ll pay over the life of the loan because you’re borrowing less principal. Thirdly, it can help you secure a better interest rate, as lenders view borrowers with substantial down payments as lower risk. We generally recommend aiming for at least 10-20% of the vehicle’s purchase price as a down payment for a new car. For a $30,000 car, this means ideally putting down $3,000 to $6,000. This upfront investment builds immediate equity in your vehicle and provides a cushion against depreciation.

Step-by-Step: How to Effectively Use a 30k Car Loan Calculator

Using a car loan calculator is straightforward, but maximizing its benefits requires a strategic approach. Think of it as a financial playground where you can test different scenarios without any real-world commitment.

-

Gather Your Initial Information: Before you start, have a rough idea of the car’s price (around $30,000 for this exercise), an estimated down payment you can afford, and your credit score range. Even approximate figures are helpful for initial calculations.

-

Input the Loan Amount: Start with the $30,000 purchase price. Then, subtract your desired down payment. For example, if you plan to put $5,000 down, your loan amount becomes $25,000. Remember to consider sales tax and other fees that might be rolled into the loan if you’re not paying them upfront.

-

Enter Your Estimated Interest Rate (APR): This is where your credit score comes into play. If you have excellent credit (720+), you might estimate a lower APR (e.g., 4-6%). If your credit is good (670-719), estimate a slightly higher rate (e.g., 6-8%). For fair or average credit, expect higher rates. You can also use average rates published by financial institutions as a starting point.

-

Select Your Desired Loan Term: Begin with a common term like 60 months. This is a popular choice that balances monthly payments and total interest.

-

Calculate and Analyze: Hit the "calculate" button. The calculator will instantly display your estimated monthly payment. Now, the real work begins: experimenting.

-

Experiment with Different Scenarios:

- Increase Down Payment: See how an extra $1,000 or $2,000 down payment impacts your monthly payment. You might be surprised by the savings.

- Adjust Loan Term: Try a shorter term (48 months) to see how much more your payment would be, but also note the reduction in total interest. Then try a longer term (72 months) to see the payment drop, but also observe the significant increase in total interest.

- Vary Interest Rate: If you’re unsure of your exact APR, try a range of rates to understand the best-case and worst-case scenarios for your monthly payments. This helps you understand the importance of improving your credit or shopping for the best rate.

By playing with these variables, you gain a clear picture of what makes a $30,000 car truly affordable for your budget. It helps you set realistic expectations before you even start looking at specific vehicles.

Beyond the Numbers: Factors That Influence Your 30k Auto Loan Approval & Terms

While the calculator provides the payment estimate, securing the best terms for your $30,000 car loan involves understanding the underlying factors that lenders consider. These elements determine not only if your loan is approved but also the interest rate and conditions you’ll receive.

Your Credit Score: The Ultimate Game Changer

Your credit score is arguably the single most important factor influencing your car loan. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. Lenders use it to assess the risk of lending money to you.

A high credit score (generally 700+) indicates a responsible borrower, making you eligible for the lowest interest rates and most favorable terms. Conversely, a low credit score (below 620) signals higher risk, leading to higher interest rates or even loan denial. Pro tips from us: If your credit score isn’t where you want it to be, spend a few months improving it before applying for a major loan like a $30,000 car. Pay bills on time, reduce existing debt, and check your credit report for errors. This effort can save you thousands in interest.

Debt-to-Income Ratio (DTI)

Your Debt-to-Income (DTI) ratio is another critical metric lenders scrutinize. It compares your total monthly debt payments (including your prospective car payment, mortgage/rent, credit cards, student loans, etc.) to your gross monthly income. Lenders want to ensure you have enough disposable income to comfortably make your car payments.

A low DTI ratio (typically below 36-43%) indicates that you’re not overextended financially, making you a more attractive borrower. A high DTI suggests you might struggle to manage additional debt, potentially leading to higher interest rates or a rejected application. Be mindful of your existing financial commitments when considering a new car loan.

Co-Signers and Co-Borrowers

If your credit score or DTI ratio isn’t strong enough to secure a favorable $30,000 car loan on your own, a co-signer or co-borrower might be an option. A co-signer adds their creditworthiness to your application, essentially guaranteeing the loan if you default. A co-borrower shares equal responsibility for the loan and often shares ownership of the vehicle.

While these options can help you get approved or secure a better rate, they come with significant implications. The co-signer’s credit is also on the line, and any missed payments will negatively impact both credit scores. This decision should not be taken lightly and requires a high degree of trust and clear communication between all parties involved.

Lender Type (Banks, Credit Unions, Dealerships)

Where you get your loan can also impact the terms.

- Banks: Offer competitive rates, especially for well-qualified buyers. They often have online pre-approval processes.

- Credit Unions: Known for member-focused services and often provide excellent rates, sometimes even better than traditional banks, due to their non-profit structure.

- Dealerships: Offer convenience by providing on-site financing. However, their rates can sometimes be higher, as they act as intermediaries. Common mistakes to avoid are accepting the first offer without shopping around. Always compare offers from at least three different lenders (banks, credit unions, and the dealership) to ensure you’re getting the best possible deal. Pre-approval from an external lender gives you strong leverage during dealership negotiations.

Strategic Planning: Making Your $30,000 Car Affordable

Beyond just securing the loan, truly affording a $30,000 car involves a holistic approach to your finances. The monthly payment is just one piece of the puzzle.

Budgeting for the True Cost of Ownership

Many first-time buyers or those upgrading forget that the car’s sticker price and monthly payment are only part of the story. The true cost of ownership extends far beyond your loan. This includes:

- Car Insurance: Premiums can vary significantly based on the car’s value, your driving record, location, and the type of coverage you choose. For a $30,000 car, expect higher insurance costs than for a less expensive vehicle.

- Fuel Costs: Consider the car’s fuel efficiency and your daily commute.

- Maintenance and Repairs: All cars need regular maintenance, and a $30,000 vehicle, especially if it’s new or a higher-end model, might have more expensive parts or specialized service requirements.

- Registration and Taxes: Annual fees vary by state and vehicle value.

- Depreciation: While not an out-of-pocket expense, depreciation is the single largest cost of car ownership. A $30,000 car will lose a significant portion of its value in the first few years.

For a deeper dive into overall car budgeting, check out our article on . Understanding these additional expenses ensures your $30,000 car remains a joy, not a financial burden.

Pre-Approval: Your Secret Weapon

Getting pre-approved for a car loan before you visit a dealership is one of the smartest moves you can make. Pre-approval means a lender has already evaluated your creditworthiness and agreed to lend you a specific amount at a particular interest rate, contingent on the final car details.

The benefits are immense. You walk into the dealership knowing exactly how much you can spend and what your interest rate will be. This transforms you into a cash buyer, giving you significant negotiation power. You can focus on negotiating the price of the car rather than being swayed by monthly payment figures offered by the dealership. It separates the financing from the purchase, streamlining the process and often leading to a better overall deal.

Negotiating Smartly

Armed with your pre-approval and an understanding of what your 30k car loan calculator has shown you, you’re ready to negotiate.

- Focus on the Out-the-Door Price: Always negotiate the total purchase price of the vehicle first, not just the monthly payment. Dealerships can manipulate loan terms (like stretching out the term) to make a higher car price seem affordable.

- Be Prepared to Walk Away: The power of walking away from a deal you’re not comfortable with is immense. There are always other cars and other dealerships.

- Don’t Forget Trade-Ins: If you have a trade-in, negotiate its value separately from the new car’s price.

- Scrutinize Add-Ons: Be wary of high-pressure sales tactics for expensive add-ons like extended warranties, paint protection, or VIN etching. Evaluate if you truly need them and if the price is fair.

FAQs About Your 30k Car Loan

Navigating a significant purchase like a $30,000 car often brings up a lot of questions. Here are some of the most common ones we encounter:

Can I get a 30k car loan with bad credit?

While challenging, it is often possible to get a $30,000 car loan with bad credit (typically a score below 620). However, you should expect significantly higher interest rates, which means your monthly payments and total cost will be much greater. Lenders view bad credit as a higher risk, and they compensate for that risk by charging more. In some cases, a co-signer with good credit might be necessary to secure approval or a more reasonable rate. It’s always advisable to work on improving your credit score before applying for such a substantial loan.

What is a good interest rate for a 30k car loan?

A "good" interest rate largely depends on your credit score and current market conditions. As of late 2023/early 2024, excellent credit (720+) might secure rates in the 5-7% APR range. Good credit (670-719) could see rates between 7-10%, while fair credit (620-669) might range from 10-15% or higher. For individuals with bad credit, rates can exceed 20%. Always compare offers from multiple lenders to ensure you’re getting the most competitive rate available for your credit profile.

How much should my monthly payment be for a 30k car?

There’s no one-size-fits-all answer, as it depends on your down payment, interest rate, and loan term. However, a common rule of thumb is that your total car expenses (payment, insurance, fuel, maintenance) should not exceed 10-20% of your take-home pay. Using a 30k car loan calculator will give you precise estimates. For example, with a $5,000 down payment, a 60-month loan at 7% APR for a $25,000 financed amount would result in a monthly payment of approximately $495. Adjust these figures based on your personal budget and comfort level.

Is it better to get a longer or shorter loan term?

Generally, a shorter loan term is financially "better" because you pay significantly less in total interest over the life of the loan. For example, a 36-month loan on a $30,000 car will cost much less overall than a 72-month loan, even though the monthly payments will be higher. However, a longer term offers lower monthly payments, which can make a $30,000 car more "affordable" on a monthly budget. The best choice depends on your financial priorities: if you can comfortably afford higher monthly payments, opt for a shorter term to save on interest. If budget tightness is a concern, a longer term might be necessary, but be aware of the increased total cost.

Should I put a large down payment on a 30k car?

Yes, absolutely! Putting a larger down payment on a $30,000 car is almost always a smart financial move. It directly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay. A substantial down payment also builds immediate equity in your vehicle, reducing the risk of being "underwater" on your loan (owing more than the car is worth) due to depreciation. Lenders also view larger down payments favorably, sometimes leading to better interest rate offers. Aim for at least 10-20% of the purchase price if possible.

Final Thoughts: Empowering Your Car Buying Journey

Buying a $30,000 car is an exciting milestone, and with the right tools and knowledge, it can also be a financially sound decision. The 30k car loan calculator is more than just a numbers cruncher; it’s an empowerment tool that puts you in the driver’s seat of your financial future. It allows you to plan, compare, and negotiate with confidence, ensuring that your dream car fits comfortably within your budget.

Don’t let the allure of a new vehicle overshadow the importance of smart financial planning. Use this guide, leverage the power of the calculator, and approach your car purchase with a clear head and a solid strategy. By understanding the core components of a loan, planning for the true cost of ownership, and strategically shopping for the best terms, you can make an informed decision that brings lasting satisfaction.

For more comprehensive financial guidance on auto loans, you can visit the Consumer Financial Protection Bureau’s Auto Loans guide at https://www.consumerfinance.gov/consumer-tools/auto-loans/. Considering a different price point? Our might also be helpful. Happy driving!