Your Ultimate Guide: How To Ask For A Car Loan (And Get Approved!)

Your Ultimate Guide: How To Ask For A Car Loan (And Get Approved!) Carloan.Guidemechanic.com

Dreaming of that new car smell or the reliable purr of a pre-owned vehicle? For most of us, turning that dream into a reality involves navigating the world of car loans. It can feel like a complex maze, full of jargon and uncertainty. But what if you could approach the process with confidence, armed with knowledge, and significantly boost your chances of approval?

Based on my years of experience helping countless individuals secure their ideal car financing, I can tell you that asking for a car loan isn’t just about filling out a form. It’s an art and a science, requiring preparation, strategy, and a clear understanding of what lenders are looking for. This comprehensive guide is designed to transform you from a hesitant applicant into an empowered borrower. We’ll break down every step, reveal expert tips, and highlight common pitfalls to ensure your journey to car ownership is smooth and successful.

Your Ultimate Guide: How To Ask For A Car Loan (And Get Approved!)

Why Understanding Car Loans is Crucial for Every Buyer

Getting a car loan is a significant financial commitment, often spanning several years. It impacts your monthly budget, your overall financial health, and your credit score. Approaching this decision without proper knowledge can lead to higher interest rates, unfavorable terms, or even rejection.

An informed borrower is a powerful borrower. When you understand the factors influencing loan approval and the different types of financing available, you gain leverage. This knowledge allows you to negotiate better terms, save thousands of dollars over the life of the loan, and ultimately make a choice that genuinely fits your financial situation. Let’s dive in and equip you with that power.

Before You Even Think About Asking: Laying the Groundwork

Success in securing a car loan begins long before you step foot in a dealership or click "apply" online. It starts with thorough preparation and a deep understanding of your financial standing. This foundational work is the single most important step in how to ask for a car loan effectively.

1. Understand Your Credit Score Inside and Out

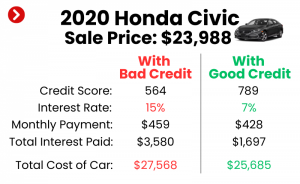

Your credit score is arguably the most critical factor lenders consider. It’s a three-digit number that summarizes your creditworthiness, essentially telling lenders how risky it might be to lend you money. A higher score typically translates to better interest rates and easier approval.

Why Your Credit Score Matters So Much

Lenders use your credit score to assess your payment history and your ability to manage debt. A strong score, generally above 670 (FICO score), signals to them that you are a reliable borrower who pays bills on time. Conversely, a lower score suggests a higher risk, often resulting in higher interest rates to compensate the lender for that perceived risk, or even a denial of your application.

How to Check Your Credit Score (and Report)

Don’t wait for a lender to tell you your score. You are entitled to a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months. You can access these reports at annualcreditreport.com. This is a crucial first step.

Pro tip: Don’t just look at the number, understand the factors influencing it. Your credit report details your payment history, types of credit accounts, amounts owed, length of credit history, and new credit inquiries. Scrutinize it for any errors, as these can negatively impact your score. If you find discrepancies, dispute them immediately.

Tips for Improving Your Credit Score

If your score isn’t where you want it to be, take steps to improve it before applying for a car loan. Even a few months of diligent effort can make a difference. The primary factors affecting your score are payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), and credit mix (10%).

- Pay all your bills on time, every time: This is the most impactful action you can take. Set up automatic payments if necessary.

- Reduce your credit utilization: Keep your credit card balances low, ideally below 30% of your available credit limit.

- Avoid opening new credit accounts: Multiple new credit inquiries in a short period can temporarily lower your score.

- Address any outstanding collections or past-due accounts: Lenders will see these.

2. Determine Your Realistic Budget

It’s exciting to imagine driving a new car, but it’s vital to stay grounded in reality when it comes to your budget. Your budget isn’t just about the monthly car payment; it’s about the total cost of car ownership. Many people make the mistake of focusing solely on the payment.

Beyond the Monthly Payment: The True Cost of Car Ownership

When budgeting for a car, you need to consider several factors:

- The Car Loan Payment: This is the most obvious, but ensure it comfortably fits within your monthly expenses.

- Car Insurance: Premiums vary significantly based on the car’s make, model, your driving record, and location. Get quotes before you buy.

- Fuel Costs: Estimate your average mileage and current gas prices.

- Maintenance and Repairs: All cars, especially used ones, require regular maintenance. Set aside a fund for unexpected repairs.

- Registration and Licensing Fees: These are recurring annual costs.

- Sales Tax: This is usually paid upfront or rolled into your loan.

Your Debt-to-Income (DTI) Ratio

Lenders look at your DTI ratio, which compares your total monthly debt payments to your gross monthly income. A lower DTI ratio (typically below 36-43%) indicates you have more disposable income to manage new debt, making you a less risky borrower. Calculate yours before applying.

Common mistake: Focusing only on the monthly payment can lead to financial strain down the road. A car that seems affordable on a monthly basis might become a burden once insurance, fuel, and maintenance are added. Always look at the holistic picture.

3. Save for a Down Payment

While it’s possible to get a car loan with no down payment, it’s almost always a smarter financial move to put money down. A down payment reduces the amount you need to borrow, which can significantly impact your loan terms.

Benefits of a Down Payment

- Lower Loan Amount: Less money borrowed means less interest paid over the life of the loan.

- Better Interest Rates: Lenders see a down payment as a sign of commitment and reduced risk, often offering more favorable APRs.

- Reduced Loan-to-Value (LTV) Ratio: LTV compares the loan amount to the car’s value. A lower LTV protects you from being "upside down" on your loan (owing more than the car is worth), which is common with new cars due to immediate depreciation.

- Lower Monthly Payments: A smaller loan balance naturally results in lower monthly payments.

Recommended Percentage

Ideally, aim for a down payment of at least 10-20% of the car’s purchase price. For used cars, even 5-10% can make a difference. The more you put down, the stronger your application becomes, and the better your long-term financial position will be.

4. Know What Car You Want (or at least the Type)

You don’t need to have the exact VIN number, but having a clear idea of the type of car you want is crucial. This includes whether it will be new or used, and a general price range. This impacts the loan terms you’ll be seeking.

New vs. Used Car Considerations

- New Cars: Often come with lower interest rates (especially through manufacturer incentives), but depreciate quickly. Loan terms might be longer, potentially extending to 72 or even 84 months.

- Used Cars: Typically have higher interest rates due to perceived higher risk, and shorter loan terms. However, they are generally more affordable upfront and depreciate less rapidly.

Understanding these differences helps you set realistic expectations for your loan application. Knowing your target car also allows you to research average selling prices, preventing you from overpaying. This preparation is a key component of how to ask for a car loan smartly.

The Art of Asking: Navigating the Application Process

With your groundwork laid, you’re now ready to actively seek out a car loan. This stage involves gathering documents, exploring various lenders, and understanding the power of pre-approval.

1. Gather Your Essential Documents

Once you decide to apply, having all your necessary documents readily available will streamline the process and demonstrate your preparedness to lenders. Missing documents can cause delays or even put your application on hold.

Key Documents You’ll Need:

- Proof of Identity: A valid government-issued photo ID (like a driver’s license or state ID) and your Social Security number.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, or tax returns (especially if self-employed or for the previous year). This shows your ability to repay the loan.

- Proof of Residence: Utility bills (electricity, water, gas) or a lease agreement/mortgage statement with your current address. This verifies your stability.

- Bank Statements: Recent statements (1-2 months) can show your financial habits and cash flow.

- Trade-in Information (if applicable): If you plan to trade in your current vehicle, have its title or registration and any loan payoff information.

Based on my experience, having all these ready dramatically speeds up the process. A well-organized applicant often makes a better impression, signaling responsibility and attention to detail.

2. Explore All Your Lender Options

Don’t make the mistake of only considering the financing offered by the car dealership. Shopping around for your loan is one of the most effective ways to secure the best possible terms. There are three main avenues for car loans:

a) Dealership Financing

- Pros: Convenience (one-stop shop), sometimes offer promotional rates from manufacturers (especially for new cars).

- Cons: Often mark up interest rates for profit, may push add-ons you don’t need, less transparency than direct lenders. Their primary goal is to sell you a car, not necessarily the best loan.

b) Banks & Credit Unions

- Pros: Often offer competitive rates, especially if you have an existing relationship with them. Credit unions are non-profit and often have some of the lowest rates. They are direct lenders, so you deal directly with them.

- Cons: Can have a slightly longer approval process than online lenders, may require you to be a member (for credit unions).

c) Online Lenders

- Pros: Very competitive rates due to lower overhead, quick application and approval processes (sometimes within minutes), wide range of options through comparison platforms.

- Cons: Less personalized service, you need to be comfortable with a fully digital process.

Pro tip: Don’t limit yourself to the first offer. Comparing offers from at least 3-4 different lenders (banks, credit unions, and online) can save you a significant amount of money over the loan term. This competitive shopping is central to how to ask for a car loan successfully.

3. Get Pre-Approved for a Loan

This is a game-changer and arguably the most powerful tool in your car buying arsenal. Pre-approval means a lender has reviewed your credit and financial information and tentatively agreed to lend you a specific amount at a particular interest rate, before you even choose a car.

What Pre-Approval Is and Why It’s Powerful

- Know Your Buying Power: You walk into the dealership knowing exactly how much you can afford, acting like a cash buyer.

- Negotiating Leverage: You have an offer in hand, which allows you to negotiate the car’s price separately from the financing. If the dealership can’t beat your pre-approved rate, you can simply use your outside financing.

- Faster Process: With financing already secured, the purchasing process at the dealership is much quicker.

- Focus on the Car: You can concentrate on finding the right vehicle without the pressure of financing decisions hanging over your head.

Soft vs. Hard Inquiries

Most pre-approvals involve a "soft inquiry" on your credit report, which doesn’t affect your score. When you finalize the loan, it becomes a "hard inquiry," which can temporarily ding your score by a few points. However, credit bureaus typically count multiple hard inquiries for the same type of loan (like car loans) within a short period (usually 14-45 days) as a single inquiry, recognizing you’re rate shopping.

Common mistake: Walking into a dealership without pre-approval puts you at a distinct disadvantage. You’re negotiating on two fronts (car price and loan terms) simultaneously, and the dealer has more control over the process. Get pre-approved first!

4. Fill Out the Application Accurately and Honestly

When it comes time to complete the loan application, whether online or in person, ensure every piece of information is accurate and truthful. Lenders verify the details you provide.

Importance of Full Disclosure

- Expedited Processing: Accurate information allows lenders to process your application quickly.

- Trust and Credibility: Providing truthful information builds trust with the lender.

- Legal Implications: Misrepresenting facts on a loan application can have serious legal consequences, including fraud charges.

Lenders will cross-reference your application details with your credit report, income documents, and other proofs. Any inconsistencies can lead to delays, requests for more information, or even outright denial. Be transparent about your financial situation, even if it’s not perfect.

Understanding the Loan Offer: What to Look For

Once you receive loan offers, it’s critical to understand every component before signing on the dotted line. Don’t just look at the monthly payment; delve into the details.

1. Annual Percentage Rate (APR)

This is perhaps the most important number after the loan amount itself. The APR is the true cost of borrowing money annually, expressed as a percentage. It includes not only the interest rate but also any other fees associated with the loan, like origination fees.

Beyond the Interest Rate: The True Cost

Two loans might have the same interest rate, but different APRs if one has additional fees. A lower APR means you’ll pay less over the life of the loan. This is why comparing APRs, not just interest rates, is crucial when evaluating different offers.

2. Loan Term

The loan term is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or 84 months).

Shorter vs. Longer Terms

- Shorter Terms (e.g., 36-48 months):

- Pros: You pay significantly less interest over the life of the loan. You own the car outright faster.

- Cons: Higher monthly payments.

- Longer Terms (e.g., 72-84 months):

- Pros: Lower monthly payments, making the car seem more affordable.

- Cons: You pay much more interest over the life of the loan. You risk being "upside down" on your loan for a longer period. The car’s value may depreciate faster than you pay off the loan.

Choose a loan term that balances affordability with the total cost of interest.

3. Monthly Payment

This is the amount you’ll be paying each month. While important for budgeting, remember not to let it be your sole focus. A lower monthly payment achieved through a longer loan term can mask a much higher total cost.

Affordability Check

Ensure the monthly payment, combined with your insurance, fuel, and maintenance estimates, comfortably fits within your budget. Never stretch your finances too thin for a car.

4. Fees and Charges

Read the loan agreement carefully for any hidden fees. Common fees can include:

- Origination Fees: A fee charged by the lender for processing the loan.

- Documentation Fees (Doc Fees): Charged by dealerships for processing paperwork. These can sometimes be negotiable.

- Prepayment Penalties: Though rare for car loans, always check if there’s a penalty for paying off your loan early. You want the flexibility to pay it down faster if your financial situation improves.

Pro tip: Always ask for the total cost of the loan over its lifetime. This includes the principal amount plus all interest and fees. This comprehensive figure gives you the clearest picture of what you’re truly paying.

Negotiating Your Car Loan: Don’t Be Afraid to Haggle

Many people are comfortable negotiating the price of a car, but fewer realize they can also negotiate the terms of their loan. This is where your pre-approval becomes a powerful bargaining chip.

1. Leveraging Pre-Approval Offers

When you have a pre-approval from an outside lender, you’re in a strong position. Present this offer to the dealership’s finance department. They may try to beat it to keep the financing in-house, which can work to your advantage. If they can’t, you simply proceed with your pre-approved loan.

2. Negotiate the Car Price Separately from the Loan

This is a critical strategy. Always finalize the car’s purchase price before discussing financing. When these two negotiations are combined, it’s easy for dealers to shift numbers around, giving you a good deal on the car but a bad loan, or vice versa.

Based on my experience, many people leave money on the table by not negotiating. Be firm, polite, and prepared to walk away if the terms aren’t favorable. Remember, you’re in control.

3. Walking Away if the Terms Aren’t Right

Never feel pressured to accept a loan offer that doesn’t align with your budget or your pre-approval. There are always other lenders and other cars. Being willing to walk away demonstrates confidence and often prompts lenders or dealers to sweeten their offer.

Common Mistakes to Avoid When Asking for a Car Loan

Even with the best intentions, borrowers often fall into common traps. Being aware of these can save you a lot of headache and money. These are the pitfalls I’ve seen countless borrowers fall into, and avoiding them is key to how to ask for a car loan successfully.

- Not Checking Your Credit Score: This is fundamental. You can’t improve what you don’t know, and you can’t challenge errors you haven’t seen.

- Not Budgeting Properly: Focusing only on the monthly payment without considering the total cost of ownership (insurance, fuel, maintenance) can lead to financial strain.

- Taking the First Offer: Whether it’s from your bank or the dealership, always shop around. Competition among lenders benefits you.

- Extending the Loan Term Too Much: While a longer term means lower monthly payments, it drastically increases the total interest paid and keeps you in debt longer.

- Focusing Solely on Monthly Payments: This often leads to longer loan terms and higher overall costs. Look at the total interest and the APR.

- Buying More Car Than You Can Afford: It’s easy to get caught up in the excitement, but stick to your budget. The car you can afford is better than the car that burdens you.

- Ignoring Add-Ons: Dealerships often try to sell you extended warranties, GAP insurance, or other add-ons. While some might be beneficial, always evaluate if you truly need them and if you can get them cheaper elsewhere.

- Not Reading the Fine Print: Always read your entire loan agreement before signing. Understand all terms, conditions, and fees.

After Approval: What Next?

Congratulations, you’ve secured your car loan! But the journey isn’t over. A few final steps ensure a smooth start to your car ownership.

1. Finalizing Paperwork

Carefully review all final documents, ensuring that the terms (APR, loan amount, monthly payment, loan term) match what you agreed upon. Don’t hesitate to ask questions if anything is unclear. Sign only when you are completely satisfied.

2. Making Payments On Time

This is paramount. Set up automatic payments to avoid missing due dates, which can incur late fees and negatively impact your credit score. Consistent, on-time payments are the best way to build a strong credit history.

3. Building Good Credit

Your car loan is an excellent opportunity to demonstrate responsible financial behavior. As you make consistent payments, your credit score will likely improve, opening doors to even better financial opportunities in the future.

Conclusion: Drive Away with Confidence

Asking for a car loan doesn’t have to be a stressful experience. By understanding your credit, setting a realistic budget, gathering your documents, exploring all your options, and getting pre-approved, you equip yourself with the knowledge and leverage needed to secure the best possible terms. Remember, an informed borrower is an empowered borrower.

Don’t let the excitement of a new vehicle overshadow the importance of smart financial planning. Take your time, do your homework, and approach the process with confidence. Your future self (and your wallet) will thank you. Now that you’re armed with this comprehensive guide, you’re ready to confidently navigate the car loan landscape and drive away in your dream car. Start preparing today, and make your car buying experience a resounding success!