Your Ultimate Guide: How To Get A Used Car Loan with Confidence and Ease

Your Ultimate Guide: How To Get A Used Car Loan with Confidence and Ease Carloan.Guidemechanic.com

Embarking on the journey to purchase a used car can be both exciting and a little daunting. While the thrill of finding your perfect pre-owned vehicle is undeniable, securing the right financing often feels like navigating a complex maze. Many people find themselves wondering: How do I get a used car loan? What do lenders look for? And how can I ensure I get the best possible terms?

You’re not alone in these questions. Securing a used car loan is a significant financial decision, and understanding the process thoroughly is your most powerful tool. This comprehensive guide is designed to demystify used car financing, providing you with actionable insights and expert tips to secure a loan that fits your budget and needs. Our ultimate goal is to empower you to drive away in your dream car, knowing you’ve made a smart financial choice.

Your Ultimate Guide: How To Get A Used Car Loan with Confidence and Ease

Understanding Used Car Loans: Laying the Foundation

Before diving into the application process, it’s crucial to understand what makes used car loans unique. Unlike new car loans, which often come with manufacturer incentives and lower interest rates, used car loans can present a different set of challenges and opportunities. Lenders assess used vehicles differently, factoring in age, mileage, and condition.

Based on my experience in the auto finance world, a common misconception is that all car loans are the same. This isn’t true. The inherent depreciation of a used car, which is typically faster initially than a new car, means lenders perceive a slightly higher risk. This risk assessment directly influences the interest rates and terms they offer.

What Factors Influence Your Used Car Loan?

Several key factors will determine the kind of used car loan you qualify for. Understanding these elements beforehand allows you to prepare and potentially improve your loan terms. It’s about more than just finding a car; it’s about presenting yourself as a reliable borrower.

- Your Credit Score: This is perhaps the most critical factor. A higher credit score signals to lenders that you have a history of managing debt responsibly.

- Your Debt-to-Income (DTI) Ratio: Lenders want to see that you have enough disposable income to comfortably make your car payments.

- The Vehicle Itself: The age, mileage, and overall condition of the used car you intend to purchase significantly impact its loan-to-value (LTV) ratio and the lender’s willingness to finance it. Older cars or those with very high mileage can be harder to finance.

- Down Payment Amount: A larger down payment reduces the amount you need to borrow, which can lead to lower monthly payments and better interest rates. It also signals your commitment to the purchase.

- Loan Term: The length of time you have to repay the loan affects your monthly payment and the total interest paid over the life of the loan. Longer terms mean lower monthly payments but higher overall interest.

Types of Lenders for Used Car Loans

You have several avenues when it comes to securing a used car loan. Each type of lender has its own advantages and disadvantages, and knowing your options is part of a smart strategy.

- Banks: Traditional banks are a popular choice, often offering competitive rates for borrowers with good credit. They typically have a structured application process and established relationships with customers.

- Credit Unions: These member-owned financial institutions are known for offering some of the best interest rates, especially to their members. If you’re eligible to join one, it’s definitely worth exploring.

- Dealerships: Many dealerships offer in-house financing or work with a network of lenders. This can be convenient, allowing you to handle the car purchase and financing in one place. However, always compare their offers with independent lenders.

- Online Lenders: A growing number of online platforms specialize in auto loans. They often provide quick pre-approvals and allow for easy comparison shopping from multiple lenders. This option offers flexibility and speed.

Pro tips from us: Don’t limit yourself to just one type of lender. Shopping around is key to finding the most favorable terms for your unique situation.

The Pre-Approval Power Play: Your First Smart Move

One of the most effective strategies when learning how to get a used car loan is to secure pre-approval. This step is often overlooked, but it gives you immense power and confidence during the car-buying process. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a certain amount of money at a specific interest rate, before you even choose a car.

Think of pre-approval as walking into a dealership with cash in hand. It immediately shifts the dynamics of negotiation in your favor. You know exactly how much you can spend, which helps you stick to your budget and avoid being swayed by high-pressure sales tactics.

How to Get Pre-Approved for a Used Car Loan

Getting pre-approved is a straightforward process, but it requires some preparation. Most lenders will ask for similar information to assess your creditworthiness.

- Gather Your Documents: You’ll typically need proof of income (pay stubs, tax returns), proof of residence (utility bill), and identification (driver’s license). Having these ready speeds up the process.

- Check Your Credit Score: Before applying, get a copy of your credit report. This allows you to identify any errors and understand where you stand. Many credit card companies offer free credit score monitoring.

- Shop Around for Lenders: Apply for pre-approval with 2-3 different lenders (banks, credit unions, online lenders). This allows you to compare offers and find the best interest rate and terms. Multiple pre-approvals within a short timeframe (usually 14-45 days) will typically only count as a single hard inquiry on your credit report.

Based on my experience, knowing your budget upfront prevents emotional overspending. It also empowers you to focus on the car’s value and condition, rather than getting caught up in monthly payment negotiations that might hide unfavorable loan terms.

Sharpening Your Financial Profile: Boosting Your Chances

Lenders look at your financial profile to determine risk. The stronger your profile, the better your chances of securing a favorable used car loan. This section focuses on key areas you can improve to make yourself a more attractive borrower.

Understanding and Improving Your Credit Score

Your credit score is a numerical representation of your creditworthiness. It’s a snapshot of how well you’ve managed debt in the past.

- Importance: A good credit score (typically 670 and above) indicates a low risk to lenders, often resulting in lower interest rates. A lower score might still get you a loan, but likely at a higher rate.

- How to Check: You can obtain a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, TransUnion) once every 12 months at AnnualCreditReport.com. Review it for accuracy.

- How to Improve It:

- Pay Bills on Time: Payment history is the most significant factor in your credit score. Make all payments, especially on credit cards and existing loans, before their due dates.

- Reduce Credit Utilization: Keep your credit card balances low relative to your credit limits. Aim for under 30% utilization.

- Avoid Opening Too Many New Accounts: Each new credit application can temporarily ding your score.

- Address Errors: Dispute any inaccuracies you find on your credit report immediately.

Common mistakes to avoid are ignoring your credit report until you need a loan. Regular monitoring can prevent unpleasant surprises and give you time to make improvements.

The Power of a Down Payment

A down payment is the initial amount of money you pay upfront for the used car. It directly reduces the amount you need to borrow.

- Why It Matters: A significant down payment reduces the lender’s risk. If you default, they have less to recover. It also means you’re financing less, leading to lower monthly payments and less interest paid over the life of the loan.

- Recommended Amounts: While there’s no hard and fast rule for used cars, aiming for at least 10-20% of the vehicle’s purchase price is a good target. For those with less-than-perfect credit, a larger down payment can often be the key to approval.

- Benefits:

- Lower monthly payments.

- Reduced total interest paid.

- Less risk of negative equity (owing more than the car is worth).

- Potentially better loan terms.

Pro tips from us: Even a small down payment is better than none. Start saving early if you know you’ll be buying a car soon.

Understanding Your Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to gauge your ability to take on additional debt.

- What It Is: To calculate your DTI, add up all your monthly debt payments (rent/mortgage, credit cards, student loans, etc.) and divide that sum by your gross monthly income.

- Lender Expectations: Most lenders prefer a DTI ratio of 36% or lower, though some might go up to 43% for auto loans. A lower DTI indicates you have more disposable income to manage your new car payment.

- How to Improve It:

- Pay down existing debts.

- Increase your income (if possible).

- Avoid taking on new debt before applying for a car loan.

Income Stability and Documentation

Lenders want assurance that you have a steady income source to make your payments. Consistent employment history and verifiable income are crucial.

- Lender Expectations: Typically, lenders look for at least two years of consistent employment with the same employer, or within the same field.

- Documentation: Be prepared to provide recent pay stubs (usually 2-3 months), W-2 forms, and sometimes even bank statements. Self-employed individuals will need tax returns and profit/loss statements.

Navigating the Application Process: Step-by-Step Guide

Once you’ve done your homework and sharpened your financial profile, it’s time to formally apply for your used car loan. This stage involves completing paperwork and understanding the terms presented to you.

Gathering Necessary Documents

Having all your paperwork in order before you apply can significantly speed up the process and demonstrate your preparedness to lenders.

- Proof of Identity: Valid driver’s license or state-issued ID.

- Proof of Income: Recent pay stubs (2-3 months), W-2 forms, tax returns (for self-employed), or bank statements.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Proof of Insurance: While you don’t need insurance before buying the car, you’ll need to show proof of coverage before driving it off the lot. Lenders require full coverage on financed vehicles.

- Vehicle Information (if you’ve chosen one): Make, model, year, VIN, and selling price.

Filling Out the Application Accurately

Take your time when completing the loan application. Accuracy is paramount. Any discrepancies or incomplete information can cause delays or even rejection.

- Be Honest: Provide accurate information about your income, employment, and debts. Lenders will verify this information.

- Review Before Submitting: Double-check all fields for correctness, especially names, addresses, and financial figures.

Common mistakes to avoid are rushing through the application or intentionally misrepresenting information. This can lead to serious consequences and erode trust with potential lenders.

Understanding Loan Terms: APR, Loan Term, Principal

When you receive a loan offer, it’s essential to understand the key terminology. Don’t just focus on the monthly payment.

- Annual Percentage Rate (APR): This is the true cost of borrowing, expressed as a yearly percentage. It includes the interest rate plus any fees associated with the loan. A lower APR means a cheaper loan.

- Loan Term: This is the length of time, typically in months (e.g., 36, 48, 60, 72 months), you have to repay the loan. Longer terms mean lower monthly payments but you’ll pay more in total interest.

- Principal: This is the initial amount of money you borrowed for the car, before interest and fees are added. Your payments slowly chip away at this principal.

Pro tips from us: Always ask for the APR, not just the interest rate. It gives you the most accurate picture of the loan’s cost.

Choosing the Right Used Car: It Impacts Your Loan

The specific used car you choose isn’t just a matter of preference; it also plays a significant role in your ability to secure a loan and the terms you’re offered. Lenders have criteria for the vehicles they’re willing to finance.

Vehicle Age and Mileage Restrictions

Many lenders have policies regarding the age and mileage of used cars they will finance. This is due to the increased risk associated with older or higher-mileage vehicles.

- Age: Some lenders may not finance cars older than 8-10 years.

- Mileage: Similarly, there might be mileage caps, for example, not financing vehicles with over 100,000 or 120,000 miles.

- Impact: If a car falls outside these parameters, you might need to find a specialized lender, put down a larger down payment, or accept a higher interest rate.

Importance of a Pre-Purchase Inspection

Before finalizing any purchase, especially for a used car, a professional pre-purchase inspection (PPI) by an independent mechanic is non-negotiable.

- Why It’s Crucial: A PPI can uncover hidden mechanical issues, safety concerns, or undisclosed damage. These problems could lead to expensive repairs down the road, making your car loan a financial burden.

- Protecting Your Investment: It ensures you’re not financing a money pit. The last thing you want is to be paying off a loan for a car that constantly needs repairs.

Researching Vehicle History

Always obtain a comprehensive vehicle history report. Services like CarFax or AutoCheck provide valuable insights into a car’s past.

- What It Reveals: These reports can show previous accidents, salvage titles, flood damage, odometer rollbacks, and service history.

- Red Flags: A clean title and accident-free history are strong indicators of a reliable vehicle. Be wary of any major red flags found in these reports.

Understanding how to choose a reliable used car is just as important as securing the loan itself. For more detailed advice on selecting the right vehicle, you might want to check out our related guide: (This is a placeholder for an internal link).

Dealer Financing vs. Independent Lenders: Weighing Your Options

When it comes to how to get a used car loan, you’ll generally find yourself choosing between financing directly through the dealership or securing a loan from an independent lender (bank, credit union, online). Each path has its own set of pros and cons.

Dealer Financing

Pros:

- Convenience: You can complete the entire car-buying and financing process in one location, often on the same day.

- Special Offers: Dealerships sometimes offer special financing rates or incentives, especially on certified pre-owned vehicles.

- Flexibility: Dealers work with multiple lenders, potentially finding options for borrowers with varying credit scores.

Cons:

- Potentially Higher Rates: While convenient, dealer financing doesn’t always guarantee the best rates. Their offers might be marked up to generate profit.

- Limited Options: You’re usually limited to the lenders the dealership partners with, which might not include every competitive offer available.

- Focus on Payments: Salespeople might focus on the monthly payment, distracting you from the overall cost of the loan (APR, total interest).

Independent Lenders (Banks, Credit Unions, Online Lenders)

Pros:

- Often Better Rates: Banks and especially credit unions often provide highly competitive interest rates, particularly for well-qualified borrowers.

- Pre-Approval Power: Getting pre-approved gives you leverage and a clear budget before you step onto the car lot.

- Established Relationships: If you have an existing banking relationship, they might offer you better terms due to your history.

- Comparison Shopping: Online lenders make it easy to compare multiple offers quickly and efficiently.

Cons:

- Less Convenient: You’ll need to handle the financing separately from the car purchase, which requires an extra step.

- Time-Consuming: The application and approval process can sometimes take longer than in-dealership financing.

Pro tips from us: Always get a pre-approval from an independent lender first. This gives you a benchmark. Then, if the dealer offers you a better rate, great! If not, you have your pre-approved loan ready. For comparing various loan offers and understanding your rights as a consumer, a trusted external source like the Consumer Financial Protection Bureau (CFPB) offers excellent resources: https://www.consumerfinance.gov/consumer-tools/auto-loans/ (This is a placeholder for an external link).

Special Situations: Getting a Used Car Loan with Challenges

Not everyone has a pristine credit history or a hefty down payment saved up. If you’re facing challenges like bad credit or no credit history, getting a used car loan might seem impossible, but it’s not. There are specific strategies and options available.

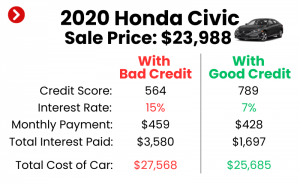

Getting a Used Car Loan with Bad Credit

Having a low credit score (typically below 600-620) doesn’t automatically disqualify you from getting a used car loan, but it will likely mean higher interest rates and stricter terms.

- Co-Signers: A co-signer with good credit can significantly improve your chances of approval and secure a better interest rate. Their credit history effectively backs your loan.

- Secured Loans: Some lenders offer secured auto loans, where you might pledge collateral (like savings) to reduce their risk.

- Subprime Lenders: These lenders specialize in working with borrowers who have lower credit scores. While they can provide access to financing, be prepared for much higher interest rates.

- Higher Down Payment: A substantial down payment reduces the loan amount and signals to lenders that you’re committed, offsetting some of the risk associated with bad credit.

- Focus on Improving Credit First: If possible, dedicate a few months to improving your credit score before applying. Pay down debts, make payments on time, and dispute errors. Even a small improvement can make a difference.

Used Car Loans with No Credit History

If you’re new to borrowing, perhaps a recent graduate or new immigrant, you might have no credit history. This is different from bad credit, but still presents a challenge as lenders have no data to assess your risk.

- Similar Strategies: Co-signers and a larger down payment are still effective strategies.

- Proof of Income and Stability: Lenders will heavily rely on your stable income, employment history, and residence history to gauge your reliability.

- Small, Secured Loan First: Consider taking out a small, secured loan or a secured credit card to start building a positive credit history before applying for an auto loan.

Financing Private Party Sales

If you’re buying a used car from a private seller instead of a dealership, the financing process differs slightly. Many traditional lenders are hesitant to finance private sales due to the lack of dealer vetting and warranties.

- Specialized Lenders: Some banks and credit unions do offer private party auto loans, but you might need to search specifically for them.

- Pre-Approval is Key: Get pre-approved for a specific amount. The lender will often require an appraisal of the vehicle to ensure its value matches the loan amount.

- Vehicle Inspection: A pre-purchase inspection is even more critical for private sales as you don’t have a dealership’s reputation to fall back on.

The Final Stretch: Understanding Your Loan Offer

Once you’ve been approved, the final step is to carefully review and understand the loan agreement. This is where you finalize the terms and commit to repayment.

Scrutinizing the Loan Agreement

Do not rush through the paperwork. Take your time to read every line of the loan contract.

- Verify Key Terms: Ensure the APR, loan term, monthly payment, and total loan amount match what you were offered and agreed upon.

- Check for Fees: Look for any unexpected fees, such as origination fees, document fees, or prepayment penalties.

- Understand the Fine Print: Pay attention to clauses regarding late payments, default, and repossession.

Beware of Hidden Fees and Add-Ons

Salespeople might try to bundle additional products or services into your loan, often without fully explaining their impact on your overall cost.

- Extended Warranties: While some can be valuable, others are overpriced. Understand what they cover and if you truly need them.

- GAP Insurance: This covers the difference between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen. It can be useful, especially if you have a low down payment, but compare prices from your auto insurer first.

- Credit Life/Disability Insurance: These pay off your loan if you die or become disabled. They are often optional and might be more expensive than similar coverage elsewhere.

Pro tips from us: Always ask for an itemized breakdown of all costs. If you don’t understand something, ask for clarification. Never feel pressured to sign until you are completely comfortable with every aspect of the agreement.

Conclusion: Drive Away with Confidence

Congratulations! You’ve just navigated the comprehensive landscape of how to get a used car loan. From understanding the nuances of used car financing to sharpening your financial profile, securing pre-approval, and carefully reviewing your loan offer, you are now equipped with the knowledge to make an informed decision. Remember, patience, preparation, and careful comparison are your most valuable assets in this process.

Getting a used car loan doesn’t have to be a stressful ordeal. By following the steps outlined in this guide, you can confidently approach lenders, negotiate effectively, and secure a loan that sets you up for financial success. Drive away in your used car with the peace of mind that comes from making a smart, well-researched financial choice.

Ready to find your perfect ride and the perfect loan to match? Start by checking your credit, getting pre-approved, and then dive into our other guides for more expert advice on buying and maintaining your vehicle!